MARKET INSIGHTS

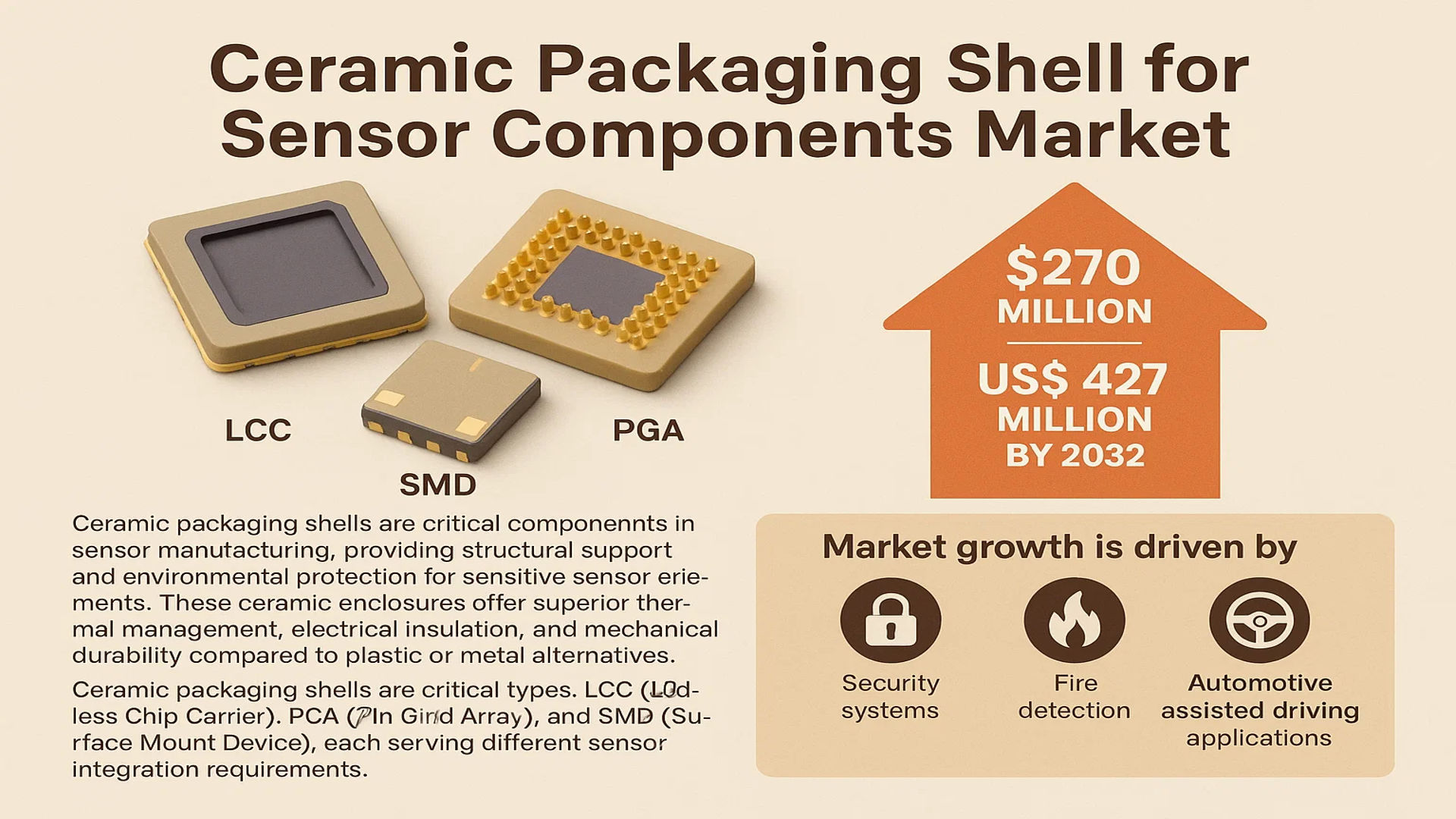

The global Ceramic Packaging Shell for Sensor Components market was valued at 270 million in 2024 and is projected to reach US$ 427 million by 2032, at a CAGR of 6.6% during the forecast period.

Ceramic packaging shells are critical components in sensor manufacturing, providing structural support and environmental protection for sensitive sensor elements. These ceramic enclosures offer superior thermal management, electrical insulation, and mechanical durability compared to plastic or metal alternatives. The market primarily consists of three package types: LCC (Leadless Chip Carrier), PGA (Pin Grid Array), and SMD (Surface Mount Device), each serving different sensor integration requirements.

Market growth is driven by increasing adoption in security systems, fire detection, and automotive assisted driving applications where reliability is paramount. While North America currently leads in technological advancements, Asia-Pacific shows the fastest growth due to expanding electronics manufacturing. Key players like Kyocera, NGK Spark Plugs, and Texas Instruments are investing in advanced ceramic formulations to meet rising demand for miniaturized, high-performance sensor packages.

MARKET DYNAMICS

MARKET DRIVERS

Expanding IoT and Smart Device Adoption Accelerates Demand for Ceramic Packaging Shells

The rapid proliferation of IoT-connected devices is creating substantial demand for high-performance sensor components, driving growth in ceramic packaging solutions. The global IoT market is projected to grow at a compound annual rate exceeding 15% through 2030, with billions of new connected devices requiring reliable sensor packages. Ceramic shells offer superior protection for sensitive sensor elements in harsh environments while maintaining excellent thermal conductivity and electrical insulation properties. This makes them particularly valuable for industrial IoT applications where components must withstand extreme temperatures, vibrations, and corrosive conditions while maintaining precision measurements.

Automotive Sector Transformation Creates New Applications

Automotive electrification and autonomous driving technologies are significantly expanding the sensor packaging market. Modern vehicles now incorporate hundreds of sensors for engine management, safety systems, and driver assistance features. The shift toward electric vehicles (EVs) is particularly impactful, as EV battery management systems require precise temperature monitoring sensors in high-voltage environments where ceramic packaging’s electrical properties are essential. Additionally, advanced driver-assistance systems (ADAS) rely on ceramic-packaged LiDAR and radar sensors that must maintain performance across temperature extremes from -40°C to +125°C.

➤ Sensor-rich autonomous vehicles currently use over 50% more ceramic-packaged components compared to traditional vehicles, a gap projected to widen as automation levels increase.

Furthermore, regulatory mandates for improved vehicle safety across multiple regions are accelerating adoption of ceramic-packaged impact and proximity sensors, creating sustained market demand.

MARKET CHALLENGES

Precision Manufacturing Requirements Increase Production Complexity

While ceramic packaging offers numerous advantages, the manufacturing process presents significant technical challenges. Producing defect-free ceramic shells with precise dimensional tolerances often below 10 microns requires specialized equipment and extensive quality control measures. The sintering process, where ceramic materials are compacted under high temperatures, frequently generates microscopic cracks or warping that can compromise sensor performance. Industry data indicates approximately 8-12% of ceramic packages fail initial quality inspections due to manufacturing defects, creating yield challenges that impact production costs.

Other Challenges

Material Science Limitations

Current ceramic formulations face trade-offs between thermal performance, mechanical strength, and cost-effectiveness. While alumina offers excellent electrical insulation, its thermal conductivity lags behind more expensive materials like aluminum nitride. Developing ceramic composites that balance these properties without dramatically increasing production costs remains an ongoing challenge for material scientists.

Miniaturization Pressures

The industry-wide push toward smaller sensor packages creates mounting challenges for ceramic solutions. As package sizes shrink below 5mm x 5mm, maintaining hermetic sealing and mechanical stability becomes increasingly difficult while still accommodating necessary electrical interconnects. These constraints often force manufacturers to choose between performance and miniaturization objectives.

MARKET RESTRAINTS

Competition from Alternative Packaging Technologies Limits Growth Potential

While ceramic packaging remains dominant for high-reliability applications, emerging plastic and composite solutions are eroding its market share in cost-sensitive segments. Advanced engineering plastics now achieve sufficient thermal stability for many consumer IoT applications at 30-50% lower costs than ceramic alternatives. However, these materials still cannot match ceramic’s performance in extreme environments or high-frequency applications where signal integrity is paramount.

Additionally, the relatively long lead times for ceramic component production – typically 8-12 weeks compared to 2-4 weeks for plastic alternatives – creates supply chain challenges that discourage adoption in fast-moving product segments. This timing disadvantage is particularly noticeable in consumer electronics, where product lifecycles continue to accelerate.

MARKET OPPORTUNITIES

Emerging 5G Infrastructure Buildout Offers Significant Growth Potential

The global rollout of 5G networks presents a major opportunity for ceramic-packaged RF sensors and components. 5G base stations require highly reliable packaging solutions that can protect sensitive millimeter-wave components from environmental factors while maintaining precise electrical characteristics. Ceramic packaging’s unique combination of high-frequency performance and environmental resistance makes it ideal for these demanding applications. Industry projections suggest the 5G infrastructure market will generate over 25% of ceramic package demand growth through 2030.

Medical Device Innovations Drive Specialty Packaging Requirements

The medical sensor market is increasingly adopting ceramic packaging for implantable devices and diagnostic equipment. Ceramic’s biocompatibility, coupled with its ability to maintain sterility through hermetic sealing, makes it particularly valuable for next-generation medical technologies. Emerging applications like continuous glucose monitoring systems and neurostimulation devices are creating demand for miniaturized ceramic packages that can withstand bodily fluids while providing long-term reliability. Additionally, the growing medical IoT sector requires sensor packages that combine wireless connectivity with medical-grade durability—a combination that ceramic solutions are uniquely positioned to provide.

Increased Adoption of Miniaturized Sensor Technologies Drives Ceramic Packaging Demand

The global ceramic packaging shell market for sensor components is experiencing significant growth due to the rising adoption of miniaturized sensor technologies across industries. As sensors become smaller and more sophisticated, ceramic packaging provides critical advantages in thermal stability, electrical insulation, and mechanical protection. The market size for ceramic sensor packaging reached $270 million in 2024 and is projected to grow at a steady 6.6% CAGR through 2032. While traditional packaging materials struggle with heat dissipation in compact designs, advanced ceramics maintain performance even in harsh environments, making them indispensable for modern sensor applications.

Other Trends

Growth in Automotive ADAS Applications

Advancements in automotive assisted driving systems (ADAS) are creating substantial demand for robust sensor packaging solutions. Ceramic shells protect sensitive LiDAR, radar, and ultrasonic sensors from vibration, moisture, and extreme temperatures – critical factors in vehicle safety systems. With the automotive sector accounting for over 30% of ceramic packaging demand, manufacturers are developing specialized solutions to meet stricter industry standards for reliability and durability. This trend aligns with the projected tripling of ADAS sensor deployments by 2030.

Expansion of Industrial IoT and Smart Infrastructure

The rapid growth of Industrial Internet of Things (IIoT) applications is driving innovation in sensor packaging requirements. Ceramic materials excel in industrial environments where sensors face corrosive chemicals, pressure variations, and electromagnetic interference. Recent developments include multi-layer ceramic packages with integrated signal conditioning for smart factory equipment. As industrial automation investments increase globally, the need for reliable sensor packaging in predictive maintenance and process monitoring systems continues to accelerate. Manufacturers are responding with customized ceramic solutions featuring enhanced thermal conductivity and hermetic sealing properties.

COMPETITIVE LANDSCAPE

Key Industry Players

Innovation and Strategic Expansion Define the Competitive Edge in Ceramic Sensor Packaging

The global ceramic packaging shell for sensor components market features a dynamic competitive environment with prominent manufacturers leveraging technological advancements and regional expansions to gain market share. Kyocera and Schott currently dominate the landscape, capturing a combined revenue share of approximately 25% as of 2024. Their leadership stems from decades of expertise in ceramic materials and strategic partnerships with automotive and industrial sensor manufacturers.

While Japanese players like NTK Ceramic and MARUWA maintain strong positions in Asia-Pacific markets, U.S.-based companies such as Materion and Texas Instruments are expanding their production capacities to meet growing demand from North American military and aerospace sectors. This geographical diversification creates both competition and collaboration opportunities across value chains.

The market has witnessed significant R&D investments in recent years, particularly in developing multi-layer ceramic packages capable of withstanding extreme temperatures exceeding 300°C. Ceramtec Group recently launched its HTCC (High-Temperature Co-fired Ceramic) series, strengthening its position in industrial and automotive applications. Meanwhile, Chinese manufacturers like SHENGDA TECHNOLOGY are gaining traction through cost-competitive solutions for consumer electronics sensors.

List of Key Ceramic Packaging Shell Manufacturers

- Kyocera Corporation (Japan)

- Schott AG (Germany)

- Materion Corporation (U.S.)

- NTK Ceramic (Japan)

- Texas Instruments (U.S.)

- MARUWA Co., Ltd. (Japan)

- Ceramtec Group (Germany)

- KOA Corporation (Japan)

- NGK Spark Plugs (Japan)

- Tensky International (Taiwan)

- AMETEK, Inc. (U.S.)

- AdTech Ceramics (U.S.)

- Alumina Systems GmbH (Germany)

- SHENGDA TECHNOLOGY (China)

- CCTC (China)

Emerging companies are adopting niche strategies, with Alumina Systems GmbH focusing on medical sensor packaging and AMETEK targeting the defense sector. The competitive landscape continues evolving as manufacturers balance between high-performance solutions for critical applications and cost-effective packages for mass-market sensors.

Segment Analysis:

By Type

LCC Type Segment Leads the Market Owing to Superior Thermal and Electrical Performance

The market is segmented based on type into:

- LCC Type

- Subtypes: Hermetic LCC, Non-hermetic LCC

- PGA Type

- SMD Type

- Others

By Application

Automotive Industry Dominates Due to Increasing Sensor Integration in Vehicles

The market is segmented based on application into:

- Automotive Industry

- Consumer Electronics

- Industrial Automation

- Medical Devices

- Others

By Material

Alumina Oxide Ceramics Hold Majority Share for Their Excellent Mechanical Properties

The market is segmented based on material into:

- Alumina Oxide Ceramics

- Aluminum Nitride Ceramics

- Zirconia Ceramics

- Others

By End User

Original Equipment Manufacturers Drive Demand for Customized Solutions

The market is segmented based on end user into:

- Original Equipment Manufacturers

- Aftermarket Suppliers

- System Integrators

- Research Institutions

Regional Analysis: Ceramic Packaging Shell for Sensor Components Market

Asia-Pacific

The Asia-Pacific region dominates the global ceramic packaging shell market, accounting for over 45% of total revenue in 2024. China leads regional demand due to its massive electronics manufacturing sector and government initiatives like Made in China 2025, which prioritizes advanced sensor technologies. Japan follows closely as a technology leader, with companies like Kyocera and NGK Spark Plugs driving innovation in high-performance ceramic packaging. While cost-competitive solutions dominate the market, there’s growing emphasis on reliability for automotive and industrial applications. India’s market is expanding rapidly due to increasing electronics production and security system installations.

North America

North America maintains strong demand for premium ceramic packaging solutions, particularly for military, aerospace, and medical sensor applications. The U.S. accounts for approximately 28% of regional market value, with companies like Materion and Texas Instruments leading development of specialized packaging. Strict quality standards and the need for extreme environmental durability drive adoption of advanced ceramic materials. Canada’s market is smaller but growing steadily, supported by investments in IoT infrastructure and smart city projects requiring robust sensor protection.

Europe

Europe’s market is characterized by stringent technical requirements and environmental regulations governing electronic components. Germany is the largest consumer, with its strong automotive and industrial automation sectors demanding high-reliability ceramic packages. Manufacturers like Schott and Ceramtec Group focus on developing eco-friendly production processes while maintaining performance standards. The region shows particular strength in PGA-type packaging for precision measurement applications. Eastern European markets are emerging as cost-effective manufacturing hubs for standard-grade ceramic packages.

Middle East & Africa

This region represents a developing market for ceramic sensor packaging, with growth concentrated in oil/gas and security applications. The UAE and Saudi Arabia are key markets, investing heavily in infrastructure monitoring systems. Local production remains limited, creating opportunities for international suppliers. Challenges include price sensitivity and preference for alternative materials in less demanding applications. However, harsh environmental conditions in many areas are gradually increasing acceptance of ceramic solutions for critical sensor protection.

South America

South America’s market faces slower growth due to economic volatility and limited local manufacturing capabilities. Brazil accounts for over half of regional demand, primarily serving its automotive and industrial sectors. Argentina shows potential in medical sensor applications but struggles with import dependency. While ceramic packaging adoption grows in premium applications, many cost-sensitive industries continue using plastic alternatives. Investments in modernizing infrastructure could drive future demand for more durable sensor protection solutions.

Report Scope

This market research report provides a comprehensive analysis of the Global Ceramic Packaging Shell for Sensor Components Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 270 million in 2024 and is projected to reach USD 427 million by 2032, growing at a CAGR of 6.6%.

- Segmentation Analysis: Detailed breakdown by product type (LCC, PGA, SMD), application (Security, Firefighting, Automotive, Military), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis for key markets like the U.S., China, Japan, and Germany.

- Competitive Landscape: Profiles of 21 leading manufacturers including Kyocera, Schott, Ceramtec Group, and NGK Spark Plugs, covering their market share (top 5 held ~% in 2024), product portfolios, and strategic developments.

- Technology Trends: Assessment of advanced ceramic materials, miniaturization trends, thermal management solutions, and integration with IoT/automotive sensors.

- Market Drivers & Restraints: Analysis of growth drivers (automotive ADAS expansion, industrial IoT adoption) and challenges (raw material price volatility, supply chain complexities).

- Stakeholder Analysis: Strategic insights for sensor manufacturers, material suppliers, packaging solution providers, and investors.

The research employs primary interviews with industry leaders and analysis of financial reports, trade data, and manufacturing trends to ensure data accuracy.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Ceramic Packaging Shell for Sensor Components Market?

->Ceramic Packaging Shell for Sensor Components market was valued at 270 million in 2024 and is projected to reach US$ 427 million by 2032, at a CAGR of 6.6% during the forecast period.

Which key companies operate in this market?

-> Leading players include Kyocera, Schott, Ceramtec Group, NGK Spark Plugs, Materion, and Texas Instruments, with the top 5 holding approximately % market share in 2024.

What are the key growth drivers?

-> Growth is driven by rising demand for automotive sensors (especially ADAS), industrial IoT expansion, and increasing military/defense applications requiring robust packaging solutions.

Which region dominates the market?

-> Asia-Pacific leads in both market share and growth rate, fueled by sensor manufacturing in China, Japan, and South Korea, while North America remains strong in high-value applications.

What are the emerging trends?

-> Key trends include development of ultra-thin ceramic packages, integration of advanced thermal interfaces, and adoption of alumina-based solutions for harsh environments.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...