MARKET INSIGHTS

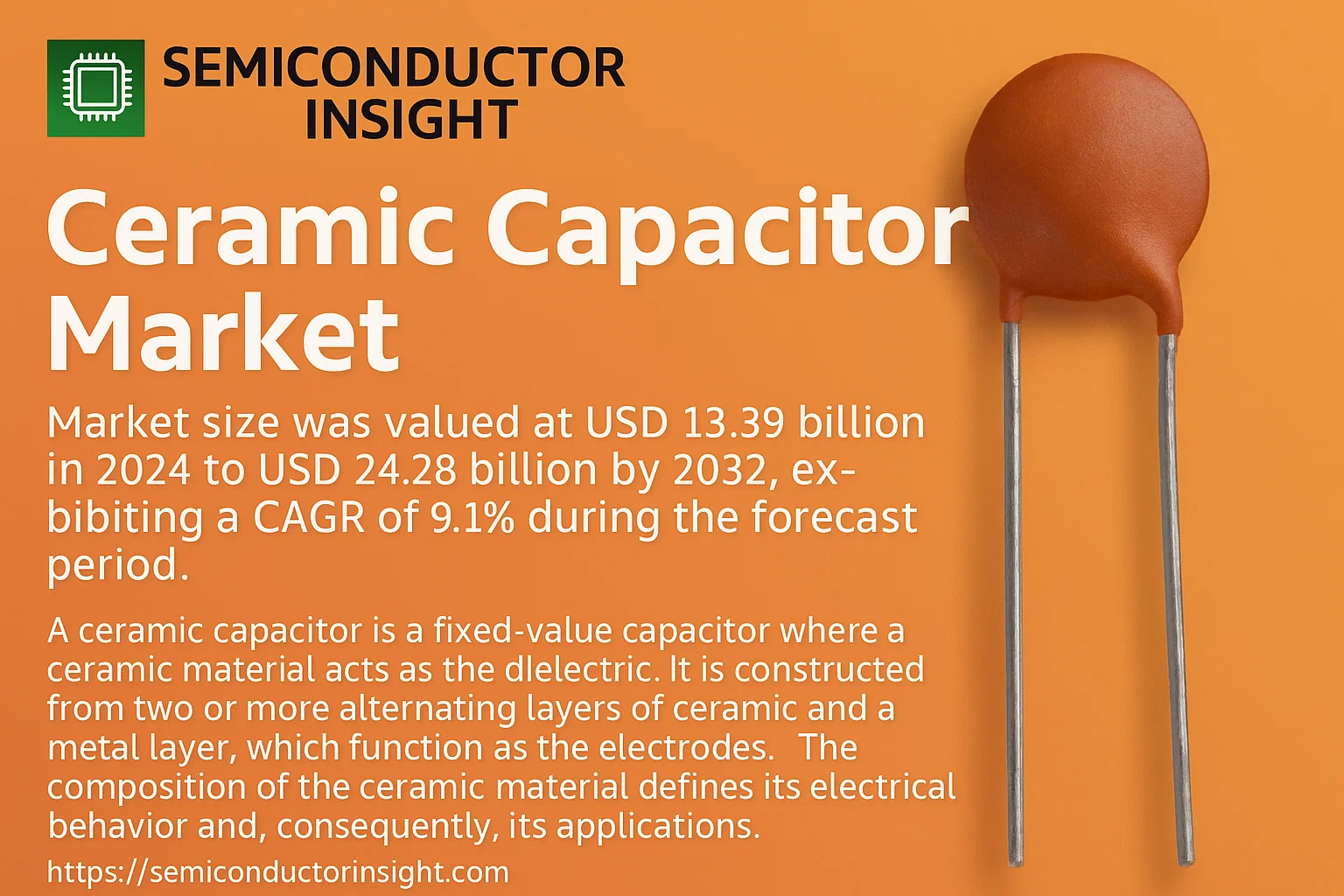

Global Ceramic Capacitor Market size was valued at USD 13.39 billion in 2024 to USD 24.28 billion by 2032, exhibiting a CAGR of 9.1% during the forecast period.

A ceramic capacitor is a fixed-value capacitor where a ceramic material acts as the dielectric. It is constructed from two or more alternating layers of ceramic and a metal layer, which function as the electrodes. The composition of the ceramic material defines its electrical behavior and, consequently, its applications.

The market is experiencing robust growth driven by several key factors, including the expanding production of consumer electronics, the rapid adoption of electric vehicles (EVs), and the global rollout of 5G infrastructure. Furthermore, increasing demand for advanced driver-assistance systems (ADAS) in automobiles and ongoing miniaturization of electronic components are contributing significantly to market expansion. Initiatives by key players are also expected to fuel growth; for instance, manufacturers are heavily investing in R&D to develop high-capacitance, miniaturized multilayer ceramic chip capacitors (MLCCs) to meet evolving industry demands. Murata Manufacturing Co., Ltd., Samsung Electro-Mechanics, and TDK Corporation are some of the key players that operate in the market with a wide range of portfolios.

MARKET DRIVERS

Proliferation of Electronics and Miniaturization

Global Ceramic Capacitor Market is primarily driven by the explosive growth in consumer electronics, telecommunications, and automotive electronics. The demand for smaller, more efficient, and higher-capacitance components is relentless. The trend towards miniaturization in devices like smartphones, wearables, and IoT sensors directly fuels the need for multilayer ceramic capacitors (MLCCs), which offer excellent performance in compact sizes. This is compounded by the increasing electronic content in modern vehicles, including advanced driver-assistance systems (ADAS) and infotainment systems.

Transition to 5G and Expansion of Infrastructure

Global rollout of 5G technology represents a significant driver. 5G infrastructure, including base stations and network equipment, requires a substantial number of high-frequency, high-reliability ceramic capacitors. Furthermore, the proliferation of 5G-enabled devices is creating sustained demand. The market is also bolstered by investments in renewable energy sectors and industrial automation, where ceramic capacitors are essential for power conditioning and noise suppression.

The push for greater energy efficiency across all electronic applications ensures that ceramic capacitors, known for their low equivalent series resistance (ESR) and high ripple current capability, remain the component of choice. This sustained demand from multiple high-growth industries underpins the market’s positive trajectory.

MARKET CHALLENGES

Supply Chain Volatility and Raw Material Constraints

The Ceramic Capacitor Market has been susceptible to significant supply chain disruptions. Key raw materials, such as base metal electrodes (BME) like nickel and precious metals like palladium and silver used in some formulations, are subject to price volatility and geopolitical supply risks. Manufacturing capacitors is a complex process, and capacity expansions require substantial capital investment and long lead times, making it difficult to quickly respond to demand surges, leading to periodic shortages and extended delivery times for certain product types.

Other Challenges

Pricing Pressure and Intense Competition

The market is highly competitive, particularly for commodity-type MLCCs, leading to persistent price pressure that squeezes manufacturer margins. This is exacerbated by the need for continuous technological innovation to meet evolving performance requirements.

Technical Limitations at High Voltages and Capacitances

While excellent for many applications, ceramic capacitors face challenges in applications requiring very high capacitance values or extremely high voltage ratings, where alternative technologies like tantalum or aluminum electrolytic capacitors may be preferred due to limitations related to dielectric materials and the piezoelectric effect.

MARKET RESTRAINTS

Economic Sensitivity and Cyclical Demand

The Ceramic Capacitor Market is inherently tied to the health of the global economy and its core end markets, such as consumer electronics and automotive. Economic downturns or slowdowns in these sectors can lead to rapid declines in orders and an accumulation of inventory, creating a boom-and-bust cycle that restrains stable, long-term growth planning for manufacturers.

Complexity in High-Frequency Applications

As electronic systems operate at increasingly higher frequencies, the performance of ceramic capacitors can be affected by parasitic effects like equivalent series inductance (ESL). Designing capacitors that maintain stable capacitance and low losses at gigahertz frequencies requires advanced materials and sophisticated designs, which increases complexity and cost, acting as a restraint for some high-end applications.

MARKET OPPORTUNITIES

Electric and Autonomous Vehicles

The transformation of the automotive industry presents a massive opportunity. The electrification of powertrains and the development of autonomous driving systems require an exponential increase in the number and quality of electronic components. Ceramic capacitors are critical for power electronics, safety systems, and sensors, with content per vehicle expected to grow significantly over the next decade, creating a large and sustained demand pipeline.

Advanced MLCCs for Next-Generation Electronics

There is a significant opportunity in developing and manufacturing advanced MLCCs with higher capacitance densities, better temperature stability (e.g., X8R, X9M dielectrics), and smaller case sizes (e.g., 008004, 01005). These next-generation components are essential for the continued miniaturization and performance enhancement of premium smartphones, high-performance computing, and advanced medical devices, representing a high-value segment of the market.

Expansion in Renewable Energy and Industrial IoT

Global push for sustainability drives growth in renewable energy systems like solar and wind power, where ceramic capacitors are used in inverters and converters. Simultaneously, the Industrial Internet of Things (IIoT) and factory automation rely on robust, reliable capacitors for control systems and sensor networks. These industrial and energy applications offer opportunities for high-reliability, long-lifecycle products.

Ceramic Capacitor Market Trends

Sustained Market Expansion Driven by Advanced Electronics Demand

Global Ceramic Capacitor Market demonstrates robust and sustained growth, with a valuation of USD 13.39 billion in 2024 and a projected expansion to USD 24.28 billion by 2032, representing a compound annual growth rate (CAGR) of 9.1%. A ceramic capacitor is a fixed-value capacitor where ceramic material acts as the dielectric, constructed from alternating layers of ceramic and metal electrodes. This essential electronic component is a cornerstone of modern technology due to its non-polarized nature and excellent frequency response, making it suitable for AC sources and high-frequency applications. The primary driver of this market trend is the insatiable global demand for smaller, more efficient, and more powerful electronic devices across all sectors.

Other Trends

Regional Market Dominance Shifts

Geographic market concentration is a notable trend, with China emerging as the dominant force, accounting for approximately 36% of the global market share. Japan follows as a significant player with about 13% market share. This concentration reflects the established supply chains and manufacturing capabilities in the Asia-Pacific region, which serves as the global hub for electronics production. The trend highlights the importance of these regions for both supply and consumption, influencing global pricing and availability.

Consolidation Among Key Industry Players

The competitive landscape is characterized by a high degree of consolidation. The top three companies—Murata, Samsung Electro, and TDK Corporation—collectively occupy about 61% of the total market share. This concentration indicates a mature market where technological expertise, economies of scale, and strong customer relationships are critical for maintaining a competitive edge. Other key players include Kyocera, Vishay, Yageo, and Walsin, all competing through innovation and specialization in different capacitor types and applications.

Segmentation Dynamics and Application Growth

Market segmentation reveals clear trends in application and product type. By type, Multilayer Ceramic Chip Capacitors (MLCCs) represent the most significant segment due to their miniaturization capabilities and high performance. In terms of application, demand is strongest from the consumer electronics, automotive, and communications equipment sectors. The automotive industry, in particular, is a major growth area, with the increasing electrification of vehicles and the integration of advanced driver-assistance systems (ADAS) requiring a higher volume of reliable ceramic capacitors. These application-specific demands continue to shape product development and market strategy for leading manufacturers.

COMPETITIVE LANDSCAPE

Key Industry Players

A Market Dominated by a Few Major Players with Strong Regional Presence

Global Ceramic Capacitor Market is characterized by a high level of concentration, with the top three players—Murata, Samsung Electro-Mechanics, and TDK Corporation—collectively accounting for approximately 61% of the market share. This dominant position is built on their extensive technological expertise, massive production capacities, and strong relationships with global electronics manufacturers. These companies lead innovation in product miniaturization, reliability, and performance, particularly for high-demand applications like consumer electronics and automotive electronics. The competitive dynamics are further shaped by regional strengths, with China being the largest market and manufacturing hub, representing about 36% of global share.

Beyond the dominant leaders, a significant number of other companies compete in specific niches, geographic regions, or product segments. These players, including Kyocera (AVX), Vishay, and Yageo, often focus on specialized capacitor types, such as high-voltage or high-frequency variants, or cater to specific regional markets. Companies like Walsin Technology and Fenghua Advanced Technology have established strong positions within the Asia-Pacific region. The competitive landscape also includes specialized manufacturers like KEMET (now part of Yageo) known for robust components and niche players like Holy Stone and Three-Circle that serve targeted industrial applications, ensuring a diverse and multi-layered market structure.

List of Key Ceramic Capacitor Companies Profiled

- Murata Manufacturing Co., Ltd.

- Samsung Electro-Mechanics

- TDK Corporation

- Kyocera Corporation (AVX)

- Vishay Intertechnology, Inc.

- Samwha Capacitor

- Yageo Corporation (KEMET)

- Japan Display Inc. (JDI)

- NIC Components Corp.

- Walsin Technology Corporation

- Darfon Electronics Corporation

- Holy Stone Enterprise Co., Ltd.

- Fenghua Advanced Technology Holding Co., Ltd.

- EYANG Technology Development Co., Ltd.

- Torch Electron

- Three-Circle (Group) Co., Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Multilayer Ceramic Chip Capacitor (MLCC) dominates the market due to its extremely compact size, excellent frequency response, and superior reliability, making it the preferred choice for high-density circuit boards in modern electronics. The prevalence of miniaturization trends across all electronic devices provides a powerful, sustained driver for this segment’s growth. Its versatility allows it to serve a broad range of capacitance values and voltage ratings within a single, standardized package format. |

| By Application |

|

Consumer Electronics Products represent the leading application segment, driven by the sheer volume of devices like smartphones, tablets, laptops, and televisions produced annually. The insatiable demand for smaller, more powerful, and feature-rich consumer gadgets necessitates a high number of reliable passive components per device. This segment’s growth is intrinsically linked to consumer purchasing trends, product innovation cycles, and the global expansion of the middle class, creating a vast and dynamic market for ceramic capacitors. |

| By End User |

|

Original Equipment Manufacturers (OEMs) are the primary end users, as they integrate ceramic capacitors directly into their final products. Large OEMs, particularly in the consumer electronics and automotive sectors, exert significant influence on market dynamics through their high-volume purchasing power and stringent quality requirements. Their demand is driven by new product launches and production forecasts, making them the most critical direct channel for capacitor suppliers. Building strong, reliable partnerships with major OEMs is a key strategic objective for leading manufacturers in the market. |

| By Dielectric Material |

|

Class 2 (High Permittivity) dielectric materials lead the market, as they enable the manufacturing of capacitors with high volumetric efficiency, which is essential for miniaturization. These materials are the backbone of the ubiquitous MLCCs used in decoupling, bypassing, and filtering applications where stable capacitance over a wide temperature range is less critical than achieving high capacitance in a small footprint. Their cost-effectiveness for general-purpose applications makes them the workhorse dielectric for the mass production of electronic goods. |

| By Voltage Range |

|

Low Voltage capacitors are the leading segment, driven by their extensive use in all portable and low-power digital electronics, including computing, communication, and consumer devices. The vast majority of integrated circuits and microprocessors operate at low voltages, requiring stable and reliable decoupling and filtering solutions. This segment benefits from the highest production volumes and continuous innovation aimed at reducing size and equivalent series resistance (ESR) to meet the power integrity demands of increasingly complex and power-hungry chips. |

Regional Analysis: Ceramic Capacitor Market

Asia-Pacific’s dominance stems from its unparalleled manufacturing infrastructure, with China being the largest producer of MLCCs globally. The region offers economies of scale, extensive raw material availability, and a highly skilled workforce, creating a resilient and efficient supply chain that serves both local and international markets.

Demand is primarily fueled by the massive consumer electronics industry, including smartphones, laptops, and televisions. Additionally, growth is accelerating from the automotive sector’s shift toward electric vehicles and advanced driver-assistance systems (ADAS), which require a high volume of reliable, temperature-stable ceramic capacitors.

The region is a center for R&D, with Japanese and Korean companies leading advancements in capacitor technology. Innovations focus on developing capacitors with higher capacitance values, smaller form factors, and improved performance for high-frequency applications in 5G and Internet of Things (IoT) devices.

The market is characterized by intense competition among established giants and emerging players. This competitive environment drives continuous improvement in product quality and cost-efficiency, while also leading to strategic partnerships and expansions to capture growing demand from various end-use industries.

North America

The North American Ceramic Capacitor Market is characterized by strong demand from the aerospace, defense, and telecommunications sectors. The region’s focus is on high-reliability, high-performance components that meet stringent quality and certification standards. The presence of leading technology companies and a robust automotive industry, particularly with the push towards electrification, sustains demand. While manufacturing within the region is significant, it also relies on imports from Asia-Pacific, with a growing emphasis on securing resilient and diversified supply chains to mitigate geopolitical and trade-related risks.

Europe

Europe holds a significant share of the Ceramic Capacitor Market, driven by its advanced automotive industrial base and strong focus on industrial automation and renewable energy. German and French automotive manufacturers, in particular, are major consumers of high-quality MLCCs for vehicle electrification and sophisticated electronic control units. The region’s stringent environmental regulations also push demand for capacitors used in energy-efficient applications. European market players are known for their specialization in high-value, niche products, often focusing on quality and reliability over high-volume, low-cost production.

p>South America

The South American market for ceramic capacitors is emerging, with growth primarily linked to the increasing adoption of consumer electronics and gradual industrial automation. Brazil is the largest market in the region, though overall demand is modest compared to global leaders. Market development is often constrained by economic volatility and less mature electronics manufacturing infrastructure. However, opportunities exist in the telecommunications sector as network expansions proceed, creating a slowly growing but consistent demand for basic electronic components.

Middle East & Africa

The Middle East & Africa region represents a smaller but growing segment of the global Ceramic Capacitor Market. Growth is largely driven by infrastructure development, particularly in telecommunications and energy sectors within Gulf Cooperation Council (GCC) countries. The increasing penetration of consumer electronics and the gradual push towards industrial diversification also contribute to demand. The market is primarily served by imports, with local manufacturing being limited, presenting potential for future growth as regional industrial capabilities develop.

Report Scope

This market research report provides a comprehensive analysis of the Ceramic Capacitor Market , covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Ceramic Capacitor Market?

-> Ceramic Capacitor Market size was valued at USD 13.39 billion in 2024 to USD 24.28 billion by 2032, exhibiting a CAGR of 9.1% during the forecast period.

Which key companies operate in Ceramic Capacitor Market?

-> Key players include Murata, Samsung Electro, TDK Corporation, Kyocera, Vishay, Samwha, Kemet, JDI, NIC Components, Yageo, Walsin, Darfon, Holy Stone, Fenghua Advanced Technology, EYANG, Torch, Three-Circle, among others. The top 3 companies occupy about 61% of the market share.

What are the key growth drivers?

-> Key growth is driven by increasing demand from key application industries such as automotive, communications equipment, and consumer electronics products.

Which region dominates the market?

-> China is the largest Ceramic Capacitor market, accounting for about 36% of the global market share. Japan is the second-largest market.

What are the emerging trends?

-> Market trends include technological advancements in dielectric materials, miniaturization of components, and the integration of capacitors in advanced electronic systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...