MARKET INSIGHTS

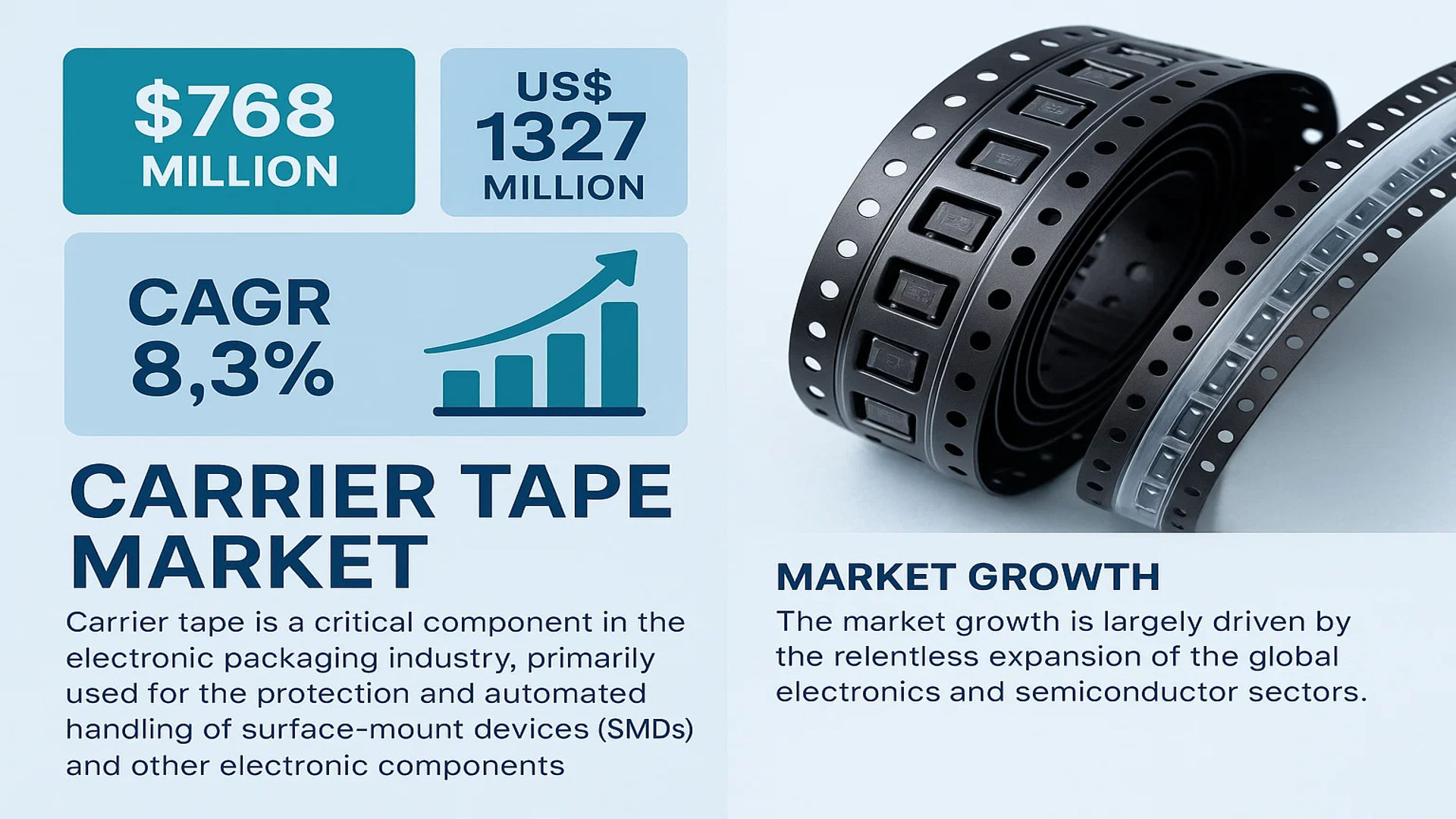

The global Carrier Tape Market was valued at 768 million in 2024 and is projected to reach US$ 1327 million by 2032, at a CAGR of 8.3% during the forecast period.

Carrier Tape is a critical component in the electronic packaging industry, primarily used for the protection and automated handling of surface-mount devices (SMDs) and other electronic components. These tapes feature precisely molded pockets or cavities that securely house components, preventing physical damage, contamination, and electrostatic discharge (ESD) during transportation, storage, and the high-speed automated assembly process on pick-and-place machines. The tape is supplied on reels and is paired with a cover tape that is sealed over the cavities.

The market growth is largely driven by the relentless expansion of the global electronics and semiconductor sectors. The increasing miniaturization of components and the rising adoption of automation in manufacturing necessitate highly reliable and precise packaging solutions like Carrier Tapes. Furthermore, the robust growth in key application segments such as integrated circuits, which command a significant market share, provides a strong foundation for demand. Geographically, Asia-Pacific dominates both production and consumption, with China alone accounting for over 50% of global production, a trend that is expected to continue due to the region’s concentrated electronics manufacturing base.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Electronic Components to Propel Carrier Tape Market Growth

The global electronics industry is experiencing robust expansion, driven by increasing adoption of smart devices, IoT applications, and automotive electronics. This growth directly fuels demand for carrier tapes as essential packaging components for surface-mount devices (SMDs) and integrated circuits. The market for electronic components is projected to grow significantly, with semiconductor sales reaching approximately $600 billion annually, creating substantial demand for protective packaging solutions. Carrier tapes provide critical protection against physical damage, moisture, and electrostatic discharge during transportation and handling, making them indispensable in modern electronics manufacturing. The proliferation of 5G technology, electric vehicles, and industrial automation further accelerates component production, thereby driving carrier tape consumption across global supply chains.

Automation in Electronics Manufacturing to Boost Market Expansion

Automated component placement systems have become standard in electronics manufacturing, requiring precise and reliable component feeding mechanisms. Carrier tapes with standardized dimensions and sprocket holes enable high-speed automated pick-and-place operations, reducing manufacturing time and improving production efficiency. Manufacturers are increasingly adopting advanced automation to maintain competitiveness, with automated assembly lines handling up to 100,000 components per hour. This automation trend necessitates consistent and high-quality carrier tapes that ensure component orientation integrity and feeding reliability. The transition toward Industry 4.0 and smart manufacturing practices further reinforces the need for standardized packaging solutions that integrate seamlessly with automated equipment, creating sustained demand for precision-engineered carrier tapes.

Expansion of Consumer Electronics and Automotive Sectors to Drive Adoption

The consumer electronics market continues to expand with rising disposable incomes and technological innovation, while the automotive sector undergoes rapid transformation through electrification and advanced driver assistance systems (ADAS). Both sectors require increasingly sophisticated electronic components that must be protected during storage and transportation. The automotive electronics market alone is projected to exceed $400 billion by 2030, requiring massive quantities of packaged components. Carrier tapes provide essential protection for sensitive components like sensors, microcontrollers, and power semiconductors that are critical for modern vehicle systems. Similarly, the consumer electronics sector demands reliable packaging for components used in smartphones, wearables, and home appliances, driving consistent growth in carrier tape utilization across multiple applications.

MARKET RESTRAINTS

Environmental Regulations and Sustainability Concerns to Limit Market Growth

The carrier tape industry faces increasing pressure from environmental regulations governing plastic usage and waste management. Many regions have implemented strict policies regarding single-use plastics and packaging materials, affecting traditional plastic-based carrier tapes. The European Union’s packaging waste directive and similar regulations in North America and Asia require manufacturers to reduce plastic consumption and improve recyclability. Plastic carrier tapes, which constitute approximately 80% of the market, face particular scrutiny due to their disposable nature and environmental impact. Manufacturers must invest in developing alternative materials and recycling programs, increasing production costs and potentially limiting market growth in environmentally conscious regions.

Volatility in Raw Material Prices to Constrain Market Development

Carrier tape production relies heavily on polymer materials whose prices fluctuate significantly based on petroleum market dynamics and supply chain conditions. Price volatility in raw materials such as polystyrene, polycarbonate, and conductive compounds creates uncertainty in manufacturing costs and profit margins. Recent supply chain disruptions have exacerbated price instability, with polymer prices experiencing fluctuations of up to 40% within short periods. This volatility forces manufacturers to either absorb cost increases or pass them to customers, potentially making carrier tapes less competitive against alternative packaging solutions. The situation is particularly challenging for smaller manufacturers with limited purchasing power and hedging capabilities, potentially leading to market consolidation and reduced competition.

MARKET CHALLENGES

Technical Complexity in Miniaturized Component Packaging to Challenge Manufacturers

The ongoing trend toward electronic component miniaturization presents significant technical challenges for carrier tape manufacturers. As components shrink to microscopic dimensions, carrier tapes must maintain precise cavity dimensions, often requiring tolerances within micrometers. Manufacturing these precision tapes demands advanced tooling, strict quality control, and specialized materials that can maintain dimensional stability under varying environmental conditions. The development of tapes for components smaller than 01005 size package (0.4mm x 0.2mm) requires investment in precision engineering capabilities that many manufacturers lack. This technical barrier limits the number of suppliers capable of producing advanced carrier tapes, potentially creating supply bottlenecks for cutting-edge electronic components.

Other Challenges

Supply Chain Disruptions

Global supply chain vulnerabilities have exposed the carrier tape industry to significant operational challenges. The concentration of manufacturing in specific regions, coupled with logistics bottlenecks, has created delivery delays and inventory management difficulties. The electronics industry’s just-in-time manufacturing approach amplifies these challenges, as any disruption in carrier tape supply can halt production lines. Recent global events have demonstrated how quickly supply chain issues can affect availability, with lead times for certain carrier tape types extending from weeks to several months during peak disruptions.

Standardization Issues

While international standards exist for carrier tape dimensions, variations in customer requirements and regional specifications create manufacturing complexities. Different component manufacturers may require slight modifications to standard tape designs, forcing carrier tape producers to maintain multiple production setups and inventory types. This lack of complete standardization increases production costs and reduces manufacturing efficiency, particularly for companies serving global customers with diverse requirements.

MARKET OPPORTUNITIES

Development of Sustainable and Bio-based Materials to Create New Market Opportunities

The growing emphasis on environmental sustainability presents significant opportunities for innovation in carrier tape materials. Development of biodegradable, recycled, and bio-based polymers can address environmental concerns while meeting technical requirements for component protection. Several manufacturers are investing in research and development of polylactic acid (PLA) based tapes and other sustainable alternatives that offer comparable performance to traditional plastics. The market for sustainable packaging solutions is growing rapidly, with environmentally conscious electronics manufacturers increasingly seeking green packaging options. This shift creates opportunities for forward-thinking carrier tape producers to differentiate their products and capture market share in the growing segment of sustainable electronics manufacturing.

Expansion in Emerging Markets to Provide Growth Potential

Emerging economies present substantial growth opportunities for the carrier tape market as electronics manufacturing continues to shift toward these regions. Countries in Southeast Asia, Eastern Europe, and Latin America are experiencing rapid growth in electronics production, driven by favorable manufacturing conditions and growing domestic markets. The establishment of new semiconductor fabrication plants and electronics assembly facilities in these regions creates immediate demand for local packaging solutions. Carrier tape manufacturers can capitalize on this trend by establishing local production facilities, developing regional partnerships, and tailoring products to meet specific regional requirements. This geographical expansion can help companies diversify their customer base and reduce dependence on traditional manufacturing hubs.

Integration of Smart Packaging Technologies to Enable Future Growth

Advancements in smart packaging technologies offer innovative opportunities for carrier tape development. Integration of RFID tags, QR codes, and sensors into carrier tapes can enable improved inventory management, component tracking, and quality control throughout the supply chain. Smart carrier tapes can provide real-time information about component conditions, including exposure to moisture, temperature extremes, or electrostatic discharge events. This enhanced functionality addresses growing industry needs for supply chain transparency and quality assurance, particularly for high-value components. While still in early stages, smart carrier tape technology represents a potential paradigm shift in component packaging that could create new revenue streams and value-added services for innovative manufacturers.

CARRIER TAPE MARKET TRENDS

Miniaturization and High-Density Packaging Driving Demand for Advanced Carrier Tapes

The relentless push towards component miniaturization in the electronics industry is a primary catalyst for innovation within the carrier tape market. As integrated circuits and passive components shrink to sizes below 0201 metric, the precision required for cavity formation and dimensional stability becomes paramount. This trend is directly fueling demand for high-performance plastic core carrier tapes, which offer superior accuracy and protection compared to paper-based alternatives. The global market for plastic core carrier tapes, which currently holds over 80% revenue share, is projected to grow in lockstep with the production of advanced semiconductor packages and micro-electromechanical systems (MEMS). Furthermore, the rise of 5G infrastructure and Internet of Things (IoT) devices, which utilize a high volume of miniature components, necessitates packaging solutions that prevent damage from electrostatic discharge (ESD) during high-speed automated handling. This has led to increased adoption of tapes with specialized static-dissipative and conductive polymers, a segment experiencing a growth rate approximately 2% higher than the overall market average.

Other Trends

Sustainability and Material Innovation

Growing environmental regulations and corporate sustainability initiatives are compelling manufacturers to develop eco-friendly carrier tape solutions. While plastic tapes dominate, there is a significant R&D focus on creating bio-based polymers and recyclable composites that do not compromise on performance. The European Union’s stringent packaging waste directives are particularly influential in this shift, prompting suppliers to explore polylactic acid (PLA) and other biodegradable materials. This is not merely a regulatory response; it is a strategic move to capture value in a market where end-users are increasingly evaluating the environmental footprint of their supply chain. Concurrently, advancements in material science are yielding new polymer blends that offer enhanced clarity for machine vision systems, higher tensile strength for thinner gauges, and improved performance across a wider temperature range, ensuring component integrity from assembly to board mounting.

Automation and Smart Manufacturing Integration

The integration of Industry 4.0 principles into electronics manufacturing is profoundly impacting carrier tape specifications and functionality. Automated assembly lines, which can place over 100,000 components per hour, require flawless tape feed performance to minimize downtime. This drives the need for tapes with exceptionally consistent mechanical properties, such as precise sprocket hole registration and minimal elongation. Moreover, the advent of smart manufacturing is introducing carrier tapes embedded with RFID tags or printable QR codes, enabling component traceability throughout the production lifecycle. This allows for real-time inventory management, counterfeit prevention, and seamless data exchange between manufacturing execution systems (MES) and automated storage and retrieval systems (ASRS). As factories become more connected, the carrier tape is evolving from a passive protective package into an active data carrier, a transformation that adds value and commands a premium in the market.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Focus on Innovation and Geographic Expansion to Maintain Competitive Edge

The global carrier tape market exhibits a semi-consolidated competitive structure, characterized by the presence of several multinational corporations, regional specialists, and numerous smaller manufacturers. The market is dominated by a handful of key players who collectively held a significant portion of the market share in 2024. 3M stands as a preeminent force, leveraging its extensive material science expertise and robust global distribution network to serve a diverse clientele across North America, Europe, and Asia-Pacific. Its leadership is further cemented by a continuous focus on developing advanced, high-reliability tapes that meet stringent electrostatic discharge (ESD) protection standards.

Similarly, Shin-Etsu Polymer and Zhejiang Jiemei Electronic Technology have established themselves as formidable competitors, particularly in the Asia-Pacific region which accounts for over 50% of global production. Their significant market share is largely attributable to cost-effective manufacturing capabilities and strong relationships with major electronics manufacturing service (EMS) providers and original equipment manufacturers (OEMs) throughout China, South Korea, and Southeast Asia.

Furthermore, companies are aggressively pursuing growth through strategic initiatives. For instance, Advantek has recently expanded its production capacity in Malaysia to better serve the growing Southeast Asian market, while Sumitomo Bakelite continues to invest heavily in R&D for next-generation biodegradable and high-temperature resistant carrier tapes. These expansion and innovation strategies are critical for capturing market share in an industry projected to grow at a CAGR of 8.3% through 2032.

Meanwhile, other significant players like Nissho Corporation and SEKISUI SEIKEI are strengthening their positions through strategic mergers and acquisitions, as well as by forming exclusive partnerships with semiconductor giants. This allows them to secure long-term supply contracts and co-develop custom tape solutions tailored for specific, high-value components like advanced integrated circuits and optoelectronics.

List of Key Carrier Tape Companies Profiled

- 3M (U.S.)

- Advantek (U.S.)

- Shin-Etsu Polymer (Japan)

- Nissho Corporation (Japan)

- Zhejiang Jiemei Electronic Technology (China)

- NIPPO CO.,LTD (Japan)

- YAC GARTER (Taiwan)

- U-PAK (Taiwan)

- C-Pak (U.S.)

- ePAK International (U.S.)

- ROTHE (Germany)

- Sumitomo Bakelite (Japan)

- Tek Pak (U.S.)

- Oji F-Tex Co., Ltd. (Japan)

- Jiangyin Winpack (China)

- SEKISUI SEIKEI (Japan)

- Asahi Kasei (Japan)

- Kanazu Giken (Japan)

- Taiwan Carrier Tape Enterprise Co., Ltd (Taiwan)

- LaserTek (Taiwan)

Segment Analysis:

By Material

Plastic Core Carrier Tape Segment Dominates the Market Due to Superior Durability and ESD Protection

The market is segmented based on material into:

- Plastic Core Carrier Tape

- Subtypes: Polystyrene (PS), Polycarbonate (PC), and others

- Paper Core Carrier Tape

By Application

Active Components Segment Leads Due to High Volume Usage in Semiconductor Manufacturing

The market is segmented based on application into:

- Active Components

- Subtypes: Integrated Circuits, Transistors, Diodes

- Passive Components

- Optoelectronics

- Power Discrete Devices

- Others

By Width

Standard Width Segment Holds Major Share Due to Compatibility with Automated Assembly Equipment

The market is segmented based on width into:

- 8mm Carrier Tape

- 12mm Carrier Tape

- 16mm Carrier Tape

- 24mm Carrier Tape

- 32mm Carrier Tape

- 44mm Carrier Tape

- Others

By End-User Industry

Consumer Electronics Segment Leads Owing to Massive Production Volumes of Electronic Devices

The market is segmented based on end-user industry into:

- Consumer Electronics

- Automotive Electronics

- Industrial Electronics

- Medical Devices

- Aerospace and Defense

- Others

Regional Analysis: Carrier Tape Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the global carrier tape market, accounting for over 60% of global production and consumption. This dominance is primarily driven by China, which alone contributes more than 50% of worldwide output, supported by a massive and mature electronics manufacturing ecosystem. The region’s strength lies in its extensive supply chain for components like integrated circuits, resistors, and capacitors, which are predominantly packaged using plastic core carrier tapes. While cost-competitive, standard solutions remain prevalent, there is a noticeable and growing shift towards higher-performance, anti-static variants to meet the stringent requirements of advanced semiconductor and consumer electronics assembly. Countries such as Japan, South Korea, and Taiwan are also significant contributors, focusing on innovation and high-precision tapes for specialized applications, further cementing the region’s central role in the global market.

North America

North America represents a mature and technologically advanced market for carrier tapes, characterized by high demand for precision and reliability rather than sheer volume. The region is a major hub for semiconductor fabrication and the assembly of high-value electronics, including aerospace, medical devices, and automotive systems. This drives a consistent need for high-performance carrier tapes that offer superior protection against electrostatic discharge (ESD) and physical damage. Key manufacturers and end-users prioritize innovation and quality, with a strong focus on custom-designed tapes for specialized components. While the market is well-established, growth is steady, supported by ongoing investments in domestic electronics manufacturing and a robust innovation ecosystem that demands packaging solutions capable of handling increasingly miniaturized and sensitive devices.

Europe

Europe’s carrier tape market is defined by its emphasis on quality, compliance, and technological sophistication. The region hosts several leading automotive and industrial electronics manufacturers, which require highly reliable and precise packaging solutions to protect components throughout complex supply chains. Environmental regulations and sustainability initiatives are increasingly influencing material choices, prompting a gradual shift towards recyclable and bio-based polymer options where feasible. Innovation is a key driver, with manufacturers developing tapes that meet strict dimensional tolerances and ESD safety standards. While the market’s volume is smaller compared to Asia-Pacific, its value is significant due to the high-cost, low-volume nature of many specialized components produced in the region, ensuring a stable demand for advanced carrier tape solutions.

South America

The carrier tape market in South America is emerging and is primarily driven by the gradual expansion of local electronics manufacturing, particularly in countries like Brazil and Argentina. Demand is largely fueled by the consumer electronics and automotive sectors, which require basic protective packaging for components. However, the market faces challenges, including economic volatility that can impact investment in new manufacturing capacity and a reliance on imported high-tech tapes for more advanced applications. The adoption of sophisticated, high-performance carrier tapes is limited, with cost sensitivity leading to a preference for standard products. Nonetheless, as regional manufacturing capabilities grow, there is potential for increased local production and adoption of more advanced packaging solutions.

Middle East & Africa

The carrier tape market in the Middle East & Africa is nascent and highly fragmented. Demand is primarily generated by import-dependent electronics assembly operations and servicing markets for consumer goods. There is very limited local production of carrier tapes, with most supply being imported from Asia and Europe. The market’s development is constrained by the lack of a significant local electronics manufacturing base and limited investment in advanced industrial infrastructure. Growth is slow and tied to broader economic development and urbanization trends. While the need for basic protective packaging exists, the adoption of specialized, high-performance carrier tapes remains minimal, focusing instead on cost-effective solutions for less sensitive components.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Carrier Tape markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Carrier Tape Market?

-> Carrier Tape Market was valued at 768 million in 2024 and is projected to reach US$ 1327 million by 2032, at a CAGR of 8.3% during the forecast period.

Which key companies operate in Global Carrier Tape Market?

-> Key players include 3M, Advantek, Shin-Etsu Polymer, Nissho Corporation, and Zhejiang Jiemei Electronic Technology, among others. The top four manufacturers hold approximately 62% of the global market share.

What are the key growth drivers?

-> Key growth drivers include the expansion of the global electronics manufacturing sector, rising demand for automated component handling, and the proliferation of integrated circuits and passive components.

Which region dominates the market?

-> Asia-Pacific is the dominant region, with China alone accounting for over 50% of global production.

What are the emerging trends?

-> Emerging trends include the development of anti-static and high-heat resistant carrier tapes, miniaturization of pocket designs for smaller components, and increased adoption of recycled and sustainable materials.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...