MARKET INSIGHTS

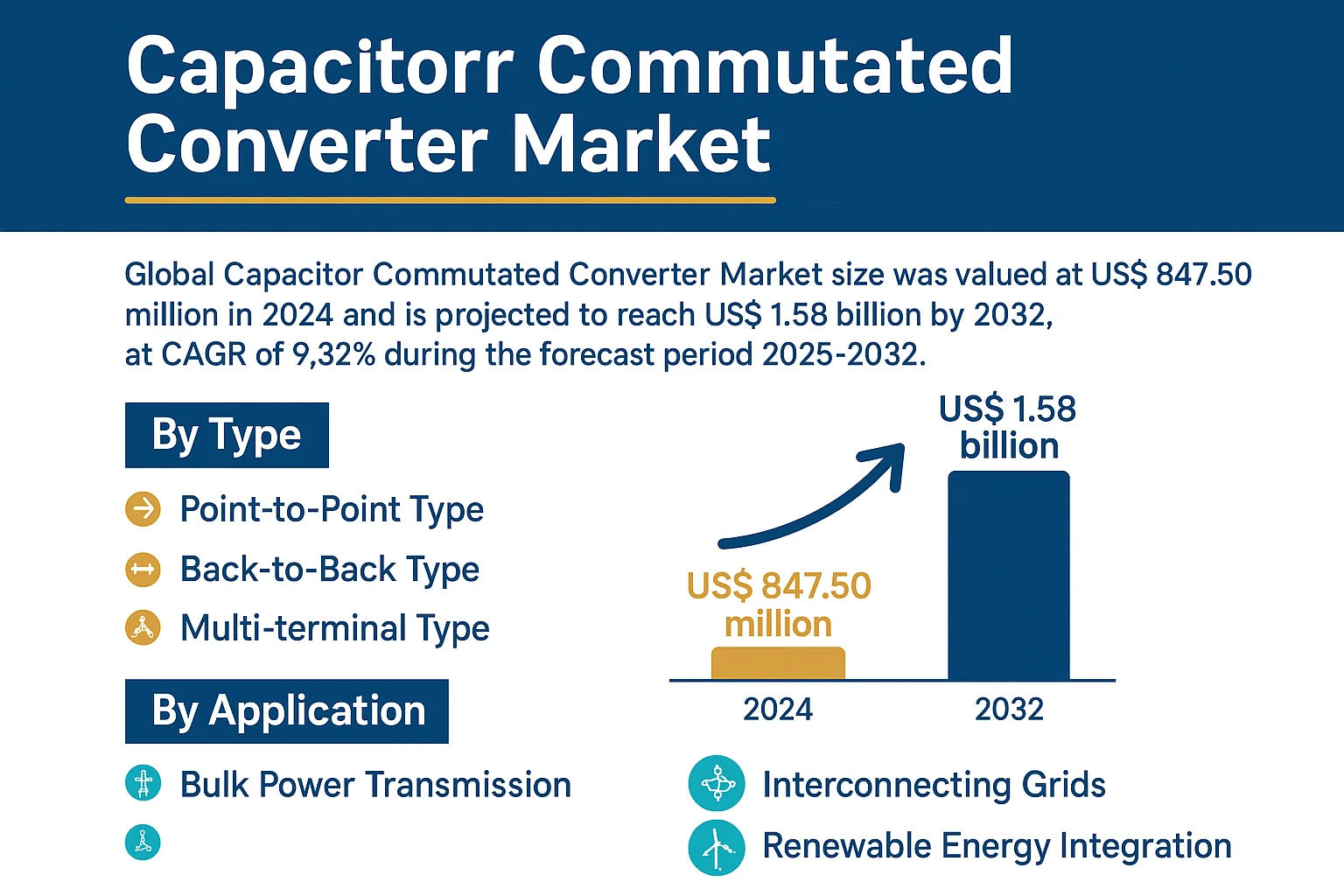

The global Capacitor Commutated Converter Market size was valued at US$ 847.50 million in 2024 and is projected to reach US$ 1.58 billion by 2032, at a CAGR of 9.32% during the forecast period 2025–2032.

Capacitor Commutated Converters (CCCs) are advanced power electronics devices that enable efficient AC/DC and DC/AC conversion through capacitor-based commutation. These systems play a critical role in high-voltage direct current (HVDC) transmission, renewable energy integration, and grid interconnection applications. The technology offers advantages including reduced harmonics, improved voltage stability, and enhanced power quality compared to conventional thyristor-based converters.

The market growth is driven by increasing investments in HVDC transmission projects and renewable energy integration. Asia-Pacific currently dominates the market with over 45% share, fueled by China’s ambitious grid expansion projects. However, Europe and North America are also witnessing significant adoption due to growing offshore wind farm developments. Key players like ABB and Siemens recently introduced next-generation CCC solutions with 25% higher efficiency ratings, further accelerating market adoption across industrial and utility applications.

MARKET DYNAMICS

MARKET DRIVERS

Growing Adoption of High-Voltage Direct Current (HVDC) Transmission Systems to Fuel Market Growth

The increasing demand for efficient long-distance power transmission is significantly boosting the capacitor commutated converter market. HVDC systems, which rely on capacitor commutated converters, enable the transmission of large amounts of electricity over vast distances with minimal losses. Countries worldwide are investing heavily in HVDC infrastructure to integrate renewable energy sources into their grids. For instance, over 200 HVDC projects are currently operational globally, with an additional 60+ under development. The superior efficiency of capacitor commutated converters in voltage conversion and reactive power compensation makes them indispensable in modern power systems.

Rapid Expansion of Renewable Energy Integration Creating Strong Demand

The global shift toward renewable energy sources is creating unprecedented demand for advanced power conversion technologies. Capacitor commutated converters play a critical role in connecting intermittent renewable power sources like wind and solar to the grid. As renewable energy capacity is projected to grow by 60% over the next decade, the need for efficient power converters will rise proportionally. The technology’s ability to handle variable power inputs while maintaining grid stability makes it particularly valuable for renewable energy applications. Recent projects integrating gigawatt-scale offshore wind farms with mainland grids have demonstrated the effectiveness of capacitor commutated converters in renewable energy systems.

MARKET RESTRAINTS

High Initial Investment Costs Limiting Market Penetration

While capacitor commutated converter technology offers significant advantages, its adoption faces challenges due to substantial upfront costs. The sophisticated power electronics and control systems required for these converters result in capital expenditures that can be 20-30% higher than conventional alternatives. This cost barrier is particularly pronounced in developing regions where budget constraints limit infrastructure investments. Furthermore, the specialized nature of these systems increases maintenance expenses, creating long-term financial considerations for utilities and energy providers.

MARKET CHALLENGES

Technical Complexity and Reliability Concerns Impacting Adoption

Capacitor commutated converters involve complex power electronics that require precise control and maintenance. The technology’s dependency on capacitor banks for commutation introduces potential failure points that can affect system reliability. Utilities often face challenges in implementing adequate protection schemes to prevent cascading failures in converter stations. These technical complexities not only increase operational risks but also require specialized expertise for installation and troubleshooting, creating additional adoption barriers.

Other Challenges

Grid Compatibility Issues

Integrating capacitor commutated converters with existing AC grids requires careful system studies and potential infrastructure upgrades. The mismatch between converter characteristics and legacy grid equipment can lead to harmonic distortions and stability concerns.

Supply Chain Constraints

The specialized components required for capacitor commutated converters, particularly high-voltage capacitors and power semiconductors, often face supply chain bottlenecks. These constraints can lead to extended lead times and project delays.

MARKET OPPORTUNITIES

Emerging Smart Grid Projects Creating New Growth Prospects

The global smart grid market, expected to surpass $100 billion by 2030, presents significant opportunities for capacitor commutated converter technology. These converters are increasingly being incorporated into smart grid designs to enhance power flow control and grid resilience. Their ability to provide fast reactive power compensation makes them ideal for modern grid applications that require rapid response to load fluctuations. Recent smart grid pilot projects incorporating capacitor commutated converters have demonstrated improvements in voltage regulation and power quality.

Offshore Wind Energy Expansion Driving Demand for Advanced Converters

The booming offshore wind sector, particularly in Europe and Asia, is creating unprecedented demand for capacitor commutated converters. These converters are essential for efficient power transmission from offshore wind farms to onshore grids. With global offshore wind capacity expected to increase by 15% annually, converter technology providers have substantial growth opportunities. Recent advancements in floating offshore wind farms have further expanded potential applications for capacitor commutated converters in challenging marine environments.

CAPACITOR COMMUTATED CONVERTER MARKET TRENDS

Renewable Energy Integration Driving Market Expansion

The increasing adoption of renewable energy sources like wind and solar power is significantly boosting demand for Capacitor Commutated Converters (CCC). These systems play a critical role in integrating intermittent renewable power into existing grids by enabling efficient AC-DC conversion with lower harmonic distortion. Recent grid modernization projects in North America and Europe demonstrate how CCC technology helps maintain grid stability despite renewable energy’s variable output. The global push toward net-zero emissions has accelerated renewable installations by 7% annually since 2020, creating substantial opportunities for CCC deployment.

Other Trends

High-Voltage Direct Current (HVDC) Transmission Growth

The rising need for long-distance power transmission is driving significant adoption of HVDC systems, where CCC technology offers superior performance compared to traditional converters. CCC systems demonstrate 15-20% lower energy losses in voltage conversion processes, making them particularly valuable for intercontinental grid interconnections. Major projects like the planned 3,800 km HVDC link between India and Oman highlight how CCC solutions enable efficient bulk power transfer across regions.

Technological Advancements Improving System Efficiency

Recent innovations in capacitor materials and converter topology design are substantially enhancing CCC performance. Next-generation film capacitors with higher energy density (>5 J/cm³) allow more compact converter designs while maintaining robust commutation capabilities. Manufacturers are integrating artificial intelligence for predictive maintenance, reducing downtime by up to 30% in operational systems. These improvements address key industry pain points like equipment longevity and operational costs, making CCC solutions increasingly attractive for utility-scale applications.

Electric Vehicle Infrastructure Development Creating New Opportunities

The rapid expansion of electric vehicle charging networks is generating substantial demand for specialized power conversion solutions. CCC technology effectively manages the fast-charging requirements (350kW+) of next-generation EV stations while minimizing grid impact. With global EV sales projected to reach 45 million units annually by 2030, power conversion systems must handle more dynamic load profiles – a challenge well-suited to CCC’s rapid switching capabilities.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Investments and Technological Advancements Drive Market Competition

The global capacitor commutated converter market features a competitive landscape dominated by multinational power and energy technology corporations. ABB and Siemens currently lead the market, together accounting for approximately 35% of the global share in 2024. Their dominance stems from extensive product portfolios, strong R&D capabilities, and established infrastructure in high-voltage direct current (HVDC) transmission systems.

General Electric Company and Mitsubishi Electric Corporation follow closely, leveraging their expertise in power electronics and strategic partnerships with grid operators. These companies have significantly invested in capacitor commutated converter technologies to enhance grid stability and renewable energy integration.

Meanwhile, Asian players like Hitachi and LS ELECTRIC are rapidly expanding their market presence through cost-effective solutions tailored for developing economies. Their growth is further accelerated by increasing government initiatives for grid modernization across Asia-Pacific regions.

Recent developments indicate that key players are focusing on modular converter designs and digital control systems to improve efficiency. Toshiba Corporation’s recent launch of its next-generation CCC platform demonstrates this trend, offering 15% higher efficiency compared to previous models.

List of Key Capacitor Commutated Converter Companies Profiled

- ABB (Switzerland)

- General Electric Company (U.S.)

- Hitachi (Japan)

- LS ELECTRIC (South Korea)

- Mitsubishi Electric Corporation (Japan)

- Nexans (France)

- NKT A/S (Denmark)

- NR Electric (China)

- Prysmian Group (Italy)

- Siemens (Germany)

- Toshiba Corporation (Japan)

Segment Analysis:

By Type

Point-to-Point Type Leads the Market Due to Wide Adoption in Long-Distance Power Transmission

The market is segmented based on type into:

- Point-to-Point Type

- Subtypes: High-voltage DC, Flexible AC transmission systems (FACTS)

- Back-to-Back Type

- Multi-terminal Type

- Subtypes: Radial configuration, Mesh configuration

By Application

Bulk Power Transmission Segment Dominates Owing to Rising Infrastructure Development

The market is segmented based on application into:

- Bulk Power Transmission

- Interconnecting Grids

- Renewable Energy Integration

- Industrial Applications

- Others

By Voltage Level

High Voltage Segment Accounts for Major Share Due to Transmission Efficiency Requirements

The market is segmented based on voltage level into:

- High Voltage (Above 72.5 kV)

- Medium Voltage (1 kV – 72.5 kV)

- Low Voltage (Below 1 kV)

By End-User

Utility Sector Holds Maximum Share Owing to Grid Modernization Initiatives

The market is segmented based on end-user into:

- Utilities

- Industrial

- Commercial

- Residential

Regional Analysis: Capacitor Commutated Converter Market

North America

The North American market for Capacitor Commutated Converters (CCC) is driven by advanced grid infrastructure projects and government initiatives promoting renewable energy integration. The U.S. leads the region with high demand for high-voltage direct current (HVDC) transmission systems, particularly in projects like the Champlain Hudson Power Express, a $6 billion underground transmission line. Regulatory standards such as NERC reliability requirements ensure the deployment of efficient power conversion technologies. However, high installation costs and supply chain constraints for high-capacity capacitors remain key challenges. Canada’s focus on electrification and inter-regional power transmission further supports market growth.

Europe

Europe showcases strong demand for CCC technology, especially in cross-border power transmission projects like NordLink (Germany-Norway interconnection) and EuroAsia Interconnector. The EU’s commitment to achieving 45% renewable energy by 2030 necessitates efficient power conversion solutions. Countries like Germany and the UK are investing in grid resilience, favoring modular multi-terminal CCC systems for offshore wind integration. However, complex permitting processes and stricter electromagnetic compatibility regulations slightly hinder deployment speed. Eastern Europe is gradually adopting CCC solutions as aging grid infrastructure undergoes modernization.

Asia-Pacific

As the fastest-growing market for CCCs, Asia-Pacific benefits from large-scale renewable energy projects and ultra-high-voltage (UHV) transmission developments. China dominates with over 60% of global HVDC projects, requiring CCCs for grid stability in its expansive power networks. India’s Green Energy Corridor Initiative is accelerating demand, while Japan’s shift toward decentralized energy systems creates opportunities for compact CCC units. Southeast Asian nations, such as Vietnam and Indonesia, face technology adoption challenges due to budget constraints, though multinational partnerships are bridging the gap. Cost-competitive local manufacturers are reshaping market dynamics.

South America

South America exhibits moderate CCC adoption, primarily in hydropower-heavy nations like Brazil and Argentina. The Itaipu Dam’s HVDC systems and Chile’s renewable energy expansions drive demand, but economic instability slows large-scale investments. Regional grids remain fragmented, and reliance on conventional thyristor-based converters persists due to lower upfront costs. However, long-term projects like the Amazon Transmission Line signal gradual GCC integration. Regulatory uncertainty and financing hurdles remain critical barriers for technology suppliers.

Middle East & Africa

This region shows nascent but promising GCC adoption, with Saudi Arabia and the UAE leading in renewable energy transitions, including solar mega-projects like NEOM. Africa’s power deficit and weak grid interconnections create opportunities, though funding shortages limit large-scale deployments. South Africa’s Cape Verde Interconnector and GCC pilot projects in Morocco indicate steady progress. Political instability in some nations and a lack of localized manufacturing slow market growth, but public-private partnerships are expected to boost future prospects.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Capacitor Commutated Converter markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at US$ 847.50 million in 2024 and is projected to reach US$ 1.58 billion by 2032.

- Segmentation Analysis: Detailed breakdown by product type (Point-to-Point, Back-to-Back, Multi-terminal), application (Bulk Power Transmission, Interconnecting Grids), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, with country-level analysis of key markets.

- Competitive Landscape: Profiles of leading market participants including ABB, Siemens, General Electric, Mitsubishi Electric, and Toshiba, covering their market share, product portfolios, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging converter technologies, efficiency improvements, and integration with renewable energy systems.

- Market Drivers & Restraints: Evaluation of factors including growing renewable energy investments, grid modernization needs, alongside challenges like high implementation costs.

- Stakeholder Analysis: Strategic insights for power utilities, equipment manufacturers, investors, and policymakers regarding market opportunities.

The research employs primary and secondary methodologies including expert interviews, industry data analysis, and market intelligence to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Capacitor Commutated Converter Market?

-> Capacitor Commutated Converter Market size was valued at US$ 847.50 million in 2024 and is projected to reach US$ 1.58 billion by 2032, at a CAGR of 9.32% during the forecast period 2025–2032.

Which key companies operate in Global Capacitor Commutated Converter Market?

-> Key players include ABB, Siemens, General Electric, Mitsubishi Electric, Toshiba, Hitachi, and Prysmian Group, among others.

What are the key growth drivers?

-> Key drivers include rising renewable energy integration, grid modernization initiatives, and increasing HVDC transmission projects globally.

Which region dominates the market?

-> Asia-Pacific leads in market share due to rapid power infrastructure development, while North America and Europe remain significant markets.

What are the emerging trends?

-> Emerging trends include development of hybrid converter systems, integration with energy storage, and smart grid applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...