MARKET INSIGHTS

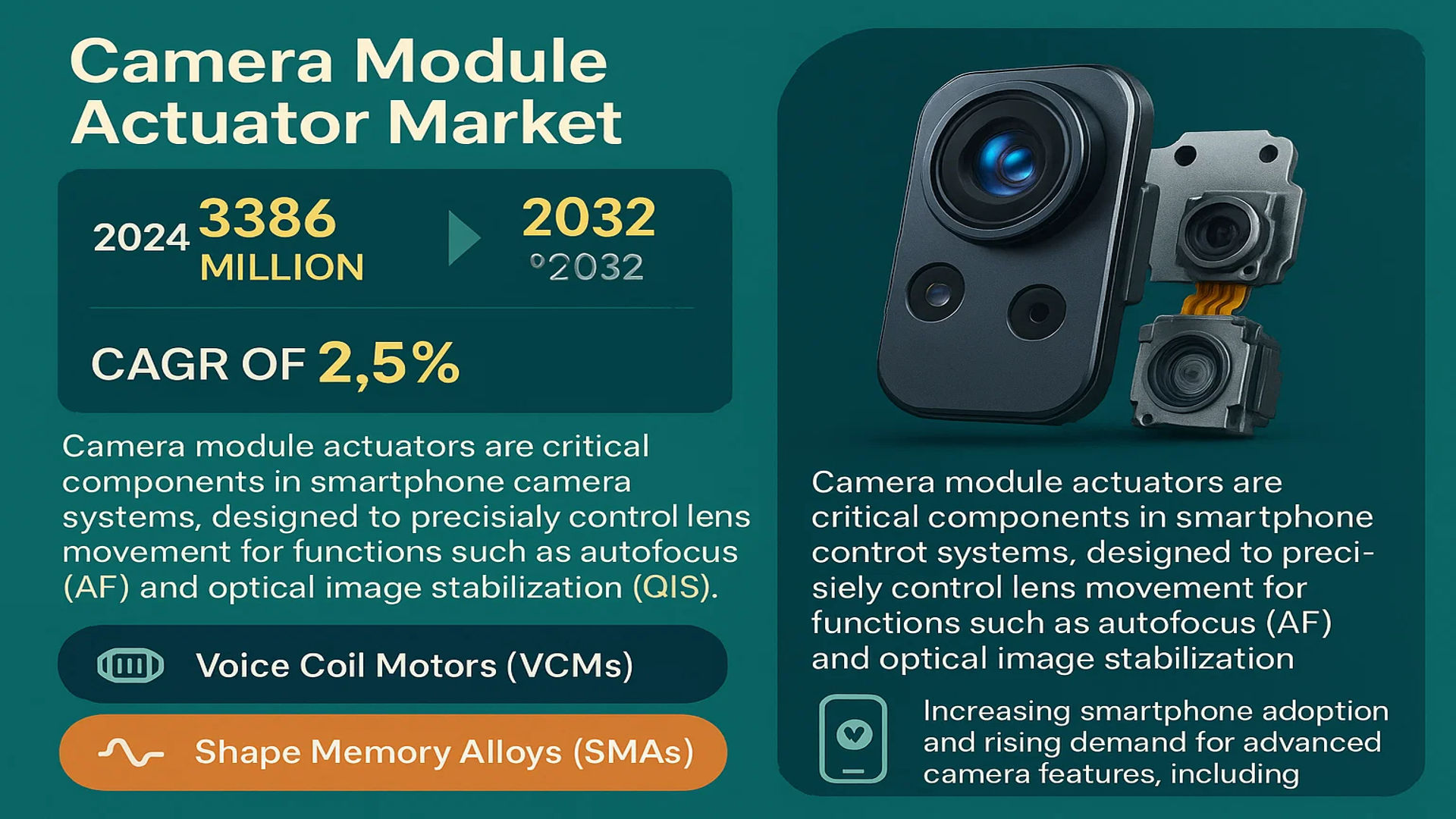

The global Camera Module Actuator Market was valued at 3386 million in 2024 and is projected to reach US$ 3997 million by 2032, at a CAGR of 2.5% during the forecast period.

Camera module actuators are critical components in smartphone camera systems, designed to precisely control lens movement for functions such as autofocus (AF) and optical image stabilization (OIS). These actuators enable the camera module to adjust lens positions accurately, enhancing image quality and performance. The two primary types of actuators used are Voice Coil Motors (VCMs) and Shape Memory Alloys (SMAs), each offering distinct advantages in terms of precision, speed, and miniaturization.

The market growth is driven by increasing smartphone adoption and the rising demand for advanced camera features, including high-resolution imaging and multi-camera setups. However, the market faces challenges due to pricing pressures and the complexity of integrating actuators into compact devices. Leading manufacturers like TDK, Alps Alpine, and LG Innotek continue to innovate, focusing on energy-efficient and compact actuator solutions to meet evolving industry requirements.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for High-Resolution Smartphone Cameras to Accelerate Market Growth

The global smartphone industry continues to prioritize advanced camera capabilities as a key differentiator, directly fueling demand for precision camera module actuators. Modern smartphones now commonly incorporate multiple high-megapixel lenses with sophisticated optical zoom capabilities. Industry reports indicate nearly 80% of flagship smartphones now feature actuators for both autofocus and optical image stabilization. This trend stems from consumer preference for professional-grade mobile photography and videography, compelling OEMs to integrate more sophisticated actuator technologies.

Adoption of Multi-Camera Setups Creates New Demand Channels

Smartphone manufacturers are increasingly adopting triple, quadruple and even penta-camera configurations to enhance photographic versatility. Current market analysis shows the average number of cameras per smartphone increased from 2.1 in 2019 to 3.8 in 2024, creating proportional growth in actuator requirements. This multi-camera evolution is particularly evident in premium Android devices, where manufacturers compete to offer superior telephoto, wide-angle and macro capabilities – each requiring dedicated actuator modules. The growing prevalence of under-display camera technology also presents new opportunities for compact actuator solutions.

5G and AI Photography Enhancements Drive Technological Innovation

The rollout of 5G networks and AI-powered computational photography are reshaping camera actuator requirements. High-speed connectivity enables advanced features like real-time imaging analytics and cloud-based processing, which demand faster and more precise lens positioning. Manufacturers are responding with next-generation actuators capable of microsecond response times and nanometer-level accuracy. Additionally, AI-driven photography modes such as night vision and portrait enhancements rely on sophisticated actuator control algorithms. These technological synergies are pushing the boundaries of what mobile cameras can achieve, creating sustained demand for innovative actuator solutions.

MARKET CHALLENGES

Miniaturization Pressures Intensify Engineering Complexities

As smartphone designs trend toward thinner profiles with larger displays, camera module actuators face significant size constraints. The industry standard for actuator thickness has decreased from 5.5mm to 4.2mm in just three years, forcing manufacturers to develop innovative solutions that maintain performance in shrinking form factors. These dimensional reductions challenge traditional voice coil motor designs, requiring alternative approaches like shape memory alloys and micro-electromechanical systems. The precision manufacturing required for these miniature components also drives up production costs and quality control expenses.

Supply Chain Fragility Impacts Production Stability

The global actuator market remains vulnerable to component shortages and geopolitical trade tensions. Recent disruptions have revealed over-reliance on specific geographic regions for rare earth metals and precision manufacturing equipment. Many actuator manufacturers report lead time increases of 30-45 days for critical components during peak demand periods. This instability complicates production planning and inventory management, particularly for just-in-time manufacturing models prevalent in the smartphone industry.

Thermal Management in High-Performance Actuators

Increased power requirements for advanced actuator functions generate significant heat in confined spaces. Prolonged exposure to elevated temperatures can degrade performance and reliability, particularly in devices marketed for continuous 4K video recording. Thermal issues already account for approximately 15% of camera module failures in field testing, prompting manufacturers to invest in heat dissipation solutions that don’t compromise actuator responsiveness or form factor.

MARKET RESTRAINTS

Cost Sensitivity Limits Advanced Actuator Adoption in Mid-Range Devices

While premium smartphones readily incorporate cutting-edge actuator technologies, price-sensitive mid-range segments face adoption barriers. High-end optical image stabilization actuators can cost 8-10 times more than basic autofocus modules, making them prohibitive for devices with strict bill-of-materials constraints. This economic reality creates a bifurcated market where technological advancements diffuse slowly beyond flagship products. Manufacturers must balance performance aspirations with consumer price expectations, often resulting in compromised solutions that limit full actuator potential.

Standardization Gaps Hinder Cross-Platform Compatibility

The lack of universal standards for camera module interfaces complicates actuator integration across different device architectures. Proprietary control protocols and mechanical specifications require extensive customization, increasing development cycles and testing overhead. These compatibility challenges are particularly acute for emerging actuator technologies trying to gain market traction, as they must support multiple implementation scenarios. Industry efforts to establish common frameworks have progressed slowly, leaving manufacturers to navigate a fragmented landscape of technical requirements.

MARKET OPPORTUNITIES

Emerging Applications in AR/VR Create New Market Verticals

The rapid development of augmented and virtual reality technologies presents significant growth potential for advanced actuator solutions. Next-generation AR glasses and VR headsets require ultra-compact focus adjustment mechanisms to maintain image clarity across varying focal planes. Early implementations already demonstrate demand for specialized actuators capable of dynamic focal length adjustments under 5 milliseconds. As these immersive technologies transition from niche applications to mainstream adoption, camera module actuators will play a critical role in enabling comfortable, extended-use experiences.

Automotive Camera Systems Offer Expansion Potential

The automotive industry’s increasing reliance on camera-based ADAS (Advanced Driver Assistance Systems) creates parallel opportunities for actuator manufacturers. Modern vehicles now integrate multiple high-performance cameras for 360-degree visibility, each requiring robust focusing and stabilization solutions that withstand vibration and temperature extremes. Unlike consumer electronics with 2-3 year replacement cycles, automotive applications demand actuator reliability across 10-15 year service lives, opening new avenues for durable, high-performance designs.

Material Science Innovations Enable Next-Generation Designs

Breakthroughs in advanced materials present transformative opportunities for actuator performance and efficiency. New shape-memory alloys with higher strain capacities and lower power requirements are expanding design possibilities beyond traditional voice coil motors. Similarly, piezoelectric materials now achieve displacement ranges suitable for miniature lens positioning while offering sub-millisecond response times. These material innovations, combined with precision manufacturing advancements, are enabling actuator architectures that were previously impractical for mass production.

CAMERA MODULE ACTUATOR MARKET TRENDS

Advancements in Smartphone Imaging to Drive Camera Module Actuator Market Growth

The global camera module actuator market is experiencing significant momentum due to the rising demand for high-resolution smartphone cameras. With consumers increasingly prioritizing professional-grade photography from mobile devices, manufacturers are integrating advanced actuator technologies like Voice Coil Motors (VCM) and Shape Memory Alloys (SMA) to enhance autofocus speed and optical image stabilization. In 2024, the market was valued at $3.38 billion, reflecting a steady adoption of multi-camera setups in flagship smartphones. The transition to 5G-enabled devices further accelerates this trend, as faster connectivity demands higher-quality imaging for augmented reality (AR) and video applications.

Other Trends

Miniaturization and Compact Designs

As smartphone designs shift toward slimmer profiles, there is a pressing need for compact actuator solutions without compromising performance. Manufacturers are increasingly exploring Micro-Electro-Mechanical Systems (MEMS) technology, which offers precision in a smaller footprint. MEMS-based actuators are particularly gaining traction in high-end smartphones, where space constraints are critical. Additionally, SMA actuators provide a viable alternative to traditional VCMs due to their lightweight yet high-performance characteristics. These innovations are essential for supporting the trend of foldable and ultra-thin smartphones, where components must balance durability with minimal thickness.

Expansion of AI-Driven Photography Solutions

The integration of artificial intelligence (AI) in smartphone cameras is transforming the functionality of camera actuators. AI-powered features such as real-time subject tracking and computational photography require actuators with rapid response times and high precision. Leading smartphone manufacturers are leveraging AI to optimize autofocus accuracy, further driving demand for next-generation actuators. The push toward low-light photography enhancement and multi-frame processing also places higher expectations on actuator stability, positioning VCMs as the dominant choice in mid-range and premium devices. Furthermore, AI-driven optimization is enabling actuators to adapt dynamically to varying shooting conditions, enhancing user experience and reducing power consumption.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Advancements and Miniaturization Drive Competition in Camera Module Actuator Market

The global camera module actuator market exhibits a dynamic competitive environment characterized by the presence of established multinational corporations and emerging regional players specializing in precision engineering. TDK Corporation currently leads the market owing to its cutting-edge Voice Coil Motor (VCM) technology that dominates over 30% of high-end smartphone applications. Their patented closed-loop autofocus systems have become industry benchmarks for responsiveness and accuracy.

Close competitors like LG Innotek and Mitsumi Electric have been gaining market share through strategic partnerships with leading smartphone OEMs. LG Innotek’s dual-stage actuator technology, combining VCM with Shape Memory Alloy (SMA) components, demonstrates particular promise for next-generation folding phones where space constraints demand exceptional compactness.

Several Japanese manufacturers including Alps Alpine and TOK Corporation differentiate themselves through materials innovation, developing proprietary alloys that improve thermal stability in SMA actuators. These advancements address a critical industry challenge as camera resolutions increase and processing temperatures rise in flagship devices.

Meanwhile, Chinese firms such as Shanghai B.L Electronics and JIANGXIN MICRO MOTOR compete aggressively in the mid-range segment through cost-efficient manufacturing and rapid prototyping capabilities. Their ability to deliver customized actuator solutions within tight development cycles has made them preferred partners for many domestic smartphone brands expanding into international markets.

List of Key Camera Module Actuator Companies Profiled

- TDK Corporation (Japan)

- Mitsumi Electric (Japan)

- LG Innotek (South Korea)

- Alps Alpine (Japan)

- Jahwa Electronics (South Korea)

- SEMCO (South Korea)

- New Shicoh Motor (Japan)

- Haesung Optics (South Korea)

- MCNEX (South Korea)

- Shanghai B.L Electronics (China)

- JIANGXIN MICRO MOTOR (China)

- TOK Corporation (Japan)

Segment Analysis:

By Type

VCM Segment Leads Due to Widespread Adoption in Smartphone Cameras

The market is segmented based on type into:

- Voice Coil Motor (VCM)

- Subtypes: Open-loop VCM, Closed-loop VCM, and others

- Shape Memory Alloy (SMA)

- Piezoelectric Actuators

- Micro-Electro-Mechanical Systems (MEMS)

- Others

By Application

High-end Smartphones Segment Dominates Due to Advanced Camera Features

The market is segmented based on application into:

- Low-end Smartphones

- Mid-range Smartphones

- High-end Smartphones

By Function

Autofocus Segment Leads Owing to Increased Demand for Clear Imaging

The market is segmented based on function into:

- Autofocus

- Optical Image Stabilization

- Zoom

- Others

By Technology

OIS Technology Gains Traction for Enhanced Photography Experience

The market is segmented based on technology into:

- Optical Image Stabilization (OIS)

- Electronic Image Stabilization (EIS)

- Hybrid Image Stabilization

Regional Analysis: Camera Module Actuator Market

Asia-Pacific

The Asia-Pacific region dominates the global camera module actuator market, accounting for over 60% of global shipments, driven by massive smartphone production in China, South Korea, and India. China serves as the manufacturing hub for major smartphone brands and component suppliers, with companies like SEMCO, Jahwa Electronics, and TDK expanding their production capacities for VCM and SMA actuators. The region benefits from strong supply chain integration, with actuator manufacturers co-located near smartphone assembly plants. While cost competition remains intense, particularly for mid-range and budget devices, there is growing demand for premium actuators as Chinese OEMs increasingly adopt multi-camera setups and OIS technology in flagship models.

North America

North America’s camera module actuator market focuses primarily on high-end applications, with strong demand for advanced auto-focus and optical image stabilization solutions from flagship smartphone manufacturers. The U.S. hosts R&D centers for several global actuator manufacturers, focusing on innovations in MEMS-based solutions and AI-driven autofocus algorithms. The region’s emphasis on premium smartphone features has accelerated adoption of SMA actuators in high-end devices, though supply remains largely dependent on Asian manufacturers. Stringent quality requirements and patent protections create barriers for new entrants, consolidating the market position of established players like Alps Alpine and Mitsumi.

Europe

Europe maintains a specialized position in the camera module actuator market, with Germany and France hosting key development centers for automotive imaging applications that require high-reliability actuators. While smartphone-related demand follows global trends, the region shows particular strength in industrial and medical imaging applications using precision actuators. European camera manufacturers increasingly specify SMA actuators for their compact size and temperature stability advantages. The presence of leading optical companies like ZEISS creates opportunities for actuator suppliers to develop customized solutions, though overall market volume remains smaller than Asia due to limited local smartphone production.

South America

The South American camera module actuator market remains in growth phase, primarily serving local smartphone assembly operations in Brazil and Argentina. Price sensitivity dominates purchasing decisions, with VCM actuators preferred for their cost advantage over SMA alternatives. Market growth faces challenges from regional economic fluctuations and import dependency for advanced components. However, increasing smartphone penetration and the rise of local brands create opportunities for actuator suppliers to establish partnerships with emerging device manufacturers, particularly for mid-range device specifications.

Middle East & Africa

This emerging market shows gradual growth in camera module actuator demand, driven by expanding smartphone adoption across the region. While most actuators are imported through global supply chains, there are initial signs of local assembly operations in countries like Turkey and South Africa. The market exhibits a clear bifurcation between premium imported smartphones using advanced actuators and budget devices employing simple VCM solutions. Infrastructure limitations for precision manufacturing currently prevent local actuator production, but the region presents long-term potential as a consumption market as disposable incomes rise and 5G networks expand.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Camera Module Actuator markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Camera Module Actuator market was valued at USD 3,386 million in 2024 and is projected to reach USD 3,997 million by 2032, at a CAGR of 2.5%.

- Segmentation Analysis: Detailed breakdown by product type (VCM, SMA), application (low-end, mid-range, high-end smartphones), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific dominates the market with over 60% revenue share in 2024.

- Competitive Landscape: Profiles of leading market participants including TDK, Mitsumi, LG Innotek, and Alps Alpine, covering their product offerings, R&D focus, manufacturing capacity, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies like MEMS-based actuators, AI-driven autofocus systems, and compact SMA solutions for high-end smartphones.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as rising smartphone demand and multi-camera trends, along with challenges like supply chain constraints.

- Stakeholder Analysis: Insights for component suppliers, smartphone OEMs, investors, and policymakers regarding strategic opportunities in the evolving camera technology ecosystem.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Camera Module Actuator Market?

->Camera Module Actuator Market was valued at 3386 million in 2024 and is projected to reach US$ 3997 million by 2032, at a CAGR of 2.5% during the forecast period.

Which key companies operate in Global Camera Module Actuator Market?

-> Key players include TDK, Mitsumi, LG Innotek, Alps Alpine, SEMCO, and Jahwa Electronics, among others.

What are the key growth drivers?

-> Key growth drivers include rising smartphone adoption, multi-camera trends in mobile devices, and demand for advanced imaging features like optical image stabilization.

Which region dominates the market?

-> Asia-Pacific dominates with over 60% market share, driven by smartphone manufacturing hubs in China, South Korea, and Japan.

What are the emerging trends?

-> Emerging trends include MEMS-based actuators, AI-driven autofocus systems, and compact SMA solutions for high-end smartphone cameras.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...