MARKET INSIGHTS

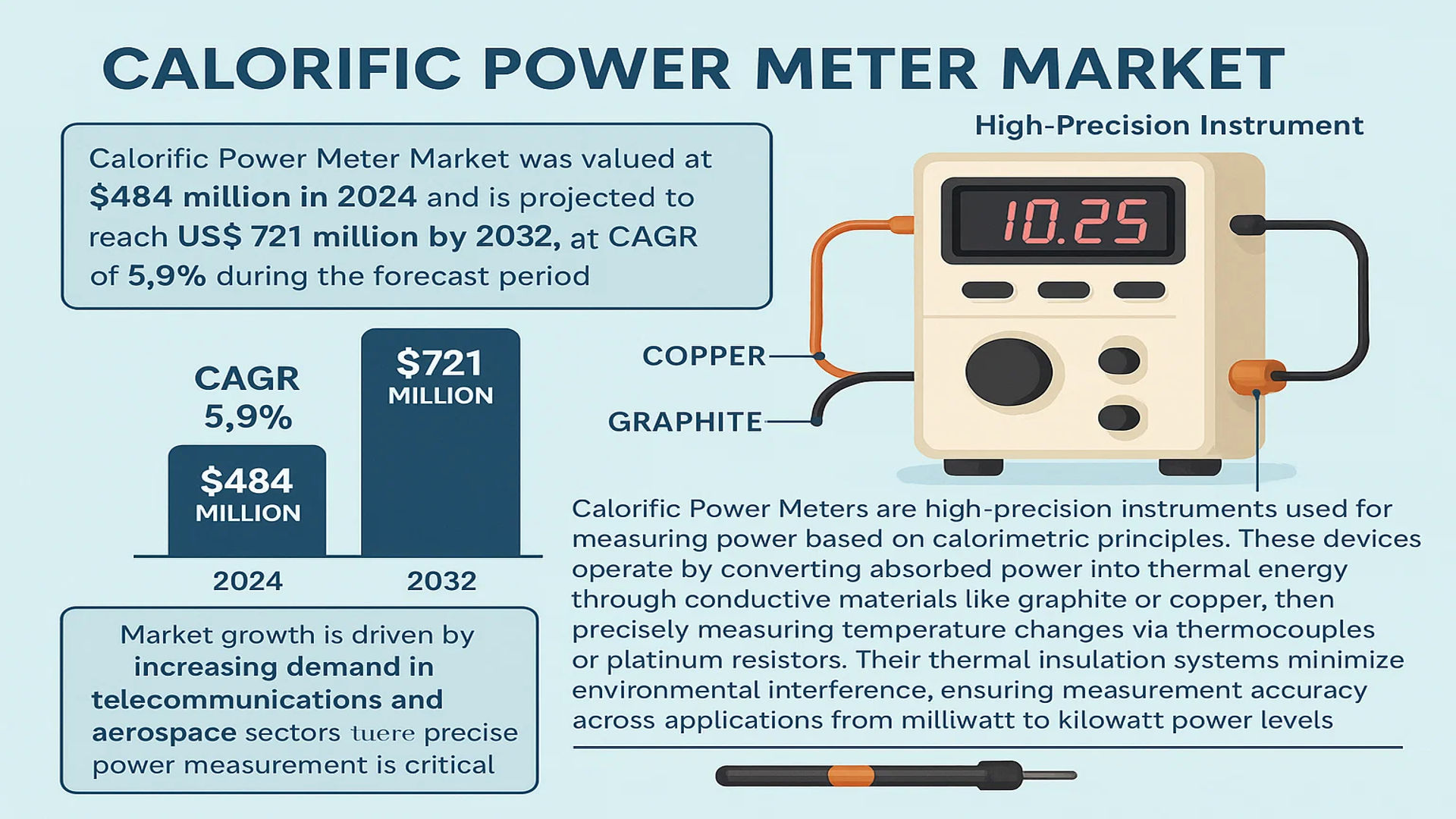

The global Calorific Power Meter Market was valued at 484 million in 2024 and is projected to reach US$ 721 million by 2032, at a CAGR of 5.9% during the forecast period.

Calorific Power Meters are high-precision instruments used for measuring power based on calorimetric principles. These devices operate by converting absorbed power into thermal energy through conductive materials like graphite or copper, then precisely measuring temperature changes via thermocouples or platinum resistors. Their thermal insulation systems minimize environmental interference, ensuring measurement accuracy across applications from milliwatt to kilowatt power levels.

The market growth is driven by increasing demand in telecommunications and aerospace sectors where precise power measurement is critical. While North America currently leads in market share, Asia-Pacific shows the highest growth potential due to expanding 5G infrastructure and manufacturing capabilities. Key players including Keysight Technologies and Rohde & Schwarz are investing in advanced models with improved thermal compensation and broader frequency ranges. The low-power segment (milliwatt level) is expected to show particular strength, growing at a higher CAGR through 2032.

MARKET DYNAMICS

MARKET DRIVERS

Expanding Telecommunications Infrastructure Fuels Calorific Power Meter Demand

The global rollout of 5G networks and expansion of communication infrastructure is creating substantial demand for accurate power measurement solutions like calorific power meters. These devices play a critical role in ensuring precise power monitoring for RF and microwave components used in base stations, satellites, and network equipment. As telecom operators worldwide accelerate their 5G deployments, requiring more sophisticated testing and measurement capabilities, the market for high-precision calorimetric power meters is experiencing significant growth. The telecommunications sector alone accounts for nearly 40% of current calorific power meter applications, highlighting its importance as a key market driver.

Advancements in Aerospace and Defense Technologies Drive Market Growth

The aerospace and defense sector’s increasing reliance on advanced electronic warfare systems, radar technologies, and satellite communications is creating robust demand for precise power measurement solutions. Calorific power meters provide the necessary accuracy for testing high-power microwave systems used in modern defense applications. With global defense budgets growing and governments increasing investments in electronic warfare capabilities, manufacturers are seeing increased orders for kilowatt-level power meters designed specifically for military applications. This segment has shown consistent annual growth between 6-8% over the past three years, indicating strong ongoing demand.

Industrial Automation and Smart Manufacturing Boost Adoption

As Industry 4.0 technologies transform manufacturing processes, there’s growing need for precise power monitoring in industrial automation systems. Calorific power meters are increasingly integrated into quality control systems for high-power industrial lasers, RF heating equipment, and other precision manufacturing tools. The ability of these devices to provide accurate thermal power measurement in harsh industrial environments makes them particularly valuable for smart manufacturing applications. With industrial automation investments projected to maintain 7-9% annual growth through 2030, this presents a sustained driver for market expansion.

MARKET RESTRAINTS

High Initial Costs Limit Adoption Among Small Enterprises

The significant capital investment required for high-precision calorific power meters creates a substantial barrier to market entry for smaller testing laboratories and manufacturing facilities. Advanced units with broad frequency ranges and high accuracy specifications can cost tens of thousands of dollars, placing them out of reach for many potential customers. This price sensitivity is particularly acute in emerging markets where budget constraints are more pronounced. While the total cost of ownership may be favorable over time, the upfront expense remains a deterrent that slows broader market penetration.

Other Restraints

Technical Complexity Requires Specialized Expertise

Proper operation and maintenance of calorific power meters requires technical knowledge that many potential users lack. The need for trained personnel to correctly interpret measurements and maintain calibration creates additional operational costs that some organizations find prohibitive. This technical barrier continues to restrain wider adoption, particularly in markets with shortages of skilled RF engineering professionals.

Competition from Alternative Measurement Technologies

While calorimetric methods offer high accuracy, they face competition from more affordable thermocouple-based and diode-based power sensors that meet basic requirements for many applications. These alternatives, while less precise, satisfy the needs of many users at significantly lower price points, creating ongoing competition that limits the addressable market for high-end calorific power meters.

MARKET OPPORTUNITIES

Emerging 6G Research Presents Future Growth Potential

The early stages of 6G technology development are creating new opportunities for advanced power measurement solutions. As research institutions and telecom equipment manufacturers begin testing higher frequency millimeter wave and terahertz components for future 6G networks, they require even more precise measurement capabilities. Calorific power meter manufacturers that can develop solutions optimized for these emerging frequency ranges will be well-positioned to capitalize on this next wave of telecommunications innovation expected to gain momentum later this decade.

Expansion of Satellite Communication Networks Drives Demand

The rapid growth of satellite constellations for global connectivity is generating significant demand for reliable power measurement solutions. Calorific power meters are particularly well-suited for testing high-power satellite transmitters and ground station equipment. With projections indicating deployment of tens of thousands of new satellites over the next five years, manufacturers have an opportunity to develop specialized solutions tailored to the unique requirements of the satellite communications industry. This sector represents one of the fastest-growing opportunities in the market, with potential for 50% growth in satellite-related applications by 2027.

MARKET CHALLENGES

Supply Chain Disruptions Impact Manufacturing Lead Times

The specialized components required for high-quality calorific power meters, including precision thermal sensors and high-conductivity materials, remain vulnerable to supply chain disruptions. Lead times for certain critical components have extended to six months or more in some cases, creating production bottlenecks that limit manufacturers’ ability to respond quickly to spikes in demand. These challenges are particularly acute for devices requiring military-grade or aerospace-qualified components with stringent certification requirements.

Other Challenges

Maintaining Measurement Accuracy in Diverse Environments

Ensuring consistent measurement accuracy across varying environmental conditions remains an engineering challenge. Temperature fluctuations, humidity changes, and electromagnetic interference can all affect performance, requiring sophisticated compensation algorithms and robust mechanical designs that add to development costs. Manufacturers must continually invest in R&D to maintain accuracy standards while meeting the needs of applications in field conditions.

Intellectual Property Protection in Growing Markets

As competition intensifies, particularly from manufacturers in developing markets, protecting proprietary technologies and designs has become increasingly challenging. The high value of technical innovations in this specialized market makes intellectual property security a significant concern that requires ongoing legal and technological investments from market leaders.

CALORIFIC POWER METER MARKET TRENDS

Advancements in Precision Measurement Technologies Driving Market Growth

The global calorific power meter market is witnessing significant growth due to advancements in high-precision measurement technologies. Manufacturers are focusing on improving thermal sensing accuracy and reducing environmental interference, leading to more reliable power measurement instruments. Calorimetric power meters, which operate on the principle of converting electrical power into measurable heat, are increasingly being adopted in applications requiring extreme accuracy such as aerospace, telecommunications, and industrial manufacturing. Recent innovations include the integration of AI-driven calibration systems that automatically compensate for temperature fluctuations, improving measurement consistency by up to 15% compared to traditional models.

Other Trends

Expanding Applications in 5G Infrastructure

The rollout of 5G networks worldwide is creating substantial demand for low-power calorific meters capable of measuring milliwatt-level signals with high precision. These instruments play a critical role in testing and maintaining 5G base stations, where precise power measurement directly affects network performance and energy efficiency. The communication industry’s segment is projected to maintain a compound annual growth rate of nearly 7% through 2032, accounting for approximately 30% of total calorific power meter applications.

Increasing Adoption in Renewable Energy Systems

As renewable energy systems become more sophisticated, calorific power meters are being increasingly utilized for efficiency testing in solar inverters and wind turbine power conversion systems. The ability to precisely measure power losses during energy conversion processes allows manufacturers to optimize system designs and improve overall energy yields. High-power kilowatt-level calorific meters are particularly seeing strong demand in this sector, with some models now capable of handling power levels exceeding 50kW while maintaining measurement accuracy within 0.1%.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Drive Innovation in High-Precision Power Measurement

The global calorific power meter market features a competitive mix of established manufacturers and emerging players striving to expand their technological capabilities. With the market projected to grow at 5.9% CAGR through 2032, companies are intensifying R&D investments to develop advanced measurement solutions for critical industries like aerospace and telecommunications.

Keysight Technologies currently leads the competitive landscape, holding significant market share due to its comprehensive portfolio of precision measurement instruments. The company’s recent introduction of next-generation calorimetric sensors with 0.1% measurement accuracy has strengthened its position in high-value applications like satellite communications and 5G infrastructure testing.

Rohde & Schwarz and Anritsu follow closely, with both companies demonstrating particular strength in the communication industry segment. Their strategic focus on developing compact, portable calorific power meters has enabled penetration into field testing markets, creating new growth opportunities beyond traditional laboratory applications.

The competitive dynamics are further intensified by Chinese manufacturers like Shenzhen Bonard Precision Instruments and Nanjing Shengbo Electronics who are gaining traction through cost-competitive offerings. These companies have successfully captured market share in Asia’s rapidly expanding industrial manufacturing sector, though they continue to face challenges in matching the measurement precision of established Western brands.

Recent industry developments highlight the strategic approaches of key players:

- Multiple patent filings for advanced thermal compensation algorithms in 2023-2024

- Increasing partnerships with aerospace OEMs for customized measurement solutions

- Growing emphasis on IoT-enabled power meters with remote monitoring capabilities

List of Key Calorific Power Meter Manufacturers

- Keysight Technologies (U.S.)

- Bird Technologies (U.S.)

- Rohde & Schwarz (Germany)

- Anritsu Corporation (Japan)

- Giga-tronics (U.S.)

- Maury Microwave (U.S.)

- Shenzhen Bonard Precision Instruments (China)

- Tianjin Ruili Optoelectronics Technology (China)

- Shanghai Boming Scientific Instruments (China)

- Nanjing Shengbo Electronics (China)

- Xi’an Aerospace Huaxun Technology (China)

- Chengdu Xinrui Electronics (China)

The market’s technological evolution is creating both opportunities and challenges. While demand grows for higher accuracy instruments, manufacturers must balance performance improvements with cost considerations to remain competitive across different market segments. The coming years will likely see further consolidation as companies seek to combine complementary technologies and expand geographical reach.

Segment Analysis:

By Type

Low Power (Milliwatt Level) Segment Holds Significant Market Share Due to Precision Measurement Applications

The market is segmented based on type into:

- Low Power (Milliwatt Level)

- Subtypes: Portable, Benchtop, and others

- High Power (Kilowatt Level)

- Subtypes: Industrial-grade, Laboratory-grade, and others

By Application

Communication Industry Leads the Market Due to Growing Need for RF Power Measurement

The market is segmented based on application into:

- Communication Industry

- Aerospace

- Industrial Manufacturing

- Others

By Technology

Thermal Sensor-based Calorimeters Dominate Due to High Accuracy in Power Measurement

The market is segmented based on technology into:

- Thermal Sensor-based

- Optical Sensor-based

- Hybrid Technology

By End User

Research Laboratories Hold Key Market Position Due to Extensive Usage in Testing Applications

The market is segmented based on end user into:

- Research Laboratories

- Manufacturing Facilities

- Telecommunication Service Providers

- Others

Regional Analysis: Calorific Power Meter Market

Asia-Pacific

Leading the global market, the Asia-Pacific region is expected to dominate calorific power meter demand, driven by rapid industrialization and technological advancements in countries like China, Japan, and South Korea. China alone contributes a significant share to the regional market due to its booming communication and aerospace sectors. Investments in 5G infrastructure and semiconductor manufacturing necessitate high-precision power measurement tools, fueling adoption. While cost competition remains intense, companies such as Shenzhen Bonard Precision Instruments and Nanjing Shengbo Electronics are strengthening their market presence through innovations in low-power and high-power measurement solutions. The region’s focus on automation and Industry 4.0 further accelerates demand, particularly in industrial manufacturing applications.

North America

The North American market is characterized by stringent quality standards and a strong emphasis on R&D, with the U.S. being the largest contributor. Key players, including Keysight Technologies and Bird Technologies, drive innovation in high-accuracy calorific meters for aerospace, defense, and telecommunications. Government and private sector investments in next-gen wireless networks and satellite communications are key growth drivers. However, the market faces challenges from the high cost of advanced metering solutions, especially for small and mid-sized enterprises. The shift toward energy-efficient industrial processes and IoT-enabled devices continues to create opportunities for specialized power measurement systems.

Europe

Europe maintains a robust market for calorific power meters, supported by regulatory frameworks promoting precision instrumentation in industrial and aerospace applications. Countries like Germany, France, and the U.K. lead in adopting advanced metering technologies, particularly for high-power applications in automotive and renewable energy sectors. Companies such as Rohde & Schwarz and Anritsu emphasize compliance with EU standards while pushing innovations in thermal measurement accuracy. However, slower industrial growth compared to Asia-Pacific and high dependency on imports for certain component supplies may restrain short-term expansion. Sustainability initiatives and Industry 4.0 adoption present long-term growth avenues.

South America

The South American market remains nascent, with Brazil and Argentina showing moderate growth in calorific power meter adoption. Local industrial manufacturing and energy sectors drive demand, though economic instability and limited R&D investments hinder progress. High reliance on imported metering solutions from North America and Europe leads to cost barriers for end-users. Nonetheless, gradual modernization in telecommunications and renewable energy infrastructure offers potential for market expansion, particularly for mid-range power measurement devices.

Middle East & Africa

This region exhibits emerging demand, primarily in Gulf Cooperation Council (GCC) countries such as Saudi Arabia and the UAE, where infrastructure development and aerospace projects are rising. Limited local manufacturing capabilities result in dependence on international suppliers, including Giga-tronics and Maury Microwave. While the aerospace and oil & gas sectors present niche opportunities, the broader market growth is constrained by funding gaps and low awareness of advanced power measurement technologies. Long-term prospects hinge on economic diversification and industrial automation trends.

Report Scope

This market research report provides a comprehensive analysis of the Global Calorific Power Meter Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 484 million in 2024 and is projected to reach USD 721 million by 2032, growing at a CAGR of 5.9%.

- Segmentation Analysis: Detailed breakdown by product type (Low Power and High Power), application (Communication Industry, Aerospace, Industrial Manufacturing, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. The U.S. and China are key markets, with significant growth potential.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships. Key players include Keysight Technologies, Bird Technologies, Rohde & Schwarz, Anritsu, and Giga-tronics.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, advancements in thermal measurement techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth, such as increasing demand for high-precision power measurement in aerospace and communication industries, along with challenges like supply chain constraints and regulatory issues.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Calorific Power Meter Market?

-> Calorific Power Meter Market was valued at 484 million in 2024 and is projected to reach US$ 721 million by 2032, at a CAGR of 5.9% during the forecast period.

Which key companies operate in Global Calorific Power Meter Market?

-> Key players include Keysight Technologies, Bird Technologies, Rohde & Schwarz, Anritsu, Giga-tronics, Maury Microwave, and Shenzhen Bonard Precision Instruments, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for high-precision power measurement, advancements in aerospace and communication technologies, and increasing industrial automation.

Which region dominates the market?

-> North America holds a significant market share, while Asia-Pacific is expected to witness the fastest growth due to rapid industrialization.

What are the emerging trends?

-> Emerging trends include integration of AI for enhanced measurement accuracy, development of portable calorific power meters, and increased adoption in renewable energy applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...