MARKET INSIGHTS

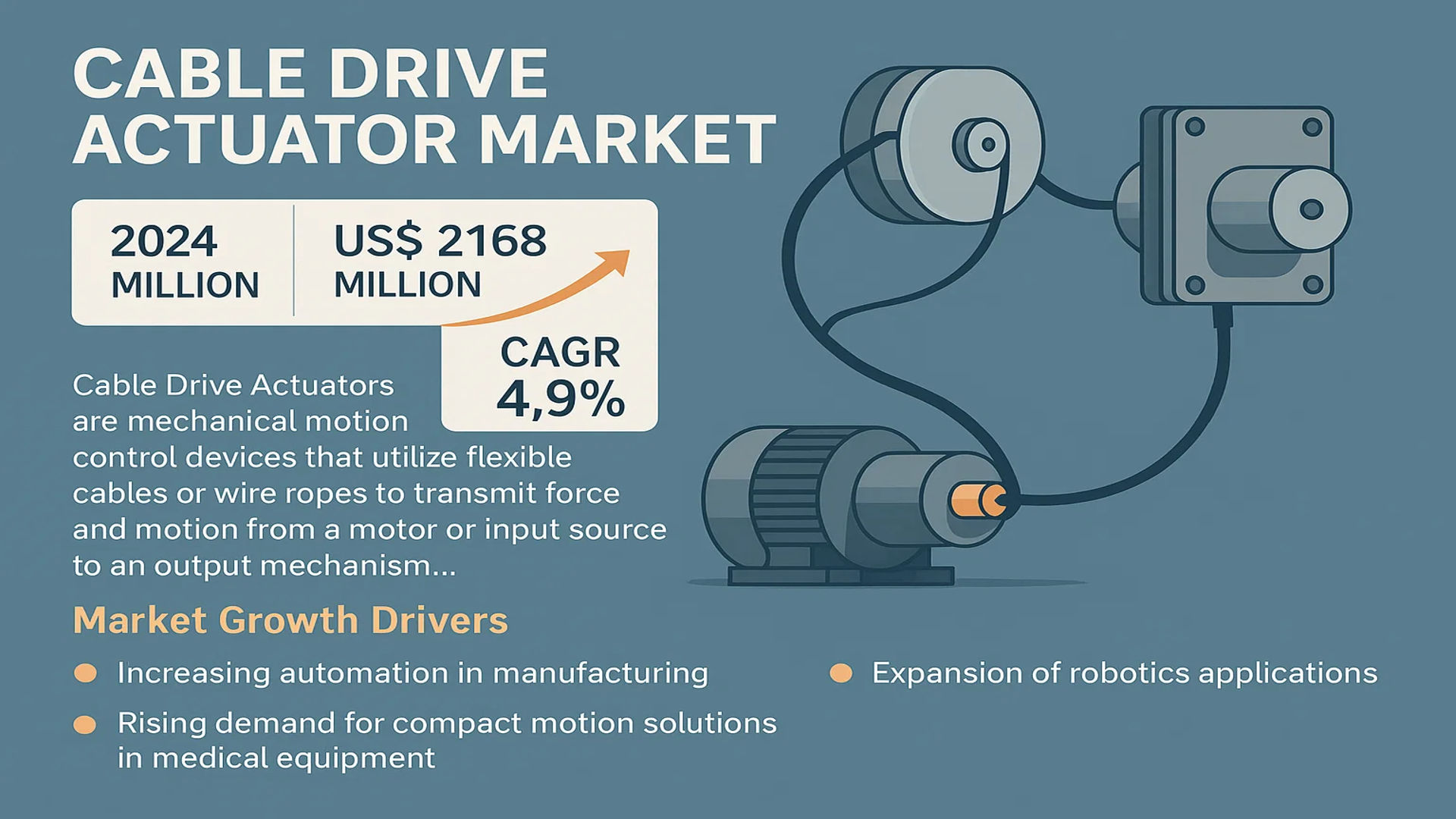

The global Cable Drive Actuator Market was valued at 1593 million in 2024 and is projected to reach US$ 2168 million by 2032, at a CAGR of 4.9% during the forecast period.

Cable Drive Actuators are mechanical motion control devices that utilize flexible cables or wire ropes to transmit force and motion from a motor or input source to an output mechanism. These actuators enable remote, flexible, and non-linear motion transfer, making them ideal for applications requiring precise movement in constrained spaces. The technology is widely adopted across industrial automation, medical devices, and automotive systems due to its reliability and efficiency.

The market growth is driven by increasing automation in manufacturing, rising demand for compact motion solutions in medical equipment, and the expansion of robotics applications. The Parallel Cable Drive segment is emerging as a key growth area due to its ability to handle higher loads with greater precision. While North America currently dominates the market, Asia-Pacific is expected to witness the fastest growth owing to rapid industrialization. Leading players like Parker Hannifin, Siemens, and Bosch Rexroth are investing in R&D to develop more efficient actuator solutions, further propelling market expansion.

MARKET DYNAMICS

MARKET DRIVERS

Growth in Industrial Automation to Drive Demand for Cable Drive Actuators

The rapid adoption of automation across industries is significantly boosting the cable drive actuator market. Industrial automation requires precise motion control systems, where cable drive actuators excel due to their flexibility, reliability, and ability to deliver force over long distances without mechanical linkages. The manufacturing sector accounts for over 35% of global actuator demand, with increasing investments in smart factories and robotics reinforcing this trend. These actuators are integral in applications like pick-and-place robots, CNC machines, and packaging systems, where they provide efficient force transmission while reducing system complexity and maintenance costs.

Expanding Medical Device Industry Creates New Application Areas

Advancements in medical technology are creating substantial opportunities for cable drive actuators, particularly in surgical robots and diagnostic equipment. The global medical robotics market, valued at over $8 billion, utilizes these actuators for their precise motion control and ability to operate in sterile environments. Minimally invasive surgical systems increasingly rely on cable-driven mechanisms to translate surgeon movements into instrument actions with precision under 100 microns. Furthermore, the growing demand for portable medical devices drives innovation in compact actuator designs suitable for MRI compatibility and radiation therapy equipment.

The aging global population and rising healthcare expenditures in emerging economies are accelerating adoption of advanced medical technologies that incorporate cable drive systems. This sector shows no signs of slowing, with surgical robot installations growing at nearly 15% annually as healthcare providers seek to improve patient outcomes through technological advancement.

MARKET RESTRAINTS

High Initial Costs and Complexity Limit Widespread Adoption

While offering significant advantages, cable drive actuators face adoption barriers due to their relatively high initial costs compared to traditional linear actuators. The precision cable systems, specialized materials, and custom engineering required for many applications can increase system costs by 20-30% over conventional solutions. This presents a particular challenge in price-sensitive markets and industries with established competing technologies. Small and medium manufacturers often hesitate to transition to cable-driven systems due to these cost considerations and the required retooling expenses.

Other Restraints

Maintenance Requirements

Cable systems require periodic tension adjustments and replacement of wear components to maintain performance. In harsh industrial environments, contamination and corrosion can accelerate wear, increasing maintenance costs. While modern designs have improved durability, these factors remain considerations for equipment manufacturers and end-users.

Standardization Challenges

The lack of industry-wide standards for cable drive systems complicates integration across platforms. Variations in cable materials, termination methods, and performance specifications require custom engineering solutions that can delay deployment and increase development costs for OEMs.

MARKET CHALLENGES

Competition from Alternative Actuation Technologies

Cable drive actuators face intensifying competition from emerging smart material actuators and advanced electromechanical systems. Piezoelectric and shape memory alloy actuators are gaining ground in applications requiring ultra-high precision, while conventional ball screw and belt drives continue to dominate in high-force industrial applications. Within the robotics sector, cable-driven systems must compete with direct-drive technologies offering superior backdrivability and control bandwidth that can exceed 100 Hz in advanced implementations.

The automotive industry’s shift toward electrification presents additional challenges as vehicle manufacturers reevaluate traditional actuation methods. While cable systems remain prevalent in certain subsystems, the industry’s focus on weight reduction and packaged efficiency drives consideration of alternative solutions that may better meet evolving design requirements.

MARKET OPPORTUNITIES

Emerging Applications in Robotics and Aerospace Offer Growth Potential

Advanced robotics applications present significant opportunities for cable drive actuator manufacturers. Collaborative robots (cobots) increasingly incorporate cable-driven joints to achieve the necessary combination of precision, backdrivability, and safety required for human-robot interaction. The aerospace sector also shows growing interest in these systems for aircraft control surfaces and space applications, where their lightweight design and reliable force transmission offer advantages over hydraulic alternatives. Commercial aircraft utilize over 100 actuators per plane, creating substantial market potential as manufacturers seek weight-saving solutions.

Innovations in material science are enabling new cable drive applications through the development of high-strength synthetic cables with fatigue lives exceeding 10 million cycles. When combined with advanced composite components, these systems can achieve weight reductions up to 40% compared to traditional metal-based actuation systems. Such advancements are particularly valuable in aerospace and mobile robotics where weight directly impacts performance and energy efficiency.

CABLE DRIVE ACTUATOR MARKET TRENDS

Industrial Automation Expansion Driving Market Growth

The global shift toward industrial automation is a major driver for the cable drive actuator market, which was valued at $1,593 million in 2024 and is projected to reach $2,168 million by 2032, growing at a CAGR of 4.9%. Cable drive actuators are increasingly being adopted in robotic applications due to their flexibility, precision, and ability to transmit motion in confined spaces where rigid linkages would be impractical. Leading manufacturers such as KUKA, Bosch Rexroth, and Yaskawa are integrating these actuators into collaborative robots (cobots), assembly lines, and material handling systems. The parallel cable drive segment, which enables multi-axis control with reduced mechanical complexity, is particularly gaining traction, with estimations indicating its accelerated growth in the next six years.

Other Trends

Medical and Surgical Robotics Adoption

The medical industry’s increasing reliance on minimally invasive surgical techniques has created a surge in demand for high-precision cable drive actuators. These actuators are essential in robotic-assisted surgical systems, offering smooth motion control and reliability in delicate procedures. The U.S. and China are key players in this segment, with the latter expected to increase its market share significantly by 2032. Cable-driven systems are also being used in rehabilitation robotics, assisting patients with mobility impairments through exoskeletons and prosthetics. This trend aligns with global healthcare investments, which are prioritizing advanced medical robotics to improve patient outcomes and surgical efficiency.

Automotive Electrification and Lightweight Actuation Solutions

The automotive industry’s transition toward electrification and lightweight design principles is fostering demand for cable drive actuators, particularly in electric vehicle (EV) applications. These actuators contribute to weight reduction and energy efficiency, critical factors in EV performance. Major automotive manufacturers are incorporating cable-driven mechanisms in throttle controls, braking systems, and adaptive seating, capitalizing on their ability to reduce friction and mechanical inertia. Furthermore, advancements in actuator materials, such as high-strength synthetic cables and corrosion-resistant alloys, are extending product lifespans and reducing maintenance costs. The automotive segment is projected to remain a substantial contributor to market growth, particularly in Europe and Asia-Pacific regions where EV adoption is highest.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Leaders Invest in Innovation to Capture Market Share

The global Cable Drive Actuator market is moderately consolidated, dominated by established automation and motion control manufacturers with complementary product offerings. Parker Hannifin and Bosch Rexroth currently lead the competitive landscape, collectively accounting for approximately 28% market share in 2024. These industry giants leverage their extensive distribution networks and integration capabilities with broader automation systems to maintain dominance.

Meanwhile, specialized manufacturers like Festo and Schunk are gaining traction through targeted innovations in precision cable actuator systems, particularly for medical and semiconductor applications. Recent data indicates Festo grew its actuator business by 6.2% year-over-year in 2023, driven by increased demand for modular cable drive solutions.

Robotics-focused players such as KUKA and Yaskawa are adopting vertical integration strategies, developing proprietary cable actuator technologies to complement their robotic arm systems. This approach helps them control component quality while creating competitive differentiation in high-growth automation segments.

Several companies are accelerating market expansion through strategic acquisitions. Parker Hannifin’s 2023 acquisition of a specialized linear motion manufacturer strengthened its cable actuator portfolio for aerospace applications, demonstrating how consolidation is reshaping the competitive environment.

List of Key Cable Drive Actuator Manufacturers

- Parker Hannifin Corporation (U.S.)

- Bosch Rexroth AG (Germany)

- Festo SE & Co. KG (Germany)

- KUKA AG (Germany)

- Siemens AG (Germany)

- Schunk GmbH (Germany)

- Yaskawa Electric Corporation (Japan)

- Velan Inc. (Canada)

- RS Components Ltd. (UK)

Segment Analysis:

By Type

Parallel Cable Drive Segment Leads the Market Due to Increased Demand in High-Precision Applications

The market is segmented based on type into:

- Parallel Cable Drive

- Subtypes: Multi-axis synchronized systems, Compact parallel actuators

- Series Single Cable Drive

- Others

- Subtypes: Rotary cable actuators, Linear cable actuators

By Application

Industrial Automation Segment Dominates Due to Growing Adoption in Manufacturing Processes

The market is segmented based on application into:

- Industrial Automation

- Subtypes: Robotic arms, CNC machinery, Assembly lines

- Medical Industry

- Subtypes: Surgical robots, Rehabilitation equipment

- Automotive Industry

- Subtypes: Vehicle assembly systems, Testing equipment

- Others

- Subtypes: Aerospace applications, Marine equipment

By End User

Manufacturing Sector Accounts for Largest Share Due to Widespread Industrial Automation

The market is segmented based on end user into:

- Manufacturing

- Healthcare

- Automotive

- Aerospace and Defense

- Others

By Operation Type

Electric Cable Drive Actuators Gain Traction Due to Energy Efficiency

The market is segmented based on operation type into:

- Electric

- Hydraulic

- Pneumatic

- Hybrid

Regional Analysis: Cable Drive Actuator Market

Asia-Pacific

The Asia-Pacific region dominates the global cable drive actuator market, accounting for over 40% of total revenue share in 2024. China’s massive industrial automation expansion, coupled with Japan’s leadership in precision robotics, drives demand for high-performance cable drive systems. The “Made in China 2025” initiative has particularly accelerated adoption in manufacturing automation. India presents strong growth potential with increasing automotive production and medical device manufacturing investments. While cost-competitive local manufacturers have gained traction, multinational players like Yaskawa and KUKA maintain technological superiority in high-end applications such as semiconductor manufacturing and surgical robotics.

North America

North America represents the second-largest market, with the U.S. contributing nearly 60% of regional demand. Stringent FDA regulations in medical applications and the proliferation of Industry 4.0 practices have compelled manufacturers to adopt advanced actuator technologies. The aerospace sector remains a key consumer, particularly for parallel cable drive systems in flight control mechanisms. Recent CHIPS Act funding has stimulated demand in semiconductor manufacturing equipment. However, higher labor costs and preference for alternative actuation technologies in certain applications slightly constrain market growth compared to Asia-Pacific.

Europe

Europe maintains a strong position in the cable drive actuator market, with Germany leading due to its robust automotive and industrial equipment sectors. The region shows particular strength in medical applications, where strict EU regulations on medical devices drive demand for precision cable actuation systems. Festo and Bosch Rexroth continue to introduce innovative solutions targeting energy efficiency and miniaturization. While Western European markets show maturity with moderate growth rates, Eastern European nations are emerging as manufacturing hubs with increasing actuator adoption. Brexit-induced supply chain disruptions have somewhat impacted the UK market’s growth trajectory.

South America

The South American cable drive actuator market remains in growth phase, with Brazil accounting for over 50% of regional consumption. Increasing automotive production and gradual automation adoption in mining equipment present key opportunities. However, economic volatility and limited local manufacturing capabilities have constrained market expansion. Most high-end actuators are imported, making the region price-sensitive. Recent trade agreements have improved access to cost-effective Asian alternatives, potentially accelerating adoption in industrial automation applications across the region’s growing manufacturing sector.

Middle East & Africa

This emerging market shows promising growth in cable drive actuator adoption, particularly in oil & gas and renewable energy applications. The UAE and Saudi Arabia lead in technological adoption, driven by economic diversification initiatives. Medical tourism growth has spurred demand for actuator-based surgical equipment in select Middle Eastern countries. However, limited industrial diversification and reliance on imports restrict overall market penetration. Infrastructure development projects across Africa present long-term opportunities, though political instability and underdeveloped supply chains remain significant barriers to market expansion.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Cable Drive Actuator markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Cable Drive Actuator market was valued at USD 1,593 million in 2024 and is projected to reach USD 2,168 million by 2032, growing at a CAGR of 4.9%.

- Segmentation Analysis: Detailed breakdown by product type (Parallel Cable Drive, Series Single Cable Drive, Others), application (Industrial Automation, Medical Industry, Automotive Industry, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with specific analysis of key markets like the U.S., China, Germany, and Japan.

- Competitive Landscape: Profiles of leading market participants including Velan, Parker Hannifin, Festo, KUKA, Siemens, Bosch Rexroth, Schunk, Yaskawa, and RS Components, covering their market share, product portfolios, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging actuator technologies, integration with automation systems, and advancements in cable drive mechanisms.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as industrial automation trends, alongside challenges like supply chain complexities and high precision requirements.

- Stakeholder Analysis: Strategic insights for manufacturers, suppliers, system integrators, and investors regarding market opportunities and competitive positioning.

The research methodology combines primary interviews with industry experts and secondary data from verified sources to ensure accuracy and reliability of market intelligence.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Cable Drive Actuator Market?

-> Cable Drive Actuator Market was valued at 1593 million in 2024 and is projected to reach US$ 2168 million by 2032, at a CAGR of 4.9% during the forecast period.

Which key companies operate in Global Cable Drive Actuator Market?

-> Key players include Velan, Parker Hannifin, Festo, KUKA, Siemens, Bosch Rexroth, Schunk, Yaskawa, and RS Components.

What are the key growth drivers?

-> Key growth drivers include increasing industrial automation, demand for precision motion control, and expansion of medical robotics applications.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth, while North America and Europe remain technologically advanced markets.

What are the emerging trends?

-> Emerging trends include miniaturization of actuators, integration with IoT systems, and development of maintenance-free cable drive solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...