C-band Pulsed EDFA Market Insights

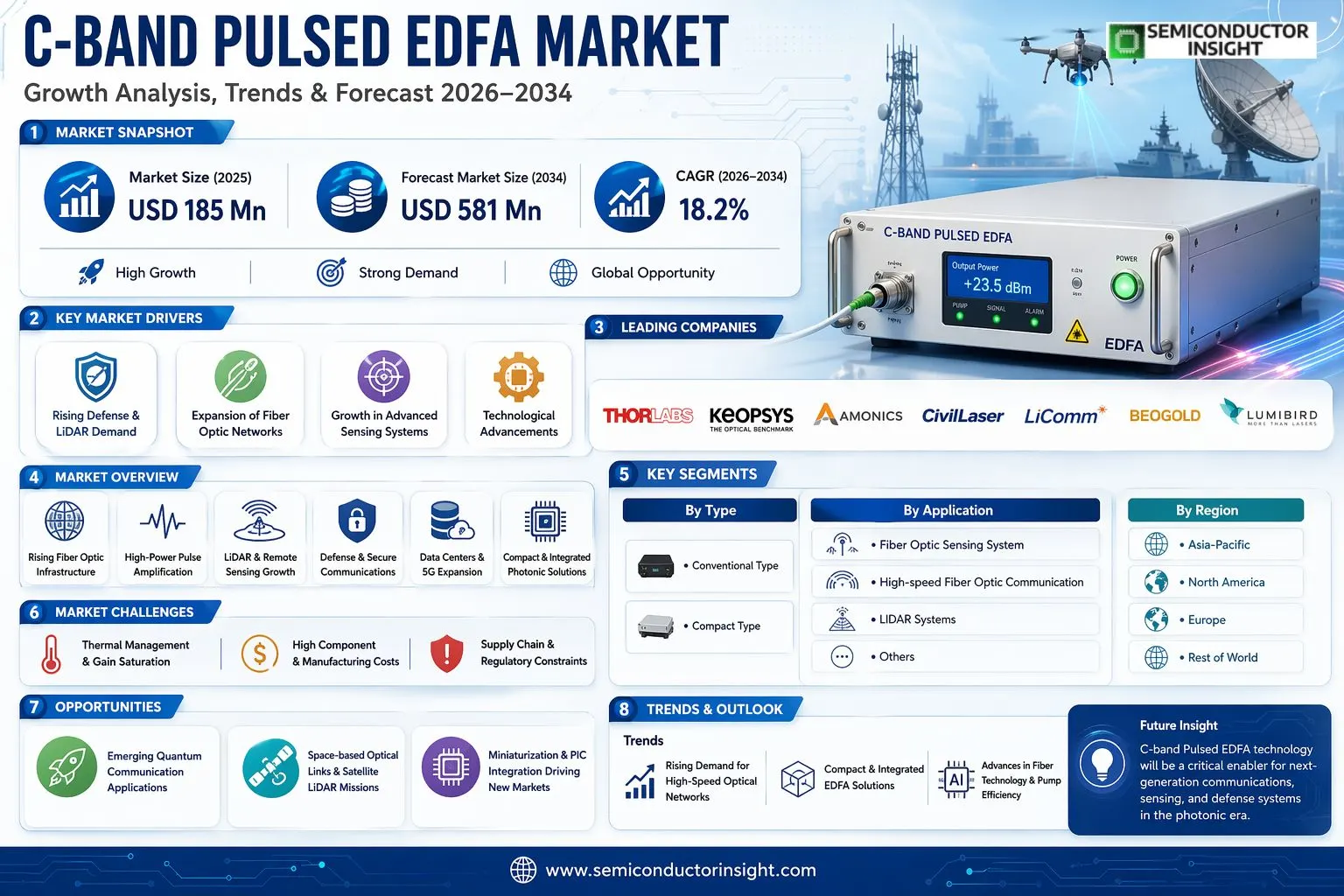

Global C-band Pulsed EDFA market size was valued at USD 185 million in 2025. The market is projected to grow from USD 219 million in 2026 to USD 581 million by 2034, exhibiting a CAGR of 18.2% during the forecast period.

EDFA is an optical amplifier based on erbium-doped fiber, utilizing the energy level transition of erbium ions to amplify optical signals across a defined wavelength range. C-band Pulsed EDFA is a specialized optical amplifier designed to amplify pulse signals operating within the C-band range (approximately 1530–1565 nm), making it particularly suited for high-precision sensing and advanced optical communication applications. These amplifiers are available in Conventional Type and Compact Type configurations, serving end-use applications including fiber optic sensing systems, high-speed fiber optic communication, and other emerging photonic applications.

The market is witnessing robust expansion driven by the surging demand for high-speed fiber optic communication infrastructure, growing deployment of distributed fiber optic sensing systems, and accelerating investments in photonics and optical networking technologies worldwide. Furthermore, the increasing adoption of light detection and ranging (LiDAR) technologies and the expansion of 5G backbone networks are creating substantial demand for high-performance pulsed amplifiers. Key manufacturers operating in the global C-band Pulsed EDFA market include LiComm, Beogold, Amonics, CivilLaser, Keopsys, and Thorlabs, among others, collectively shaping a competitive and innovation-driven landscape.

MARKET DRIVERS

Surging Demand for High-Power Optical Amplification in Defense and LiDAR Applications

C-band Pulsed EDFA Market is experiencing robust momentum driven by the accelerating adoption of high-peak-power optical amplifiers across defense, aerospace, and advanced sensing sectors. Pulsed Erbium-Doped Fiber Amplifiers operating in the C-band (1530–1565 nm) are increasingly preferred for range-finding, target designation, and free-space optical communication systems, where short-duration, high-intensity pulses are operationally critical. The alignment of the C-band with established telecom-grade fiber infrastructure further reduces integration costs, making pulsed EDFA solutions commercially attractive for system integrators and original equipment manufacturers.

Expansion of Coherent Optical Communication Infrastructure

Global investments in next-generation coherent optical networks are creating a secondary but significant pull for C-band pulsed EDFA technology. As hyperscale data center operators and telecommunications carriers deploy 400G and 800G transceivers over long-haul and metro routes, the need for amplification modules capable of handling both continuous-wave and pulsed signal formats has intensified. C-band pulsed EDFAs provide the gain bandwidth and noise figure performance required to support dense wavelength division multiplexing (DWDM) channels, enabling carriers to maximize spectral efficiency without incurring penalties from amplified spontaneous emission.

➤ The convergence of defense-grade pulsed laser requirements and commercial fiber optic network expansion is positioning C-band Pulsed EDFA Market as a strategically critical segment within the broader photonics industry, attracting increased R&D investment from both established players and emerging technology firms.

Additionally, the rapid proliferation of industrial and scientific LiDAR systems—used in autonomous vehicle sensing, atmospheric research, and topographic mapping—is reinforcing demand for compact, reliable C-band pulsed amplification. The C-band’s favorable atmospheric transmission window and compatibility with eye-safer wavelength bands are driving system architects to specify pulsed EDFA modules over competing solid-state or semiconductor amplifier technologies, further consolidating market growth prospects.

MARKET CHALLENGES

Thermal Management and Gain Saturation Under High-Repetition Pulsed Regimes

One of the most technically demanding challenges facing C-band Pulsed EDFA Market is the management of thermal loading and gain saturation that occurs when amplifiers are operated at high pulse repetition frequencies. Under pulsed excitation, the erbium ion population inversion undergoes rapid depletion and recovery cycles, and at elevated repetition rates, incomplete inversion recovery leads to gain compression and pulse-to-pulse amplitude instability. Thermal gradients within the erbium-doped fiber can introduce stress-induced birefringence, degrading polarization purity and increasing insertion loss—both of which are critical performance parameters in precision sensing and coherent communication applications. Addressing these issues requires advanced fiber coil packaging, active thermal stabilization, and sophisticated pump laser management, all of which add to system complexity and manufacturing cost.

Other Challenges

High Component and Integration Costs

The fabrication of high-performance C-band pulsed EDFAs involves specialized rare-earth-doped fiber, high-brightness single-mode pump diodes, and precision fiber fusion splicing, all of which contribute to elevated bill-of-materials costs. For defense procurement programs operating under strict budgetary constraints, the per-unit cost of qualified pulsed EDFA modules remains a barrier to widespread platform integration, limiting near-term volume scaling opportunities for suppliers.

Regulatory and Export Control Barriers

C-band pulsed EDFA systems with peak power outputs exceeding certain thresholds are subject to dual-use export control regulations, including ITAR and EAR classifications in the United States and equivalent frameworks in other jurisdictions. These regulatory requirements impose compliance overhead on manufacturers seeking to address international defense and security markets, extending sales cycles and requiring dedicated legal and compliance resources that can strain the operational capacity of smaller technology developers.

MARKET RESTRAINTS

Competition from Alternative Amplification Technologies and Wavelength Bands

C-band Pulsed EDFA Market faces persistent competitive pressure from alternative amplification platforms, including thulium-doped fiber amplifiers (TDFAs) operating in the S-band, L-band EDFAs, and emerging semiconductor optical amplifier (SOA) technologies. In applications where compactness and low power consumption are prioritized over peak output power, semiconductor-based pulsed amplifiers are increasingly specified by system designers, particularly in cost-sensitive commercial LiDAR and industrial sensing segments. The maturation of these competing technologies is constraining the addressable market for C-band pulsed EDFAs in certain application verticals, requiring suppliers to continuously demonstrate differentiated performance advantages to maintain design-win momentum.

Supply Chain Vulnerabilities in Rare-Earth and Specialty Photonic Components

The production of C-band pulsed EDFA modules depends on a supply chain that includes specialty erbium-doped fiber, high-power pump laser diodes, and precision optical isolators—components that are sourced from a relatively concentrated group of global suppliers. Geopolitical tensions and trade policy uncertainties have introduced variability into the availability and pricing of these critical inputs, creating procurement risk for EDFA manufacturers. Lead times for qualified high-power pump diodes have extended in recent periods due to semiconductor fabrication capacity constraints, compelling some manufacturers to hold elevated safety stock levels and accept associated working capital burdens. These supply chain dynamics represent a structural restraint on the market’s ability to scale production responsively to demand surges.

MARKET OPPORTUNITIES

Integration with Next-Generation Free-Space Optical and Satellite Communication Systems

The accelerating deployment of low-earth-orbit (LEO) satellite constellations and high-altitude platform systems is opening a significant growth avenue for C-band pulsed EDFA suppliers. Free-space optical (FSO) communication terminals aboard satellites and airborne platforms require compact, radiation-tolerant optical amplifiers capable of delivering high-fidelity pulsed signal amplification across extended link distances. C-band pulsed EDFAs, with their well-characterized gain spectra and compatibility with existing single-mode fiber interfaces, are well positioned to serve as the core amplification element in these emerging platforms, provided that suppliers can demonstrate the necessary environmental qualification and size, weight, and power (SWaP) performance levels demanded by space-grade system integrators.

Advancements in Photonic Integration and Miniaturization Enabling New Market Segments

Progress in photonic integrated circuit (PIC) technology and advanced fiber packaging methodologies is creating opportunities for the development of next-generation miniaturized C-band pulsed EDFA modules suitable for deployment in unmanned aerial vehicles, handheld range-finding instruments, and portable medical diagnostic equipment. As manufacturing techniques for erbium-doped waveguide amplifiers on planar substrates continue to mature, the cost and size barriers associated with traditional discrete fiber-based pulsed EDFA architectures are expected to diminish, enabling market penetration into application segments that were previously inaccessible due to form-factor constraints. Companies investing in chip-scale pulsed EDFA development are likely to secure first-mover advantages in these high-growth adjacent markets, broadening the overall commercial scope of C-band pulsed amplification technology well beyond its traditional defense and telecommunications strongholds.

Trends

Expanding Role of C-band Pulsed EDFA in High-Speed Fiber Optic Communication

C-band Pulsed EDFA Market is witnessing accelerated momentum driven by the rapid global expansion of high-speed fiber optic communication infrastructure. As network operators and telecom providers scale their data transmission capabilities to meet surging bandwidth demands, C-band Pulsed EDFA technology has emerged as a critical enabler. These optical amplifiers, which leverage erbium-doped fiber to amplify pulse signals within the C-band spectral range, offer superior signal integrity over long-haul transmission distances. The increasing deployment of wavelength-division multiplexing systems has further reinforced demand, as C-band Pulsed EDFAs are well-suited to amplify multiple channels simultaneously with minimal noise accumulation. North America and Asia, particularly China and Japan, are among the leading regions contributing to this demand uptick, supported by ongoing investments in next-generation optical network upgrades.

Other Trends

Rising Adoption in Fiber Optic Sensing Systems

Beyond communications, C-band Pulsed EDFA Market is seeing notable traction in fiber optic sensing applications. Industries such as oil and gas, structural health monitoring, and aerospace are increasingly utilizing pulsed EDFA-based systems for distributed sensing due to their ability to deliver high-peak-power optical pulses with precise timing. This trend is encouraging manufacturers to develop application-specific variants that balance pulse energy, repetition rate, and spectral purity. The growing emphasis on industrial automation and smart infrastructure is expected to sustain this demand trajectory, particularly across European and Asia-Pacific markets where industrial sensing investments are intensifying.

Shift Toward Compact and Integrated Product Designs

A significant product-level trend shaping C-band Pulsed EDFA Market is the transition from conventional form factors to compact, integrated designs. While the Conventional Type continues to hold a substantial market share due to its established performance benchmarks, the Compact Type segment is gaining ground rapidly. End users in laboratory, defense, and portable instrumentation segments are prioritizing space-efficient solutions without compromising optical output quality. Leading manufacturers including Thorlabs, Keopsys, and Amonics are actively investing in miniaturization technologies and modular architectures to address this evolving preference.

Competitive Innovation and Strategic Positioning Among Key Manufacturers

The competitive landscape of C-band Pulsed EDFA Market is characterized by continuous product innovation and strategic differentiation. Key global players such as LiComm, Beogold, Amonics, CivilLaser, Keopsys, and Thorlabs are focusing on enhancing gain flatness, improving pulse fidelity, and expanding operational flexibility across varying input power conditions. Collaboration with system integrators and increased participation in regional distribution networks are also emerging as key go-to-market strategies. As the technology matures, players that can offer scalable, reliable, and cost-effective C-band Pulsed EDFA solutions are well-positioned to capture a larger share of this evolving global market.

COMPETITIVE LANDSCAPE

Key Industry Players

C-band Pulsed EDFA Market: Competitive Dynamics, Leading Manufacturers, and Strategic Positioning

The global C-band Pulsed EDFA market, valued at approximately USD 185 million in 2025 and projected to reach USD 581 million by 2034 at a robust CAGR of 18.2%, is characterized by a moderately consolidated competitive landscape where a handful of specialized photonics and fiber optics companies command significant revenue share. The top five players collectively accounted for a notable share of global revenues in 2025, reflecting the high degree of technical expertise and capital investment required to manufacture high-performance erbium-doped fiber amplifiers capable of delivering pulsed optical gain within the C-band spectrum. Market leaders differentiate themselves through superior pulse shaping capabilities, high peak power output, low noise figure performance, and the ability to serve dual-demand segments spanning fiber optic sensing systems and high-speed fiber optic communication infrastructure. Companies such as Keopsys and Thorlabs have established strong footholds owing to their broad photonics product portfolios, established distribution networks, and sustained investment in R&D. LiComm and Amonics have similarly positioned themselves as competitive forces by offering application-specific C-band pulsed EDFA solutions tailored for both conventional and compact form factor requirements across global end-user verticals.

Beyond the leading incumbents, a growing number of niche and regionally significant players are intensifying competition within C-band Pulsed EDFA Market. Companies such as Beogold and CivilLaser serve targeted market segments, particularly in Asia, where demand from China, Japan, South Korea, and Southeast Asia continues to accelerate driven by expanding fiber optic communication deployments and industrial sensing applications. The competitive environment is further shaped by ongoing product innovation, strategic mergers and acquisitions, capacity expansions, and efforts to develop compact-type EDFA modules that reduce system integration complexity for OEM customers. Price competitiveness, especially among Asian manufacturers, is also emerging as a key differentiating factor, while Western players continue to emphasize performance benchmarks, reliability certifications, and after-sales technical support. As the market matures through the forecast period to 2034, competitive pressures are expected to intensify, prompting further consolidation and technology partnerships across the value chain.

List of Key C-band Pulsed EDFA Companies Profiled

- Keopsys

- Thorlabs

- Amonics

- CivilLaser

- LiComm

- Beogold

- IPG Photonics

- II-VI Incorporated (Coherent Corp.)

- Lumentum Holdings

- Finisar (II-VI)

- Furukawa Electric

- NTT Electronics

- Alnair Labs

- Accelink Technologies

- O-Net Technologies

Need proxies cheaper than the market?

https://op.wtf

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Conventional Type continues to hold a dominant position in C-band Pulsed EDFA Market, driven by its well-established design architecture and proven reliability across long-haul optical communication deployments.

|

| By Application |

|

High-speed Fiber Optic Communication represents the most prominent application segment for C-band Pulsed EDFAs, underpinned by surging global demand for high-bandwidth data transmission infrastructure.

|

| By End User |

|

Telecom Operators & Network Service Providers form the largest and most influential end-user base for C-band Pulsed EDFAs, consistently driving procurement volumes through network modernization and capacity expansion programs.

|

| By Output Power Level |

|

High Power C-band Pulsed EDFAs are experiencing robust demand growth, driven by the expanding requirements of advanced sensing, industrial laser processing, and defense photonics applications that necessitate amplifiers capable of delivering intense peak pulse energies without compromising spectral purity.

|

| By Sales Channel |

|

Direct Sales through OEM partnerships and System Integrators constitute the dominant commercial channel for C-band Pulsed EDFA transactions, reflecting the technically complex and specification-driven nature of the procurement process in this market.

|

Need proxies cheaper than the market?

https://op.wtfI’ll generate a detailed regional analysis for C-band Pulsed EDFA Market following the exact HTML template provided.

c-band-pulsed-edfa-regional-analysis text/html C-band Pulsed EDFA Market – Regional Analysis

Regional Analysis: C-band Pulsed EDFA Market

North America hosts some of the world’s most advanced photonics research centers, enabling continuous refinement of C-band Pulsed EDFA architectures. Collaborative efforts between universities, federal agencies, and commercial entities have produced breakthroughs in pulse shaping, gain optimization, and noise reduction, keeping the region at the forefront of next-generation optical amplifier development well into the 2030s.

Robust procurement budgets allocated to defense and aerospace sectors in the United States create sustained demand for high-performance C-band Pulsed EDFA systems used in directed energy, target designation, and atmospheric sensing. The region’s strategic emphasis on optical countermeasures and secure free-space communications continues to stimulate specialized pulsed amplifier development across multiple defense contractors.

The rapid expansion of hyperscale data centers and the ongoing rollout of high-capacity fiber optic backbone networks across North America are generating significant opportunities for C-band Pulsed EDFA integration. Providers are increasingly incorporating pulsed amplification to support burst-mode transmission, wavelength-division multiplexing upgrades, and ultra-low-latency optical interconnects essential for cloud computing infrastructure.

North American regulatory bodies and standards organizations play a pivotal role in shaping global frameworks for optical amplifier performance and safety compliance. Active participation from the region’s industry stakeholders in IEEE, TIA, and ITU working groups ensures that C-band Pulsed EDFA specifications align with emerging application requirements, providing a stable and predictable commercial environment for manufacturers and end-users alike.

Europe

Europe represents a strategically significant region within the global C-band Pulsed EDFA market, characterized by strong industrial photonics capabilities, progressive research funding frameworks, and a growing emphasis on sovereign technology resilience. Countries such as Germany, the United Kingdom, France, and the Netherlands are home to leading fiber optics manufacturers and academic institutions conducting pioneering research in erbium-doped amplification. The European Union’s Horizon Europe program and various national photonics initiatives continue to channel investment into advanced optical systems, including C-band Pulsed EDFA platforms used in scientific instrumentation, medical diagnostics, and industrial laser processing. Europe’s automotive sector, particularly its adoption of LiDAR for autonomous vehicle programs, is emerging as a notable demand driver for pulsed fiber amplifiers. Additionally, European defense agencies are increasingly evaluating C-band Pulsed EDFA technologies for airborne and ground-based sensing platforms, reflecting a broader trend toward optically enabled warfare and surveillance capabilities across NATO member states.

Asia-Pacific

Asia-Pacific is rapidly emerging as the fastest-growing regional market for C-band Pulsed EDFA solutions, propelled by aggressive telecommunications infrastructure investment, expanding defense modernization programs, and a burgeoning photonics manufacturing base. China, Japan, South Korea, and India are the primary contributors to regional growth, each pursuing distinct yet complementary trajectories in optical amplifier adoption. China’s large-scale fiber optic network deployments and state-sponsored photonics research programs represent a transformative force in the regional landscape. Japan’s precision manufacturing heritage and deep expertise in optical components continue to yield high-quality EDFA products catering to both domestic and export markets. South Korea’s advanced semiconductor ecosystem provides synergistic advantages for integrated photonic device development, while India’s growing telecommunications sector and defense self-reliance initiatives are creating new procurement avenues for C-band Pulsed EDFA suppliers targeting the subcontinent.

South America

South America occupies an emerging position in C-band Pulsed EDFA Market, with growth driven primarily by telecommunications modernization, academic research investments, and gradual expansion of industrial laser applications. Brazil stands out as the region’s dominant market, supported by a relatively advanced fiber optic infrastructure and a growing number of photonics research institutions affiliated with federal universities. Argentina and Chile also contribute to regional demand, particularly through academic and scientific research applications requiring precise optical amplification. While the South American market remains smaller in scale compared to North America, Europe, and Asia-Pacific, its long-term trajectory is encouraging. Increasing foreign direct investment in digital infrastructure, coupled with government-led broadband expansion programs, is expected to create a more favorable environment for C-band Pulsed EDFA adoption across key verticals including telecommunications, remote sensing, and environmental monitoring throughout the 2026 to 2034 forecast period.

Middle East & Africa

The Middle East and Africa region presents a developing yet strategically noteworthy market for C-band Pulsed EDFA technologies, with growth anchored in telecommunications infrastructure expansion, defense capability enhancement, and emerging smart city initiatives. Gulf Cooperation Council nations, particularly the United Arab Emirates, Saudi Arabia, and Qatar, are investing substantially in next-generation fiber optic networks and optical communication systems as part of broader digital transformation agendas. These investments are creating incremental demand for advanced optical amplifier technologies including C-band Pulsed EDFA platforms. In the defense domain, several Middle Eastern countries are procuring state-of-the-art sensing and directed energy systems that incorporate pulsed fiber amplifier components. Africa, while at an earlier stage of photonics market development, holds long-term potential as mobile and fixed-line broadband penetration increases and regional technology hubs in South Africa, Kenya, and Nigeria begin to engage with advanced optical networking solutions.

Report Scope

This market research report provides a comprehensive analysis of C-band Pulsed EDFA Market, covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of C-band Pulsed EDFA in powering advancements across industries such as fiber optic sensing, high-speed telecommunications, industrial automation, and optical communications.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type (Conventional Type, Compact Type), application (Fiber Optic Sensing System, High-speed Fiber Optic Communication, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, erbium-doped fiber amplifier design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of C-band Pulsed EDFA Market?

-> Global C-band Pulsed EDFA Market was valued at USD 185 million in 2025 and is expected to reach USD 581 million by 2034, growing at a CAGR of 18.2% during the forecast period.

Which key companies operate in C-band Pulsed EDFA Market?

-> Key players include LiComm, Beogold, Amonics, CivilLaser, Keopsys, and Thorlabs, among others. In 2025, the global top five players collectively held a significant share of the market in terms of revenue.

What are the key growth drivers?

-> Key growth drivers include rising demand for fiber optic sensing systems, expansion of high-speed fiber optic communication networks, increasing adoption of optical amplifiers in telecommunications infrastructure, and growing investments in advanced photonics technologies.

Which region dominates the market?

-> Asia is among the fastest-growing regions driven by strong demand from China, Japan, South Korea, and Southeast Asia, while North America remains a significant market with substantial contributions from the U.S.

What are the emerging trends?

-> Emerging trends include development of compact C-band Pulsed EDFA designs, integration with advanced fiber optic sensing systems, growing deployment in high-speed optical communication networks, and increasing R&D investments in erbium-doped fiber amplifier technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...