MARKET INSIGHTS

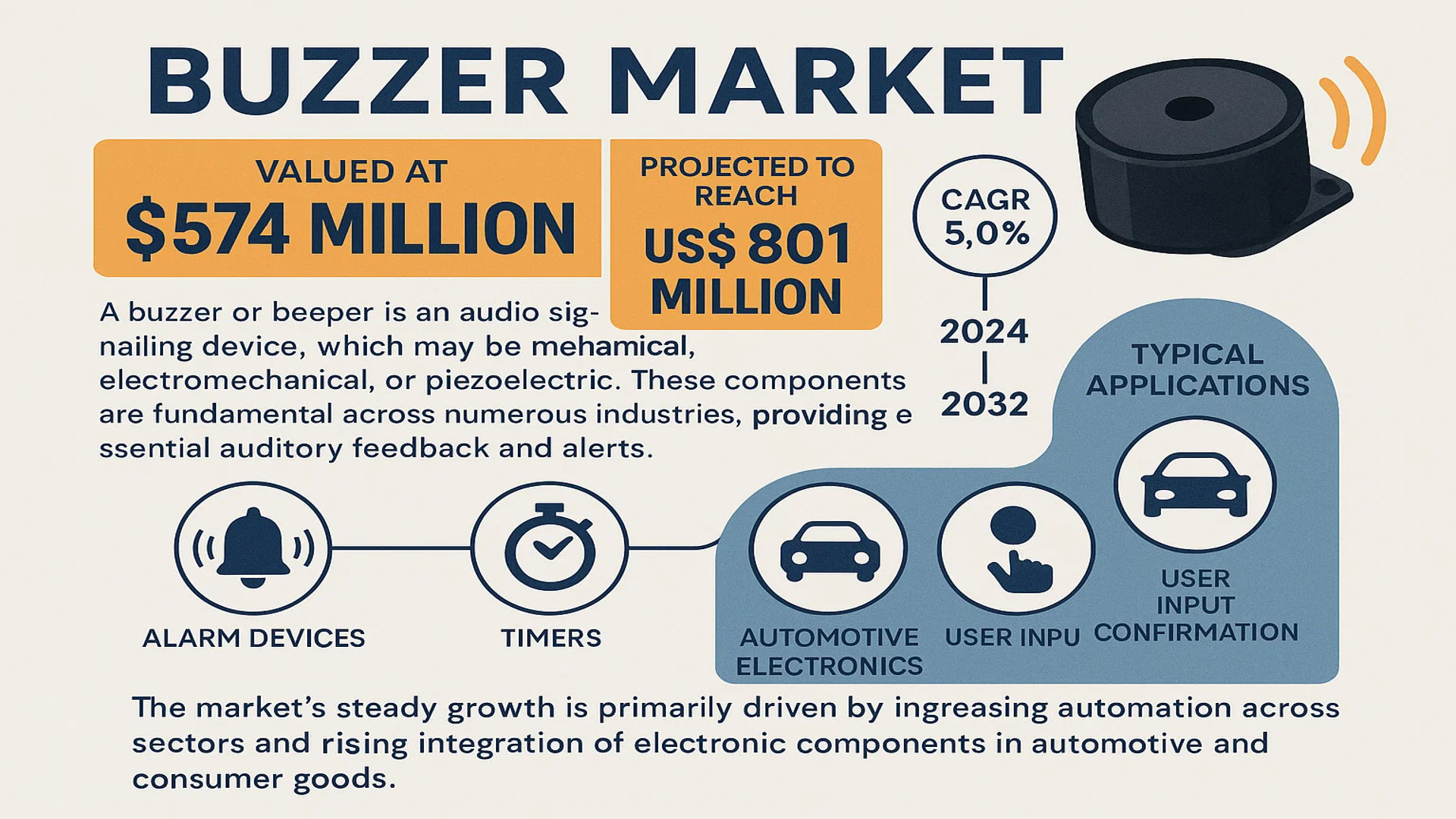

The global Buzzer Market was valued at 574 million in 2024 and is projected to reach US$ 801 million by 2032, at a CAGR of 5.0% during the forecast period.

A buzzer or beeper is an audio signalling device, which may be mechanical, electromechanical, or piezoelectric. These components are fundamental across numerous industries, providing essential auditory feedback and alerts. Typical applications include alarm devices, timers, automotive electronics, and user input confirmation such as a mouse click or keystroke.

The market’s steady growth is primarily driven by increasing automation across sectors and the rising integration of electronic components in automotive and consumer goods. However, the industry faces challenges such as price volatility of raw materials and intense competition among key manufacturers. Leading companies like Murata, TDK, and Kingstate Electronics collectively hold approximately 38% of the market share, focusing on innovation and expanding their product portfolios to maintain competitiveness.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand Across Automotive Electronics to Drive Market Growth

The automotive electronics sector represents a significant growth driver for the buzzer market, with increasing integration in vehicles for safety alerts, keyless entry confirmation, and electric vehicle (EV) status indicators. Global automotive production, which exceeded 85 million vehicles in 2023, continues to incorporate more electronic components per vehicle, directly boosting demand for reliable audio signaling devices. The transition toward electric and autonomous vehicles particularly accelerates this trend, as these vehicles require more sophisticated alert systems for both driver awareness and pedestrian safety. Furthermore, stringent government safety regulations mandating auditory warnings in vehicles for reversing and other functions create a stable, regulatory-driven demand stream that supports market expansion.

Expansion of Smart Home and IoT Devices to Accelerate Adoption

The proliferation of smart home devices and the broader Internet of Things (IoT) ecosystem presents substantial opportunities for buzzer integration. With over 15 billion connected IoT devices globally, the need for user feedback mechanisms—such as confirmation beeps for smart locks, appliance timers, and security system alarms—is growing exponentially. This sector’s expansion, projected to maintain a double-digit growth rate, directly correlates with increased buzzer shipments. The miniaturization and energy efficiency of modern piezoelectric buzzers make them particularly suitable for battery-operated IoT devices, enabling manufacturers to incorporate audible signals without significantly impacting power consumption or device size.

Increasing Industrial Automation to Fuel Market Development

Industrial automation continues to be a major catalyst for buzzer market growth, with manufacturing facilities increasingly using audio signals for equipment status alerts, process completion notifications, and safety warnings. The global industrial automation market, valued at approximately $200 billion, relies on buzzers as essential components in human-machine interface systems. As factories adopt Industry 4.0 standards and smart manufacturing practices, the requirement for reliable, durable audio indicators grows correspondingly. These industrial-grade buzzers must often meet specific standards for sound pressure levels and frequency ranges to ensure they are audible over machinery noise, creating demand for specialized products with higher performance characteristics.

MARKET RESTRAINTS

Price Sensitivity in Consumer Electronics to Limit Margin Expansion

While the buzzer market shows strong growth potential, significant price pressure from consumer electronics manufacturers restrains profit margins. Consumer electronics account for approximately 30% of global buzzer consumption, but this segment demonstrates extreme cost sensitivity, with manufacturers constantly seeking to reduce bill-of-materials expenses. This pressure forces buzzer producers to either absorb cost increases or risk losing volume contracts to competitors. The situation is particularly challenging for magnetic buzzers, which face competition from lower-cost alternatives in price-sensitive applications. Additionally, the trend toward miniaturization often requires research and development investments that cannot always be recovered through product pricing, creating financial constraints for market participants.

Technical Limitations in Harsh Environments to Constrain Application Scope

Buzzer technology faces inherent limitations in extreme environmental conditions, which restricts adoption in certain industrial and outdoor applications. Operating temperature ranges typically span from -20°C to 70°C for standard buzzers, making them unsuitable for applications requiring operation in more extreme temperatures without significant design modifications that increase costs. Additionally, buzzers generally offer limited protection against moisture, dust, and chemicals unless specifically engineered with protective housings, which again adds to manufacturing expenses. These technical constraints prevent market penetration in sectors such as heavy industrial manufacturing, marine applications, and certain automotive under-hood applications where more robust and expensive alternatives are required.

Audio Pollution Concerns to Impact Market Development in Residential Applications

Increasing awareness of noise pollution presents a growing challenge for buzzer implementation in residential and public environments. Regulatory bodies in numerous regions are implementing stricter guidelines regarding acceptable noise levels from electronic devices, particularly those used in household appliances and public notification systems. This trend requires manufacturers to develop buzzers that operate at lower volumes while maintaining audibility, often necessitating advanced acoustic engineering that increases production costs. Furthermore, consumer preference for visual or haptic feedback alternatives is growing in applications where audible signals may cause disturbance, creating competitive pressure from alternative notification technologies that do not generate sound.

MARKET CHALLENGES

Global Supply Chain Vulnerabilities to Challenge Production Consistency

The buzzer manufacturing industry faces significant challenges related to global supply chain dependencies, particularly for specialized components including piezoelectric elements, magnetic materials, and integrated circuits. Recent disruptions have highlighted vulnerabilities in the supply of rare earth materials essential for magnetic buzzers, with price volatility affecting production planning and cost structures. Additionally, the concentration of certain component manufacturing in specific geographic regions creates logistical challenges and potential single points of failure. These supply chain complexities require manufacturers to maintain higher inventory levels, implement dual-sourcing strategies, and absorb cost fluctuations, ultimately affecting profitability and delivery reliability across the market.

Other Challenges

Technological Transition Risks

The industry faces challenges related to the transition from traditional electromagnetic buzzers to piezoelectric alternatives. While piezoelectric technology offers advantages in power efficiency and miniaturization, the retooling costs and technical expertise required for manufacturing transition create significant barriers for established producers. This technological shift requires substantial capital investment in new production equipment and retraining of personnel, while simultaneously maintaining production capabilities for legacy products that remain in demand. The uncertainty regarding the pace of adoption across different application segments further complicates investment decisions and strategic planning.

Standardization and Compatibility Issues

The lack of global standardization in buzzer specifications creates compatibility challenges for manufacturers and end-users. Electrical characteristics, mounting configurations, and acoustic performance metrics vary significantly between suppliers, making it difficult for device manufacturers to substitute components without redesigning their products. This absence of standardization limits competitive pressure and can lead to vendor lock-in situations, particularly for custom-designed buzzers used in specialized applications. The industry faces the challenge of balancing customization needs with the benefits of standardization, a complex issue that affects procurement strategies and product development cycles.

MARKET OPPORTUNITIES

Advancements in Piezoelectric Technology to Open New Application Areas

Recent advancements in piezoelectric materials and manufacturing processes present significant opportunities for market expansion. Innovations in composite piezoelectric materials have enabled the development of buzzers with improved acoustic performance, broader frequency response, and reduced power consumption. These technological improvements are creating opportunities in emerging applications such as wearable medical devices, where miniaturized, low-power audio alerts are essential. Additionally, developments in multilayer piezoelectric elements allow for higher sound pressure levels from smaller form factors, addressing the growing need for effective audio signaling in space-constrained applications across consumer electronics, automotive, and industrial sectors.

Growing Electric Vehicle Production to Create New Demand Streams

The rapid expansion of the electric vehicle market represents a substantial growth opportunity for buzzer manufacturers. Regulatory requirements mandating acoustic vehicle alerting systems (AVAS) for EVs at low speeds have created a new application segment with significant volume potential. With global EV production exceeding 10 million units annually and projected to grow substantially, the demand for specialized buzzers meeting automotive-grade reliability and performance standards is increasing correspondingly. This application requires buzzers capable of producing specific frequency ranges and sound patterns to ensure pedestrian safety, creating opportunities for products with enhanced acoustic capabilities and environmental durability.

Integration with Smart City Infrastructure to Drive Future Growth

The development of smart city infrastructure worldwide presents long-term opportunities for buzzer implementation in public safety and notification systems. Urban infrastructure projects increasingly incorporate audio signaling devices for applications including traffic management, public transportation alerts, and emergency notification systems. These applications require buzzers with high reliability, weather resistance, and specific acoustic characteristics to ensure effectiveness in outdoor environments. The scale of smart city deployments, particularly across Asia and the Middle East, creates potential for substantial volume requirements over the coming decade, representing a strategic growth avenue for manufacturers capable of meeting the technical and regulatory requirements of these large-scale projects.

BUZZER MARKET TRENDS

Integration of Advanced Electronics and Miniaturization to Emerge as a Key Trend

The global buzzer market is experiencing a significant transformation driven by the pervasive integration of advanced electronics across consumer and industrial sectors. A key trend is the relentless push towards miniaturization, as modern electronic devices demand smaller, more efficient, and more power-conscious components. This is particularly evident in the automotive industry, where the average modern vehicle incorporates over 40 buzzer units for various alerts, from seatbelt reminders to electric vehicle proximity warnings. Furthermore, the evolution towards surface-mount device (SMD) technology buzzers, which offer better compatibility with automated assembly lines and reduced board space, is accelerating. This shift is complemented by advancements in sound pressure level (SPL) and power efficiency, allowing for clearer auditory signals without a corresponding increase in energy consumption, a critical factor for battery-operated Internet of Things (IoT) devices and portable electronics.

Other Trends

Rising Demand in Automotive Electronics and Electric Vehicles

The automotive sector represents one of the largest and fastest-growing application segments for buzzers, a trend fueled by increasing electronic content per vehicle and the global transition to electric vehicles (EVs). Modern vehicles utilize buzzers for a multitude of safety and convenience features beyond traditional alarms, including parking assistance systems, lane departure warnings, and alerts for open doors or low tire pressure. The EV segment, in particular, creates a unique demand for external acoustic vehicle alerting systems (AVAS) to ensure pedestrian safety due to the near-silent operation of electric motors at low speeds. Regulations mandating such systems in regions like the European Union and North America have created a substantial and sustained market driver, with the automotive segment accounting for approximately 30% of global buzzer consumption.

Expansion of Smart Home and Industrial Automation Applications

The proliferation of smart home ecosystems and industrial automation, often referred to as Industry 4.0, is substantially expanding the application horizons for buzzer components. In the consumer space, smart devices such as security systems, smoke and carbon monoxide detectors, smart locks, and home appliances rely on buzzers to provide immediate and clear user feedback and warnings. Concurrently, industrial automation leverages these components extensively within control panels, manufacturing equipment, and robotics for status indicators, error codes, and operational alerts. This dual demand from both consumer and industrial IoT is a powerful growth vector, as the number of connected devices globally is projected to exceed 29 billion by 2030, each potentially requiring reliable audio signalling solutions. This trend emphasizes the need for buzzers that offer not only reliability but also a range of tones and volumes to convey different types of information effectively in varied environmental conditions.

COMPETITIVE LANDSCAPE

Key Industry Players

Manufacturers Focus on Technological Innovation and Geographic Expansion to Enhance Market Position

The global buzzer market exhibits a fragmented competitive structure, characterized by numerous established multinational corporations alongside a multitude of regional and specialized manufacturers. This dynamic creates a highly competitive environment where companies compete primarily on technological innovation, product reliability, and cost-effectiveness. Murata Manufacturing Co., Ltd. and TDK Corporation are recognized as dominant forces, collectively commanding a significant portion of the market share. Their leadership is underpinned by extensive research and development capabilities, a diverse and advanced product portfolio encompassing both piezoelectric and electromagnetic buzzers, and a robust global distribution network that serves a wide array of industries from automotive to consumer electronics.

Following these leaders, companies like Kingstate Electronics Corp. and OMRON Corporation have also secured substantial market presence. Their growth is largely driven by strong relationships with downstream manufacturers, particularly in the automotive and industrial automation sectors, and a consistent focus on producing high-quality, durable components that meet stringent international standards. These players have successfully expanded their footprint beyond their domestic markets, establishing production facilities and sales offices in key regions to better serve local demand and reduce logistical complexities.

The competitive intensity is further amplified by the strategic activities of mid-sized players. Companies such as DB PRODUCTS LIMITED and CUI Inc are aggressively pursuing market share through targeted product development and strategic partnerships. For instance, recent industry movements have seen an increased focus on developing buzzers with lower power consumption and smaller form factors to cater to the burgeoning portable and IoT device markets. Furthermore, mergers and acquisitions, though less frequent, are a tactic employed by larger entities to consolidate market position and acquire novel technologies or access new customer bases.

Meanwhile, several Chinese manufacturers, including Changzhou Chinasound and Dongguan Ruibo, are strengthening their influence globally by leveraging cost-competitive manufacturing and scaling up production capacities. Their strategy often involves offering a wide range of products at aggressive price points, making them formidable competitors in price-sensitive market segments. However, to move up the value chain, these companies are increasingly investing in quality control and obtaining necessary certifications to appeal to a broader, more demanding international clientele.

List of Key Companies Profiled

- Murata Manufacturing Co., Ltd. (Japan)

- TDK Corporation (Japan)

- Kingstate Electronics Corp. (Taiwan)

- DB PRODUCTS LIMITED (UK)

- Changzhou Chinasound Electronics Co., Ltd. (China)

- CUI Inc (U.S.)

- Huayu Electronics (China)

- Hunston Electronics Co., Ltd. (China)

- DONGGUAN PARK’S INDUSTRIAL CO., LTD. (China)

- Ariose Electronics Co., Ltd. (China)

- Hitpoint Inc. (Japan)

- Mallory Sonalert Products, Inc. (U.S.)

- Dongguan Ruibo Electronics Co., Ltd. (China)

- Bolin Group (China)

- Soberton, Inc. (China)

- OMRON Corporation (Japan)

- KEPO Electronics Co., Ltd. (China)

- KACON (China)

- OBO Seahorn (Germany)

Segment Analysis:

By Type

Piezo Buzzers Segment Dominates the Market Due to Superior Acoustic Performance and Energy Efficiency

The market is segmented based on type into:

- Piezo Buzzers

- Magnetic Buzzers

By Application

Automotive Electronics Segment Leads Due to Increasing Integration of Safety and Notification Systems

The market is segmented based on application into:

- Automotive Electronics

- Alarm

- Toy

- Timer

- Others

By End User

Consumer Electronics Sector Holds Significant Share Driven by Proliferation of Smart Devices

The market is segmented based on end user into:

- Consumer Electronics

- Automotive

- Industrial

- Healthcare

- Others

By Operating Voltage

Low Voltage Buzzers are Prevalent Owing to Compatibility with Modern Portable Electronics

The market is segmented based on operating voltage into:

- Low Voltage (Below 12V)

- Medium Voltage (12V – 24V)

- High Voltage (Above 24V)

Regional Analysis: Buzzer Market

Asia-Pacific

The Asia-Pacific region dominates the global buzzer market, accounting for over 60% of total consumption by volume. This leadership position is driven by massive manufacturing hubs in China, Japan, and South Korea, which serve both domestic demand and global export markets. China, in particular, is the epicenter of production, home to major manufacturers like Murata, TDK, Kingstate Electronics, and Changzhou Chinasound. The region’s growth is fueled by its extensive electronics manufacturing sector, rapid urbanization, and increasing adoption of smart home devices and automotive electronics. While cost-competitive magnetic buzzers remain popular for high-volume applications, there is a noticeable shift towards higher-performance piezo buzzers, especially in automotive safety systems and premium consumer electronics. However, intense price competition and fluctuating raw material costs present ongoing challenges for manufacturers.

North America

North America represents a mature but technologically advanced market, characterized by demand for high-reliability, specialized buzzers with advanced acoustic performance. The region’s strong automotive sector, particularly in the United States, is a key driver, with buzzers being critical components in vehicle alarm systems, seatbelt reminders, and electric vehicle warnings. Furthermore, stringent product safety standards and a robust industrial automation sector necessitate buzzers that offer consistent performance and longevity. While the market is not the largest by volume, it is a high-value segment. Leading suppliers like CUI Inc and Mallory Sonalert are well-established, focusing on innovation in miniaturization and sound output clarity to meet the demands of advanced medical equipment, telecommunications infrastructure, and commercial security systems.

Europe

The European market is shaped by strict regulatory frameworks, including the Restriction of Hazardous Substances (RoHS) and Waste Electrical and Electronic Equipment (WEEE) directives, which mandate the use of environmentally compliant components. This has accelerated the adoption of lead-free and recyclable buzzer designs. Germany, France, and the U.K. are the largest markets, driven by their strong automotive and industrial manufacturing bases. European OEMs prioritize suppliers that can provide documentation for full compliance and product traceability. Innovation is focused on energy efficiency and integration with smart IoT ecosystems. While local manufacturing exists, a significant portion of components is sourced from Asian partners, requiring European firms to maintain rigorous quality control and supply chain management.

South America

The South American buzzer market is emerging, with growth primarily tied to the consumer electronics and automotive aftermarket sectors. Brazil and Argentina are the most significant markets, though economic volatility and currency fluctuations often impact import costs and final product pricing. This makes the market highly sensitive to cost, favoring more affordable magnetic buzzer types. The industrial and alarm system segments show steady, albeit slow, growth. The lack of a strong local manufacturing base means the region is largely dependent on imports from Asia and North America, which can lead to longer lead times and inventory challenges. Nonetheless, economic stabilization efforts and growing digitalization present long-term opportunities for market expansion.

Middle East & Africa

This region represents a developing market with potential concentrated in specific sectors and nations. The Gulf Cooperation Council (GCC) countries, such as Saudi Arabia and the UAE, show the most promise, driven by construction booms, smart city initiatives, and investments in infrastructure that incorporate security and fire alarm systems. South Africa also has a established industrial base that generates steady demand. However, the broader region’s growth is constrained by economic disparities, political instability in certain areas, and a relatively underdeveloped local electronics manufacturing industry. The market is primarily served by international distributors and suppliers, with a focus on durable, cost-effective products suitable for harsh environmental conditions. Long-term growth is anticipated as digital infrastructure continues to expand.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Buzzer markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Buzzer Market?

-> Buzzer Market was valued at 574 million in 2024 and is projected to reach US$ 801 million by 2032, at a CAGR of 5.0% during the forecast period.

Which key companies operate in Global Buzzer Market?

-> Key players include Murata, TDK, Kingstate Electronics, DB PRODUCTS LIMITED, Changzhou Chinasound, CUI Inc, Huayu Electronics, Hunston Electronics, DONGGUAN PARK’S INDUSTRIAL, Ariose, Hitpoint, Mallory Sonalert, Dongguan Ruibo, Bolin Group, Soberton, OMRON, KEPO Electronics, KACON, and OBO Seahorn, among others.

What are the key growth drivers?

-> Key growth drivers include increasing demand from automotive electronics, rising adoption in alarm systems, expansion in consumer electronics, and growing industrial automation applications.

Which region dominates the market?

-> Asia-Pacific is the dominant market, accounting for over 60% of global production and consumption, with China being the largest manufacturing hub.

What are the emerging trends?

-> Emerging trends include miniaturization of components, development of ultra-low power consumption buzzers, integration with smart IoT devices, and advancements in piezoelectric technology.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...