MARKET INSIGHTS

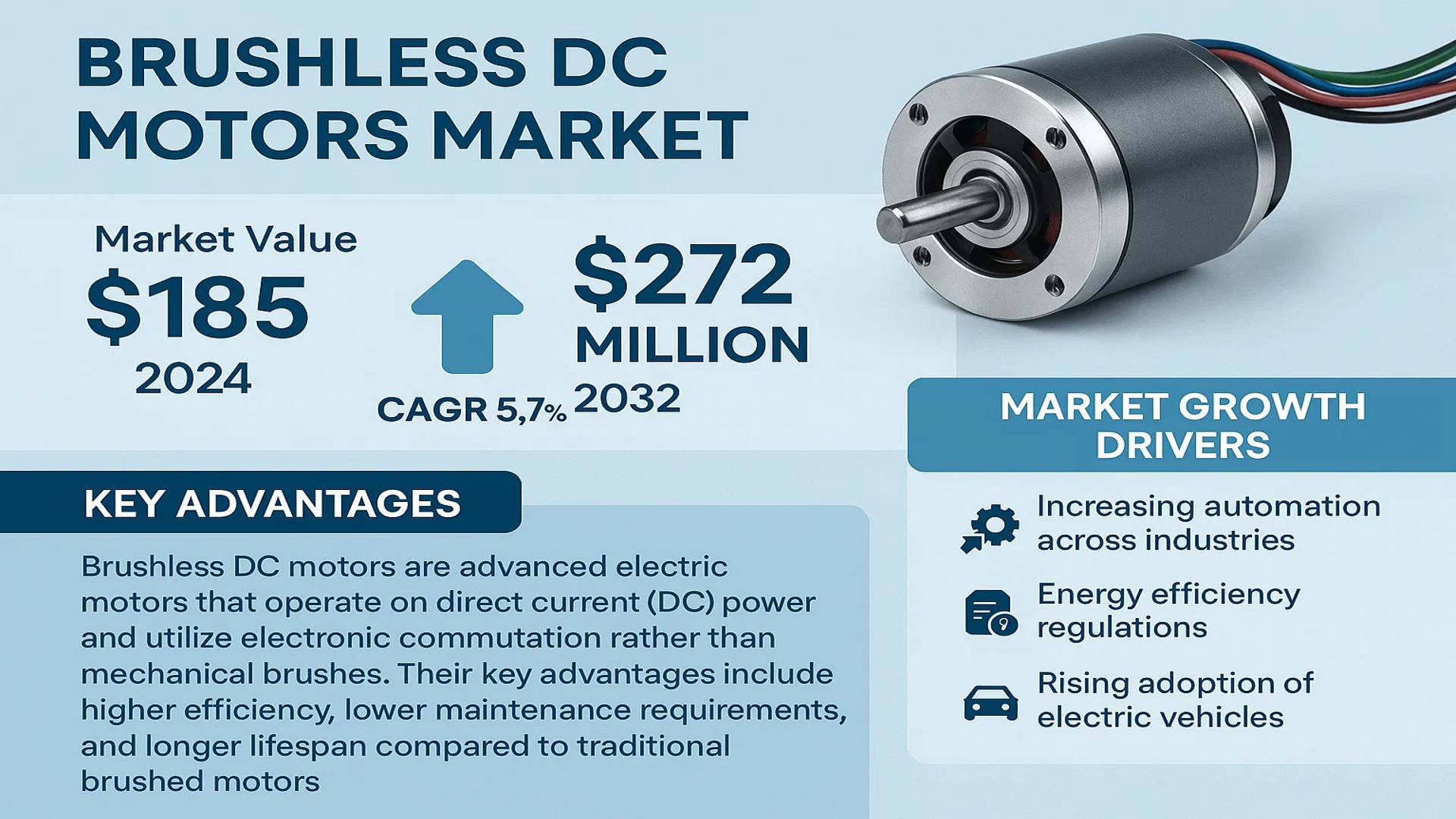

The global Brushless DC Motors Market was valued at 185 million in 2024 and is projected to reach US$ 272 million by 2032, at a CAGR of 5.7% during the forecast period.

Brushless DC motors are advanced electric motors that operate on direct current (DC) power and utilize electronic commutation rather than mechanical brushes. These motors feature a rotor with permanent magnets and a stator with wound coils, controlled by an integrated driver or external controller. Their key advantages include higher efficiency, lower maintenance requirements, and longer lifespan compared to traditional brushed motors.

The market growth is driven by increasing automation across industries, energy efficiency regulations, and the rising adoption of electric vehicles. Brushless DC motors find extensive applications in automotive systems, industrial automation, medical devices, and consumer electronics. Major manufacturers are focusing on developing compact, high-torque variants to meet evolving industry demands, particularly in robotics and electric mobility applications.

MARKET DYNAMICS

MARKET DRIVERS

Growing Industrial Automation Revolutionizing Brushless DC Motor Adoption

The rapid industrialization and automation across manufacturing sectors is significantly driving the demand for brushless DC (BLDC) motors. These motors offer superior efficiency – typically 85-90% compared to 75-80% for brushed motors – making them ideal for automated systems requiring continuous operation. The global robotics market, expected to exceed $75 billion by 2025, heavily relies on BLDC motors for their precision, reliability, and low maintenance characteristics. Furthermore, Industry 4.0 implementation across factories is accelerating the replacement of traditional motors with smart BLDC motor systems that can be integrated with IoT platforms for real-time monitoring and predictive maintenance.

Electric Vehicle Boom Creating Substantial Demand Growth

The automotive industry’s shift toward electrification presents a massive opportunity for BLDC motor manufacturers. With over 10 million electric vehicles sold globally in 2022, and projections suggesting this number will triple by 2030, BLDC motors are becoming indispensable components in various vehicle systems. These motors power critical functions including HVAC systems, power steering, and braking mechanisms due to their high torque-to-weight ratio and energy efficiency. The automotive segment now accounts for approximately 25% of all BLDC motor applications, with significant growth potential as EVs penetrate emerging markets.

Energy Efficiency Regulations Accelerating Market Transition

Stringent global energy efficiency standards are compelling manufacturers to phase out less efficient motor technologies. BLDC motors typically reduce energy consumption by 20-30% compared to their brushed counterparts, making them the preferred choice across industries aiming to meet carbon reduction targets. Various government initiatives promoting energy-efficient technologies through subsidies and tax incentives are further catalyzing this transition. The industrial sector alone represents over 40% of global electricity consumption, where motor systems contribute significantly to this usage, creating substantial opportunities for BLDC adoption.

MARKET RESTRAINTS

High Initial Costs Impeding Widespread Adoption

While BLDC motors offer long-term operational savings, their higher upfront cost remains a significant barrier, particularly in price-sensitive markets. The complex electronics required for operation, including controllers and sensors, can make BLDC systems 30-50% more expensive than conventional alternatives. These cost differentials prove particularly challenging in emerging economies where upfront cost considerations often outweigh lifecycle savings calculations. Furthermore, the specialized nature of BLDC motor installations often requires additional system integration expenses.

Technical Complexity Creates Implementation Challenges

The sophisticated control mechanisms essential for BLDC operation present implementation barriers that restrain market expansion. The requirement for precise electronic commutation demands specialized knowledge for both installation and maintenance, which is often scarce in developing markets. Additionally, the interoperability challenges between motors from different manufacturers create integration headaches for end-users. These technical complexities frequently result in longer deployment timelines and increased project risks for equipment manufacturers and system integrators.

Other Restraints

Supply Chain Vulnerabilities

The BLDC motor industry faces supply chain interruptions for critical raw materials like rare-earth magnets and electronic components. These materials are essential for motor production but subject to significant price volatility and geopolitical supply risks.

Limited Awareness in Emerging Markets

Despite their advantages, BLDC motors still suffer from low awareness among small and medium enterprises in developing economies, where traditional motor technology remains deeply entrenched.

MARKET OPPORTUNITIES

Smart Manufacturing Creating New Application Horizons

The integration of BLDC motors with Industry 4.0 technologies presents a transformative opportunity, enabling predictive maintenance and real-time performance optimization. Smart BLDC motors equipped with embedded sensors and connectivity can provide continuous operational data, allowing for condition monitoring that reduces downtime by up to 30%. This capability is particularly valuable in critical applications such as medical devices and aerospace systems where reliability is paramount. The ability to monitor motor health remotely also facilitates new service-based business models for manufacturers.

Next-Generation Battery Technologies Expanding Applications

Advancements in battery technology are creating new opportunities for BLDC motor adoption in cordless power tools and portable medical equipment. Lithium-ion battery improvements have extended operating times significantly, addressing one of the traditional limitations of battery-powered BLDC systems. This development has been particularly impactful in the power tools sector, where brushless motors now dominate premium product lines due to their extended runtime and durability advantages.

Renewable Energy Sector Opening New Verticals

The renewable energy industry presents substantial growth potential for BLDC motor applications, particularly in solar tracking systems and small wind turbines. These applications demand highly reliable motors capable of operating in challenging environmental conditions with minimal maintenance. The global solar tracker market alone is projected to grow significantly, creating additional demand for specialized BLDC motors designed for continuous outdoor operation.

MARKET CHALLENGES

Intellectual Property Battles Creating Industry Friction

The BLDC motor market faces increasing patent disputes as companies compete over proprietary technologies. These legal conflicts can delay product development and increase costs for manufacturers. The electronic control segments in particular have seen numerous patent infringement cases, creating uncertainty for companies developing new systems. Such disputes risk slowing innovation and diverting resources from product development to legal defenses.

Skilled Labor Shortage Constraining Market Expansion

The specialized knowledge required for BLDC motor design, implementation, and maintenance creates a significant workforce challenge. Many regions lack sufficient training programs to develop personnel capable of working with these sophisticated systems. This skills gap is particularly acute in emerging markets where technical education infrastructure lags behind technology adoption. The shortage inhibits market growth by limiting the implementation capabilities of potential customers.

Other Challenges

Standardization Hurdles

The lack of universal standards for BLDC motor interfaces and communication protocols creates interoperability challenges across different manufacturers’ products. This issue complicates system integration and limits the plug-and-play potential of these motors.

Cybersecurity Vulnerabilities

As BLDC motors become increasingly connected and smart, they face growing cybersecurity risks that could compromise operational integrity in critical applications.

BRUSHLESS DC MOTORS MARKET TRENDS

Rising Demand for Energy-Efficient Solutions to Propel Market Growth

The increasing global focus on energy efficiency is driving the adoption of brushless DC (BLDC) motors across various industries. Unlike traditional brushed motors, BLDC motors eliminate mechanical commutation, which reduces energy loss and enhances efficiency by up to 90%. Industries such as automotive, HVAC, and industrial automation are increasingly integrating BLDC motors to comply with stringent energy regulations. For instance, electric vehicle manufacturers prioritize these motors due to their high torque-to-weight ratio and reliability. Furthermore, the demand for smart home appliances like air conditioners and refrigerators is accelerating the shift toward brushless motors, which offer quieter operation and longer lifespans.

Other Trends

Industrial Automation and Robotics

The rapid expansion of automation in manufacturing and warehouse logistics is significantly boosting the demand for BLDC motors. Precision and reliability are critical in robotics, where BLDC motors excel due to their low maintenance requirements and high-speed control. Collaborative robots (cobots) and automated guided vehicles (AGVs) heavily rely on these motors for smooth and efficient motion control. The growth of Industry 4.0 and investments in smart factories further underscores the importance of BLDC motors in achieving seamless automation integration.

Technological Innovations Enhancing Motor Performance

Recent advancements in motor design and materials are enhancing the performance and application scope of BLDC motors. The development of high-performance permanent magnets, such as neodymium magnets, has significantly improved power density and thermal stability. Additionally, sensorless control technologies are emerging as a cost-effective alternative, eliminating the need for position sensors while maintaining accuracy. Innovations in integrated motor-drive systems are simplifying installation and reducing overall system costs, making BLDC motors more accessible to small and medium-sized enterprises. Coupled with IoT-enabled monitoring, these motors now offer predictive maintenance capabilities, reducing downtime in industrial applications.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansion Shape the Competitive Dynamics

The global brushless DC motors market features a semi-consolidated structure, with dominant players competing alongside specialized manufacturers across different voltage ranges and applications. Nidec Corporation leads the sector with its broad product portfolio spanning industrial automation, automotive, and consumer electronics applications. Their 2023 acquisition of Omron’s motor business further strengthened their technological edge in precision motor systems.

Minebea Mitsumi follows closely, capitalizing on its vertically integrated manufacturing capabilities and strong presence in Asian markets. The company’s recent investments in high-efficiency motors for HVAC systems demonstrate its focus on energy-saving solutions. Meanwhile, Maxon Motor maintains dominance in medical and robotics applications through its proprietary drive systems and customization capabilities.

Mid-tier players like Johnson Electric and Allied Motion are gaining traction through strategic collaborations with automotive OEMs and industrial automation providers. Johnson’s 2024 partnership with a leading EV battery manufacturer underscores the growing crossover between brushless motor technology and electric mobility solutions.

The competitive environment is further intensified by regional specialists such as China’s Topband and HyUnion Holding, who are capturing market share through aggressive pricing strategies and government-supported R&D initiatives in smart manufacturing applications.

List of Key Brushless DC Motor Manufacturers

- Nidec Corporation (Japan)

- Minebea Mitsumi Inc. (Japan)

- Shinano Kenshi Co., Ltd. (Japan)

- Maxon Motor (Switzerland)

- Johnson Electric Holdings (Hong Kong)

- Portescap (U.S.)

- Allied Motion Technologies (U.S.)

- HyUnion Holding (China)

- AMETEK Precision Motors (U.S.)

- ABB Motion (Switzerland)

- Panasonic Industrial Devices (Japan)

- Rockwell Automation (U.S.)

Segment Analysis:

By Type

200-400V Segment Leads Due to Wide Industrial and Automotive Applications

The market is segmented based on voltage into:

- Below 200V

- Subtypes: 12V, 24V, 48V

- 200-400V

- Above 400V

- Subtypes: 600V, 800V, and others

By Application

Automobile Manufacturing Segment Drives Demand for High-Efficiency Motors

The market is segmented based on application into:

- Automatic Instruments

- Medical Devices

- Consumer Electronics

- Automobile Manufacturing

- Others

By End User

Industrial Automation Sector Shows Significant Adoption for Precision Control

The market is segmented based on end user into:

- Industrial Automation

- Healthcare

- Consumer Electronics

- Automotive

- Others

Regional Analysis: Brushless DC Motors Market

Asia-Pacific

The Asia-Pacific region dominates the Brushless DC Motors market, accounting for over 43% of global demand, primarily driven by China’s manufacturing prowess and Japan’s technological leadership. China’s aggressive automation across industries, particularly in automotive and electronics manufacturing (where brushless motor adoption exceeds 65% among tier-1 suppliers), creates massive demand. Japan’s precision engineering culture fosters continuous innovation in high-performance motors for robotics and medical devices. India is emerging as a key growth market, with industrial automation investments growing at 12.3% annually. While cost sensitivity persists in Southeast Asia, the region benefits from Japanese and Chinese manufacturers establishing production clusters in Thailand and Vietnam to leverage lower labor costs.

North America

North America’s market is characterized by premium applications, with nearly 38% of brushless motors deployed in medical devices and aerospace systems. The U.S. leads in high-torque precision motors, supported by defense contracts and FDA-compliant medical equipment requirements. Canada’s growing EV component manufacturing (particularly in Ontario and Quebec) is driving brushless motor adoption in traction applications. Mexico serves as a strategic production hub, with motor manufacturers supplying both domestic appliance markets and U.S. automotive clients under USMCA trade provisions. However, supply chain realignments post-pandemic have increased localization pressures on motor manufacturers.

Europe

European demand centers on energy efficiency compliance, with EU Ecodesign Regulations mandating IE4 efficiency levels for most industrial motors. Germany’s Industry 4.0 initiatives accelerate brushless motor integration in smart manufacturing systems, particularly in automotive robotics. Nordic countries lead in marine and offshore applications, leveraging brushless motors’ corrosion resistance. Italy’s packaging machinery sector and France’s aerospace industry remain steady demand drivers. The region faces challenges from high energy costs impacting production economics, prompting gradual production shifts to Eastern Europe where labor and energy costs are 25-30% lower than Western Europe.

South America

Market growth in South America trails other regions, constrained by economic volatility and limited industrial automation penetration (below 35% in major industries). Brazil’s automotive sector shows promise, with brushless motor adoption in electric power steering systems exceeding 50% in new vehicle models. Argentina’s renewable energy sector drives demand for brushless generators in wind applications. However, import dependence on Chinese motors (covering 72% of regional demand) creates vulnerability to currency fluctuations. Local production remains limited to basic assemblies, with value-added manufacturing hindered by infrastructure gaps and technical skill shortages.

Middle East & Africa

The region presents a dichotomy – Gulf states demonstrate advanced adoption in oil/gas applications (where brushless motors power 49% of new pumping systems), while African markets remain largely untapped. UAE and Saudi Arabia lead smart city developments incorporating brushless motors in building automation and transportation. South Africa’s mining

Report Scope

This market research report provides a comprehensive analysis of the Global Brushless DC Motors market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 185 million in 2024 and is projected to reach USD 272 million by 2032, growing at a CAGR of 5.7%.

- Segmentation Analysis: Detailed breakdown by product type (Below 200V, 200~400V, Above 400V), application (Automatic Instruments, Medical Devices, Consumer Electronics, Automobile Manufacturing, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant. Asia-Pacific holds the largest market share, driven by rapid industrialization.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT in motor control systems, and evolving industry standards for energy efficiency and performance.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as automation trends and demand for energy-efficient motors, along with challenges like supply chain constraints and regulatory issues.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Brushless DC Motors Market?

-> Brushless DC Motors Market was valued at 185 million in 2024 and is projected to reach US$ 272 million by 2032, at a CAGR of 5.7% during the forecast period.

Which key companies operate in Global Brushless DC Motors Market?

-> Key players include Nidec, Minebea Mitsumi, Shinano Kenshi, Maxon Motor, Johnson Electric, ABB, and Panasonic, among others.

What are the key growth drivers?

-> Key growth drivers include increasing automation across industries, demand for energy-efficient motors, and growing adoption in electric vehicles and medical devices.

Which region dominates the market?

-> Asia-Pacific is the largest market, while North America shows significant growth potential due to technological advancements.

What are the emerging trends?

-> Emerging trends include smart motor controllers, integration with IoT systems, and development of high-torque density motors for industrial applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...