MARKET INSIGHTS

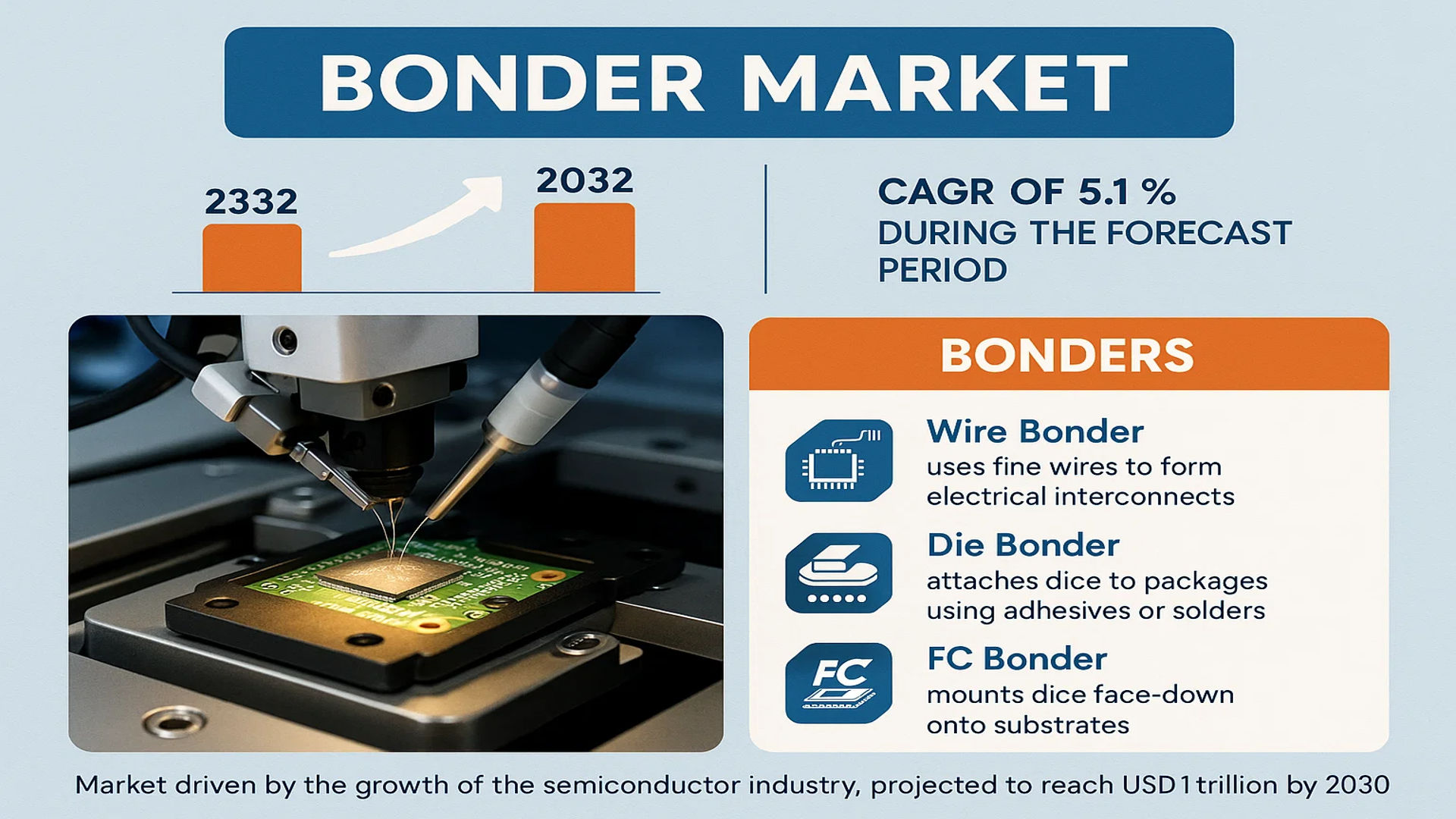

The global Bonder Market was valued at 2332 million in 2024 and is projected to reach US$ 3321 million by 2032, at a CAGR of 5.1% during the forecast period.

Bonders are specialized machines used in semiconductor manufacturing for creating electrical and mechanical connections between integrated circuits (ICs) and their packages. These precision instruments include Wire Bonder, Die Bonder, and FC Bonder (Flip Chip Bonder), each serving a distinct function in the assembly process. Wire bonders use fine gold or aluminum wires to form electrical interconnects, while die bonders attach semiconductor dice to packages using adhesives or solders. FC bonders mount dice face-down onto substrates, enabling direct connections for high-performance applications requiring superior electrical performance and thermal management.

The market is experiencing steady growth driven by the expansion of the global semiconductor industry, which is projected to reach USD 1 trillion by 2030. This growth is fueled by rising demand in key sectors such as 5G infrastructure, artificial intelligence, and automotive electronics. Furthermore, advancements in packaging technologies including 3D integration and wafer-level packaging are creating increased demand for high-precision bonding equipment. However, the market faces challenges including high technical barriers to entry and cost pressures, particularly for small and medium-sized enterprises. Leading players such as Besi, ASMPT Ltd, and Kulicke & Soffa dominate the market with continuous innovations in automation and precision engineering.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Expansion of Semiconductor Industry to Propel Bonder Demand

The global semiconductor industry is experiencing unprecedented growth, driven by advancements in 5G technology, artificial intelligence, Internet of Things (IoT), and automotive electronics. This expansion directly fuels demand for advanced packaging technologies, where bonders play a critical role. Semiconductor manufacturing equipment spending reached approximately $100 billion in 2024, representing a 15% year-over-year increase, with packaging equipment accounting for nearly 20% of this expenditure. The proliferation of smart devices and connected technologies requires increasingly sophisticated integrated circuits, necessitating precision bonding solutions. Furthermore, the automotive sector’s transition toward electric and autonomous vehicles has created substantial demand for semiconductor components, with modern vehicles containing an average of 1,400 semiconductor chips compared to just 550 in 2010. This exponential growth in semiconductor content across multiple industries establishes a robust foundation for bonder market expansion throughout the forecast period.

Advancements in Advanced Packaging Technologies to Accelerate Market Growth

Technological innovations in packaging methodologies, particularly wafer-level packaging (WLP), 3D integration, and heterogeneous packaging, are creating substantial opportunities for bonder manufacturers. These advanced packaging techniques require exceptionally high precision and reliability, driving demand for sophisticated bonding equipment. The market for advanced packaging technologies is projected to grow at a compound annual growth rate of 8.7% through 2030, significantly outpacing traditional packaging segments. Flip chip technology, which relies heavily on FC bonders, has seen particularly strong adoption in high-performance computing applications, with penetration rates exceeding 40% in certain semiconductor categories. The development of 2.5D and 3D packaging solutions has further intensified the need for bonders capable of handling complex multi-die arrangements and fine-pitch interconnections. This technological evolution necessitates continuous innovation in bonding equipment to maintain alignment accuracy within micrometer tolerances and ensure thermal management capabilities.

Proliferation of MEMS and Sensor Applications to Drive Equipment Demand

The widespread integration of micro-electromechanical systems (MEMS) and sensors across consumer electronics, automotive, healthcare, and industrial applications is generating sustained demand for bonding equipment. The global MEMS market has demonstrated remarkable resilience and growth, exceeding $15 billion in 2024 with projected expansion to $25 billion by 2030. Modern smartphones incorporate an average of 12-15 MEMS devices, including accelerometers, gyroscopes, and environmental sensors, each requiring precise bonding during manufacturing. The automotive sector represents another significant growth area, where advanced driver assistance systems (ADAS) utilize numerous sensors for collision avoidance, lane keeping, and autonomous driving functions. Medical applications, particularly in diagnostic equipment and wearable health monitors, have also contributed to increased bonder requirements. This diversification of MEMS applications across multiple industries ensures consistent demand for bonding equipment capable of handling various substrate materials and package configurations while maintaining high throughput and yield rates.

MARKET RESTRAINTS

High Capital Investment Requirements to Constrain Market Penetration

The bonder market faces significant constraints due to the substantial capital investment required for advanced bonding equipment. High-end bonders, particularly those designed for advanced packaging applications, represent major capital expenditures for semiconductor manufacturers, with prices ranging from $500,000 to over $2 million per unit depending on configuration and capabilities. This financial barrier particularly affects small and medium-sized enterprises and emerging market participants who may lack the capital resources for such investments. The total cost of ownership extends beyond initial purchase prices to include maintenance contracts, spare parts, and operator training, which can add 15-20% annually to the equipment cost. Additionally, the rapid pace of technological obsolescence in semiconductor manufacturing creates pressure for frequent equipment upgrades, further amplifying financial challenges for market participants. These economic factors collectively create substantial barriers to entry and expansion within certain market segments.

Technical Complexity and Precision Requirements to Limit Market Accessibility

The development and operation of high-precision bonding equipment involve exceptional technical challenges that restrain market growth. Modern bonders must achieve placement accuracies within 1-2 micrometers while maintaining high throughput rates, requiring sophisticated vision systems, motion control mechanisms, and thermal management solutions. The complexity of these systems creates significant barriers for new market entrants, as developing competitive bonding technology requires extensive expertise in precision mechanics, optics, software control, and materials science. Furthermore, the increasing diversity of packaging formats and materials necessitates flexible bonding platforms capable of handling various process requirements, adding another layer of technical complexity. The industry’s transition toward smaller package sizes and finer pitch interconnections continues to push the boundaries of bonding technology, requiring continuous research and development investments that many companies struggle to sustain. These technical challenges collectively limit the number of viable market participants and constrain the pace of market expansion.

Global Supply Chain Vulnerabilities to Impact Market Stability

The bonder market remains susceptible to supply chain disruptions that affect both equipment manufacturing and semiconductor production. The sophisticated components required for bonding equipment, including high-precision linear motors, vision systems, and specialized bonding tools, often originate from limited sources, creating vulnerability to geopolitical tensions, trade restrictions, and logistical challenges. Recent global events have demonstrated how supply chain interruptions can delay equipment deliveries by six to nine months, directly impacting semiconductor manufacturers’ capacity expansion plans. Additionally, the semiconductor industry’s cyclical nature creates periods of oversupply and undersupply that affect capital equipment investments. During market downturns, semiconductor manufacturers typically defer or cancel equipment orders, creating revenue volatility for bonder suppliers. These supply chain and market cycle challenges create uncertainty in production planning and investment decisions, ultimately restraining consistent market growth.

MARKET CHALLENGES

Shortage of Skilled Technical Personnel to Challenge Operational Efficiency

The bonder market faces significant challenges due to an increasing shortage of qualified technical personnel capable of operating, maintaining, and optimizing advanced bonding equipment. The semiconductor industry’s rapid growth has created demand for skilled engineers and technicians that exceeds available supply, particularly in emerging manufacturing regions. This talent gap affects multiple aspects of the market, from equipment development and manufacturing to field service and customer support. The complexity of modern bonding systems requires comprehensive training programs that typically span six to twelve months, creating delays in workforce development. Furthermore, experienced personnel often command premium compensation packages, increasing operational costs for both equipment manufacturers and end-users. The aging workforce in established semiconductor manufacturing regions compounds this challenge, as retirements outpace new talent acquisition. These human resource constraints directly impact equipment utilization rates, maintenance responsiveness, and ultimately, production yields for semiconductor manufacturers.

Other Challenges

Rapid Technological Obsolescence

The accelerated pace of semiconductor technology advancement creates continuous pressure for bonder manufacturers to develop new capabilities and features. Equipment that represented the industry standard three years ago may already be approaching obsolescence due to changing package requirements and process specifications. This rapid technological turnover challenges manufacturers to maintain adequate research and development investments while managing product lifecycle considerations. Customers increasingly demand future-proof equipment designs that can be upgraded rather than replaced, adding complexity to product development strategies.

Process Integration Complexities

Integrating bonding equipment into existing semiconductor manufacturing lines presents numerous technical challenges. Compatibility with upstream and downstream processes, factory automation systems, and data management platforms requires extensive customization and validation efforts. Each semiconductor manufacturer has unique facility layouts, material handling systems, and quality requirements, necessitating significant engineering resources for successful implementation. These integration challenges can prolong installation timelines and increase total project costs, creating barriers to new equipment adoption.

MARKET OPPORTUNITIES

Emerging Applications in Advanced Electronics to Create New Growth Avenues

The continuous development of emerging electronic applications presents substantial growth opportunities for the bonder market. Flexible electronics, wearable devices, augmented reality/virtual reality systems, and quantum computing applications are creating demand for specialized bonding solutions beyond traditional semiconductor packaging. The wearable technology market alone is projected to exceed $100 billion by 2030, requiring bonding equipment capable of handling flexible substrates and unconventional package geometries. Quantum computing development, though still in early stages, represents another promising frontier where specialized bonding techniques will be essential for qubit packaging and interconnects. These emerging applications often require bonding processes that operate at lower temperatures, accommodate sensitive materials, and achieve even higher precision than conventional semiconductor packaging. Companies that develop bonding solutions tailored to these specific requirements stand to capture significant market share as these technologies mature and achieve commercial scale.

Automation and Industry 4.0 Integration to Enhance Market Potential

The integration of advanced automation and Industry 4.0 technologies into bonding equipment creates substantial opportunities for market expansion. Semiconductor manufacturers increasingly seek fully automated production lines with minimal human intervention, driving demand for bonders with enhanced robotics, material handling capabilities, and data connectivity. The implementation of predictive maintenance systems using artificial intelligence and machine learning can reduce equipment downtime by up to 30% and improve overall equipment effectiveness. Furthermore, the collection and analysis of process data enable continuous optimization of bonding parameters, leading to improved yields and reduced material consumption. The transition toward smart factories also creates opportunities for remote equipment monitoring and support services, allowing bonder manufacturers to develop new revenue streams through service contracts and performance-based pricing models. These technological enhancements not only improve operational efficiency but also create competitive differentiation in an increasingly crowded market.

Geographical Market Expansion to Provide Significant Growth Potential

The ongoing geographical diversification of semiconductor manufacturing presents considerable opportunities for bonder market expansion. While the Asia-Pacific region continues to dominate semiconductor production, accounting for approximately 60% of global capacity, numerous countries are implementing strategies to develop domestic semiconductor capabilities for supply chain security reasons. These initiatives, supported by government incentives and private investments, are creating new demand for bonding equipment in regions that previously had limited semiconductor manufacturing presence. The establishment of new fabrication facilities typically involves comprehensive equipment procurement cycles that include multiple bonding systems for various packaging applications. Additionally, the growing outsourcing of semiconductor assembly and test operations to specialized providers creates sustained demand for bonding equipment as these companies expand their capacity to serve multiple customers. This geographical expansion, combined with the continuous technology migration toward more advanced packaging nodes, ensures long-term growth opportunities for bonder manufacturers with global reach and local support capabilities.

BONDER MARKET TRENDS

Advancements in Semiconductor Packaging Technologies to Emerge as a Trend in the Market

The global semiconductor packaging landscape is undergoing a profound transformation, driven by the relentless demand for smaller, faster, and more powerful electronic devices. This evolution is directly fueling the bonder market, as these precision machines are fundamental to advanced packaging techniques. The proliferation of heterogeneous integration and 3D packaging necessitates bonders capable of handling ultra-fine pitch interconnects and complex multi-die stacks. Furthermore, the rise of wafer-level packaging (WLP), which processes the entire wafer before dicing, requires bonders with exceptional accuracy and throughput to manage the increased density of interconnects. This trend is particularly critical for applications in high-performance computing, artificial intelligence accelerators, and 5G infrastructure, where thermal management and signal integrity are paramount. The market is responding with bonders that integrate advanced vision systems, real-time process control, and AI-driven algorithms to optimize bonding parameters, thereby significantly enhancing yield rates and reducing production costs.

Other Trends

Automation and Smart Manufacturing Integration

The integration of bonders into fully automated and intelligent production lines is a dominant trend reshaping the market. While standalone bonders remain crucial, there is a significant shift towards fully integrated systems that offer seamless material handling, pre- and post-processing, and in-line inspection. This drive towards Industry 4.0 is compelling manufacturers to equip bonders with sophisticated IoT sensors and data analytics capabilities. These smart bonders can predict maintenance needs, autonomously adjust to material variations, and communicate with other machinery to optimize the entire assembly flow. This level of automation is no longer a luxury but a necessity to meet the escalating production volumes and stringent quality requirements of modern semiconductor fabs and OSAT facilities, ensuring consistent output and minimizing human error.

Expansion into Emerging Application Fields

Beyond traditional integrated circuits, the bonder market is experiencing robust growth from its expansion into several high-potential emerging application fields. The rapid adoption of MEMS and sensors across consumer electronics, automotive (for ADAS and infotainment systems), and medical devices has created a substantial and sustained demand for specialized bonding solutions. Similarly, the markets for flexible electronics and wearable devices present unique challenges, requiring bonders that can handle delicate, non-rigid substrates and employ low-temperature bonding processes to avoid damaging sensitive components. The development of AR/VR technologies also relies on precise bonding for micro-displays and sensors. This diversification of application areas provides new growth vectors for the market, pushing manufacturers to develop more versatile and application-specific bonding platforms to capture these opportunities.

COMPETITIVE LANDSCAPE

Key Industry Players

Companies Strive to Strengthen their Product Portfolio to Sustain Competition

The global bonder market exhibits a semi-consolidated competitive structure, characterized by a mix of established multinational corporations, specialized mid-sized firms, and innovative smaller players. This dynamic is driven by the high technical barriers to entry and the capital-intensive nature of manufacturing advanced semiconductor assembly equipment. Market leadership is primarily determined by technological innovation, product reliability, and the ability to offer comprehensive after-sales support across key semiconductor manufacturing hubs.

ASMPT Ltd and Kulicke & Soffa are recognized as dominant forces, collectively holding a significant portion of the global market share. Their leadership is underpinned by extensive R&D investments, which amounted to over $150 million annually for K&S in recent fiscal years, and a robust global service network that ensures minimal downtime for high-volume manufacturing clients. These companies have consistently pioneered advancements in high-speed bonding and vision system accuracy, making them preferred suppliers for major integrated device manufacturers (IDMs) and outsourced semiconductor assembly and test (OSAT) providers.

Meanwhile, Besi has carved out a strong position, particularly in the European and Asian markets, through its focus on advanced packaging solutions like thermocompression bonding. The company’s strategic acquisitions, such as its purchase of certain Siemens AG business units, have expanded its technological capabilities and customer base. Similarly, Shibaura (formerly Toshiba Machine Co.) and Shinkawa Ltd. maintain formidable presence in the Asian market, leveraging their deep relationships with local semiconductor giants and expertise in precision engineering.

The competitive intensity is further heightened by companies like Palomar Technologies and Hanmi Semiconductor, which are aggressively expanding their market presence through specialized offerings. Palomar’s focus on high-accuracy, high-throughput solutions for photonics and microelectronics packaging allows it to compete effectively in niche segments. Hanmi, on the other hand, has gained traction by providing cost-competitive alternatives without compromising on core performance metrics, particularly appealing to emerging OSATs and smaller IDMs.

Looking forward, the competitive landscape is expected to evolve as companies accelerate investments in automation, artificial intelligence integration, and sustainable manufacturing processes. Partnerships with semiconductor manufacturers for co-development of next-generation bonding solutions are becoming a key differentiator, as the industry moves towards more complex heterogeneous integration and 3D packaging architectures.

List of Key Companies Profiled

- ASMPT Ltd (Singapore)

- Kulicke & Soffa (Singapore)

- Besi (Netherlands)

- Shibaura (Japan)

- Shinkawa Ltd. (Japan)

- Fasford Technology (China)

- SUSS MicroTec (Germany)

- Hanmi Semiconductor (South Korea)

- Palomar Technologies (United States)

- Panasonic (Japan)

- Toray Engineering (Japan)

- Ultrasonic Engineering (Japan)

- Hesse GmbH (Germany)

- SET (France)

- F&K Delvotec (Germany)

- WestBond, Inc. (United States)

- Hybond (China)

- DIAS Automation (Germany)

Segment Analysis:

By Type

Wire Bonder Segment Commands Significant Market Share Due to its Pervasive Use in Traditional Semiconductor Packaging

The market is segmented based on type into:

- Wire Bonder

- Subtypes: Ball Bonder and Wedge Bonder

- Die Bonder

- FC Bonder (Flip Chip Bonder)

By Application

Integrated Device Manufacturer (IDMs) Segment is a Major Consumer Due to In-House Packaging Requirements

The market is segmented based on application into:

- Integrated device manufacturer (IDMs)

- Outsourced semiconductor assembly and test (OSATs)

By Bonding Technology

Thermocompression Bonding Gains Traction for High-Density and Fine-Pitch Applications

The market is segmented based on bonding technology into:

- Thermosonic Bonding

- Thermocompression Bonding

- Ultrasonic Bonding

- Adhesive Bonding

By End-User Industry

Consumer Electronics Remains the Largest End-User Sector Driven by Proliferation of Smart Devices

The market is segmented based on end-user industry into:

- Consumer Electronics

- Automotive Electronics

- Telecommunications

- Industrial Manufacturing

- Medical Devices

Regional Analysis: Bonder Market

Asia-Pacific

The Asia-Pacific region dominates the global bonder market, accounting for over 65% of global consumption due to its position as the world’s semiconductor manufacturing hub. China, Taiwan, South Korea, and Japan are the primary drivers, with China alone representing approximately 35% of global semiconductor production capacity. Massive investments in domestic semiconductor manufacturing, such as China’s $150 billion semiconductor fund and Taiwan’s continued leadership in advanced foundry services, fuel demand for high-precision bonding equipment. While cost sensitivity maintains demand for conventional wire bonders, there’s rapid adoption of advanced flip chip and die bonding technologies to support cutting-edge applications in 5G, AI processors, and automotive electronics. The region benefits from established supply chains and concentration of OSAT facilities, though geopolitical tensions create some supply chain diversification pressures.

North America

North America’s bonder market is characterized by technological innovation and high-value manufacturing, particularly in the United States. The region’s market is driven by advanced packaging requirements for AI chips, high-performance computing, and defense applications. Recent developments include the CHIPS and Science Act, which allocates $52 billion to bolster domestic semiconductor research and manufacturing, creating significant opportunities for bonder equipment suppliers. The market demands increasingly sophisticated bonding solutions, particularly flip chip bonders for heterogeneous integration and 3D packaging. Major IDMs and fabless companies driving innovation require bonders with sub-micron accuracy and advanced process control. While manufacturing volume is lower than Asia-Pacific, the region’s focus on leading-edge technology creates premium demand for high-end bonding equipment.

Europe

Europe maintains a strong position in the bonder market, particularly in automotive and industrial electronics applications. Germany leads regional demand, supported by its robust automotive semiconductor industry and Industry 4.0 initiatives. The European Chips Act, with €43 billion in proposed investments, aims to double Europe’s semiconductor market share to 20% by 2030, driving demand for bonding equipment. The region shows particular strength in MEMS and sensor applications, with bonding equipment requirements for automotive sensors, medical devices, and industrial IoT. European manufacturers emphasize quality and reliability over cost competitiveness, creating demand for precision bonding equipment with advanced monitoring and control capabilities. Environmental regulations also drive development of energy-efficient bonding technologies with reduced environmental impact.

South America

South America represents an emerging market for bonder equipment, primarily serving consumer electronics and basic industrial applications. Brazil accounts for the majority of regional demand, supported by its developing electronics manufacturing sector. The market remains constrained by economic volatility and limited semiconductor manufacturing infrastructure, resulting in reliance on imported bonded components rather than local production. Most bonding equipment in the region consists of entry-level wire bonders for basic packaging applications. However, recent trade policies encouraging local electronics production and the growing automotive sector present opportunities for market development. The region typically adopts mature bonding technologies due to cost considerations and limited technical expertise in advanced packaging.

Middle East & Africa

The Middle East and Africa region shows nascent development in bonder equipment adoption, primarily focused on consumer electronics assembly and basic industrial applications. Israel demonstrates the most advanced capabilities, particularly in specialized military and aerospace applications requiring high-reliability bonding. The region generally lacks significant semiconductor manufacturing infrastructure, limiting bonder equipment demand to replacement markets and small-scale production facilities. Recent investments in technology diversification, particularly in UAE and Saudi Arabia, could stimulate future demand, though the market remains in early development stages. Most equipment purchases consist of refurbished or entry-level bonding systems, with limited adoption of advanced flip chip or sophisticated die bonding technologies.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Semiconductor and Electronics markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Bonder Market?

-> Bonder Market was valued at 2332 million in 2024 and is projected to reach US$ 3321 million by 2032, at a CAGR of 5.1% during the forecast period..

Which key companies operate in Global Bonder Market?

-> Key players include Besi, ASMPT Ltd, Kulicke & Soffa, Shibaura, Shinkawa Ltd., Fasford Technology, SUSS MicroTec, Hanmi, Palomar Technologies, and Panasonic, among others.

What are the key growth drivers?

-> Key growth drivers include semiconductor industry expansion, advanced packaging technologies, MEMS and sensor proliferation, and miniaturization trends across consumer electronics, automotive, and medical sectors.

Which region dominates the market?

-> Asia-Pacific dominates the global bonder market, accounting for over 65% of global demand, driven by semiconductor manufacturing hubs in China, Taiwan, South Korea, and Japan.

What are the emerging trends?

-> Emerging trends include high-precision multifunctional systems, automation and AI integration, laser bonding technologies, and regionalized production strategies to mitigate supply chain risks.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...