MARKET INSIGHTS

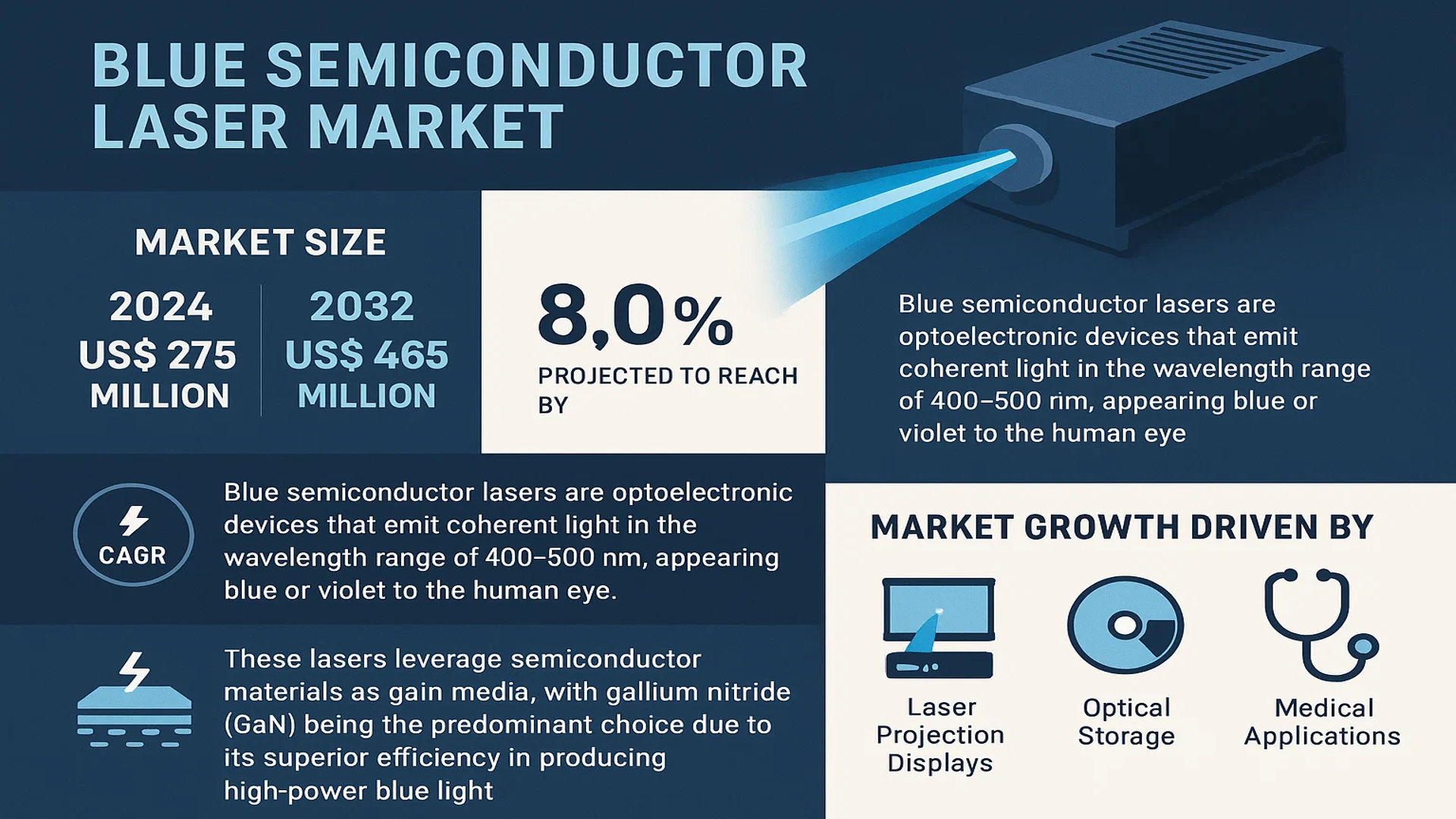

The global Blue Semiconductor Laser market was valued at 275 million in 2024 and is projected to reach US$ 465 million by 2032, at a CAGR of 8.0% during the forecast period..

Blue semiconductor lasers are optoelectronic devices that emit coherent light in the wavelength range of 400-500 nm, appearing blue or violet to the human eye. These lasers leverage semiconductor materials as gain media, with gallium nitride (GaN) being the predominant choice due to its superior efficiency in producing high-power blue light. The technology’s ability to deliver precise, collimated beams makes it indispensable across industries requiring fine material processing and high-resolution applications.

Market growth is driven by increasing adoption in laser projection displays, optical storage, and medical applications. Furthermore, advancements in laser diode technology and rising demand for high-brightness lasers in automotive and aerospace sectors are accelerating expansion. Key players like Nuburu and Shimadzu Corporation continue to innovate, with recent developments focusing on enhancing power output and thermal stability for industrial applications. The Asia-Pacific region dominates demand due to robust electronics manufacturing, while North America leads in R&D investments.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand in High-Precision Industrial Applications to Accelerate Market Growth

The global blue semiconductor laser market is experiencing substantial growth due to increasing adoption in high-precision industrial applications. Blue lasers, operating in the 400-500 nm wavelength range, offer superior beam quality and precision compared to traditional infrared lasers, making them ideal for applications such as metal cutting, welding, and additive manufacturing. The superior beam collimation allows for finer detail in micromachining, which is driving demand in the automotive and aerospace sectors where precision is critical. With industrial automation on the rise, manufacturers are increasingly shifting toward blue laser technology to enhance productivity and reduce material waste. For instance, laser-based metal processing applications have grown by over 15% annually, demonstrating the expanding role of blue lasers in modern manufacturing.

Expansion of Lithium-Ion Battery Production to Fuel Market Expansion

The lithium-ion battery industry is one of the fastest-growing sectors driving blue semiconductor laser adoption. As electric vehicle (EV) production surges globally, manufacturers require high-precision laser systems for battery welding and electrode cutting. Blue lasers, with their superior beam control, enable precise ablation and welding of thin copper and aluminum foils used in battery cells, reducing thermal damage and improving efficiency. The global EV battery market is projected to grow at a CAGR of over 20%, indicating strong potential for blue laser integration. Additionally, rising government investments in renewable energy storage solutions are further propelling demand for advanced laser processing technologies in battery manufacturing.

➤ The superior absorption of blue lasers in copper processing, where traditional infrared lasers struggle, is a key factor behind their adoption in high-throughput battery production lines.

Furthermore, advancements in laser diode technology, such as increased power output and improved thermal management, are enabling blue lasers to replace conventional laser systems across multiple industries. The market is witnessing robust R&D investments aimed at enhancing efficiency and reducing costs, which is expected to accelerate adoption.

MARKET RESTRAINTS

High Initial Costs and Limited Power Output to Restrain Market Penetration

Despite their advantages, blue semiconductor lasers face significant cost-related restraints that hinder widespread adoption. The production of high-quality blue laser diodes requires specialized materials such as gallium nitride (GaN), which remains expensive compared to traditional materials used in infrared lasers. Additionally, achieving high power outputs with blue lasers is still a technological challenge, limiting their use in heavy-duty industrial applications. These factors contribute to a higher total cost of ownership compared to other laser types, discouraging small and medium-sized enterprises from investing in blue laser technology.

Other Restraints

Technical Limitations in Heat Dissipation

Blue semiconductor lasers generate significant heat, requiring advanced cooling solutions that increase system complexity and cost. Thermal management remains a critical challenge, as overheating can degrade performance and reduce laser lifespan. This issue is particularly pronounced in high-power applications where consistent output is essential.

Market Fragmentation and Component Sourcing Issues

The supply chain for blue laser components is still developing, leading to procurement challenges. Limited availability of key semiconductor materials and fluctuating prices impact production scalability, restraining wider market penetration. Manufacturers face difficulties in securing stable supplies of high-quality GaN-based components, which affects overall product reliability.

MARKET CHALLENGES

Integration Difficulties in Existing Manufacturing Systems to Pose Adoption Hurdles

Incorporating blue semiconductor lasers into existing production lines presents several technical challenges. Unlike infrared lasers, which have been industry-standard for decades, blue lasers require specialized optical components and safety measures. Many manufacturing facilities would need significant retrofitting, including upgrades to cooling systems and beam delivery mechanisms, increasing deployment costs. Furthermore, the lack of standardized integration protocols complicates the transition for manufacturers accustomed to conventional laser systems.

Other Challenges

Skilled Workforce Shortage in Advanced Laser Applications

The specialized nature of blue laser systems demands trained operators and maintenance personnel. However, there is a shortage of professionals skilled in high-precision laser processing, particularly in emerging markets. Companies struggle to find qualified technicians capable of handling the unique challenges associated with blue laser operation.

Regulatory Compliance and Safety Concerns

Blue lasers pose higher safety risks due to their visibility and potential for retinal damage. Regulatory bodies impose stringent safety standards, which increase compliance costs for manufacturers. Workplace safety training requirements add another layer of complexity for companies adopting this technology.

MARKET OPPORTUNITIES

Emerging Applications in Consumer Electronics to Unlock New Revenue Streams

The consumer electronics sector represents a high-growth opportunity for blue semiconductor laser technology. Applications such as micro-displays, laser projection systems, and ultra-high-definition (UHD) optical storage devices are driving demand. The miniaturization trend in electronics manufacturing favors blue lasers due to their precise ablation capabilities on delicate materials. With the global smart device market continuing to expand, manufacturers are exploring blue lasers for next-generation displays and wearable technology.

Other Opportunities

Advancements in Medical and Biotech Laser Applications

Blue lasers are gaining traction in medical and biotechnological fields for applications such as photodynamic therapy, DNA sequencing, and surgical procedures. Their ability to produce clean, controlled cuts with minimal thermal damage makes them suitable for sensitive medical applications. The increasing adoption of laser-based diagnostic tools presents lucrative prospects for market expansion in healthcare.

Strategic Partnerships to Drive Innovation

Collaborations between laser manufacturers and end-use industries are accelerating technological advancements. Companies specializing in semiconductor lasers are partnering with automotive, aerospace, and medical device firms to co-develop tailored solutions, fostering innovation and expanding market reach.

BLUE SEMICONDUCTOR LASER MARKET TRENDS

Rising Demand in Industrial Applications to Drive Market Growth

The Blue Semiconductor Laser Market is witnessing significant growth driven by expanding applications in precision manufacturing, particularly in industries such as automotive, aerospace, and battery production. Blue lasers, operating in the 400-500 nm wavelength range, offer superior precision and efficiency compared to traditional laser systems due to their shorter wavelengths and higher energy densities. In battery manufacturing, these lasers are increasingly used for electrode processing and welding, which require high power and fine control. The demand for blue semiconductor lasers in industrial applications is expected to grow at a CAGR of 8.0%, propelled by the need for advanced material processing techniques.

Other Trends

Technological Advancements in Laser Systems

Continuous innovation in semiconductor laser technology is enhancing performance and reliability, making blue semiconductor lasers more viable for industrial and scientific applications. Recent developments include higher power output models (>1000W) that enable deeper penetration and faster processing speeds. Innovations in beam shaping and modulation techniques are further improving the accuracy and versatility of these lasers. The integration of AI-driven control systems for real-time adjustments in manufacturing processes is another key advancement driving adoption, particularly in industries requiring micron-level precision.

Growing Adoption in Medical and Scientific Research

While industrial applications dominate the market, the medical and scientific research sectors are emerging as significant growth areas for blue semiconductor lasers. These lasers are increasingly used in fluorescence microscopy and photodynamic therapy due to their ability to excite fluorophores efficiently. Additionally, research institutions are adopting blue lasers for spectroscopy and quantum optics experiments, leveraging their stability and coherence properties. The expansion of biotechnology and materials science research is expected to bolster demand further, particularly in regions with strong R&D investments such as North America and Europe.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Expand Technological Capabilities to Secure Competitive Edge

The global Blue Semiconductor Laser Market exhibits a dynamic competitive environment with both established players and emerging contenders shaping industry growth. Valued at $275 million in 2024, the market is projected to surge to $465 million by 2032, growing at a CAGR of 8.0%. This expansion fuels strategic investments in R&D and portfolio diversification among key market participants.

Nuburu Inc. has emerged as a market leader, leveraging its proprietary high-power blue laser technology that delivers superior performance in industrial applications like metal processing and additive manufacturing. The company’s 2023 strategic partnership with a major automotive manufacturer to develop laser-based battery welding solutions exemplifies its commitment to application-specific innovation.

Meanwhile, Laserline GmbH and DILAS have strengthened their positions through continuous product enhancements, particularly in the >1000W power segment which currently dominates 62% of market revenue. Both companies have expanded their Asia-Pacific presence to capitalize on the region’s growing demand for precision manufacturing tools.

The competitive landscape is further characterized by technological collaborations, as seen when Shimadzu Corporation partnered with a leading aerospace components manufacturer to develop specialized blue laser systems for composite material processing. Such alliances are becoming increasingly crucial as industrial applications demand more customized solutions.

List of Key Blue Semiconductor Laser Companies Profiled

- Nuburu Inc. (U.S.)

- DILAS (Germany)

- Shimadzu Corporation (Japan)

- Laserline GmbH (Germany)

- Shenzhen United Winners Laser (China)

- Wuhan Raycus Fiber Laser Technologies (China)

- BWT Group (China)

- Changchun New Industries Optoelectronics Tech (China)

Segment Analysis:

By Type

High-Power Segment (≥1000W) Leads the Market Due to Industrial and Scientific Applications

The market is segmented based on power output into:

- High-power lasers (≥1000W)

- Subtypes: Industrial cutting, welding, and material processing

- Low-power lasers (<1000W)

- Subtypes: Medical, research, and consumer electronics applications

By Application

Automotive Segment Dominates Market Share Due to Adoption in Precision Manufacturing

The market is segmented based on application into:

- Automotive

- Battery manufacturing

- Aerospace and defense

- Medical devices

- Scientific research

- Others

By Wavelength

405-450 nm Range Accounts for Significant Demand in Optical Storage

The market is segmented based on wavelength into:

- 400-405 nm

- 405-450 nm

- 450-500 nm

By End-Use Industry

Manufacturing Sector Exhibits Highest Adoption Due to Material Processing Needs

The market is segmented based on end-use industry into:

- Industrial manufacturing

- Healthcare

- Research and development

- Consumer electronics

- Others

Regional Analysis: Blue Semiconductor Laser Market

Asia-Pacific

The Asia-Pacific region dominates the global blue semiconductor laser market, accounting for over 40% of the total market share in 2024. This leadership position stems from China’s aggressive manufacturing expansion and Japan’s technological prowess in photonics. China’s ‘Made in China 2025’ initiative actively promotes domestic production of high-power blue lasers, particularly for applications in electric vehicle battery welding and consumer electronics manufacturing. Japan maintains technological leadership through companies like Shimadzu Corporation, which pioneered high-efficiency blue laser diodes. The region benefits from strong government support, a skilled workforce, and massive demand from electronics and automotive sectors. While cost competition remains intense, the adoption of blue laser technology in precision manufacturing applications continues to accelerate across Southeast Asian countries as well.

North America

North America represents the second-largest market for blue semiconductor lasers, driven by advanced R&D initiatives and substantial defense/aerospace applications. The U.S. Department of Defense has increased investments in directed energy weapons utilizing blue laser technology, creating specialized demand. Commercial applications are expanding rapidly in medical devices (particularly dermatology and dentistry) and additive manufacturing. Strict FDA regulations regarding laser safety and efficacy standards have shaped product development roadmaps, leading to high-value customized solutions. The presence of market leaders like Nuburu and a robust venture capital ecosystem supporting photonics startups further strengthens the region’s position. Canadian research institutions are making significant contributions to improving blue laser efficiency and power output through novel semiconductor materials research.

Europe

Europe maintains a technologically advanced but niche position in the blue laser market, with Germany and the UK leading industrial applications. The region excels in high-precision manufacturing applications, particularly in the automotive sector where blue lasers are increasingly used for welding dissimilar metals in electric vehicle battery packs. EU-funded photonics initiatives such as Horizon Europe program support the development of next-generation blue laser technologies. Environmental regulations favor energy-efficient laser systems, creating opportunities for blue lasers which typically offer better electrical-to-optical conversion efficiency compared to traditional alternatives. However, the market faces challenges from relatively higher production costs and competition from Asian suppliers. Recent breakthroughs in blue laser diode reliability by European research consortia may help regain competitiveness in specialized applications.

Middle East & Africa

The Middle East & Africa region represents an emerging market with focused growth in oil & gas and medical applications. Gulf Cooperation Council countries are investing in laser-based oil exploration technologies, where blue lasers show promise for improved spectroscopic analysis. South Africa has developed niche capabilities in laser-based mining applications. However, the overall market remains constrained by limited local manufacturing capabilities and reliance on imports. Recent partnerships between regional universities and global laser manufacturers aim to build local expertise. The healthcare sector shows particularly strong potential, with blue laser systems gaining traction in specialized dermatological treatments and cosmetic procedures across affluent Middle Eastern markets.

South America

South America’s blue semiconductor laser market remains in early development stages, with Brazil and Argentina showing the most significant activity. The region primarily imports blue laser systems for research institutions and specialized industrial applications. Brazil’s growing aerospace sector has created some demand for laser-based manufacturing systems, while Argentina has seen increased adoption in the medical sector. Economic volatility and limited local technical expertise present challenges to widespread adoption. However, several multinational laser manufacturers have established local service centers to support the mining and agriculture equipment sectors, which may drive future growth in ruggedized blue laser applications.

Report Scope

This market research report provides a comprehensive analysis of the Global Blue Semiconductor Laser market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, power output (≤1000W and >1000W), application (Automobile, Battery, Aerospace, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis for key markets.

- Competitive Landscape: Profiles of leading market participants, including their product portfolios, R&D investments, manufacturing capabilities, and strategic initiatives.

- Technology Trends & Innovation: Analysis of emerging blue laser technologies, material advancements, and integration with Industry 4.0 applications.

- Market Drivers & Restraints: Evaluation of growth factors including industrial automation demand and challenges like high manufacturing costs.

- Stakeholder Analysis: Strategic insights for laser manufacturers, system integrators, component suppliers, and investors.

The research methodology combines primary interviews with industry experts and analysis of verified secondary data sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Blue Semiconductor Laser Market?

-> Blue Semiconductor Laser market was valued at 275 million in 2024 and is projected to reach US$ 465 million by 2032, at a CAGR of 8.0% during the forecast period.

Which key companies operate in Global Blue Semiconductor Laser Market?

-> Major players include Nuburu, DILAS, Shimadzu Corporation, Laserline, Shenzhen United Winners Laser, Wuhan Raycus Fiber Laser Technologies, BWT, and Changchun New Industries Optoelectronics Tech.

What are the key growth drivers?

-> Growth is driven by increasing adoption in automotive manufacturing, battery welding applications, and aerospace component fabrication.

Which region dominates the market?

-> Asia-Pacific holds the largest market share, with China being the dominant country due to its manufacturing capabilities.

What are the emerging trends?

-> Emerging trends include higher power blue laser development, integration with automated production systems, and applications in electric vehicle battery manufacturing.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...