BiCMOS variable gain amplifier for 100G coherent transceivers Market Insights

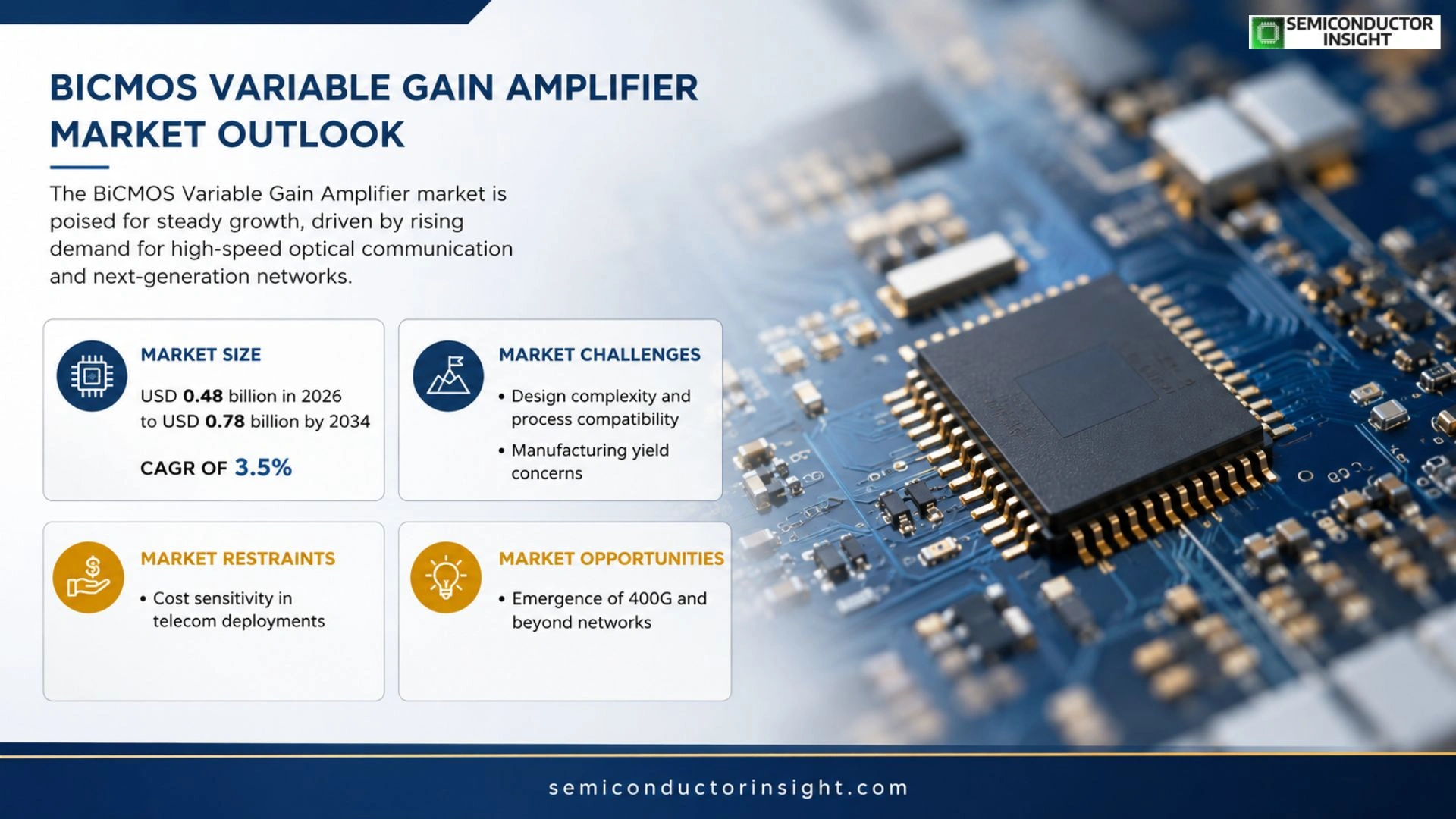

Global BiCMOS variable gain amplifier market size was valued at USD 0.45 billion in 2025. The market is projected to grow from USD 0.48 billion in 2026 to USD 0.78 billion by 2034, exhibiting a CAGR of 3.5% during the forecast period.

BiCMOS variable gain amplifiers merge bipolar and CMOS processes to deliver high linearity, low noise figure, and wide dynamic range required for optical‑electrical conversion in 100 Gb/s coherent transceivers. Their programmable gain capability compensates link loss and supports adaptive equalization across diverse fiber conditions.

The market is experiencing rapid growth because data‑center interconnects and metro‑network upgrades are driving demand for higher‑speed optical modules. Furthermore, next‑generation mobile backhaul rollouts and silicon‑photonic integration initiatives are accelerating adoption of BiCMOS VGAs.

MARKET DRIVERS

Rising Demand for High‑Capacity Data Center Interconnects

BiCMOS variable gain amplifier for 100G coherent transceivers Market is being propelled by the exponential growth of data traffic in hyperscale data centers. Operators require amplifiers that can sustain high linearity while supporting dynamic gain control, enabling efficient scaling to 100 Gbps per wavelength. This demand translates into higher adoption rates for BiCMOS‑based solutions that balance performance and power efficiency.

Advancements in SiGe‑BiCMOS Integration

Recent breakthroughs in SiGe heterojunction bipolar transistor (HBT) integration have reduced parasitics, allowing variable gain amplifiers to achieve broader bandwidths with lower noise figures. The seamless co‑integration of analog and digital blocks on a single BiCMOS platform shortens design cycles and lowers total cost of ownership, further accelerating market uptake.

➤ The integration of BiCMOS technology enables lower power consumption while sustaining linearity, a critical advantage for 100 Gbps coherent links.

Overall, the convergence of traffic growth, technology maturation, and cost pressures creates a compelling value proposition that drives BiCMOS variable gain amplifier for 100G coherent transceivers Market forward.

MARKET CHALLENGES

Design Complexity and Process Compatibility

Designing variable gain amplifiers that meet stringent phase‑noise and linearity specifications while remaining compatible with existing silicon photonics processes presents a significant engineering hurdle. Engineers must balance high gain bandwidth product against thermal stability, often requiring extensive simulation and validation cycles.

Other Challenges

Manufacturing Yield Concerns

Yield variability in mixed‑signal BiCMOS fabs can increase unit costs, especially when advanced node sizes are employed. Achieving consistent performance across large volumes demands robust process control and thorough testing protocols.

MARKET RESTRAINTS

Cost Sensitivity in Telecom Deployments

Telecom operators operate under tight capex constraints, and the premium pricing of BiCMOS‑based variable gain amplifiers can limit adoption in cost‑sensitive segments. While performance benefits are clear, the higher upfront investment may deter early deployment until economies of scale are achieved.

MARKET OPPORTUNITIES

Emergence of 400G and Beyond Networks

The migration toward 400 Gbps and higher optical channels creates a natural extension path for 100 Gbps coherent transceiver components. BiCMOS variable gain amplifiers can be re‑engineered to support multi‑lane aggregation, offering scalable solutions that align with the next wave of high‑capacity network rollouts.

BiCMOS variable gain amplifier for 100G coherent transceivers Market Trends

Growing Adoption in Data‑Center Interconnects

BiCMOS variable gain amplifier for 100G coherent transceivers Market is being propelled by a surge in data‑center traffic that demands higher‑speed optical links. The ability of BiCMOS VGAs to deliver high linearity, low noise figure, and wide dynamic range makes them well suited for optical‑electrical conversion at 100 Gb/s. Programmable gain control compensates for link loss and supports adaptive equalization, which aligns with the performance requirements of modern hyperscale facilities. As metro‑network upgrades continue, operators are favoring components that can be re‑configured without hardware replacement, reinforcing the market’s expansion.

Other Trends

Integration with Silicon‑Photonic Platforms

Silicon‑photonic integration initiatives are encouraging the embedding of BiCMOS VGAs directly onto photonic chips. This approach reduces package count, improves thermal management, and shortens the electrical‑to‑optical conversion path. Early deployments in next‑generation mobile backhaul demonstrate a measurable improvement in link stability under varying fiber conditions, confirming the strategic advantage of tightly coupled BiCMOS and silicon photonics solutions.

Competitive Landscape and Innovation

Key industry players such as Broadcom Inc., Analog Devices Inc., and Texas Instruments are broadening their portfolios through strategic partnerships and advanced process node investments. These companies are focusing on lowering power consumption while preserving the high‑gain characteristics essential for 100 Gb/s coherent transceivers. Recent product roadmaps indicate a trend toward multi‑band VGAs that can serve both C‑band and L‑band wavelengths, offering operators greater flexibility in network design. Continuous innovation in mixed‑mode device architectures is expected to sustain the market’s momentum over the next several years.

COMPETITIVE LANDSCAPE

Key Industry Players

BiCMOS VGA Market Overview for 100G Coherent Transceivers

BiCMOS variable gain amplifier (VGA) segment for 100 Gb/s coherent transceivers is currently dominated by a handful of vertically integrated semiconductor leaders that combine deep‑submicron CMOS with bipolar BJT processes. Broadcom Inc. leads the market with its high‑volume silicon‑photonic fabs and a mature portfolio of VGA IP that is tightly coupled to its 100G PHY families. Analog Devices Inc. and Texas Instruments follow closely, leveraging their mixed‑signal expertise to offer programmable‑gain blocks that meet the stringent linearity and noise specifications demanded by data‑center interconnects. These incumbents benefit from extensive design‑win pipelines, strategic OEM alliances, and aggressive roadmap commitments that reinforce a concentrated yet highly innovative market structure.

Beyond the core trio, a broader ecosystem of niche players is expanding the competitive landscape. NXP Semiconductors and Infineon Technologies are pushing BiCMOS VGA solutions that target automotive and industrial backhaul, while Skyworks Solutions and Qorvo have entered the space by adapting their RF power‑amplifier know‑how to optical‑electrical conversion. Smaller specialists such as Renesas Electronics, STMicroelectronics, Mitsubishi Electric, and ON Semiconductor contribute differentiated process nodes or customized ASIC services for emerging silicon‑photonic integration platforms. Additionally, emerging foundries like Skywater Technology provide accessible multi‑project wafer runs that enable boutique designers to prototype low‑noise VGAs, further diversifying supply options for system integrators.

List of Key BiCMOS Variable Gain Amplifier Companies Profiled

- Broadcom Inc.

- Analog Devices Inc.

- Texas Instruments Inc.

- NXP Semiconductors

- Infineon Technologies AG

- Skyworks Solutions

- Qorvo, Inc.

- Renesas Electronics Corp.

- STMicroelectronics

- Mitsubishi Electric Corporation

- ON Semiconductor

- Skywater Technology Foundry

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Linear BiCMOS VGA

|

| By Application |

|

Data‑Center Interconnect

|

| By End User |

|

Network Equipment Manufacturers

|

| By Architecture |

|

Hybrid Si‑Photonic + BiCMOS

|

| By Integration Level |

|

Embedded in Transceiver ASICs

|

Regional Analysis: BiCMOS variable gain amplifier for 100G coherent transceivers Market

The United States houses the majority of fab facilities capable of producing the high‑precision BiCMOS processes required for 100G coherent transceivers. Collaborative programs between universities and industry accelerate device scaling, enabling higher gain linearity without compromising power efficiency.

North American manufacturers have diversified their component sourcing, mitigating risks associated with geopolitical tensions. Strategic stockpiling of key substrates and proactive vendor qualification ensure steady component flow for amplifier production.

Favorable spectrum allocation policies and supportive standards bodies streamline the certification process for high‑speed coherent modules, reducing time‑to‑market for new BiCMOS‑based solutions.

Large carriers prioritize network scalability and energy savings, prompting early adoption of variable gain amplifiers that can dynamically adjust performance based on traffic patterns, fostering a wave of upgrades across backbone infrastructures.

Europe

European telecom operators are focusing on extending the reach of 100G coherent services across metropolitan and regional networks. The presence of several key optical component manufacturers in Germany and the Nordic region fuels a collaborative environment for BiCMOS amplifier integration. Sustainability mandates encourage designs that minimize power consumption, aligning well with the variable gain architecture. Although the market is competitive, Europe’s strong standards framework and access to EU research funding support incremental innovation and gradual market penetration.

Asia‑Pacific

The Asia‑Pacific region exhibits rapid growth driven by massive data‑center deployments in China, Japan, and South Korea. Local semiconductor firms are scaling BiCMOS production capabilities to meet soaring demand for high‑capacity transceivers. While cost sensitivity remains a factor, the region’s aggressive network expansion plans create an environment conducive to early adoption, especially in submarine and metro fiber networks. Collaborative R&D initiatives between universities and manufacturers promise continuous performance enhancements.

South America

South America’s market is characterized by gradual modernization of legacy fiber infrastructure. Leading operators in Brazil and Chile are evaluating BiCMOS variable gain amplifiers as part of upgrade pathways to support increasing broadband traffic. Government incentives aimed at expanding fiber‑to‑the‑home (FTTH) projects provide a catalyst for adoption, though capital constraints slow widespread rollout. Local design houses are beginning to partner with global foundries to source the required BiCMOS technology.

Middle East & Africa

In the Middle East & Africa, high‑density data‑center projects in the Gulf Cooperation Council (GCC) states are driving interest in advanced coherent transceiver solutions. The variable gain amplifier’s ability to balance performance and power efficiency matches the region’s focus on sustainable infrastructure. African markets remain nascent, with pilot deployments in South Africa and Kenya signaling early-stage exploration. Partnerships with international manufacturers are essential to bridge technology gaps and enable future growth.

Report Scope

This market research report provides a comprehensive analysis of the BiCMOS variable gain amplifier for 100G coherent transceivers Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of BiCMOS variable gain amplifier for 100G coherent transceivers Market?

-> BiCMOS variable gain amplifier market size is projected to grow from USD 0.48 billion in 2026 to USD 0.78 billion by 2034.

Which key companies operate in BiCMOS variable gain amplifier for 100G coherent transceivers Market?

-> Key players include Broadcom Inc., Analog Devices Inc., Texas Instruments, among others.

What are the key growth drivers?

-> Key growth drivers include data‑center interconnects, metro‑network upgrades, next‑generation mobile backhaul rollouts, and silicon‑photonic integration initiatives.

Which region dominates the market?

-> Information on regional dominance is not specified in the referenced source.

What are the emerging trends?

-> Emerging trends include adoption of BiCMOS VGAs for higher‑speed optical modules, integration with silicon‑photonic platforms, and adaptive equalization techniques.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...