MARKET INSIGHTS

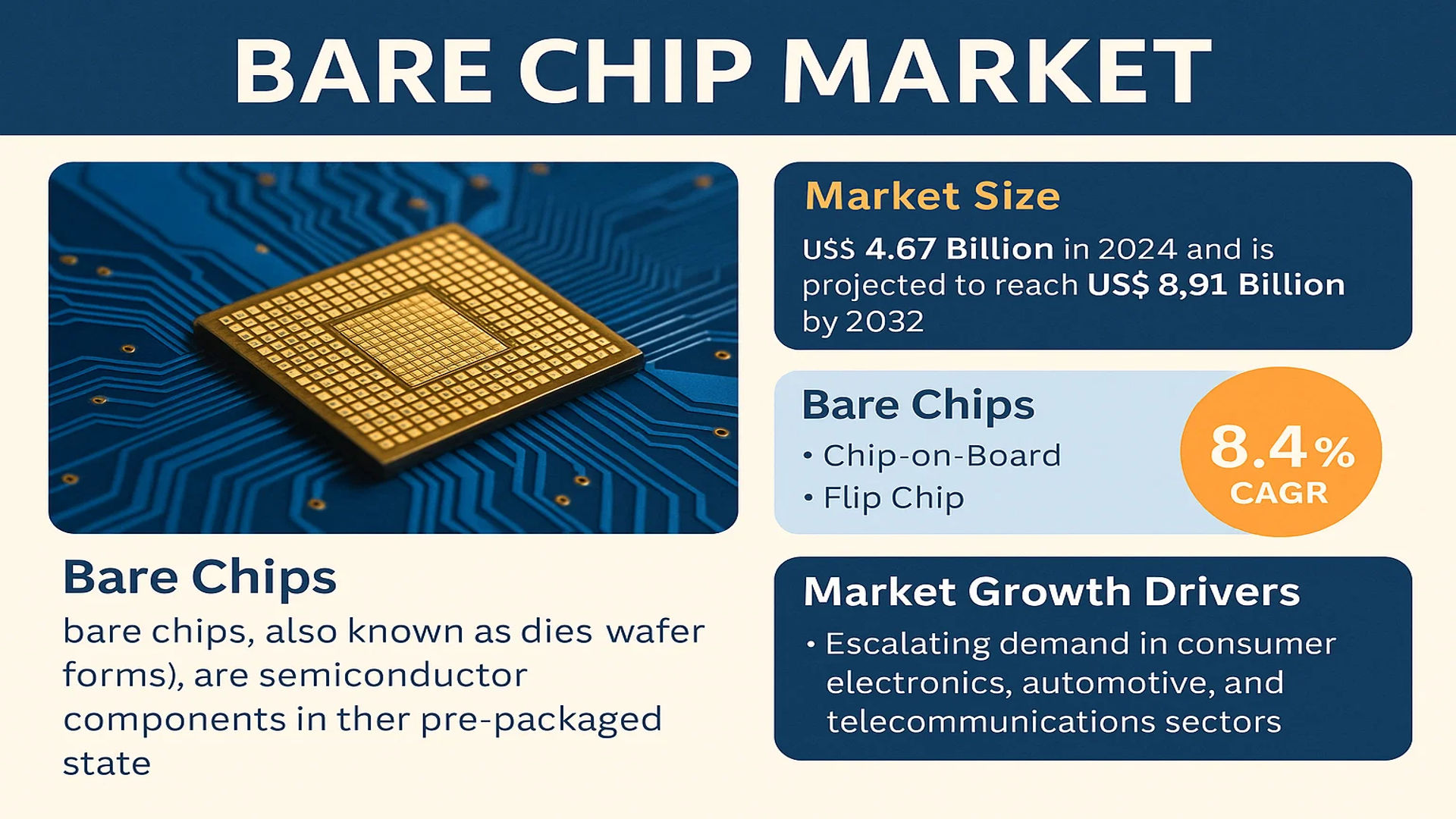

The global Bare Chip market size was valued at US$ 4.67 billion in 2024 and is projected to reach US$ 8.91 billion by 2032, at a CAGR of 8.4% during the forecast period 2025-2032.

Bare chips (also known as dies or wafer forms) are semiconductor components in their pre-packaged state, serving as foundational elements for integrated circuits and hybrid circuits. These chips exist either as individual dies or as part of wafer forms before undergoing packaging processes that transform them into functional semiconductor devices. Key types include COB (Chip-on-Board) and Flip Chip technologies, which enable diverse applications across industries.

The market growth is driven by escalating demand in consumer electronics, automotive, and telecommunications sectors, alongside advancements in semiconductor manufacturing. In 2022, global semiconductor sales reached USD 574 billion, with bare chips playing a pivotal role. While traditional PC/communications markets dominate, automotive and industrial applications are witnessing accelerated adoption. Major players like Texas Instruments, Infineon Technologies, and Micron Technology are expanding their bare chip portfolios to capitalize on emerging opportunities in AI and IoT-driven markets.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of 5G and IoT Technologies Accelerating Bare Chip Demand

The global proliferation of 5G networks and Internet of Things (IoT) devices is creating unprecedented demand for semiconductor components. Bare chips, as foundational elements in semiconductor manufacturing, are experiencing heightened adoption across telecommunications infrastructure and smart device ecosystems. With over 1.7 billion 5G subscriptions projected globally this year, the need for high-performance bare chips in RF front-end modules and base station components has surged. The miniaturization trend in electronics further emphasizes the importance of advanced packaging technologies using bare dies, particularly in space-constrained 5G devices and IoT sensors.

Automotive Semiconductor Boom Driving Flip Chip Adoption

The automotive industry’s rapid digital transformation is significantly impacting the bare chip market. Modern vehicles incorporate hundreds of semiconductor devices, with electric vehicles requiring approximately 2.5 times more chips than conventional vehicles. Advanced driver-assistance systems (ADAS), in-vehicle networking, and electrification components increasingly rely on flip-chip technology for superior thermal performance and interconnect density. The automotive semiconductor market, representing about 12% of the total semiconductor demand, continues to grow at double-digit rates, creating sustained demand for automotive-grade bare chips with enhanced reliability standards.

Artificial Intelligence Hardware Requirements Fueling Specialty Chip Needs

Artificial intelligence applications are driving innovative bare chip architectures optimized for machine learning workloads. AI accelerators increasingly utilize specialized bare dies with high-bandwidth memory (HBM) interconnects and advanced packaging solutions. The AI chip market is projected to maintain over 30% annual growth through the decade, with cloud service providers and hyperscalers investing heavily in custom silicon solutions. This trend favors bare chip manufacturers capable of producing high-performance computing dies with tight thermal and power efficiency specifications for data center and edge AI deployments.

MARKET RESTRAINTS

Semiconductor Manufacturing Complexity Constraining Capacity Expansion

The sophisticated nature of semiconductor fabrication presents significant barriers to bare chip production scaling. Current state-of-the-art facilities require investments exceeding $10 billion for leading-edge nodes, with yield optimization in bare die production presenting unique challenges. The transition to sub-7nm processes has increased manufacturing complexity, requiring precise control over hundreds of process steps. These technical hurdles, combined with lengthy qualification cycles for advanced packages, limit the industry’s ability to rapidly respond to demand fluctuations and often create supply-demand imbalances.

Geopolitical Tensions Disrupting Supply Chain Stability

Recent geopolitical developments have introduced significant uncertainty in semiconductor supply chains, particularly affecting bare chip availability. Export controls on advanced manufacturing equipment and regional trade restrictions have compelled manufacturers to reevaluate production footprints and supplier relationships. The concentration of certain specialty materials and equipment suppliers in specific geographic regions creates vulnerability to supply shocks, with bare chips being particularly sensitive due to their position early in the semiconductor value chain. These factors contribute to longer lead times and pricing volatility across the industry.

Standardization Challenges Hindering Ecosystem Development

The lack of universal standards for bare chip interfaces and testing methodologies creates interoperability issues throughout the semiconductor ecosystem. Diverse customer specifications and proprietary packaging requirements result in fragmented production processes, reducing manufacturing efficiency. While some progress has been made in standardizing chiplet interfaces, the broader standardization of bare die characteristics and quality metrics remains an ongoing challenge. These standardization gaps increase development costs and time-to-market for new bare chip products while complicating multi-sourcing strategies for OEMs.

MARKET OPPORTUNITIES

Chiplet Architecture Revolution Creating New Market Segments

The emergence of chiplet-based designs represents a transformative opportunity for bare chip manufacturers. This architectural approach allows semiconductor companies to combine specialized bare dies from multiple sources into advanced SoC solutions, potentially reducing development costs while improving performance. The market for chiplet-based products is forecast to expand significantly, particularly in high-performance computing applications where customized IP combinations provide competitive advantages. Foundries and packaging specialists investing in chiplet integration capabilities are well-positioned to capitalize on this emerging paradigm shift in semiconductor design.

Advanced Packaging Innovations Enabling New Applications

Breakthroughs in packaging technologies such as 3D IC stacking and silicon interposers are expanding the addressable market for bare chips. These innovations overcome traditional limitations in interconnect density and power efficiency, making bare dies viable for applications previously dominated by monolithic ICs. Heterogeneous integration capabilities are particularly valuable for medical devices, aerospace systems, and high-end computing, where performance-per-watt metrics are critical. The advanced packaging sector is projected to outpace overall semiconductor market growth, creating new opportunities for bare chip suppliers to collaborate with packaging specialists on integrated solutions.

Regional Semiconductor Ecosystem Development Fostering Local Supply Chains

Government initiatives worldwide to develop domestic semiconductor capabilities are creating favorable conditions for bare chip manufacturers. Significant investments in regional semiconductor ecosystems, particularly in North America and Asia, include substantial funding for fabrication facilities, packaging houses, and testing centers. These initiatives aim to reduce reliance on global supply chains and create vertically integrated regional capabilities. Bare chip suppliers establishing local operations near these emerging clusters can benefit from government incentives while securing long-term partnerships with domestic semiconductor companies.

MARKET CHALLENGES

Material Shortages and Price Volatility Impacting Production Stability

The bare chip manufacturing process relies on specialized materials with limited global supply bases. Recent years have seen significant price fluctuations and allocation conditions for critical items including high-purity silicon wafers, specialty gases, and packaging substrates. These supply constraints, combined with extended lead times for semiconductor equipment, create production planning challenges. While fab capacities are expanding, these material bottlenecks continue to impact throughput rates and potentially delay new technology adoption timelines across the industry.

Other Challenges

Testing Complexity for Advanced Nodes

The verification and testing of bare chips at leading-edge nodes presents growing technical and economic challenges. Smaller feature sizes and complex 3D structures require sophisticated test methodologies and equipment, with test costs representing an increasing proportion of total production expenses. The industry faces ongoing difficulties in developing cost-effective testing solutions that maintain quality standards while keeping pace with performance demands.

Intellectual Property Security Concerns

The distributed nature of chiplet-based designs and advanced packaging introduces new intellectual property protection challenges. Ensuring security across multiple supplier ecosystems becomes increasingly complex as functions are disaggregated across multiple bare dies. These concerns may slow adoption of innovative integration approaches until robust security frameworks become widely established.

BARE CHIP MARKET TRENDS

Expansion of Semiconductor Applications Drives Bare Chip Market Growth

The global bare chip market is experiencing robust growth, fueled by the increasing adoption of semiconductor technology across multiple industries. Beyond traditional applications like consumer electronics and telecommunications, bare chips are gaining prominence in automotive electronics, medical devices, and industrial automation. The automotive sector, in particular, has witnessed significant demand due to the integration of advanced driver-assistance systems (ADAS) and electric vehicle (EV) technologies, requiring high-performance bare chips for efficient power management. Furthermore, emerging applications in artificial intelligence (AI) and the Internet of Things (IoT) are pushing manufacturers to develop bare chips with enhanced processing capabilities and energy efficiency.

Other Trends

Miniaturization and Advanced Packaging Techniques

The rising demand for compact, high-performance electronic components has led to increased adoption of advanced packaging techniques such as flip-chip and chip-on-board (COB) solutions. These technologies improve thermal performance, reduce signal loss, and enhance electrical connections, making them ideal for applications in 5G infrastructure, wearables, and high-performance computing. While flip-chip technology has dominated the market due to its superior interconnect density, COB solutions remain popular in cost-sensitive applications where space optimization is critical. The ongoing shift towards 3D IC packaging is also creating new growth opportunities for bare chip manufacturers.

Geopolitical Factors and Supply Chain Realignment

Global semiconductor supply chain disruptions have prompted a strategic realignment in the bare chip market, with companies diversifying production locations and increasing investment in domestic manufacturing capabilities. Governments worldwide are implementing policies to strengthen semiconductor self-sufficiency, leading to new fabrication facilities in regions like North America and Europe. Meanwhile, Asia maintains its stronghold in bare chip production, with China, Taiwan, and South Korea collectively accounting for a significant share of global manufacturing capacity. This geographic diversification is reshaping procurement strategies while ensuring a more resilient supply chain for critical industries.

COMPETITIVE LANDSCAPE

Key Industry Players

Semiconductor Giants Dominate as Emerging Players Disrupt Traditional Dynamics

The global bare chip market features a dynamic competitive landscape, with established semiconductor leaders competing alongside specialized foundries and emerging regional players. While the market remains dominated by multinational corporations, recent supply chain disruptions have accelerated shifts in market share distribution. Texas Instruments maintains a strong position, leveraging its vertically integrated manufacturing capabilities and broad portfolio spanning automotive, industrial, and consumer applications.

Infineon Technologies and ROHM Semiconductor have significantly expanded their bare chip offerings, particularly for automotive and power electronics applications. Both companies benefited from the accelerated adoption of electric vehicles and renewable energy systems, with Infineon reporting a 29% year-over-year growth in its automotive segment in 2023.

Meanwhile, packaging specialists like Shinko Electric Industries are gaining traction through advanced interconnect solutions that bridge bare chips with final packaged products. The company’s recent investments in fan-out wafer-level packaging (FOWLP) technology position it strongly for next-generation applications where bare chip performance is critical.

Asia-based players are making notable inroads, with Shanghai Jita Semiconductor capturing market share through cost-competitive offerings for consumer electronics. The company’s recent capacity expansion aligns with China’s push for semiconductor self-sufficiency, though it still trails global leaders in advanced node capabilities.

List of Key Bare Chip Market Players

- Texas Instruments (U.S.)

- Infineon Technologies (Germany)

- ROHM Semiconductor (Japan)

- Shinko Electric Industries (Japan)

- ON Semiconductor Inc. (U.S.)

- Micron Technology (U.S.)

- Synopsys Inc. (U.S.)

- Micross (U.S.)

- Shanghai Jita Semiconductor Co., Ltd. (China)

- Chengdu Hanxin Guoke Integration Technology Co., Ltd. (China)

- Die Devices (U.S.)

- Box Optronics (U.S.)

- Central Semiconductor Corp. (U.S.)

Segment Analysis:

By Type

Flip Chip Segment Leads Due to Superior Performance in High-Density Packaging

The market is segmented based on type into:

- Chip-on-Board (COB)

- Flip Chip

- Subtypes: Copper pillar bumps, solder bumps, and others

By Application

Consumer Electronics Drives Demand Owing to Miniaturization Trends in Smart Devices

The market is segmented based on application into:

- Consumer Electronics Products

- Telecommunications

- Automotive

- Medical

- Others

By Packaging Technology

Fan-Out WLP Gains Traction for Advanced Semiconductor Packaging Solutions

The market is segmented based on packaging technology into:

- Wafer-Level Packaging (WLP)

- 3D IC Packaging

- System-in-Package (SiP)

By End-User Industry

Automotive Sector Shows Strong Growth Potential with Increasing Semiconductor Content per Vehicle

The market is segmented based on end-user industry into:

- Electronics Manufacturing

- Automotive

- Healthcare

- Industrial

Regional Analysis: Bare Chip Market

Asia-Pacific

The Asia-Pacific region dominates the global Bare Chip market, accounting for over 55% of total demand due to strong semiconductor manufacturing ecosystems in China, Japan, South Korea, and Taiwan. China leads in both production and consumption, driven by its “Made in China 2025” initiative and massive investments in semiconductor self-sufficiency. Meanwhile, Japan remains a key player in advanced packaging technologies, with companies like Shinko Electric Industries pioneering high-density interconnect solutions. However, geopolitical tensions and export controls create supply chain challenges, particularly for advanced node technologies. The region benefits from tight integration between foundries and assembly houses.

North America

North America captures approximately 20% of the global Bare Chip market, primarily serviced by fabless semiconductor companies and specialized bare die suppliers. The U.S. passed the CHIPS and Science Act in 2022, allocating $52 billion to boost domestic semiconductor production, which will influence bare chip supply. There’s increasing demand from aerospace/defense applications where unpackaged dies are preferred for space-constrained designs. However, reliance on Asian foundries for wafer supply creates vulnerabilities, prompting reshoring efforts. The region leads in R&D for advanced packaging like fan-out wafer-level packaging (FOWLP) for bare die applications.

Europe

The European Bare Chip market focuses on automotive and industrial applications, benefiting from strict quality requirements in these sectors. Germany’s Infineon and Netherlands’ NXP are key suppliers of automotive-grade bare dies. The European Chips Act aims to double the EU’s semiconductor market share to 20% by 2030, which may alter supply dynamics. However, Europe lacks leading-edge wafer production capacity, depending primarily on external suppliers for advanced nodes. The medical device industry presents growth opportunities for specialty bare chips due to miniaturization trends in implantable devices and diagnostic equipment.

Middle East & Africa

This emerging region shows potential in localized packaging and test services, particularly in Israel and the UAE. While wafer production is minimal, some governments are investing in downstream assembly capabilities to diversify from oil dependency. Israel’s Tower Semiconductor provides specialty foundry services for niche bare chip applications. However, infrastructure limitations and lack of local demand restrict market growth. Some growth is expected in telecommunication base stations and oil/gas sensor applications where rugged bare die solutions are preferred for extreme environments.

South America

South America remains the smallest regional market, constrained by limited semiconductor manufacturing infrastructure. Brazil has some assembly/test operations catering to consumer electronics and automotive sectors, with most bare chips imported from Asia. Government initiatives like Brazil’s PADIS program provide tax incentives for semiconductor activities, though impact has been limited. The market shows potential as a secondary sourcing location for North American companies seeking to diversify supply chains, but political/economic instability continues to deter major investments in wafer production facilities.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Bare Chip markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Bare Chip Market?

-> Bare Chip market size was valued at US$ 4.67 billion in 2024 and is projected to reach US$ 8.91 billion by 2032, at a CAGR of 8.4% during the forecast period 2025-2032.

Which key companies operate in Global Bare Chip Market?

-> Key players include Shinko Electric Industries, Micross, Texas Instruments, ON Semiconductor, ROHM Semiconductor, Infineon Technologies, Micron Technology, and Synopsys Inc, among others.

What are the key growth drivers?

-> Key growth drivers include rising demand for advanced semiconductor packaging, miniaturization of electronic devices, growth in IoT and AI applications, and increasing automotive electronics adoption.

Which region dominates the market?

-> Asia-Pacific dominates the market with over 60% share in 2024, led by semiconductor manufacturing hubs in China, Taiwan, South Korea, and Japan.

What are the emerging trends?

-> Emerging trends include 3D chip stacking technology, wafer-level packaging advancements, heterogeneous integration, and increasing adoption in automotive power electronics.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...