Aviation Sensors Market Insights

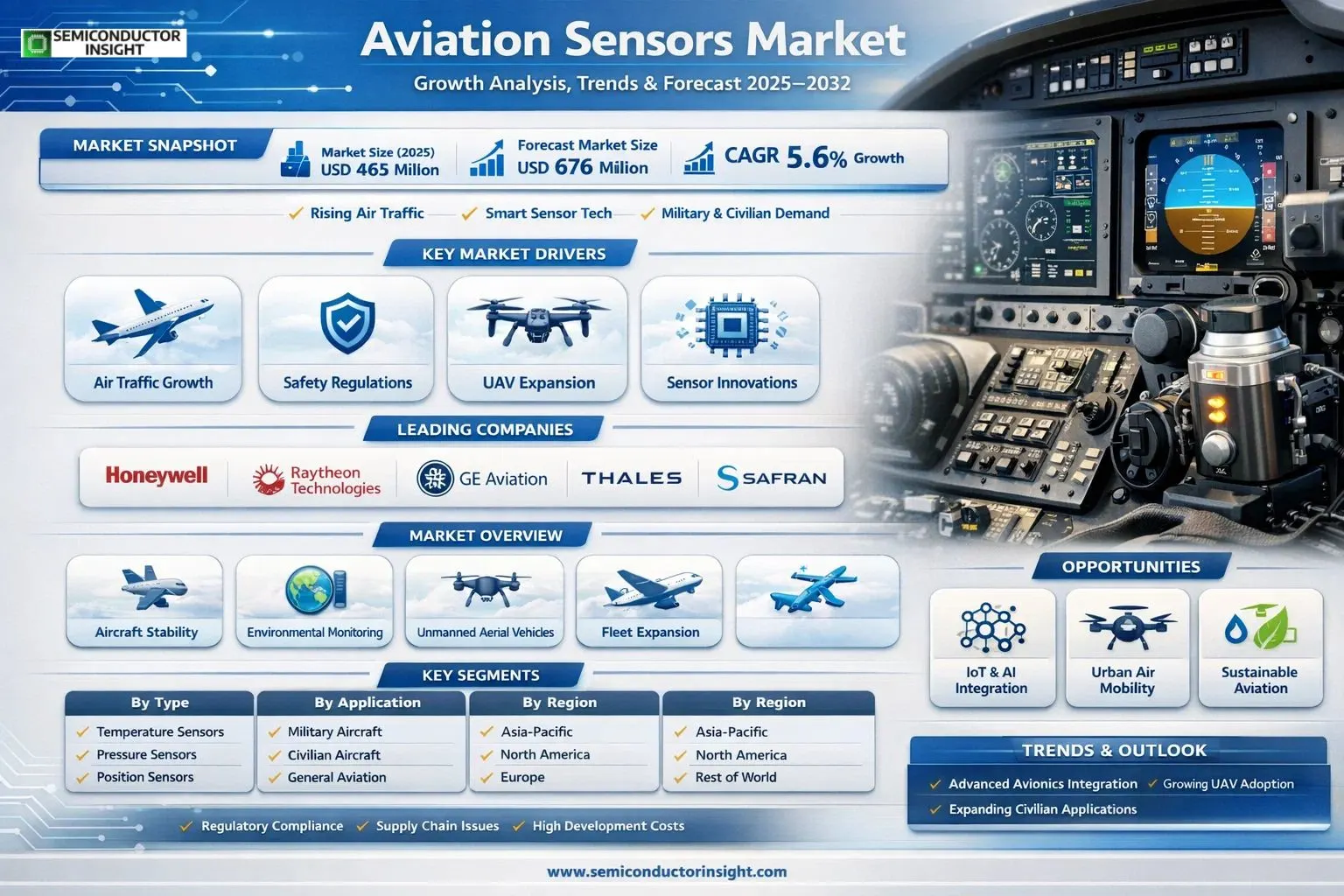

Global Aviation Sensors market size was valued at USD 465 million in 2025. The market is projected to reach USD 676 million by 2032, exhibiting a CAGR of 5.6% during the forecast period.

Aviation sensors are specialized measuring instruments crucial for ensuring aircraft stability and safety during flight. These sensors monitor environmental changes around the aircraft, facilitating real-time data for navigation, control, and performance optimization. They represent one of the most vital components of avionics equipment on an aircraft. Key types include Temperature Sensors, Humidity Sensors, Oxygen Sensors, Pressure Sensors, Flow Sensors, Speed Sensors, and Position Sensors.

The market is experiencing steady growth driven by factors such as rising global air traffic, stringent safety regulations from bodies like the FAA and EASA, and advancements in smart sensor technologies. Furthermore, the surge in unmanned aerial vehicle (UAV) deployments and commercial fleet expansions are accelerating demand. Key players are bolstering innovation through strategic initiatives. Honeywell International Inc., Raytheon Company, GE Aviation, United Technologies Corp, Thales, Meggitt PLC, Safran SA, and TE Connectivity Ltd. dominate with comprehensive portfolios, holding significant revenue shares among the top manufacturers.

MARKET DRIVERS

Technological Advancements

Aviation Sensors Market is propelled by rapid innovations in micro-electro-mechanical systems (MEMS) and fiber optic sensors, enabling lighter, more precise measurements for flight controls and engine monitoring. These technologies enhance aircraft performance and fuel efficiency, aligning with global sustainability goals. With the integration of smart sensors in modern airframes, manufacturers are achieving real-time data analytics that reduce operational downtimes.

Surging Air Traffic Demand

Global air passenger traffic is projected to reach 4.7 billion by 2025, driving demand for advanced sensors in commercial aviation fleets. Airlines are retrofitting older aircraft with next-generation inertial and pressure sensors to meet heightened safety standards. This expansion supports Aviation Sensors Market’s growth trajectory at a CAGR of approximately 7.2% through 2030.

➤ Key growth factor: UAV proliferation, with over 1 million commercial drones expected by 2030, necessitating compact, rugged sensors for navigation and obstacle avoidance.

Furthermore, the push for autonomous flight systems amplifies the need for reliable environmental and vibration sensors, fostering market expansion across military and civil sectors.

MARKET CHALLENGES

Regulatory Compliance Hurdles

Navigating stringent certifications from FAA and EASA poses significant challenges in Aviation Sensors Market, often extending development timelines by 18-24 months. Compliance testing for harsh environmental conditions, such as extreme temperatures and vibrations, requires extensive validation, increasing project costs by up to 30%.

Other Challenges

Supply Chain Disruptions

Post-pandemic shortages of rare earth materials critical for sensor manufacturing have delayed production, impacting 25% of OEM deliveries. Geopolitical tensions exacerbate this, forcing diversification strategies.Integration complexities with legacy avionics systems further complicate upgrades, demanding custom interfaces that elevate engineering expenses and slow market penetration in regional aviation.

MARKET RESTRAINTS

High Development Costs

Elevated R&D investments, averaging $50-100 million per sensor platform, restrain smaller players in Aviation Sensors Market. The need for redundancy and fail-safe designs multiplies expenses, limiting innovation to major incumbents like Honeywell and Safran.Volatile raw material prices, influenced by semiconductor shortages, add financial pressure, with costs rising 15% in recent years. This hampers scalability for emerging applications in electric vertical takeoff vehicles.Cybersecurity vulnerabilities in connected sensor networks introduce risks, prompting cautious adoption amid evolving threats. Airlines prioritize proven technologies, curbing rapid market shifts.Economic uncertainties, including fluctuating fuel prices and reduced fleet investments during downturns, further constrain growth in commercial aviation segments.

MARKET OPPORTUNITIES

IoT and AI Integration

Aviation Sensors Market stands to benefit from IoT-enabled predictive maintenance, potentially saving airlines $4-5 billion annually in downtime costs. AI algorithms processing sensor data for anomaly detection will drive adoption in next-gen aircraft.Urban air mobility initiatives, with eVTOL deliveries forecasted at 25,000 units by 2030, create demand for lightweight, high-accuracy sensors in propulsion and battery management systems.Sustainable aviation fuels and hybrid-electric propulsion open avenues for advanced temperature and flow sensors, supporting net-zero emission targets by 2050.Aftermarket services, including sensor retrofits for aging fleets, represent a $2 billion opportunity, bolstered by digital twin technologies for enhanced lifecycle management.

Aviation Sensors Market Trends

Integration of Advanced Sensors in Avionics for Enhanced Safety

Aviation sensors play a critical role in monitoring environmental changes to ensure aircraft stability and safety during flight. In Aviation Sensors Market, there is a strong push toward integrating advanced sensors within avionics systems. These instruments detect variations in pressure, temperature, humidity, oxygen levels, flow, speed, and position, enabling real-time data for pilots and automated systems. Manufacturers are focusing on precision and reliability to meet stringent regulatory standards from bodies like the FAA and EASA. This trend is driven by the need for superior situational awareness, particularly in complex flight conditions.

Other Trends

Diversification Across Sensor Types

Aviation Sensors Market shows diversification in product types, with pressure sensors, position sensors, and speed sensors gaining prominence alongside traditional temperature and humidity sensors. This expansion addresses varied aircraft requirements, from engine monitoring to flight control surfaces. Industry surveys highlight that suppliers are innovating to combine multiple sensing capabilities into compact modules, reducing weight and improving efficiency in modern aircraft designs.

Growth in Military and Civilian Applications

Applications in both military and civilian sectors are shaping Aviation Sensors Market. Military uses demand rugged sensors for high-stress environments, while civilian aviation emphasizes cost-effective, lightweight solutions for commercial fleets. Key players like Honeywell International Inc., Raytheon Company, and GE Aviation are leading developments tailored to these segments. Recent advancements include enhanced oxygen and flow sensors for life support systems in fighters and passenger jets alike. Regional dynamics show North America maintaining leadership due to established manufacturers, while Asia, particularly China and Japan, is emerging with increased production to support growing fleets.

Competitive landscapes reveal top firms holding significant shares through mergers and R&D investments. Challenges include supply chain disruptions and cybersecurity risks for connected sensors, prompting a shift toward resilient designs. Overall, Aviation Sensors Market is evolving with emphasis on smart, interconnected technologies that support next-generation aircraft autonomy and sustainability goals.

COMPETITIVE LANDSCAPE

Key Industry Players

Aviation Sensors Market Leaders and Strategic Positioning

Aviation Sensors Market exhibits an oligopolistic structure dominated by established aerospace giants, with Honeywell International Inc. leading as a primary innovator in avionics sensing technologies. Honeywell’s extensive portfolio, encompassing pressure, temperature, and position sensors critical for flight stability and safety, positions it at the forefront, supported by its robust R&D investments and integration with major aircraft OEMs. Raytheon Company, GE Aviation, United Technologies Corp (now part of RTX), and Thales collectively command a substantial revenue share, leveraging synergies in military and civilian applications. This concentration among top players fosters innovation in sensor precision and reliability, amid a market projected to grow from $465 million in 2025 to $676 million by 2032 at a 5.6% CAGR, driven by rising air traffic and stringent safety regulations.

Beyond the frontrunners, niche players like Meggitt PLC, Safran SA, and Esterline Technologies Corporation carve out specialized roles, focusing on advanced humidity, flow, and oxygen sensors for extreme aviation environments. Companies such as Eaton Corporation and TE Connectivity Ltd. excel in connectivity-integrated sensors, addressing emerging needs in smart avionics and unmanned systems. Additional significant contributors including Ametek, Crane Co., Stellar Technology, Curtiss-Wright Corporation, and CETC provide tailored solutions for regional markets, particularly in Asia-Pacific defense sectors. This diverse competitive ecosystem encourages mergers, acquisitions, and technological collaborations, enhancing market resilience against supply chain challenges and regulatory hurdles while spurring advancements in sensor miniaturization and data analytics for predictive maintenance.

List of Key Aviation Sensors Companies Profiled

- Honeywell International Inc.

- Raytheon Company

- GE Aviation

- United Technologies Corp

- Thales

- Meggitt PLC

- Safran SA

- Esterline Technologies Corporation

- Eaton Corporation

- TE Connectivity Ltd.

- Ametek

- Crane Co.

- Stellar Technology

- Curtiss Wright Corporation

- CETC

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Leading Segment: Pressure Sensor

|

| By Application |

|

Leading Segment: Civilian Aircraft

|

| By End User |

|

Leading Segment: OEMs

|

| By Platform |

|

Leading Segment: Fixed-Wing Aircraft

|

| By Technology |

|

Leading Segment: MEMS Sensors

|

Regional Analysis: Aviation Sensors Market

North America

Strong aerospace heritage fuels demand for precision aviation sensors market solutions. Fleet modernization initiatives prioritize sensors for fuel efficiency and safety. Government contracts bolster military sensor deployments, while urban air mobility concepts spur lightweight, compact designs.

Industry giants like Honeywell and Collins Aerospace dominate, offering integrated sensor suites. Their extensive portfolios cover flight control and engine health monitoring, supported by robust service networks. Strategic partnerships enhance market penetration.

Focus on IoT-enabled sensors enables data analytics for proactive maintenance. Fiber optic and MEMS technologies improve accuracy in harsh environments. R&D investments drive AI integration for autonomous flight systems.

FAA certifications streamline approvals for sensor innovations. Emphasis on cybersecurity and data integrity shapes compliance. Harmonized standards with EASA facilitate exports, strengthening aviation sensors market leadership.

Europe

Europe’s aviation sensors market thrives on a collaborative ecosystem centered around Airbus and suppliers like Safran. Emphasis on sustainable aviation fuels and noise reduction drives demand for advanced environmental sensors. The EASA’s rigorous certification processes ensure seamless integration across multinational fleets. Regional focus on digitalization introduces next-generation sensors for connected aircraft, enhancing operational resilience. Defense sector growth, particularly in unmanned systems, expands applications for ruggedized navigation sensors. Supply chain diversification post-disruptions strengthens resilience, while EU-funded projects accelerate innovations in health monitoring and vibration analysis for extended aircraft lifespans.

Asia-Pacific

Asia-Pacific emerges as a dynamic hub in Aviation Sensors Market, propelled by rapid fleet expansion from airlines in China and India. Local manufacturing ramps up to meet booming air travel, with sensors vital for cost-effective maintenance. Government initiatives promote indigenous aerospace capabilities, fostering sensor localization. Urban air mobility and drone regulations spur lightweight sensor development. Regional collaborations with global players transfer technology, boosting precision in flight control systems. Supply chain integration with Southeast Asian hubs enhances efficiency, positioning the region for sustained growth in commercial and cargo aviation.

South America

South America’s aviation sensors market gains momentum from increasing air connectivity in Brazil and neighboring countries. Emphasis on regional manufacturing supports domestic fleets with reliable engine and structural health sensors. Infrastructure upgrades prioritize safety enhancements amid challenging terrains, driving adoption of weather-resilient systems. Partnerships with North American firms introduce advanced diagnostics for aging aircraft. Growing cargo operations demand robust logistics sensors, while biofuel experiments integrate environmental monitoring. Regulatory alignment with international standards facilitates technology imports, nurturing a maturing aviation sensors market landscape.

Middle East & Africa

The Middle East & Africa aviation sensors market benefits from ambitious airline expansions and hub developments. Premium carriers invest in luxury cabin sensors for passenger comfort and safety. Harsh climate adaptations favor durable, high-precision systems for navigation and fuel management. Defense modernization introduces military-grade sensors, while African initiatives focus on affordable solutions for regional connectivity. Cross-continental collaborations enhance supply chains, promoting sensor innovations for long-haul operations. Sustainable aviation goals integrate low-emission monitoring, solidifying the region’s strategic role in global aviation sensors market dynamics.

Report Scope

This market research report provides a comprehensive analysis of Aviation Sensors Market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of aviation sensors in powering advancements across industries such as commercial aviation, military aircraft, unmanned systems, and general aviation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Aviation Sensors Market?

-> Aviation Sensors Market was valued at USD 465 million in 2025 and is expected to reach USD 676 million by 2032 at a CAGR of 5.6%.

Which key companies operate in Aviation Sensors Market?

-> Key players include Honeywell International Inc., Raytheon Company, GE Aviation, United Technologies Corp, Thales, Meggitt PLC, Safran SA, Esterline Technologies Corporation, Eaton Corporation, TE Connectivity Ltd., among others.

What are the key growth drivers?

-> Key growth drivers include demand for aircraft stability and safety monitoring, expansion in military and civilian aviation, and advancements in avionics equipment.

Which region dominates the market?

-> North America is a key market with significant U.S. presence, while Asia shows strong potential in China and other countries.

What are the emerging trends?

-> Emerging trends include growth in segments like Temperature Sensor, Pressure Sensor, Position Sensor, and focus on military and civilian applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...