Autonomous Control Systems Market Insights

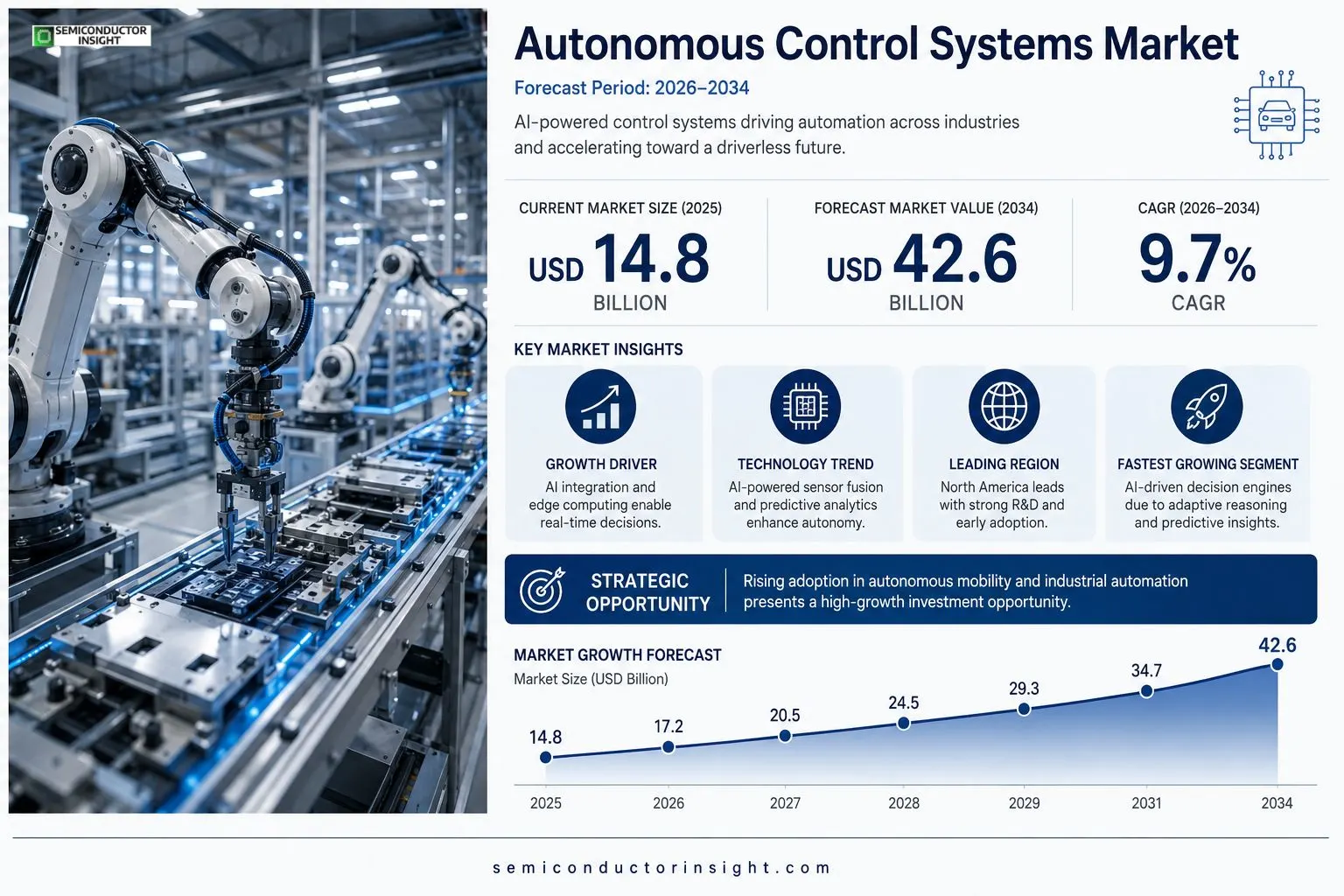

Global autonomous control systems market size was valued at USD 14.8 billion in 2025. The market is projected to grow from USD 15.2 billion in 2025 to USD 42.6 billion by 2034, exhibiting a CAGR of 9.7% during the forecast period.

Autonomous control systems comprise integrated hardware and software that enable machines,such as industrial robots, unmanned aerial vehicles and self‑driving cars,to perceive their environment, make real‑time decisions and execute precise actions without human intervention. Core components include sensor‑fusion algorithms, predictive‑analytics engines and safety‑critical actuators.The market is accelerating because of rapid advances in artificial intelligence, expanding demand for automation in manufacturing and logistics, and supportive regulatory frameworks for driverless transportation. Furthermore, rising capital spending by OEMs and strategic partnerships,e.g., the March 2024 alliance between NVIDIA and Bosch to co‑develop AI‑powered control modules,are fueling growth among key players such as Siemens AG, Honeywell International and Continental AG.

MARKET DRIVERS

Rapid Integration of AI and Edge Computing

Autonomous Control Systems Market is being propelled by the convergence of artificial intelligence with edge‑computing platforms, allowing real‑time decision making in vehicles, drones, and industrial robots. Manufacturers are deploying AI‑enhanced control loops that reduce latency and improve safety, creating a strong growth foundation.

Expanding Regulatory Support for Autonomy

Governments worldwide are issuing guidelines that standardize testing protocols for autonomous operations, especially in logistics and transportation. This regulatory clarity lowers entry barriers, encouraging investment and accelerating market adoption.

➤ Industry analysts forecast a compound annual growth rate exceeding 12% through 2035, driven largely by these technological and policy enablers.

In addition, the rise of connected ecosystems,where autonomous devices communicate via 5G and private networks,creates network effects that further stimulate demand across sectors such as agriculture, mining, and smart manufacturing.

MARKET CHALLENGES

High Development Costs and Skill Gaps

Designing reliable autonomous control algorithms requires substantial R&D investment and specialized talent. Many firms face budgetary constraints while struggling to recruit engineers proficient in machine learning, sensor fusion, and safety‑critical coding.

Other Challenges

Cybersecurity Vulnerabilities

As systems become more interconnected, the risk of malicious intrusion rises, compelling manufacturers to embed robust security layers that add complexity and cost.

MARKET RESTRAINTS

Stringent Safety Certification Processes

Obtaining safety certifications such as ISO 26262 or IEC 61508 involves extensive testing and documentation. The time‑intensive nature of these procedures can delay product launches, limiting the speed at which new autonomous solutions reach the market.

MARKET OPPORTUNITIES

Emerging Applications in Renewable Energy Management

Autonomous control technologies are increasingly being applied to optimize wind‑farm turbine positioning and solar‑panel tracking, delivering efficiency gains and reducing operational costs. This niche presents a lucrative growth avenue for companies that can tailor control systems to renewable‑energy infrastructures.

Autonomous Control Systems Market Trends

AI‑Driven Sensor Fusion Fuels Rapid Adoption

The integration of advanced sensor‑fusion algorithms with predictive‑analytics engines is reshaping how machines perceive and react to dynamic environments. By combining lidar, radar, and camera inputs in real time, autonomous platforms achieve higher reliability and lower latency, which directly supports expanded use in manufacturing lines and logistics hubs. Edge‑computing capabilities now allow these complex models to run on localized processors, reducing dependence on cloud connectivity and enhancing security. Continuous model optimization through reinforcement learning further refines decision‑making under variable conditions. Moreover, the adoption of lightweight neural networks optimized for low‑power microcontrollers is expanding the viability of autonomous functions in smaller equipment such as AGVs and precision farming drones. These developments collectively lower total cost of ownership and accelerate customer migration from legacy control loops to fully autonomous solutions. This technical progression is a core catalyst for Autonomous Control Systems Market, enabling OEMs to deliver products that meet increasingly stringent performance benchmarks without additional human oversight.

Other Trends

Strategic OEM Partnerships

Collaborations between hardware specialists and AI leaders are accelerating development cycles. Notably, the March 2024 alliance between NVIDIA and Bosch to co‑develop AI‑powered control modules exemplifies how joint R&D reduces time‑to‑market for next‑generation solutions. Similar partnerships among Siemens AG, Honeywell International, and Continental AG are focusing on modular architectures that simplify integration across vehicle and industrial robot platforms. These alliances deepen the technology pool available to end users and reinforce the market’s momentum. In addition, joint standard‑setting initiatives and shared test‑beds are emerging, allowing partners to validate safety functions collectively and streamline certification pathways, which further drives adoption among system integrators.

Emerging Safety Standards and Regulatory Momentum

Regulatory bodies worldwide are establishing clearer safety frameworks for driverless vehicles and autonomous industrial equipment. New standards emphasize functional safety, cybersecurity resilience, and rigorous validation protocols. As compliance requirements become more predictable, manufacturers are investing in safety‑critical actuators and redundant control pathways, thereby strengthening confidence among end‑users. International organizations such as ISO and national agencies like the U.S. NHTSA are publishing guidance that aligns testing procedures across regions, reducing the complexity of multi‑market launches. This regulatory clarity is reducing barriers to entry and prompting broader adoption across transportation and factory automation sectors, further reinforcing the overall market trajectory and encouraging long‑term investment in resilient control architectures. Several leading logistics providers have already deployed autonomous fleets in Europe and Asia, demonstrating tangible efficiency gains and setting industry benchmarks for future expansions.

COMPETITIVE LANDSCAPEKey Industry Players

Autonomous Control Systems Market – Competitive Overview

Autonomous Control Systems Market is dominated by a mix of traditional industrial automation giants and rapidly evolving AI‑focused firms. Siemens AG leverages its extensive portfolio of PLCs, sensor‑fusion software, and industrial IoT platforms to serve automotive, aerospace and heavy‑equipment OEMs, establishing a strong foothold in large‑scale deployments. Honeywell International and Bosch combine deep safety‑critical hardware expertise with AI‑acceleration capabilities, positioning themselves as preferred partners for regulated sectors such as autonomous vehicles and unmanned aerial systems. Meanwhile, NVIDIA’s GPU‑centric AI processors and its 2024 partnership with Bosch catalyze the development of high‑performance control modules, accelerating market growth and reshaping the competitive hierarchy.Beyond the incumbents, a vibrant ecosystem of niche innovators contributes specialized value. ABB and Schneider Electric focus on energy‑efficient actuators and modular control architectures for smart factories. Mitsubishi Electric and Rockwell Automation deliver vertically integrated solutions for robotics and logistics automation. New‑age players such as Aurora Innovation, Waymo (Alphabet), and Cruise (General Motors) concentrate on end‑to‑end autonomous driving stacks, often partnering with legacy hardware manufacturers to integrate safety‑critical actuators. The cumulative effect is a fragmented yet collaborative landscape where strategic alliances, joint R&D programs, and cross‑licensing agreements drive differentiation and market expansion.

List of Key Autonomous Control Systems Companies Profiled

- Siemens AG

- Honeywell International

- Continental AG

- NVIDIA

- Bosch

- ABB

- Schneider Electric

- Rockwell Automation

- Mitsubishi Electric

- Toyota Industries

- Aurora Innovation

- Waymo (Alphabet)

- Cruise (General Motors)

- Zoox (Amazon)

- Tesla

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

AI‑Driven Decision Engines

|

| By Application |

|

Industrial Automation

|

| By End User |

|

OEM Manufacturers

|

| By Technology |

|

Edge Computing Platforms

|

| By Industry |

|

Automotive

|

Regional Analysis: North America

United States

The manufacturing sector in the United States is increasingly adopting autonomous control systems to optimize production lines, enhance quality control, and improve overall efficiency. This involves integrating sophisticated sensors, actuators, and software solutions to automate various processes, leading to reduced operational costs and increased output. The rising need for precision and consistency in manufacturing is a key driver.

The transportation and logistics industry is witnessing a surge in the implementation of autonomous control systems for warehouse management, fleet optimization, and supply chain automation. This includes the use of automated guided vehicles (AGVs), robotic systems, and intelligent traffic management systems to streamline operations and enhance responsiveness. The growing e-commerce sector further accelerates this trend.

The energy infrastructure sector is leveraging autonomous control systems for monitoring, maintenance, and operational efficiency of power grids, oil and gas facilities, and renewable energy plants. This involves deploying advanced sensors and control algorithms to ensure reliable and safe energy distribution and production. Predictive maintenance capabilities are gaining traction.

Within healthcare, autonomous control systems are being implemented for tasks such as robotic surgery assistance, automated laboratory processes, and smart hospital management systems. These systems contribute to improved accuracy, reduced recovery times, and enhanced patient care while optimizing resource allocation within healthcare facilities.

Europe

Europe represents the second largest market for Autonomous Control Systems, with significant growth potential across various industries. The region’s strong focus on sustainability and industrial automation is driving demand for these systems. Several countries, including Germany, the UK, and France, are leading the adoption efforts. The emphasis is on integrating autonomous solutions to improve energy efficiency, enhance manufacturing capabilities, and optimize supply chains within the European Union.

Asia-Pacific

The Asia-Pacific region is poised for rapid expansion in Autonomous Control Systems Market. Driven by increasing industrialization in countries like China, Japan, and South Korea, coupled with growing investments in smart manufacturing, the demand for advanced control systems is escalating. The region’s large manufacturing base and rising adoption of digital technologies are key factors propelling market growth. The focus is shifting towards automation in sectors like automotive, electronics, and consumer goods.

South America

South America presents a promising but relatively nascent market for Autonomous Control Systems. The increasing need for efficiency in agriculture, mining, and infrastructure development is creating opportunities for adoption. Countries like Brazil and Argentina are witnessing a gradual increase in investments in automation technologies. Overcoming infrastructure challenges and fostering technological expertise will be crucial for sustained growth in this region.

Middle East & Africa

The Middle East and Africa region is experiencing growing interest in Autonomous Control Systems, particularly in sectors like oil and gas, construction, and logistics. Investments in smart city initiatives and infrastructure projects are driving demand. The region’s focus on diversifying economies and improving operational efficiency is contributing to the adoption of automation technologies. Further development of local expertise and supportive regulatory frameworks will be important for market advancement.

Report Scope

This market research report provides a comprehensive analysis of the Autonomous Control Systems Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Autonomous Control Systems Market?

-> Autonomous Control Systems Market was valued at USD 14.8 billion in 2025 and is expected to reach USD 42.6 billion by 2034.

Which key companies operate in Autonomous Control Systems Market?

-> Key players include Siemens AG, Honeywell International, Continental AG, NVIDIA, and Bosch.

What are the key growth drivers?

-> Key growth drivers include advancements in artificial intelligence, rising demand for automation in manufacturing and logistics, supportive regulatory frameworks for driverless transportation, and increased OEM capital spending.

Which region dominates the market?

-> The reference does not specify a dominant region for Autonomous Control Systems Market.

What are the emerging trends?

-> Emerging trends include AI‑powered control modules, sensor‑fusion algorithms, predictive‑analytics engines, and safety‑critical actuator technologies.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...