MARKET INSIGHTS

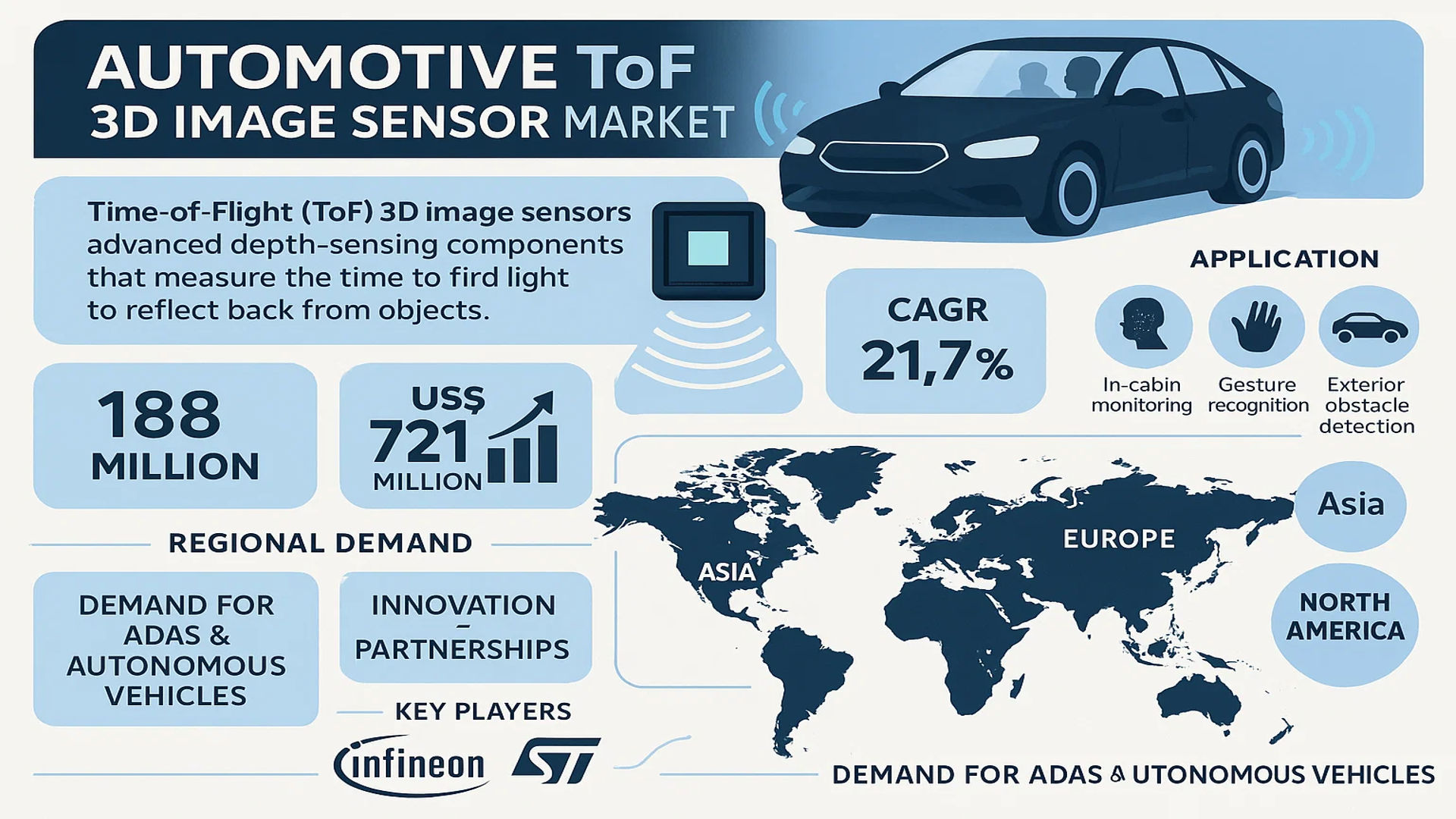

The global Automotive ToF 3D Image Sensor Market was valued at 188 million in 2024 and is projected to reach US$ 721 million by 2032, at a CAGR of 21.7% during the forecast period.

Time-of-Flight (ToF) 3D image sensors are advanced depth-sensing components that measure the time taken for light to reflect back from objects, enabling precise three-dimensional mapping. These sensors are increasingly deployed in automotive applications for in-cabin monitoring, gesture recognition, and short-range exterior obstacle detection. Major variants include Direct ToF (dToF) and Indirect ToF (iToF), each offering distinct advantages in accuracy and power efficiency.

The market growth is fueled by rising demand for advanced driver-assistance systems (ADAS) and autonomous vehicles, which rely on 3D sensing for real-time environmental perception. While Asia dominates automotive production (56% global share per OICA data), Europe and North America lead in ADAS adoption, creating regional demand hotspots. Key players like Infineon Technologies and STMicroelectronics are accelerating innovation, with recent partnerships focusing on miniaturization and cost reduction to broaden market penetration.

MARKET DYNAMICS

MARKET DRIVERS

Rising Adoption of ADAS and Autonomous Vehicles to Accelerate Demand

The automotive industry is undergoing a seismic shift towards advanced driver assistance systems (ADAS) and autonomous driving technologies, creating unprecedented demand for Time-of-Flight (ToF) 3D image sensors. These sensors play a critical role in enabling key safety features like adaptive cruise control, automatic emergency braking, and pedestrian detection. With over 50% of new vehicles worldwide expected to include Level 2+ autonomous capabilities by 2026, sensor manufacturers are experiencing heightened demand. Major automotive OEMs have increased their ADAS-related R&D budgets by an average of 23% year-over-year since 2020, signaling strong long-term commitment to sensor-based safety systems.

In-Cabin Monitoring Requirements Fuel Sensor Integration

Stringent safety regulations mandating driver monitoring systems (DMS) are propelling ToF sensor adoption. The European Union’s General Safety Regulation, which requires all new vehicles to include DMS by 2026, has created a ripple effect across global markets. ToF sensors excel in detecting driver fatigue, distraction, and occupant positioning – capabilities that are becoming standard in next-generation vehicles. Recent advancements in sensor resolution (now exceeding VGA quality) and reduced power consumption (below 100mW for latest models) make them ideal for continuous cabin monitoring without draining vehicle batteries.

Automotive Digitalization Trend Creates New Application Areas

The automotive interior revolution is opening new opportunities for ToF applications beyond traditional safety functions. Modern vehicles increasingly incorporate gesture control (projected 45% CAGR through 2032) and augmented reality displays that rely on precise depth sensing. Luxury automakers are leading this transformation, with several German brands already implementing 15+ ToF sensors per vehicle for various HMI and comfort features. As consumer expectations for smart vehicle interiors grow, mid-range manufacturers are following suit, creating a broader addressable market for sensor suppliers.

MARKET RESTRAINTS

High System Integration Costs Impede Mass Market Adoption

While ToF technology offers superior performance in many automotive applications, its implementation costs remain significantly higher than competing solutions like stereo cameras or ultrasonic sensors. A complete ToF system (including illumination, optics, and processing) can cost 3-5 times more than conventional alternatives, making it challenging to justify for entry-level vehicles. Manufacturers face ongoing pressure to reduce bill-of-materials costs while meeting OEMs’ demanding reliability standards (typically requiring >10-year lifespans), creating complex engineering trade-offs.

Performance Limitations in Extreme Conditions

Environmental factors present persistent challenges for ToF sensor deployment in vehicles. Performance degradation in adverse weather conditions (particularly heavy rain, snow, or fog) and under direct sunlight (can reduce effective range by over 60%) limits reliability for critical safety applications. While newer generations of sensors incorporate advanced filtering algorithms, achieving consistent performance across all operating conditions remains technically demanding. These limitations currently restrict ToF systems to secondary roles in many ADAS architectures rather than primary sensing functions.

Supply Chain Complexities and Component Shortages

The automotive semiconductor industry continues grappling with supply chain disruptions that particularly affect specialized components like ToF sensors. Lead times for key optoelectronic components recently exceeded 40 weeks, forcing automakers to redesign systems or seek alternative solutions. The specialized nature of automotive-grade ToF sensors (requiring ASIL-B or higher certification) creates additional supplier qualification challenges, limiting the number of viable manufacturing partners and creating bottlenecks in the production ramp-up phase.

MARKET OPPORTUNITIES

Emerging Applications in Electric and Shared Mobility

The rapid growth of electric vehicles and mobility-as-a-service presents untapped potential for ToF sensor applications. EV manufacturers are particularly interested in smart charging solutions using gesture control and enhanced battery management systems that could benefit from 3D sensing. Ride-sharing platforms are piloting advanced occupancy detection systems to improve fleet utilization, creating new demand for robust in-cabin monitoring that ToF sensors can uniquely provide. These segments are projected to account for over 35% of new ToF deployments by 2026.

Advancements in Sensor Fusion Architectures

Vehicle manufacturers are increasingly adopting heterogeneous sensor arrays where ToF complements other sensing modalities. This trend towards sensor fusion creates opportunities to develop specialized versions of ToF modules optimized for integration with radar, LiDAR, and vision systems. Recent breakthroughs in edge AI processing allow ToF sensors to perform on-sensor object classification, reducing bandwidth requirements for central ECUs. These technical developments are making ToF systems more viable for mass-market applications by improving overall system efficiency.

Aftermarket and Retrofit Potential

As regulatory requirements evolve and consumer awareness of vehicle safety grows, an emerging aftermarket for advanced sensing systems is taking shape. Fleet operators and safety-conscious consumers are driving demand for retrofit solutions that can upgrade existing vehicles. This segment currently represents less than 5% of the market but is growing at over 28% annually, offering sensor manufacturers an alternative path to market penetration beyond traditional OEM supply chains.

MARKET CHALLENGES

Intense Competition from Alternative Sensing Technologies

ToF sensor providers face mounting pressure from competing approaches like structured light and stereo vision systems that continue to improve in performance and cost-effectiveness. These alternatives now offer comparable depth resolution in many scenarios while benefiting from established manufacturing ecosystems. The competitive landscape is further complicated by the trend towards multi-modal sensing, where ToF must demonstrate clear advantages to maintain its value proposition against increasingly sophisticated alternatives.

Stringent Automotive Certification Requirements

Meeting automotive-grade qualification standards represents a significant hurdle for sensor manufacturers. The rigorous testing protocols (including 2,000+ hours of temperature cycling and mechanical stress tests) substantially increase development costs and time-to-market. Smaller players often struggle to bear these upfront investments, leading to industry consolidation as larger semiconductor companies acquire promising startups to accelerate their automotive qualification processes.

Data Privacy and Security Concerns

The extensive cabin monitoring capabilities of modern ToF systems raise legitimate privacy concerns that manufacturers must address. Regulatory bodies are increasing scrutiny on in-vehicle data collection practices, with several jurisdictions proposing strict limitations on biometric data processing. Ensuring compliance while maintaining system functionality requires sophisticated anonymization techniques that add complexity to sensor firmware and data processing pipelines.

AUTOMOTIVE TOF 3D IMAGE SENSOR MARKET TRENDS

Increased Adoption in Advanced Driver Assistance Systems (ADAS) Drives Market Growth

The automotive industry is witnessing a surge in demand for Time-of-Flight (ToF) 3D image sensors, primarily driven by their integration into advanced driver assistance systems (ADAS). These sensors enable precise depth perception, critical for applications such as automatic emergency braking, pedestrian detection, and adaptive cruise control. With over 90% of new vehicles in developed markets expected to feature some level of ADAS by 2030, automotive manufacturers are increasingly turning to ToF technology for its superior performance in varying light conditions compared to traditional 2D cameras. Recent direct ToF sensor innovations now achieve measurement accuracy within millimeters while consuming significantly less power, making them ideal for electric vehicles where energy efficiency is paramount.

Other Trends

In-Cabin Monitoring and Occupant Safety

The development of sophisticated in-cabin monitoring systems represents a major growth area for automotive ToF sensors. These systems can detect driver alertness, passenger positioning for optimized airbag deployment, and even child presence detection to prevent hot-car incidents. Leading automakers have begun implementing these solutions to meet upcoming Euro NCAP 2025 safety protocols, which will award additional points for advanced occupant monitoring. The technology has shown particular promise in commercial vehicle applications, where fatigue detection can significantly reduce accident rates among fleet operators.

Integration with Autonomous Driving Ecosystems

As automakers progress toward Level 3 and Level 4 autonomous vehicles, ToF sensors are becoming integral components of multi-modal perception systems. Their ability to provide real-time depth mapping complements LiDAR and radar technologies in creating comprehensive environment models for self-driving cars. Recent developments have seen sensor fusion algorithms improve dramatically, with some systems now processing ToF data alongside other inputs at frame rates exceeding 60 fps for seamless decision-making. Furthermore, the automotive industry’s push toward standardization of sensor interfaces has encouraged wider adoption, with the MIPI Alliance recently releasing specifications optimized for ToF implementations in vehicles.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Partnerships Drive Market Leadership

The Automotive ToF 3D Image Sensor market features a highly competitive ecosystem dominated by semiconductor giants and specialized sensor manufacturers. With the market projected to grow from $188 million in 2024 to $721 million by 2032 (21.7% CAGR), companies are aggressively expanding their portfolios to capture ADAS and autonomous vehicle opportunities.

Infineon Technologies leads the space with its REAL3™ sensor family, capturing approximately 28% of 2024’s market share. Their recent collaboration with PMD Technologies has strengthened their position in automotive-grade ToF solutions, particularly for driver monitoring systems.

Texas Instruments and STMicroelectronics follow closely, together holding 35% of the market. Their strength lies in integrating ToF sensors with existing automotive microcontroller ecosystems, giving OEMs streamlined implementation paths. STMicroelectronics’ FlightSense technology has seen particular success in European luxury vehicle brands.

While established players dominate, emerging specialists like PMD Technologies and Melexis are gaining traction through niche applications. PMD’s work on in-cabin gesture recognition has been adopted by several Chinese EV manufacturers, while Melexis recently launched a breakthrough indirect ToF sensor with 0.1mm precision for seat occupancy detection.

The competitive intensity is further evidenced by recent developments:

- Analog Devices acquired a ToF specialist startup in Q1 2024 to enhance its automotive sensor capabilities

- Omron partnered with a major Tier 1 supplier to develop combined LiDAR/ToF systems

- AMS (now part of Renesas) introduced industry’s first AEC-Q102 certified ToF sensor for exterior applications

Looking ahead, competition will likely center on three key battlegrounds: power efficiency (critical for electric vehicles), functional safety certification (ISO 26262 compliance), and multi-sensor fusion capabilities. Companies investing in these areas while maintaining cost competitiveness will emerge as long-term winners.

List of Key Automotive ToF 3D Image Sensor Companies

- Infineon Technologies (Germany)

- Texas Instruments (U.S.)

- Analog Devices (U.S.)

- STMicroelectronics (Switzerland)

- OMRON Corporation (Japan)

- Nuvoton Technology (Taiwan)

- Brookman Technology (Japan)

- AMS (Renesas) (Austria)

- Elmos Semiconductor (Germany)

- PMD Technologies (Germany)

- Melexis (Belgium)

- MESA Imaging (Switzerland)

- IFM Electronic (Germany)

- Espros Photonics (Switzerland)

- Silicon Integrated (U.S.)

- Evisionics (Israel)

Segment Analysis:

By Type

Direct ToF Segment Leads Due to Higher Accuracy in Distance Measurement for Autonomous Vehicles

The market is segmented based on type into:

- Direct ToF

- Subtypes: Single-photon avalanche diode (SPAD), Photonic mixer device (PMD), and others

- Indirect ToF

By Application

In-cabin Sensing Segment Dominates for Enhanced Driver Monitoring and Safety Features

The market is segmented based on application into:

- In-cabin sensing

- Subtypes: Driver monitoring, Occupancy detection, Gesture recognition, and others

- Short range exterior

- Other applications

By Vehicle Type

Passenger Vehicles Segment Leads Owing to Higher Adoption of ADAS Features

The market is segmented based on vehicle type into:

- Passenger vehicles

- Commercial vehicles

By Technology

ADAS Segment Dominates with Growing Demand for Safety Features in Vehicles

The market is segmented based on technology into:

- Advanced Driver Assistance Systems (ADAS)

- Autonomous driving systems

Regional Analysis: Automotive ToF 3D Image Sensor Market

Asia-Pacific

Asia-Pacific dominates the global Automotive Time-of-Flight (ToF) 3D Image Sensor market, holding over 56% of the global automotive production share as of 2022. China, the largest automobile producer (32% global share), alongside Japan, South Korea, and India, drives substantial demand for advanced driver monitoring systems (DMS) and ADAS technologies. Rapid urbanization, increasing consumer expectations for in-cabin safety features, and large-scale government investments in autonomous vehicle R&D accelerate adoption. For instance, China’s “China Standards 2035” plan prioritizes smart vehicle components, including 3D sensing solutions. However, cost sensitivity remains a challenge, pushing manufacturers to balance performance with affordability.

North America

The North American market, led by the U.S. (16% of global auto production), is a key innovator in autonomous vehicle technology, fueled by stringent safety regulations such as the NHTSA’s ADAS mandates and substantial private-sector R&D investments. ToF sensors are increasingly integrated for occupant monitoring and pedestrian detection, with projections indicating a 21.7% CAGR through 2032. Collaborations between automakers (e.g., Tesla, GM) and semiconductor firms (Texas Instruments, Analog Devices) reinforce regional growth. The infrastructure push, including the $1.2 trillion Bipartisan Infrastructure Law, further supports smart mobility solutions. Nevertheless, supply chain bottlenecks and high manufacturing costs pose short-term hurdles.

Europe

Europe, contributing 20% to global auto production, is a nexus for premium automotive ToF solutions, driven by EU safety standards like Euro NCAP’s 2025 roadmap for driver monitoring. Germany and France lead in deploying ToF-based gesture control and cabin occupancy detection, with OEMs (e.g., BMW, Mercedes-Benz) prioritizing passenger safety. Regulatory pressure to reduce road fatalities and a thriving EV ecosystem amplify demand. However, complex compliance requirements and slow adoption in budget vehicle segments temper growth. The region’s focus on Indirect ToF (lower power consumption) aligns with its sustainability goals, offering long-term scalability.

South America

South America’s market is emerging, with Brazil and Argentina gradually adopting ToF sensors for luxury and mid-tier vehicles. Economic volatility and reliance on imported automotive tech limit penetration, but local assembly plants (e.g., Volkswagen in Argentina) are beginning to integrate basic ADAS features. Government initiatives like Brazil’s Rota 2030 promote innovation, yet infrastructural gaps and low consumer awareness hinder large-scale deployment. Potential exists in fleet management and commercial vehicle safety systems, contingent on economic stabilization.

Middle East & Africa

The region shows nascent interest in ToF sensors, primarily in GCC countries (UAE, Saudi Arabia) through luxury vehicle imports and smart city projects. Dubai’s Autonomous Transportation Strategy underscores long-term potential, though current demand is constrained by fragmented regulations and low automotive production. Partnerships with global tech providers (e.g., Infineon, STMicroelectronics) aim to localize supply chains, but funding limitations and geopolitical risks delay advanced adoption. Over time, urbanization and tourism-driven transport upgrades may catalyze growth.

Report Scope

This market research report provides a comprehensive analysis of the Global Automotive Time-of-Flight (ToF) 3D Image Sensor market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The market was valued at USD 188 million in 2024 and is projected to reach USD 721 million by 2032, growing at a CAGR of 21.7%.

- Segmentation Analysis: Detailed breakdown by product type (Direct ToF, Indirect ToF), application (In-cabin Sensing, Short Range Exterior, Others), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa, including country-level analysis of major automotive markets.

- Competitive Landscape: Profiles of 16 leading market participants including Infineon Technologies, Texas Instruments, STMicroelectronics, and others, covering their product portfolios and strategic developments.

- Technology Trends & Innovation: Assessment of emerging ADAS applications, autonomous vehicle integration, and advancements in depth-sensing technologies.

- Market Drivers & Restraints: Evaluation of factors including automotive safety regulations, autonomous vehicle development, and supply chain challenges for semiconductors.

- Stakeholder Analysis: Strategic insights for sensor manufacturers, automotive OEMs, Tier 1 suppliers, and investors regarding market opportunities.

The research methodology combines primary interviews with industry experts and analysis of verified market data from automotive and semiconductor industry sources to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive ToF 3D Image Sensor Market?

-> Automotive ToF 3D Image Sensor Market was valued at 188 million in 2024 and is projected to reach US$ 721 million by 2032, at a CAGR of 21.7% during the forecast period.

Which key companies operate in this market?

-> Key players include Infineon Technologies, Texas Instruments, STMicroelectronics, Analog Devices, OMRON, and AMS, among others.

What are the key growth drivers?

-> Primary growth drivers include increasing ADAS adoption, autonomous vehicle development, and stringent automotive safety regulations.

Which region dominates the market?

-> Asia-Pacific leads the market with 56% of global automotive production, followed by Europe and North America.

What are the emerging applications?

-> Emerging applications include driver monitoring systems, gesture control interfaces, and advanced occupant detection for next-generation vehicles.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...