MARKET INSIGHTS

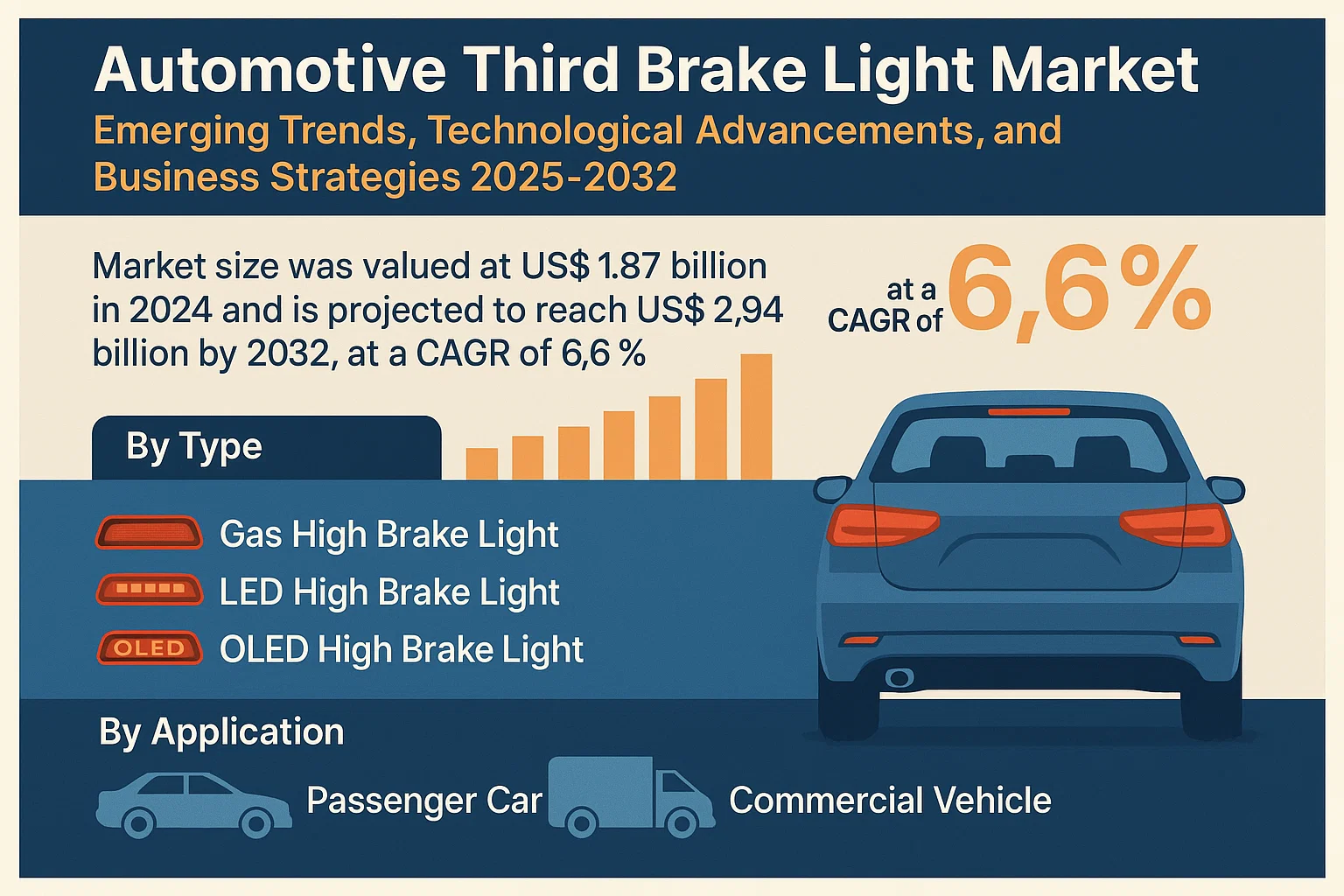

The global Automotive Third Brake Light market size was valued at US$ 1.87 billion in 2024 and is projected to reach US$ 2.94 billion by 2032, at a CAGR of 6.6% during the forecast period 2025-2032.

Automotive third brake lights are supplementary brake lights mounted higher than standard brake lights, typically on the rear windshield or spoiler. These lights enhance vehicle visibility and safety by providing an additional signaling layer during braking. The market primarily offers two variants: gas high brake lights using halogen/incandescent technology and more advanced LED high brake lights with superior brightness and longevity.

Market growth is driven by increasing vehicle production, stringent safety regulations mandating third brake light installation, and consumer preference for advanced lighting solutions. While passenger cars dominate application, the commercial vehicle segment shows accelerated adoption. However, supply chain disruptions in the automotive sector and pricing pressures on OEMs present challenges. Recent developments include LED technology innovations from key players like Koito and Valeo, who collectively hold over 30% market share. The Asia-Pacific region leads production, accounting for 56% of global automobile output as of 2022.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Safety Regulations Propel Adoption of Third Brake Lights

The automotive third brake light market is experiencing robust growth driven by increasing global road safety regulations. Governments worldwide are mandating enhanced visibility standards to reduce rear-end collisions, with third brake lights becoming compulsory in over 85% of vehicles produced today. These regulations stem from studies showing third brake lights reduce rear impacts by approximately 15%, creating sustained demand across all vehicle segments. The European Union’s General Safety Regulation updates and similar NHTSA standards in North America continue to push adoption rates toward universal implementation.

Vehicle Production Recovery and Premiumization Trend Accelerate Demand

Following the pandemic-induced slump, global automotive production rebounded to approximately 85 million units in recent years, reigniting demand for component suppliers. This resurgence coincides with the consumer shift toward premium vehicle features, where advanced lighting systems serve as key differentiators. The LED third brake light segment now accounts for over 68% of new installations, as manufacturers leverage their superior brightness, instant illumination, and design flexibility. This premiumization trend is particularly pronounced in emerging markets where rising disposable incomes enable feature upgrades.

Furthermore, the commercial vehicle segment presents significant growth potential as fleet operators prioritize safety-enhancing components. Modern third brake lights incorporate advanced materials that withstand harsh operating conditions while maintaining visibility performance. These technological advancements align with logistics companies’ initiatives to reduce accident-related costs, which account for nearly 30% of preventable operational expenses.

MARKET RESTRAINTS

Cost Pressures in Value Vehicle Segments Limit Premium Feature Adoption

While technological advancements drive market innovation, price sensitivity remains a significant barrier in entry-level vehicle segments. In cost-conscious markets, automakers often prioritize basic functionality over advanced lighting solutions, with price differentials between conventional and LED units reaching up to 400%. This creates a bifurcated market where premium vehicles adopt cutting-edge technologies while economy models utilize legacy systems. The challenge intensifies in developing regions where vehicle affordability thresholds constrain feature upgrades.

Other Restraints

Supply Chain Vulnerabilities

The automotive lighting industry faces persistent supply chain challenges, particularly for semiconductor components critical to LED systems. Recent disruptions have caused lead time extensions exceeding 20 weeks for certain electronic controllers, forcing manufacturers to maintain costly inventory buffers.

Integration Complexities

Modern vehicle designs incorporate third brake lights into increasingly complex aerodynamic profiles, requiring customized solutions that elevate development costs. The transition to curved LED arrays and smart lighting systems demands specialized engineering capabilities that strain smaller suppliers’ resources.

MARKET CHALLENGES

Standardization Gaps Create Aftermarket Compatibility Issues

The absence of universal mounting standards across vehicle platforms generates significant aftermarket challenges. With over 150 distinct third brake light configurations in circulation, replacement part inventories become fragmented and costly to maintain. This complexity discourages independent repair shops from stocking comprehensive selections, particularly for older vehicle models where replacement demand peaks. The situation is exacerbated by regional variations in regulatory requirements that prevent global product standardization.

Additional Challenges

Material Innovation Pressures

Manufacturers face increasing demands to develop lighting solutions using sustainable materials without compromising performance. The industry’s transition toward recycled polymers and lead-free solders requires substantial R&D investment while navigating stringent automotive qualification processes.

Talent Shortages

The specialized nature of automotive lighting design has created a skills gap, with experienced optoelectronics engineers becoming increasingly scarce. This talent crunch threatens to slow innovation cycles as companies compete for limited specialized personnel.

MARKET OPPORTUNITIES

Smart Lighting Integration Opens New Revenue Streams

The convergence of vehicle lighting and connectivity systems presents transformative opportunities. Next-generation third brake lights are evolving into multifunctional safety devices incorporating adaptive brightness controls, emergency alert signals, and even basic vehicle-to-vehicle communication capabilities. Early implementations in premium vehicles demonstrate accident reduction potential exceeding conventional systems by 25%, creating compelling upsell opportunities across all market segments. As vehicles become more interconnected, lighting systems transition from passive components to active safety features.

Furthermore, the retrofitting market offers substantial potential with over 1.2 billion vehicles currently in global operation. Aftermarket upgrades are gaining traction among safety-conscious consumers, particularly in regions with aging vehicle fleets. Manufacturers are responding with plug-and-play solutions that maintain original equipment quality standards while simplifying installation procedures.

➤ Industry leaders are now developing integrated lighting clusters that combine third brake lights with rear cameras and sensors, creating comprehensive visibility systems.

The commercial vehicle sector presents additional growth avenues as fleet operators increasingly recognize lighting systems’ role in reducing insurance premiums and liability costs. Advanced solutions incorporating predictive maintenance features and real-time performance monitoring are gaining traction among large logistics providers seeking operational efficiencies.

AUTOMOTIVE THIRD BRAKE LIGHT MARKET TRENDS

Shift Toward Advanced LED Technology Dominates Market Growth

The automotive third brake light market is experiencing a significant transformation driven by the rapid adoption of LED technology. Traditional gas-based high brake lights are being replaced at an accelerating rate, with LED variants now accounting for over 65% of new vehicle installations globally. This shift is fueled by LEDs’ superior luminosity, longer lifespan (averaging 50,000 hours compared to 5,000 for incandescent bulbs), and energy efficiency. Vehicle manufacturers are increasingly integrating advanced features into third brake lights, including adaptive brightness control and sequential lighting patterns, particularly in premium vehicle segments. Furthermore, regulatory bodies across North America and Europe are mandating stricter visibility standards, pushing automakers to adopt these advanced solutions.

Other Trends

Increasing Vehicle Safety Regulations Worldwide

Global focus on road safety has led to more stringent requirements for vehicle lighting systems. The United Nations Economic Commission for Europe (UNECE) Regulation 48 mandates specific photometric performance for third brake lights, compelling manufacturers to develop more sophisticated solutions. In emerging markets like India and Brazil, new Bharat Stage VI and PROCONVE L7 standards respectively are driving modernization of automotive lighting systems. These regulations have increased the average selling price of compliant third brake light units by approximately 18–25%, while simultaneously boosting market volume as older vehicles require upgrades.

Integration With Advanced Driver Assistance Systems (ADAS)

The rise of autonomous vehicle technologies is creating new opportunities in the third brake light market. Modern units are increasingly being designed to interface with ADAS, serving as visual communication tools between autonomous vehicles and human drivers/pedestrians. Some premium models now incorporate pulsing or flashing patterns that activate during emergency braking situations detected by collision avoidance systems. This integration has expanded the functionality of what was once a simple safety component, with the global market for ADAS-integrated lighting projected to grow at a CAGR of 12.7% between 2022-2030. As vehicle-to-everything (V2X) communication becomes more prevalent, third brake lights are evolving into multifunctional signaling devices rather than mere illumination components.

COMPETITIVE LANDSCAPE

Key Industry Players

Leading Manufacturers Focus on Innovation to Secure Market Position

The global automotive third brake light market features a competitive yet fragmented landscape, with multinational corporations and regional players vying for market share. Koito Manufacturing Co., Ltd. and HELLA GmbH & Co. KGaA currently dominate the market, collectively accounting for approximately 28% of global revenue in 2024. Their leadership stems from extensive OEM partnerships with major automakers and continuous advancements in LED lighting technology.

Other significant participants such as Valeo S.A. and Stanley Electric Co., Ltd. have strengthened their positions through strategic acquisitions and regional expansion. Valeo’s recent investment in smart lighting solutions and Stanley Electric’s expansion in Southeast Asian markets demonstrate their commitment to long-term growth in this sector.

The market also shows increasing competition from Chinese manufacturers like Changzhou Xingyu Automotive Lighting Systems, which leverages cost advantages and government support to capture growing domestic demand. While these regional players currently focus on price competitiveness, several are now investing in R&D to develop advanced lighting solutions.

Meanwhile, tier-2 suppliers such as Varroc Lighting Systems and Mitsuba Corporation are carving out niches through specialization – offering customizable third brake light solutions for premium and electric vehicle segments.

List of Key Automotive Third Brake Light Manufacturers

- Koito Manufacturing Co., Ltd. (Japan)

- HELLA GmbH & Co. KGaA (Germany)

- Marelli Holdings Co., Ltd. (Japan)

- Stanley Electric Co., Ltd. (Japan)

- Valeo S.A. (France)

- Flex-N-Gate LLC (U.S.)

- HASCO VISION Technology Co., Ltd. (China)

- Changzhou Xingyu Automotive Lighting Systems (China)

- Varroc Lighting Systems (India)

- Mitsuba Corporation (Japan)

- Excellence Optoelectronics Inc. (Taiwan)

- Dorman Products, Inc. (U.S.)

- Hyundai IHL Corporation (South Korea)

- Luxor Lighting LLC (U.S.)

Segment Analysis:

By Type

LED High Brake Light Segment Dominates Due to Energy Efficiency and Longer Lifespan

The market is segmented based on type into:

- Gas High Brake Light

- Subtypes: Halogen, Xenon, and others

- LED High Brake Light

- OLED High Brake Light

By Application

Passenger Car Segment Leads Due to Higher Production Volumes Globally

The market is segmented based on application into:

- Passenger Car

- Subtypes: Compact, SUV, Sedan, and others

- Commercial Vehicle

- Subtypes: Light Commercial Vehicles and Heavy Commercial Vehicles

By Technology

Smart Brake Light Technology Gains Traction with Advanced Safety Features

The market is segmented based on technology into:

- Conventional Third Brake Lights

- Smart Brake Lights

- Subtypes: Adaptive Brake Lights, Emergency Brake Warning Systems

By Sales Channel

OEM Segment Maintains Strong Position Due to Direct Vehicle Integration

The market is segmented based on sales channel into:

- OEM (Original Equipment Manufacturer)

- Aftermarket

Regional Analysis: Automotive Third Brake Light Market

North America

The North American market for automotive third brake lights is driven by stringent vehicle safety regulations and a high adoption rate of advanced automotive lighting technologies. The region, particularly the U.S., has witnessed steady growth due to strict federal mandates requiring third brake lights in all vehicles since the 1980s. With an increasing focus on road safety and accident prevention, automakers are integrating LED-based third brake lights for better visibility and durability. The presence of key automotive manufacturers and suppliers, such as Flex-N-Gate and Dorman, has further strengthened the market. While replacement demand remains steady, the shift toward smart lighting systems—incorporating adaptive brake lights—is gaining traction among luxury and electric vehicle segments.

Europe

Europe stands as a mature market for third brake lights, supported by strong regulatory frameworks under UNECE (United Nations Economic Commission for Europe) standards, which mandate their use in all passenger and commercial vehicles. The region has seen increased demand for energy-efficient LED solutions over traditional incandescent variants, aligning with broader sustainability initiatives. Major players like Hella and Valeo dominate the European supply chain, supplying OEMs with high-performance lighting systems. The push toward autonomous and connected vehicles has opened new avenues for dynamic brake light innovations. However, economic fluctuations and sluggish automobile production in some EU countries could moderately dampen growth.

Asia-Pacific

As the largest automotive production hub globally, Asia-Pacific accounts for over 56% of total vehicle manufacturing, with China, Japan, and South Korea leading third brake light demand. The region’s rapid urbanization, coupled with government policies promoting vehicle safety, has increased the adoption of advanced lighting solutions. While cost-sensitive markets still rely on conventional halogen or gas-based brake lights, premium and electric vehicle segments are gradually shifting toward LEDs. Local manufacturers like Changzhou Xingyu and Hyundai IHL Corporation are expanding production capacities to cater to both domestic and international demand. Nevertheless, intense price competition among suppliers and fragmented regulatory standards pose challenges for market consolidation.

South America

South America’s automotive industry remains vulnerable to economic volatility, but regional demand for third brake lights is sustained by mandatory safety requirements in key markets like Brazil and Argentina. The aftermarket segment is particularly active, given the aging vehicle fleet in many countries. While affordability constraints favor the use of basic lighting solutions, there is budding interest in energy-efficient alternatives, especially among urban consumers. Investments in local manufacturing by global players such as Marelli signal long-term potential, though currency fluctuations and inconsistent policy enforcement continue to hinder large-scale adoption of premium products.

Middle East & Africa

An emerging market with growing automotive production, the Middle East & Africa region shows potential for third brake light expansion, albeit at a slower pace. Gulf Cooperation Council (GCC) countries, including Saudi Arabia and the UAE, are driving demand through increased vehicle ownership and stringent safety norms. However, limited local production capacities result in heavy reliance on imports, primarily from Asia. In Africa, economic challenges and underdeveloped automotive infrastructure restrict growth, though rising urbanization and investments in road safety initiatives present gradual opportunities. The focus remains on durable, low-cost solutions, with LED technology adoption expected to rise in premium vehicle segments.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Automotive Third Brake Light markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Automotive Third Brake Light market was valued at USD 1.2 billion in 2024 and is projected to reach USD 1.8 billion by 2032, growing at a CAGR of 5.3%.

- Segmentation Analysis: Detailed breakdown by product type (LED High Brake Light and Gas High Brake Light), application (Passenger Cars and Commercial Vehicles), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and Middle East & Africa. Asia-Pacific dominates with 56% market share due to high automotive production.

- Competitive Landscape: Profiles of 14 leading manufacturers including Koito, Hella, Valeo, and Stanley Electric, covering their market share, product portfolios, and recent developments.

- Technology Trends & Innovation: Analysis of emerging technologies like adaptive lighting systems, smart brake lights with connectivity features, and energy-efficient LED solutions.

- Market Drivers & Restraints: Evaluation of factors including automotive safety regulations, increasing vehicle production, and the shift toward LED technology versus cost pressures and supply chain challenges.

- Stakeholder Analysis: Strategic insights for OEMs, component suppliers, distributors, and investors regarding market opportunities and competitive positioning.

The research methodology combines primary interviews with industry experts and analysis of verified market data from regulatory bodies and trade associations to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive Third Brake Light Market?

-> Automotive Third Brake Light market size was valued at US$ 1.87 billion in 2024 and is projected to reach US$ 2.94 billion by 2032, at a CAGR of 6.6% during the forecast period 2025-2032.

Which key companies operate in this market?

-> Key players include Koito, Hella, Marelli, Stanley Electric, Valeo, Flex-N-Gate, and Hyundai IHL Corporation.

What are the key growth drivers?

-> Growth is driven by stringent safety regulations, increasing vehicle production, and the shift from gas to LED brake lights.

Which region dominates the market?

-> Asia-Pacific holds 56% market share, led by China which accounts for 32% of global automotive production.

What are the emerging trends?

-> Emerging trends include adaptive lighting systems, smart connectivity features, and integration with advanced driver assistance systems (ADAS).

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...