MARKET INSIGHTS

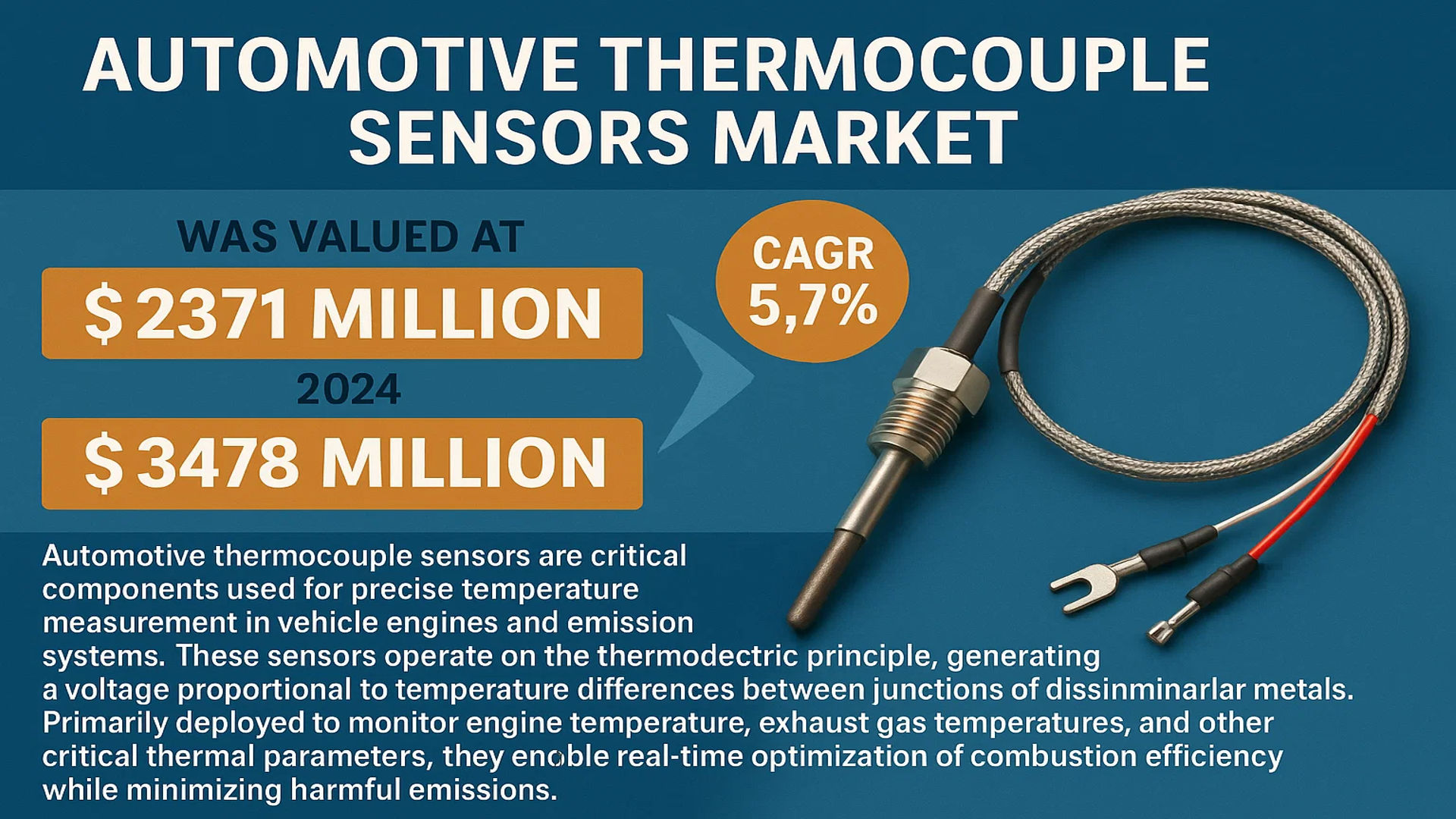

The global Automotive Thermocouple Sensors Market was valued at 2371 million in 2024 and is projected to reach US$ 3478 million by 2032, at a CAGR of 5.7% during the forecast period.

Automotive thermocouple sensors are critical components used for precise temperature measurement in vehicle engines and emission systems. These sensors operate on the thermoelectric principle, generating a voltage proportional to temperature differences between junctions of dissimilar metals. Primarily deployed to monitor engine temperature, exhaust gas temperatures, and other critical thermal parameters, they enable real-time optimization of combustion efficiency while minimizing harmful emissions.

Market expansion is driven by stringent emission regulations globally, particularly Euro 7 and China VI standards, which mandate advanced thermal monitoring solutions. The increasing adoption of electric vehicles presents new opportunities, as thermocouples play vital roles in battery thermal management systems. Leading manufacturers like Omega Engineering and TE Connectivity are investing in high-accuracy MEMS-based thermocouples, with the K-type segment expected to dominate due to its wide temperature range (-200°C to +1260°C) and cost-effectiveness for automotive applications.

MARKET DYNAMICS

MARKET DRIVERS

Stringent Emission Regulations to Accelerate Automotive Thermocouple Sensor Adoption

Global emissions regulations are becoming increasingly stringent, compelling automakers to integrate advanced temperature monitoring systems into vehicle designs. Thermocouple sensors play a critical role in optimizing engine performance and reducing harmful exhaust emissions by providing real-time temperature data for precise combustion control. Regulatory bodies worldwide are implementing stricter Euro 6 and EPA Tier 3 standards, with penalties for non-compliance reaching into billions annually. This regulatory pressure is directly driving demand for high-precision temperature sensing solutions across passenger and commercial vehicle segments.

Electrification Trend in Automotive to Create New Sensor Applications

The rapid electrification of vehicles is creating new applications for thermocouple sensors beyond traditional combustion engines. Battery temperature management systems in electric vehicles require multiple precision sensors to monitor cell temperatures within 0.5°C accuracy. With global EV production projected to exceed 40 million units annually by 2030, thermocouple sensors are becoming essential components in battery packs, charging systems, and power electronics cooling circuits. Leading manufacturers are developing specialized high-temperature variants capable of operating in the harsh environments of electric drivetrains.

Advancements in Sensor Materials Engineering to Improve Market Prospects

Recent innovations in thermoelectric materials are significantly enhancing sensor performance characteristics. New nickel-chromium and nicrosil-nisil alloy formulations now offer improved thermal stability with measurement ranges extending beyond 1300°C while reducing drift to less than 1% over extended operational periods. These material advancements are particularly valuable for high-performance automotive applications where sensor longevity and measurement consistency are critical. Manufacturers investing in these next-generation materials are gaining competitive advantage in both OEM and aftermarket segments.

➤ The development of MEMS-based miniature thermocouples has enabled integration into space-constrained vehicle systems while maintaining measurement accuracy, creating new design possibilities for engineers.

Furthermore, the growing integration of wireless connectivity in sensor systems allows for real-time temperature monitoring across vehicle platforms, supporting predictive maintenance strategies and reducing warranty costs for manufacturers.

MARKET CHALLENGES

High Development Costs for Automotive-Grade Sensors to Constrain Market Entry

The automotive sector demands sensors that meet rigorous quality and reliability standards while maintaining cost-effectiveness. Developing thermocouples that satisfy AEC-Q200 qualification requirements involves extensive testing and validation processes that can exceed $2 million per sensor variant. This high barrier to entry limits participation primarily to established players with substantial R&D budgets. Smaller manufacturers face challenges competing on both technical specifications and price points in this highly specialized market.

Other Challenges

Supply Chain Vulnerability

Reliance on specialized metal alloys from limited global sources creates vulnerability in the thermocouple supply chain. Political instability in key mining regions and trade restrictions can cause significant price volatility, with some platinum-group metals experiencing 30-40% annual price fluctuations. Manufacturers must maintain complex inventory strategies to mitigate these risks.

Integration Complexities

Modern vehicle architectures present increasing challenges for sensor integration. The transition to domain-based vehicle electronics requires thermocouples to interface with multiple control units while maintaining EMI/EMC compliance. These integration demands add validation complexity and can delay time-to-market for new sensor implementations.

MARKET RESTRAINTS

Thermal Measurement Accuracy Limitations to Hinder Market Penetration

While thermocouples offer broad temperature measurement capabilities, inherent accuracy limitations constrain their use in certain automotive applications. Standard K-type thermocouples typically provide ±2.2°C accuracy, which may be insufficient for emerging precision thermal management requirements. Alternative technologies like RTDs and thermistors, though more expensive, are gaining traction in applications where sub-degree accuracy is mandatory, particularly in battery electric vehicle systems.

Additionally, the non-linear output characteristics of thermocouples require complex signal conditioning that adds to system cost and complexity. These technical constraints are prompting some automakers to evaluate hybrid sensing solutions that combine multiple measurement technologies.

MARKET OPPORTUNITIES

Emerging Predictive Maintenance Applications to Drive Future Growth

The integration of thermocouple data with vehicle telematics systems is creating new opportunities in predictive maintenance. By combining real-time temperature data with machine learning algorithms, manufacturers can develop early warning systems for component failures before they occur. This capability is particularly valuable for commercial fleet operators, where unplanned downtime costs can exceed $1,000 per vehicle per day. Sensor manufacturers partnering with telematics providers are well-positioned to capitalize on this growing $3.5 billion predictive maintenance market.

Furthermore, the development of smart sensor networks within vehicles enables comprehensive thermal mapping that optimizes both performance and energy efficiency. These advanced applications are creating demand for thermocouples with integrated diagnostics and self-calibration capabilities.

The aftermarket segment also presents significant growth potential, particularly in emission-related repairs where thermocouples are critical components of OBD-II compliant systems. Expanding workshop networks and tightening inspection regulations are expected to drive sustained replacement demand across all vehicle classes.

AUTOMOTIVE THERMOCOUPLE SENSORS MARKET TRENDS

Rising Demand for Engine Efficiency and Emission Control to Drive Market Growth

The global automotive thermocouple sensors market is witnessing significant growth, primarily driven by increasing regulatory requirements for emission control and fuel efficiency in vehicles. With automotive manufacturers adopting stricter compliance measures, the demand for accurate temperature monitoring in engines and exhaust systems has surged, pushing thermocouple sensor adoption. K-Type thermocouples, known for their broad temperature range (-200°C to 1260°C) and durability, dominate the market, capturing over 45% of revenue share as of 2024. The engine monitoring segment alone accounts for more than 55% of the total market due to the critical need for real-time temperature control in combustion optimization.

Other Trends

Advancements in Sensor Miniaturization

Automotive thermocouple sensors are evolving with miniaturized designs, improving integration into compact engine compartments while maintaining high accuracy. Leading manufacturers are leveraging advanced materials, such as ceramic-based insulators and high-temperature alloys, to enhance sensor longevity under extreme conditions. Recent innovations in wireless thermocouples with IoT-enabled diagnostics are transforming predictive maintenance, providing real-time data to optimize engine performance and reduce downtime.

Expansion of Electric and Hybrid Vehicle Segment

While traditional combustion engines dominate demand, the electric vehicle (EV) sector is emerging as a key growth area for automotive thermocouples, particularly in battery thermal management systems (BTMS). With global EV sales projected to exceed 30 million units by 2030, thermocouples are increasingly deployed to monitor battery temperatures, ensuring safety and efficiency. China, the largest EV market, contributes significantly to this trend, as local manufacturers integrate high-precision thermocouples to comply with stringent battery regulations.

However, challenges such as the competition from resistance temperature detectors (RTDs) in mid-range temperature applications pose restraint. Yet, thermocouples maintain dominance in high-temperature zones above 600°C, where their cost-effectiveness and robustness outperform alternatives.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Innovation and Market Expansion Drive Competition in Automotive Thermocouple Sensors

The global Automotive Thermocouple Sensors market is characterized by a dynamic competitive environment, with established players and emerging manufacturers vying for market share. The market, valued at $2.37 billion in 2024, is projected to reach $3.48 billion by 2032, growing at a steady CAGR of 5.7%. This growth is fueled by increasing demand for energy-efficient vehicles and stringent emission regulations worldwide.

Omega Engineering and TE Connectivity dominate the market, leveraging their extensive product portfolios and strong distribution networks. Omega’s expertise in precision temperature measurement solutions gives it a competitive edge, particularly in high-performance automotive applications. TE Connectivity, with its diversified industrial presence, has been expanding its automotive sensor solutions through strategic acquisitions and technological partnerships.

The market also features specialized players like Emerson and WIKA, who are strengthening their positions through continuous R&D investments. Emerson’s recent development of compact, high-accuracy thermocouples for electric vehicle battery monitoring exemplifies the industry’s innovation trend. Meanwhile, WIKA has been focusing on ruggedized sensor solutions for extreme automotive environments, particularly in commercial vehicle applications.

While large multinationals lead in market share, regional players such as Holykell in Asia and Danfoss in Europe are making significant inroads by offering cost-competitive alternatives. The competitive intensity is further heightened by technological advancements in wireless sensor networks and IoT-enabled temperature monitoring solutions, prompting companies to accelerate their digital transformation initiatives.

List of Key Automotive Thermocouple Sensor Manufacturers

- Omega Engineering (U.S.)

- TE Connectivity (Switzerland)

- Emerson Electric Co. (U.S.)

- WIKA Alexander Wiegand SE & Co. KG (Germany)

- NXP Semiconductors (Netherlands)

- Danfoss Group (Denmark)

- Maxim Integrated (U.S.)

- Keyence Corporation (Japan)

- Holykell (China)

- Durex Industries (U.S.)

Segment Analysis:

By Type

K-Type Thermocouple Segment Leads Due to High Temperature Stability and Wide Application Range

The market is segmented based on type into:

- K-Type Thermocouple

- S-Type Thermocouple

- E-Type Thermocouple

- N-Type Thermocouple

- J-Type Thermocouple

By Application

Car Engine Segment Dominates Market Share Owing to Critical Temperature Monitoring Requirements

The market is segmented based on application into:

- Car Engine

- Car Exhaust System

By Vehicle Type

Passenger Vehicles Account for Majority Demand Due to Higher Production Volumes

The market is segmented based on vehicle type into:

- Passenger Vehicles

- Commercial Vehicles

Regional Analysis: Automotive Thermocouple Sensors Market

Asia-Pacific

The Asia-Pacific region leads the global automotive thermocouple sensors market, driven by rapid vehicle production and stringent emission regulations in countries like China, India, and Japan. China dominates with its thriving automotive manufacturing sector, accounting for over 30% of global vehicle production. The increasing adoption of electric vehicles, coupled with government mandates for efficient combustion monitoring, accelerates demand. While cost-effective K-type thermocouples remain prevalent, OEMs are gradually shifting to high-precision variants to meet advanced engine control requirements. Japan and South Korea contribute significantly through technological innovations in sensor accuracy and durability from key players like Keyence and NXP Semiconductors.

North America

Stringent EPA emissions standards and the shift toward hybrid/electric vehicles are reshaping the thermocouple sensor market in North America. The U.S. accounts for the majority of regional demand, with automotive manufacturers integrating these sensors into exhaust aftertreatment systems and battery thermal management. Recent CAFE (Corporate Average Fuel Economy) standards have prompted suppliers like Omega and TE Connectivity to develop compact, high-temperature-resistant variants. Canada shows growing adoption due to cold-climate performance requirements, while Mexico’s expanding auto parts industry supports market growth through localized production.

Europe

Europe’s market is characterized by rigorous Euro 7 emission norms and the rapid electrification of vehicles. Germany leads in technological advancements, with automotive suppliers focusing on dual-function sensors that monitor both exhaust gases and catalytic converter efficiency. The EU’s 2035 combustion engine ban has intensified R&D in EV-specific thermal sensors, particularly for battery packs. France and the UK are notable for aftermarket demand, while Eastern Europe emerges as a manufacturing hub for cost-competitive sensors. Wika and Danfoss Group play pivotal roles in supplying precision thermocouples to premium automakers.

South America

The region experiences moderate growth, with Brazil as the primary market due to its robust ethanol-fuel vehicle segment requiring specialized temperature monitoring. Economic volatility and irregular enforcement of emission standards hinder widespread adoption, though Argentina shows potential with increasing investments in automotive electronics. Most sensors imported are mid-range K-types, as price sensitivity limits premium product penetration. Local players like Jalc Trading are expanding distribution networks to serve regional OEMs and repair markets.

Middle East & Africa

This emerging market focuses predominantly on aftermarket replacements, with the UAE and Saudi Arabia as key importers of thermocouple sensors for luxury vehicles. Harsh desert conditions drive demand for heat-resistant variants, while limited local manufacturing capabilities create dependency on European and Asian suppliers. South Africa shows promise with its mature automotive ecosystem, though infrastructure challenges and low emission compliance slow market maturation. Long-term growth is expected as regional automakers align with global emission trends.

Report Scope

This market research report provides a comprehensive analysis of the global Automotive Thermocouple Sensors market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Automotive Thermocouple Sensors market was valued at USD 2,371 million in 2024 and is projected to reach USD 3,478 million by 2032, growing at a CAGR of 5.7%.

- Segmentation Analysis: Detailed breakdown by product type (K-Type, S-Type, E-Type, N-Type, J-Type Thermocouples) and application (Car Engine, Car Exhaust System) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. market size is estimated at USD million in 2024, while China is projected to reach USD million.

- Competitive Landscape: Profiles of leading market participants including Omega, TE Connectivity, Emerson, NXP Semiconductors, and Danfoss Group, covering their product portfolios, market share, and strategic developments.

- Technology Trends & Innovation: Assessment of emerging sensor technologies, integration with automotive control systems, and advancements in temperature measurement accuracy.

- Market Drivers & Restraints: Evaluation of factors such as stringent emission regulations, demand for fuel-efficient vehicles, and challenges in sensor durability under extreme conditions.

- Stakeholder Analysis: Insights for automotive OEMs, component suppliers, and investors regarding growth opportunities in electric vehicle applications and aftermarket segments.

The research methodology combines primary interviews with industry experts and analysis of verified market data to ensure accuracy and reliability of findings.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive Thermocouple Sensors Market?

-> Automotive Thermocouple Sensors Market was valued at 2371 million in 2024 and is projected to reach US$ 3478 million by 2032, at a CAGR of 5.7% during the forecast period.

Which key companies operate in Global Automotive Thermocouple Sensors Market?

-> Key players include Omega, TE Connectivity, Emerson, Maxim Integrated, NXP Semiconductors, Danfoss Group, and Wika.

What are the key growth drivers?

-> Growth is driven by stringent emission regulations, increasing vehicle electrification, and demand for precise engine temperature monitoring.

Which region dominates the market?

-> Asia-Pacific shows the fastest growth due to automotive production expansion, while North America leads in technological advancements.

What are the emerging trends?

-> Emerging trends include miniaturization of sensors, integration with IoT platforms, and development of high-temperature resistant materials.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...