MARKET INSIGHTS

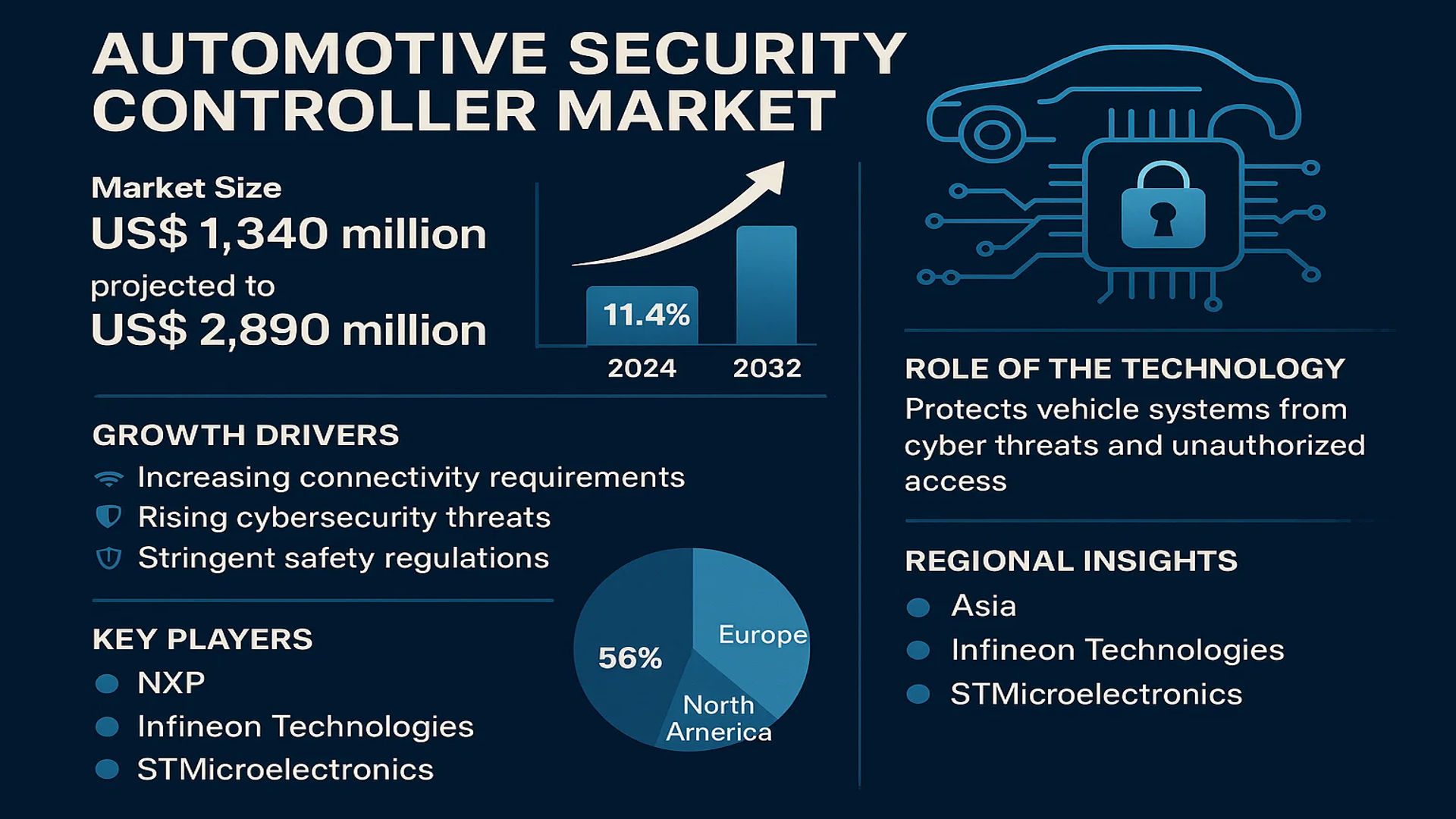

The global Automotive Security Controller Market size was valued at US$ 1,340 million in 2024 and is projected to reach US$ 2,890 million by 2032, at a CAGR of 11.4% during the forecast period 2025-2032

Automotive security controllers are specialized integrated circuits designed to protect vehicle systems from cyber threats and unauthorized access. These controllers enable secure communication between electronic control units (ECUs), manage cryptographic operations, and authenticate connected devices. The technology plays a critical role in modern vehicles, especially with the rise of connected cars and autonomous driving systems.

The market growth is driven by increasing vehicle connectivity requirements, rising cybersecurity threats in automotive systems, and stringent government regulations for vehicle safety. While Asia currently dominates vehicle production (accounting for 56% of global output), Europe and North America lead in security technology adoption. Major manufacturers like NXP, Infineon Technologies, and STMicroelectronics are actively developing advanced security solutions to address evolving threats in automotive networks.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Connected Vehicles and Advanced Security Solutions to Propel Market Growth

The automotive security controller market is experiencing significant growth due to the rapid adoption of connected vehicle technologies. With over 50 million connected cars on the road globally as of 2024, the need for robust security solutions has never been more critical. These controllers provide essential protection against cyber threats targeting vehicle ECUs, infotainment systems, and communication modules. Modern vehicles now contain over 150 electronic control units on average, creating multiple potential attack surfaces that security controllers help protect. As automakers accelerate their digital transformation strategies, the integration of advanced security chips is becoming standard practice across the industry.

Stringent Government Regulations Mandating Vehicle Cybersecurity to Drive Adoption

Governments worldwide are implementing stringent cybersecurity regulations for automobiles, creating strong market drivers for security controllers. Recent regulations including UN Regulation No. 155 for cybersecurity management systems mandate comprehensive protection measures across vehicle lifecycles. These regulations require automakers to implement state-of-the-art security technologies, including hardware-based security controllers, to protect against unauthorized access and data breaches. The European Union’s General Safety Regulation and similar frameworks in North America and Asia are compelling OEMs to integrate advanced security solutions earlier in the design process, significantly boosting market demand.

➤ The automotive cybersecurity market is projected to grow at a compound annual growth rate of over 20% through 2030, with security controllers representing one of the fastest-growing segments.

Increasing Deployment of Autonomous Driving Technologies Creating New Demand

The development of autonomous vehicles is creating substantial opportunities for automotive security controllers. As autonomous driving systems progress toward higher SAE levels, the security requirements become exponentially more complex. These controllers now must protect not just vehicle data but also critical driving functions from potential cyber attacks. With over 45% of new vehicles expected to feature at least Level 2 autonomy by 2027, the need for secure communication between sensors, control units and cloud platforms is driving innovation in security controller technology. The market is responding with solutions that offer higher processing power while maintaining automotive-grade reliability.

MARKET RESTRAINTS

High Development Costs and Long Automotive Certification Cycles Slowing Market Penetration

While demand is strong, the automotive security controller market faces significant challenges in development costs and certification timelines. Creating ASIL-D compliant security solutions that meet stringent automotive requirements often requires investments exceeding $10 million per product line. The certification process alone can take 18-24 months, creating barriers for smaller players and slowing time-to-market. These factors contribute to higher end-product costs that some automakers, particularly in price-sensitive emerging markets, may be reluctant to absorb despite the security benefits.

Legacy Vehicle Architectures Creating Integration Challenges

The automotive industry’s gradual transition from traditional ECU architectures to domain and zonal controllers presents ongoing integration challenges for security solutions. Many existing vehicle platforms were not designed with modern cybersecurity requirements in mind, forcing automakers to retrofit security solutions onto legacy systems. This can lead to suboptimal implementations and requires additional engineering resources. The industry shift toward software-defined vehicles promises to alleviate these challenges in future generations but creates temporary market friction during the transition period.

MARKET CHALLENGES

Evolving Cyber Threat Landscape Requiring Continuous Innovation

The automotive security controller market faces the constant challenge of staying ahead of sophisticated cyber threats. Attack methods are becoming more advanced, with demonstrated vulnerabilities in vehicle networks increasing by over 150% in the past five years. Security controllers must continually evolve to address new attack vectors targeting wireless interfaces, supply chain components, and even physical access points. This requires significant ongoing R&D investment from suppliers and creates version control challenges for automakers managing multi-year vehicle programs.

Other Challenges

Supply Chain Constraints

The semiconductor shortage crisis demonstrated vulnerabilities in the automotive supply chain that continue to impact security controller availability. These components often require specialized manufacturing processes and secure production facilities, limiting the number of qualified suppliers. The industry is working to diversify production capabilities, but capacity constraints remain a near-term challenge.

Skills Shortage

There is a significant shortage of engineers with expertise in both automotive systems and cybersecurity. Developing security controllers requires teams that understand hardware security, automotive safety standards, and real-time operating systems – a rare combination that makes talent acquisition and retention difficult.

MARKET OPPORTUNITIES

Emerging Vehicle-to-Everything (V2X) Communication Creating New Security Demands

The rollout of V2X technologies presents substantial growth opportunities for automotive security controllers. These systems require robust authentication and encryption to secure communications between vehicles, infrastructure, and other road users. With regulatory mandates for V2X adoption expected in multiple regions by 2025, security controller vendors are developing specialized solutions that meet the unique requirements of these safety-critical applications. The market potential is significant, with projections suggesting over 60% of new vehicles will incorporate V2X capabilities by the end of the decade.

Over-the-Air Update Capabilities Driving Demand for Secure Boot Solutions

As automakers implement over-the-air (OTA) update systems to maintain vehicle software throughout its lifecycle, the need for secure boot and update verification mechanisms is creating new opportunities. Security controllers with advanced cryptographic capabilities are essential to ensure the authenticity and integrity of software updates while preventing malicious actors from compromising vehicle systems. With the OTA update market expected to reach $10 billion by 2027, security controller providers are developing specialized solutions tailored to this high-growth application.

Growing Electric Vehicle Market Creating Specialized Security Requirements

The rapid growth of electric vehicles represents another significant opportunity, as these vehicles often incorporate more advanced electronics and connectivity features than traditional vehicles. Security controllers for EVs must protect not only the conventional vehicle systems but also charging infrastructure communications and battery management systems. With EV production expected to account for over 30% of global automotive output by 2030, security controller providers are developing solutions that address the unique needs of electrified powertrains while meeting stringent automotive safety standards.

AUTOMOTIVE SECURITY CONTROLLER MARKET TRENDS

Rising Vehicle Connectivity and Cybersecurity Demands Driving Market Growth

The increasing connectivity of modern vehicles has heightened concerns around cybersecurity, propelling demand for automotive security controllers globally. As connected car technologies proliferate—from telematics to autonomous driving systems—the risk of cyber threats has grown exponentially. By 2030, an estimated 95% of new vehicles will incorporate embedded connectivity features, requiring robust security solutions to protect against hacking and unauthorized access. Recent developments in hardware-based security modules (HSMs) and secure cryptographic processors are enabling automakers to implement end-to-end encryption and authentication mechanisms across vehicle networks.

Other Trends

Regulatory Pressures and Standardization

Governments and industry bodies are implementing stringent regulations mandating cybersecurity standards for vehicles, compelling manufacturers to adopt advanced security controllers. The UNECE WP.29 regulation, implemented across major automotive markets including the EU and Japan, requires cybersecurity management systems in all new vehicle types entering production. Similarly, ISO/SAE 21434 provides a framework for automotive cybersecurity risk assessment, driving OEMs to integrate security controllers that comply with these emerging standards while managing costs.

Technological Advancements in Embedded Security Solutions

Innovations in 32-bit microcontroller architectures and tamper-resistant hardware designs are revolutionizing automotive security controller capabilities. Leading semiconductor vendors now offer integrated security controllers combining high-performance processing with advanced encryption engines capable of supporting post-quantum cryptography algorithms. The shift toward vehicle-to-everything (V2X) communication has further accelerated demand for security controllers that can authenticate and secure data exchanges between vehicles and infrastructure, even in high-temperature automotive environments. Recent product launches feature hardened security ICs designed specifically for automotive applications, with operating temperature ranges exceeding 125°C.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive Security Controller Market Witnesses Strategic Battles Among Tech Giants

The global automotive security controller market features a dynamic competitive environment where semiconductor manufacturers and automotive electronics specialists are aggressively expanding their foothold. Infineon Technologies has emerged as a dominant player, commanding approximately 28% market share in 2024 through its comprehensive portfolio of 32-bit security controllers designed for vehicle authentication systems.

NXP Semiconductors and STMicroelectronics follow closely, collectively accounting for nearly 40% of the market revenue. Their competitive advantage stems from deep-rooted relationships with automotive OEMs and continuous innovation in secure V2X communication solutions. Both companies recently introduced next-generation eSIM-compatible security controllers, responding to the growing demand for connected car technologies.

The market also sees Renesas Electronics making significant strides through strategic partnerships with Japanese automakers. The company’s focus on ASIL-D certified security solutions has positioned it strongly in the autonomous vehicle segment. Meanwhile, Microchip Technology is gaining traction in the mid-range vehicle segment with cost-optimized 16-bit security controllers.

What makes this market particularly competitive is the accelerating pace of technological convergence. While traditional semiconductor companies lead in hardware capabilities, new entrants are challenging the status quo through software-defined security solutions. Established players are countering this by increasing R&D spending, with top companies allocating 15-20% of revenues to develop cybersecurity solutions for next-generation vehicles.

List of Key Automotive Security Controller Companies

- Infineon Technologies AG (Germany)

- NXP Semiconductors N.V. (Netherlands)

- STMicroelectronics N.V. (Switzerland)

- Renesas Electronics Corporation (Japan)

- Microchip Technology Inc. (U.S.)

- Omron Corporation (Japan)

- ABB Ltd. (Switzerland)

- Texas Instruments Incorporated (U.S.)

- Robert Bosch GmbH (Germany)

Segment Analysis:

By Type

32-bit Security Controller Segment Leads Due to Higher Processing Capabilities for Advanced Vehicle Systems

The market is segmented based on type into:

- 32-bit Security Controller

- Subtypes: Automotive-grade MCUs, Secure microprocessors

- 16-bit Security Controller

- Subtypes: Basic automotive control modules, Entry-level security processors

- Others

By Application

In-vehicle Emergency Call Segment Dominates With Mandatory Safety Regulations Worldwide

The market is segmented based on application into:

- In-vehicle Emergency Call (eCall)

- Autonomous Driving Systems

- Vehicle Access Control

- Telematics Systems

- Other Applications

By Vehicle Type

Passenger Vehicles Account for Largest Share Due to Higher Production Volumes

The market is segmented based on vehicle type into:

- Passenger Vehicles

- Subtypes: Sedans, SUVs, Hatchbacks

- Commercial Vehicles

- Subtypes: Light Commercial Vehicles, Heavy Commercial Vehicles

- Electric Vehicles

- Subtypes: Battery Electric Vehicles, Hybrid Electric Vehicles

By Security Feature

Authentication Modules Lead as Vehicle Cybersecurity Threats Increase

The market is segmented based on security features into:

- Authentication

- Secure Boot

- Secure Communication

- Intrusion Detection

- Data Encryption

Regional Analysis: Automotive Security Controller Market

Asia-Pacific

The Asia-Pacific region dominates the global Automotive Security Controller market, accounting for over 50% of global automotive production in 2024, primarily driven by China’s massive manufacturing output (32% global share). Rapid vehicle electrification, government mandates for connected car technologies, and growing concerns about cyber threats in intelligent transportation systems are accelerating demand. Japan leads in technological innovation with security controller exports, while India’s expanding automotive sector – projected to become the world’s third-largest market by 2030 – presents significant growth opportunities. The prevalence of 32-bit security controllers is increasing as regional OEMs prioritize advanced vehicle architectures.

Europe

Europe represents the second-largest market, underpinned by stringent automotive cybersecurity regulations (UNECE WP.29) and high adoption of connected vehicles. Germany remains the technology hub, with security controller development focused on autonomous driving applications. The region shows strong preference for integrated security solutions combining hardware and software protection layers. While market growth remains steady, inflationary pressures and supply chain reconfigurations post-Russia-Ukraine conflict have moderately impacted production volumes. The EU’s upcoming cybersecurity certification framework (EUCC) is expected to further shape market requirements.

North America

North America’s market is characterized by heightened focus on vehicle data protection, with the U.S. accounting for 85% of regional demand. Stringent NHTSA guidelines for vehicle-to-everything (V2X) communication security and high penetration of telematics systems drive sophisticated security controller adoption. The region shows particular strength in autonomous vehicle security solutions, with Silicon Valley tech firms collaborating with traditional automakers. Canada’s emerging EV sector presents new opportunities, though market growth faces temporary headwinds from economic uncertainties and shifting automotive investment patterns.

South America

The South American market remains in growth phase, with Brazil constituting approximately 60% of regional demand. While security controller adoption lags behind developed markets, increasing vehicle connectivity features in budget segments and growing awareness of cybersecurity risks are driving gradual market expansion. The lack of comprehensive regional cybersecurity standards and economic instability in key markets continue to restrain faster adoption. Local automakers are increasingly partnering with global security solution providers to address baseline protection needs for entry-level connected vehicles.

Middle East & Africa

This emerging market shows divergent growth patterns, with GCC countries leading in premium vehicle security solutions while African markets remain largely untapped. The UAE and Saudi Arabia are establishing as regional hubs for connected vehicle technologies, driven by smart city initiatives. However, the market faces challenges including limited local manufacturing capabilities, fragmentation of automotive standards across countries, and prioritization of basic vehicle features over advanced security in price-sensitive segments. Long-term growth potential exists as regional cybersecurity awareness improves and luxury vehicle penetration increases.

Report Scope

This market research report provides a comprehensive analysis of the Global and regional Automotive Security Controller markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global Automotive Security Controller market was valued at US$ 1,340 million in 2024 and is projected to reach US$ 2,890 million by 2032, growing at a CAGR of 11.4% during the forecast period.

- Segmentation Analysis: Detailed breakdown by product type (32-bit and 16-bit security controllers), application (in-vehicle emergency call, autonomous vehicles, others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis for major automotive markets including China, US, Germany, Japan, and South Korea.

- Competitive Landscape: Profiles of leading market participants including Omron, Infineon Technologies, ABB, Microchip Technology, NXP, STMicroelectronics, and Renesas, covering their product portfolios, market share, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging technologies in vehicle cybersecurity, including embedded SIM (eUICC) solutions, AI-driven threat detection, and hardware security modules for automotive applications.

- Market Drivers & Restraints: Evaluation of factors such as increasing vehicle connectivity mandates, rising cybersecurity threats, and automotive semiconductor shortages impacting market growth.

- Stakeholder Analysis: Strategic insights for automotive OEMs, tier-1 suppliers, semiconductor manufacturers, and cybersecurity solution providers regarding the evolving ecosystem and business opportunities.

The research methodology combines primary interviews with industry experts and secondary data from verified sources including trade associations, company filings, and government publications to ensure data accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive Security Controller Market?

->Automotive Security Controller Market size was valued at US$ 1,340 million in 2024 and is projected to reach US$ 2,890 million by 2032, at a CAGR of 11.4% during the forecast period 2025-2032

Which key companies operate in Global Automotive Security Controller Market?

-> Key players include Omron, Infineon Technologies, ABB, Microchip Technology, NXP, STMicroelectronics, and Renesas, among others.

What are the key growth drivers?

-> Key growth drivers include increasing vehicle connectivity mandates, rising cybersecurity threats in connected cars, and government regulations for vehicle data protection.

Which region dominates the market?

-> Asia-Pacific holds the largest market share (42% in 2024), driven by automotive production in China, Japan, and South Korea, while Europe leads in technological adoption.

What are the emerging trends?

-> Emerging trends include quantum-resistant cryptography for vehicles, hardware-based security modules, and integrated security solutions for autonomous driving systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...