MARKET INSIGHTS

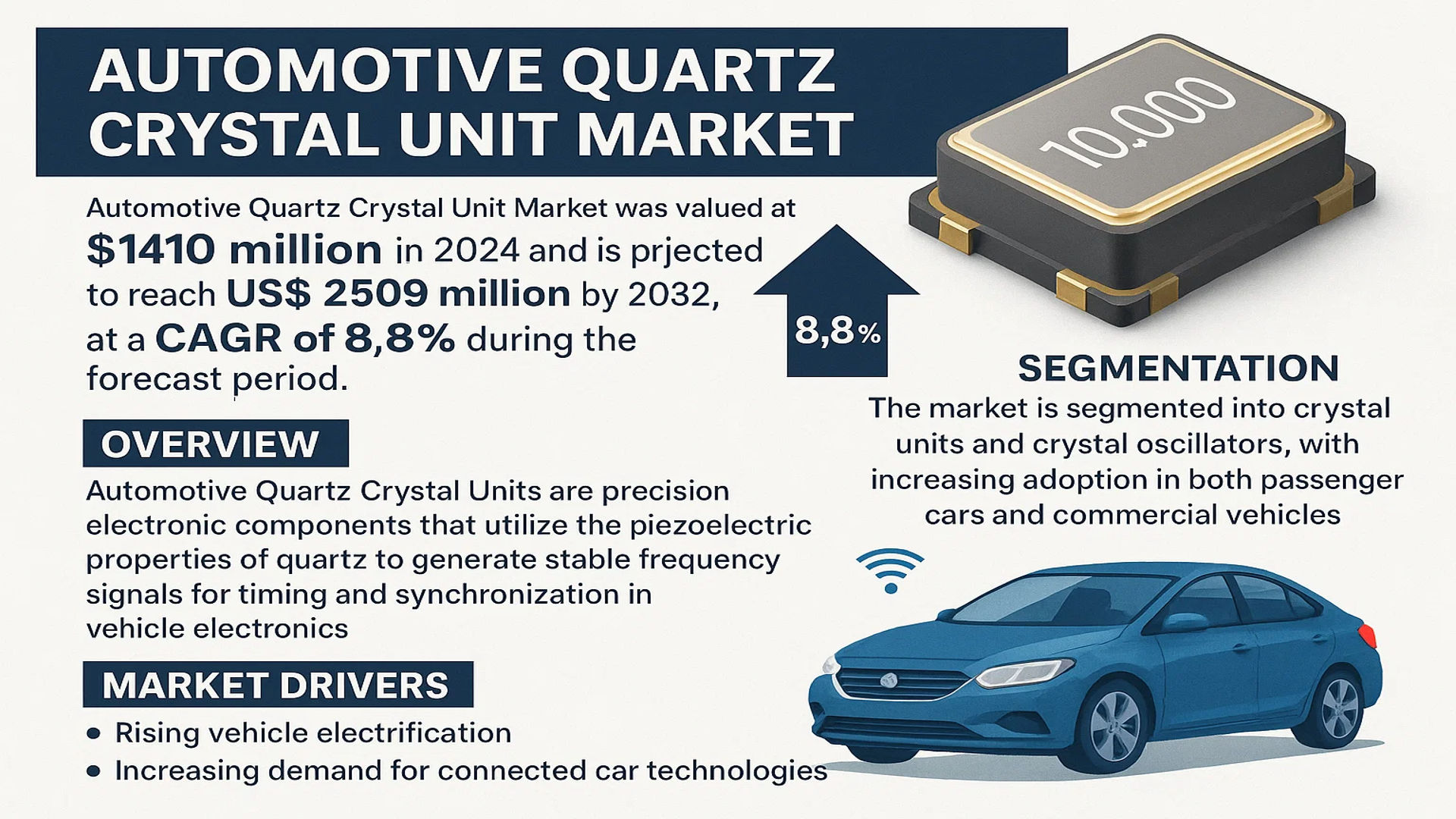

The global Automotive Quartz Crystal Unit Market was valued at 1410 million in 2024 and is projected to reach US$ 2509 million by 2032, at a CAGR of 8.8% during the forecast period.

Automotive Quartz Crystal Units are precision electronic components that utilize the piezoelectric properties of quartz to generate stable frequency signals for timing and synchronization in vehicle electronics. These components are critical for applications including engine control units, infotainment systems, advanced driver-assistance systems (ADAS), and telematics. The market is segmented into crystal units and crystal oscillators, with increasing adoption in both passenger cars and commercial vehicles.

Market growth is primarily driven by rising vehicle electrification and increasing demand for connected car technologies. The automotive industry’s shift toward electric and autonomous vehicles further amplifies the need for high-precision timing components. According to industry data, Asia dominates vehicle production, accounting for 56% of global output, with China alone contributing 32%. Key players like Seiko Epson, Murata Manufacturing, and TXC Corporation are expanding their product portfolios to meet evolving automotive requirements.

MARKET DYNAMICS

MARKET DRIVERS

Rising Automotive Electronics Integration to Propel Market Expansion

The global automotive industry is undergoing a significant transformation with the increasing integration of advanced electronic systems, driving substantial demand for quartz crystal units. Modern vehicles now incorporate over 100 electronic control units (ECUs) that require precise timing and frequency control components. Quartz crystal units serve as fundamental timing devices in various automotive applications including infotainment systems, advanced driver assistance systems (ADAS), engine control modules, and telematics. The automotive quartz crystal unit market is experiencing robust growth due to the rising production of electric vehicles, which typically contain 40-50% more electronic components compared to conventional internal combustion engine vehicles. This technological shift is creating sustained demand for high-reliability quartz components that can withstand harsh automotive environments while maintaining precise frequency stability.

Expansion of Connected Car Technologies to Accelerate Market Growth

The rapid adoption of connected car technologies represents a major growth driver for automotive quartz crystal units. With the global connected car market projected to exceed 125 billion dollars by 2025, the requirement for reliable timing components has never been greater. These quartz units are essential for vehicle-to-everything (V2X) communication systems, GPS modules, and cellular connectivity solutions that form the backbone of modern connected vehicles. The increasing implementation of 5G technology in automotive applications further amplifies this demand, as 5G networks require extremely precise timing synchronization. Automotive manufacturers are increasingly incorporating multiple quartz crystal units per vehicle to support various connectivity features, with premium vehicles containing up to 15-20 timing devices for different electronic systems.

Stringent Automotive Safety Standards to Drive Quality Component Demand

Increasingly rigorous automotive safety regulations worldwide are compelling manufacturers to adopt higher-quality electronic components, including quartz crystal units. Regulatory bodies across major automotive markets have implemented standards requiring fail-safe operation of electronic systems, particularly in safety-critical applications such as braking systems, airbag control, and stability control. Quartz crystal units must meet stringent AEC-Q200 reliability standards for automotive applications, ensuring they can operate reliably across temperature ranges from -40°C to +125°C while maintaining frequency stability within ±10 ppm. The growing emphasis on functional safety standards like ISO 26262 has further accelerated the adoption of certified quartz components that guarantee consistent performance throughout the vehicle’s lifespan.

MARKET CHALLENGES

Supply Chain Vulnerabilities and Component Shortages to Challenge Market Stability

The automotive quartz crystal unit market faces significant challenges from ongoing supply chain disruptions and component shortages. The global semiconductor crisis that began in 2020 has had ripple effects across the electronic components industry, including quartz crystal manufacturing. Production constraints have been exacerbated by limited availability of raw materials, particularly high-quality quartz crystals, which are predominantly sourced from specific geographical regions. The automotive industry’s just-in-time manufacturing approach has made it particularly vulnerable to these disruptions, leading to production delays and increased costs. Manufacturers are struggling to maintain adequate inventory levels while meeting the automotive industry’s rigorous quality standards and delivery schedules.

Other Challenges

Technical Complexity in Harsh Environment Operation

Developing quartz crystal units that can reliably operate in automotive environments presents substantial technical challenges. These components must maintain frequency stability despite exposure to extreme temperature variations, mechanical vibrations, electromagnetic interference, and humidity. The automotive operating temperature range is particularly demanding, requiring specialized materials and manufacturing processes that increase production complexity and cost. Additionally, the miniaturization trend in automotive electronics creates further challenges in maintaining performance while reducing component size.

Cost Pressure from Automotive OEMs

Automotive original equipment manufacturers exert significant price pressure on component suppliers, including quartz crystal unit manufacturers. The highly competitive nature of the automotive industry forces suppliers to continuously reduce costs while improving quality and reliability. This cost pressure is particularly challenging given the increasing technical requirements and the need for additional testing and certification to meet automotive standards. Suppliers must balance these competing demands while maintaining profitability.

MARKET RESTRAINTS

Competition from Alternative Timing Technologies to Limit Market Growth

The automotive quartz crystal unit market faces restraint from emerging alternative timing technologies that threaten traditional quartz dominance. Silicon-based timing solutions, including microelectromechanical systems (MEMS) oscillators, are gaining traction in certain automotive applications due to their smaller size, better shock resistance, and potential cost advantages at high volumes. While quartz still maintains superior frequency stability and phase noise characteristics, ongoing improvements in silicon timing technology are narrowing this performance gap. The adoption of these alternative technologies is particularly noticeable in non-critical automotive applications where extreme precision is less crucial, creating competitive pressure on quartz component manufacturers.

Consolidation in Automotive Supply Chain to Create Entry Barriers

The automotive industry’s ongoing consolidation and the formation of strategic partnerships between major OEMs and large component suppliers create significant barriers to entry for smaller quartz crystal unit manufacturers. Automotive companies increasingly prefer to work with established suppliers that can provide global support, extensive quality assurance capabilities, and large-scale production capacity. This trend makes it difficult for new entrants to penetrate the market and for smaller specialized manufacturers to compete effectively. The qualification process for automotive components is lengthy and expensive, often requiring 18-24 months of testing and validation, which further disadvantages smaller companies with limited resources.

Economic Volatility and Automotive Production Fluctuations to Impact Demand

Global economic uncertainties and fluctuations in automotive production directly impact demand for quartz crystal units. The automotive industry is highly cyclical and sensitive to economic conditions, consumer confidence, and regulatory changes. Production volumes can vary significantly based on these factors, creating demand volatility for component suppliers. The COVID-19 pandemic demonstrated how quickly automotive production can decline, with global vehicle production dropping by approximately 16% in 2020. Such fluctuations make capacity planning challenging for quartz crystal manufacturers and can lead to periods of both oversupply and shortages.

MARKET OPPORTUNITIES

Autonomous Vehicle Development to Create New Growth Frontiers

The development and gradual implementation of autonomous driving technologies present substantial opportunities for automotive quartz crystal unit manufacturers. Autonomous vehicles require an extensive array of sensors, processing units, and communication systems, all of which depend on precise timing components. Level 4 and Level 5 autonomous vehicles are expected to incorporate significantly more electronic systems than current vehicles, potentially doubling or tripling the number of quartz crystal units per vehicle. The redundancy requirements for safety-critical systems in autonomous vehicles will further increase component counts, creating additional demand for high-reliability timing solutions.

Electric Vehicle Revolution to Drive Component Innovation

The global shift toward electric vehicles offers significant growth opportunities for quartz crystal unit suppliers. Electric vehicles typically contain more electronic content than traditional vehicles, with advanced battery management systems, power electronics, and charging systems all requiring precise timing components. The electric vehicle market is growing rapidly, with projections indicating that electric vehicles could represent over 30% of new vehicle sales by 2030. This transition creates demand for specialized quartz crystal units that can operate in the unique electromagnetic environment of electric vehicles, where high-power electronics generate substantial electrical noise that can interfere with timing signals.

Advanced Driver Assistance Systems Expansion to Fuel Market Growth

The expanding adoption of advanced driver assistance systems (ADAS) creates substantial opportunities for quartz crystal unit manufacturers. Modern ADAS implementations rely on multiple sensors including radar, lidar, and cameras, all requiring precise synchronization and timing. The increasing sophistication of these systems, with features such as automatic emergency braking, adaptive cruise control, and lane-keeping assistance, drives demand for high-performance timing components. As regulatory requirements for vehicle safety become more stringent worldwide, the penetration of ADAS features into mid-range and economy vehicles will further expand the addressable market for automotive quartz crystal units.

AUTOMOTIVE QUARTZ CRYSTAL UNIT MARKET TRENDS

Vehicle Electrification and Advanced Driver-Assistance Systems (ADAS) Propel Market Growth

The global automotive industry is undergoing a significant transformation, driven by the rapid shift towards electrification and the integration of sophisticated electronic systems. This evolution is fundamentally increasing the demand for highly reliable timing components, with automotive quartz crystal units serving as the critical heartbeat for countless electronic control units (ECUs). The proliferation of Advanced Driver-Assistance Systems (ADAS), which require precise sensor synchronization and data processing, has become a primary catalyst. For instance, a modern premium vehicle can contain over 100 ECUs, each potentially requiring its own stable clock source, directly correlating to increased unit consumption per vehicle. Furthermore, the transition to electric vehicles (EVs), which are essentially computers on wheels, intensifies this demand. The battery management systems, powertrain controllers, and infotainment systems in EVs all depend on the unwavering frequency stability that quartz crystals provide, a necessity underscored by the projection that the market will grow from a value of $1410 million in 2024 to $2509 million by 2032. This trend is not merely about volume but also about performance, pushing manufacturers towards developing units with higher frequency stability, lower power consumption, and enhanced resilience to the harsh automotive environment.

Other Trends

Miniaturization and Enhanced Performance Specifications

A concurrent and powerful trend is the relentless drive towards the miniaturization of electronic components. As automotive designers strive to pack more functionality into limited space without compromising performance, the demand for smaller, surface-mount device (SMD) quartz crystal units is surging. This is particularly critical for applications like tire pressure monitoring systems (TPMS), smart keys, and compact camera modules used in surround-view systems. However, miniaturization brings its own set of engineering challenges, primarily concerning maintaining frequency stability and resistance to extreme temperature fluctuations, vibration, and shock. Manufacturers are responding with innovations in packaging and materials, leading to products that offer a smaller footprint while meeting the stringent Automotive Electronics Council (AEC-Q200) reliability standards. This focus on producing robust, miniature components is essential for supporting the next generation of compact and powerful automotive electronics.

Regional Production Shifts and Supply Chain Consolidation

The geographical landscape of automobile manufacturing profoundly influences the automotive quartz crystal unit market. With over 56% of global vehicle production concentrated in Asia, this region naturally represents the largest and most concentrated demand base. China, accounting for approximately 32% of worldwide production, is an epicenter of both automotive manufacturing and electronics component supply. This concentration drives a strategic imperative for quartz crystal unit suppliers to have a strong manufacturing and distribution footprint within Asia to ensure supply chain efficiency and responsiveness. Meanwhile, other major producing regions like Europe and North America, with 20% and 16% shares respectively, maintain demand for high-reliability components tailored for premium and luxury vehicle segments. This regional dynamic is fostering a trend towards supply chain consolidation and strategic partnerships, as crystal unit manufacturers align closely with Tier-1 suppliers and automakers to ensure just-in-time delivery and co-develop custom solutions for specific vehicle platforms, thereby mitigating potential logistical and geopolitical risks.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansion Define Market Leadership

The global Automotive Quartz Crystal Unit market exhibits a semi-consolidated competitive structure, characterized by the presence of established multinational corporations, specialized medium-sized enterprises, and emerging regional players. This dynamic is driven by the critical role these components play in automotive electronics, providing precise timing and frequency control for applications ranging from infotainment systems and advanced driver-assistance systems (ADAS) to engine control units and telematics. The market’s growth, projected to reach US$ 2509 million by 2032, intensifies competition, compelling companies to innovate and expand their global footprint.

Murata Manufacturing Co., Ltd. (Japan) is a dominant force in this landscape, leveraging its extensive expertise in ceramic-based electronic components and its formidable manufacturing scale. Its stronghold is particularly evident in the Asia-Pacific region, which accounts for over 56% of global automobile production, providing a massive and proximate customer base. The company’s continuous investment in miniaturization and high-reliability products tailored for harsh automotive environments solidifies its leading position.

Similarly, Seiko Epson Corp (Japan) and NDK (Japan) hold significant market shares, a status bolstered by Japan’s reputation as a global hub for high-quality electronic components and the world’s largest vehicle exporter. Their growth is intrinsically linked to their ability to supply Japanese automakers and Tier 1 suppliers with components that meet stringent automotive-grade qualifications for temperature stability and longevity.

Meanwhile, other key players are aggressively strengthening their positions through strategic initiatives. TXC Corporation (Taiwan) and Microchip Technology Inc. (U.S.) are making significant inroads through robust research and development focused on developing crystals and oscillators that support next-generation vehicle architectures, including electric and autonomous vehicles. Their strategy often involves forming strategic partnerships with automotive semiconductor manufacturers to offer integrated solutions. Companies like Rakon Limited (New Zealand) are also enhancing their market presence by focusing on high-precision timing solutions for automotive navigation and connectivity systems, ensuring they remain relevant as cars become increasingly connected.

List of Key Automotive Quartz Crystal Unit Companies Profiled

- Murata Manufacturing Co., Ltd. (Japan)

- Seiko Epson Corporation (Japan)

- Nihon Dempa Kogyo Co., Ltd. (NDK) (Japan)

- TXC Corporation (Taiwan)

- Microchip Technology Inc. (U.S.)

- KDS Daishinku Corp. (Japan)

- Kyocera Crystal Device Corporation (KCD) (Japan)

- Abracon LLC (U.S.)

- Rakon Limited (New Zealand)

- Micro Crystal AG (Switzerland)

- Hosonic Electronic Co., Ltd. (Taiwan)

- Siward Crystal Technology Co., Ltd. (Taiwan)

Segment Analysis:

By Type

Crystal Oscillators Lead the Market Due to High Demand in Vehicle Electronics Applications

The Automotive Quartz Crystal Unit market is segmented based on type into:

- Crystal Units

- Subtypes: AT-Cut, BT-Cut, and Others

- Crystal Oscillators

- Subtypes: SPXO, TCXO, VCXO, and Others

By Application

Passenger Car Segment Holds Major Share Due to Increasing Vehicle Production

The market is segmented based on application into:

- Commercial Vehicle

- Passenger Car

By Technology

Surface Mount Technology (SMT) Dominates Due to Compact Design Requirements

The market is segmented based on technology into:

- Surface Mount Technology (SMT)

- Through-Hole Technology (THT)

By Vehicle System

Infotainment Systems Drive Growth Due to Rising Consumer Demand for Connectivity

The market is segmented based on vehicle system into:

- Infotainment Systems

- Advanced Driver Assistance Systems (ADAS)

- Telematics Systems

- Engine Control Units

- Body Control Modules

Regional Analysis: Automotive Quartz Crystal Unit Market

Asia-Pacific

The Asia-Pacific region dominates the global Automotive Quartz Crystal Unit market, accounting for the largest market share due to its robust automotive manufacturing sector. Countries like China, Japan, and South Korea lead in both production and consumption, with China alone contributing approximately 32% of global vehicle manufacturing as of 2022. The increasing adoption of advanced driver-assistance systems (ADAS) and in-vehicle infotainment systems is driving demand for precision timing components, including quartz crystal units. Local manufacturers such as TXC Corporation, KDS, and Hosonic Electronic are key suppliers, benefiting from established supply chains and government incentives for electronics innovation. However, the region faces competition from low-cost alternatives, requiring continual advancements in miniaturization and temperature stability to maintain dominance.

Europe

Europe is a critical market for high-performance automotive quartz crystal units, driven by stringent vehicle safety and emissions regulations. The EU’s focus on electric vehicles (EVs) and autonomous driving technologies has elevated demand for reliable timing solutions. Germany, France, and the U.K. are major hubs, with manufacturers like Micro Crystal and Rakon Limited supplying premium-grade components. The region’s emphasis on quality and precision supports higher adoption of crystal oscillators over basic crystal units. Challenges include high production costs and competition from Asian suppliers, but European players differentiate through R&D investments in low-power and ultra-stable solutions for next-gen automotive applications.

North America

The North American market thrives on innovation, with the U.S. and Canada prioritizing connected and autonomous vehicles. Major automotive OEMs and Tier-1 suppliers collaborate with quartz crystal manufacturers like Microchip and Abracon to integrate components into ADAS and telematics systems. The U.S. Infrastructure Investment and Jobs Act indirectly benefits the market by promoting EV adoption. While the region’s production volume lags behind Asia, its focus on high-value applications ensures steady growth. Supply chain disruptions and reliance on imports from Asia remain key constraints.

South America

South America’s market is nascent but growing, with Brazil and Argentina showing potential due to expanding local automotive assembly. Economic volatility and limited domestic electronics manufacturing hinder large-scale adoption, but demand for aftermarket replacements and basic timing components persists. The region relies heavily on imports, creating opportunities for cost-effective suppliers like Siward Crystal Technology. Investments in regional production could unlock long-term growth.

Middle East & Africa

This region is emerging as a niche market, with demand driven by luxury vehicle imports and gradual automotive sector development. The UAE and Saudi Arabia are key markets, though reliance on imported electronic components limits local growth. Partnerships with global players like Murata Manufacturing aim to strengthen supply chains. While infrastructure challenges persist, rising urbanization and EV pilot projects signal future opportunities.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Automotive Quartz Crystal Unit markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive Quartz Crystal Unit Market?

-> Automotive Quartz Crystal Unit Market was valued at 1410 million in 2024 and is projected to reach US$ 2509 million by 2032, at a CAGR of 8.8% during the forecast period.

Which key companies operate in Global Automotive Quartz Crystal Unit Market?

-> Key players include Seiko Epson Corp, TXC Corporation, NDK, Murata Manufacturing, and Microchip, among others.

What are the key growth drivers?

-> Key growth drivers include rising automotive production, increasing electronic content per vehicle, demand for advanced driver assistance systems (ADAS), and the transition to electric vehicles.

Which region dominates the market?

-> Asia-Pacific is the dominant market, accounting for over 56% of global automotive production, while Europe and North America are significant markets for premium and electric vehicles.

What are the emerging trends?

-> Emerging trends include miniaturization of components, development of ultra-stable crystals for autonomous driving systems, and integration with IoT for vehicle connectivity.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...