MARKET INSIGHTS

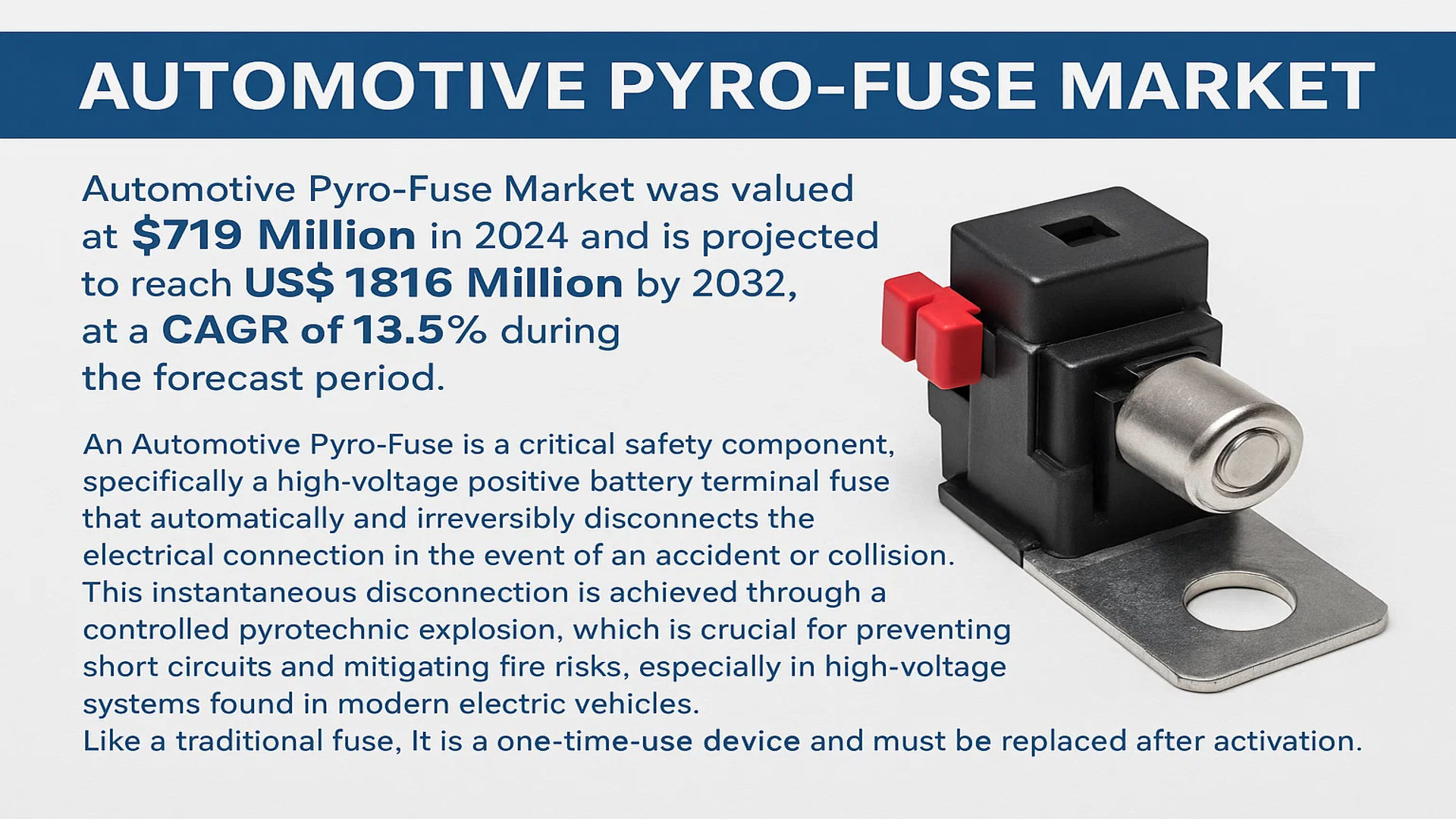

The global Automotive Pyro-Fuse Market was valued at 719 million in 2024 and is projected to reach US$ 1816 million by 2032, at a CAGR of 13.5% during the forecast period.

An Automotive Pyro-Fuse is a critical safety component, specifically a high-voltage positive battery terminal fuse that automatically and irreversibly disconnects the electrical connection in the event of an accident or collision. This instantaneous disconnection is achieved through a controlled pyrotechnic explosion, which is crucial for preventing short circuits and mitigating fire risks, especially in high-voltage systems found in modern electric vehicles. Like a traditional fuse, it is a one-time-use device and must be replaced after activation.

The market is experiencing robust growth, primarily driven by the rapid global expansion of the electric vehicle (EV) industry. With increasing regulatory pressure for enhanced vehicle safety and a rising consumer shift towards Battery Electric Vehicles (BEVs) and Hybrid Electric Vehicles (HEVs), the demand for these essential safety fuses is accelerating. The market structure is highly concentrated, with European, American, and Japanese brands holding a dominant 90% of the global market share. In 2024, the top three vendors—Autoliv, Daicel, and Pacific Engineering Corporation (PEC)—collectively accounted for approximately 65% of the total market revenue, underscoring the competitive landscape.

MARKET DYNAMICS

MARKET DRIVERS

Rapid Expansion of Electric Vehicle Production to Drive Market Growth

The global automotive pyro-fuse market is experiencing robust growth primarily due to the accelerating production and adoption of electric vehicles (EVs). With over 14 million EVs sold globally in 2023, representing a 35% increase from the previous year, the demand for advanced safety components like pyro-fuses has surged dramatically. These devices are critical safety components in high-voltage battery systems, providing instantaneous circuit interruption during collision events to prevent electrical fires and thermal runaway incidents. The transition toward electrification is further supported by stringent government regulations mandating enhanced safety features in vehicles operating with high-voltage systems exceeding 400 volts. Major automotive markets including the European Union, China, and North America have implemented comprehensive safety standards that specifically require reliable high-voltage disconnection systems, creating a substantial driver for pyro-fuse adoption across all vehicle segments.

Increasing Stringency of Vehicle Safety Regulations to Boost Market Expansion

Global automotive safety regulations are becoming increasingly rigorous, particularly concerning high-voltage systems in electric and hybrid vehicles. Regulatory bodies worldwide have established mandatory requirements for rapid electrical disconnection systems that can isolate high-voltage circuits within milliseconds of detecting a collision. These regulations stem from documented safety incidents involving high-voltage battery systems, where conventional fuses cannot provide the rapid response necessary to prevent catastrophic failures. The implementation of UN Regulation No. 94, 95 and 100 across numerous countries specifically addresses occupant protection in electric vehicles, mandating instant high-voltage disconnection during impacts. This regulatory landscape has compelled automotive manufacturers to integrate pyro-fuse technology as a standard safety feature, creating a sustained demand driver across all vehicle platforms utilizing high-voltage systems.

Furthermore, automotive safety assessment programs are increasingly weighting high-voltage safety systems in their evaluation criteria, creating additional market pressure for advanced pyro-fuse integration.

➤ For instance, recent updates to the New Car Assessment Program (NCAP) protocols in multiple regions now include specific evaluation criteria for high-voltage system safety performance during collision scenarios.

Additionally, the growing consumer awareness regarding EV safety features and the insurance industry’s focus on reducing high-voltage related claims are creating secondary demand drivers that support market growth throughout the forecast period.

MARKET CHALLENGES

High Development and Validation Costs to Challenge Market Penetration

The automotive pyro-fuse market faces significant challenges related to the substantial development and validation costs associated with these safety-critical components. Each pyro-fuse design requires extensive testing and validation to meet automotive safety standards, including rigorous environmental testing, vibration resistance validation, and crash performance verification. The development process typically involves investment exceeding $2 million per platform-specific design, creating substantial barriers for new market entrants and smaller manufacturers. Additionally, the certification process requires compliance with multiple international standards including ISO 26262 for functional safety, which mandates extensive documentation and validation procedures. These high upfront costs are particularly challenging for manufacturers targeting price-sensitive market segments or emerging economies where cost considerations often outweigh advanced safety feature integration.

Other Challenges

Supply Chain Complexity

The complex supply chain for explosive materials and precision electronic components creates significant operational challenges. Pyro-fuses require specialized explosive compounds that are subject to stringent transportation and storage regulations across different jurisdictions. The manufacturing process involves precision assembly of energetic materials with electronic control systems, requiring specialized facilities and highly trained personnel. Recent global supply chain disruptions have highlighted the vulnerability of these complex supply networks, with lead times for certain critical components extending beyond 12 months in some cases.

Technical Integration Barriers

Integrating pyro-fuse systems with existing vehicle architectures presents substantial technical challenges. The devices must interface with multiple vehicle systems including airbag control units, battery management systems, and crash sensors while maintaining reliability across extreme environmental conditions. The integration process requires sophisticated calibration to ensure proper deployment timing while avoiding false activations, creating additional development complexity and validation requirements that can delay product implementation timelines.

MARKET RESTRAINTS

Limited Standardization and Compatibility Issues to Deter Market Growth

The automotive pyro-fuse market faces significant restraints due to the lack of standardization across different vehicle platforms and manufacturers. Each automotive OEM typically develops proprietary specifications for pyro-fuse systems, creating compatibility issues and limiting component interoperability. This fragmentation requires manufacturers to develop multiple product variants to serve different customers, increasing development costs and manufacturing complexity. The absence of industry-wide standards for interface protocols, mounting configurations, and electrical specifications creates barriers to market entry and limits economies of scale. Furthermore, the rapid evolution of vehicle architectures and battery technologies means that pyro-fuse designs must constantly adapt to new requirements, creating additional development burdens and potentially limiting market growth in certain segments.

Additionally, the specialized nature of these components creates significant barriers for aftermarket replacement and service networks. The requirement for specialized training and equipment to handle and replace pyro-fuse systems limits the development of independent service networks, creating potential bottlenecks in vehicle repair and maintenance processes that could affect overall market adoption rates.

MARKET OPPORTUNITIES

Emerging Applications in Autonomous Vehicle Systems to Provide Growth Opportunities

The development of autonomous vehicle technologies presents significant growth opportunities for the pyro-fuse market. Advanced driver assistance systems (ADAS) and autonomous driving platforms require increasingly sophisticated safety systems that can respond to complex collision scenarios. The integration of pyro-fuse technology with predictive crash detection systems represents a substantial market opportunity, particularly as vehicles achieve higher levels of autonomy. Current development efforts focus on creating intelligent pyro-fuse systems that can preemptively disconnect high-voltage systems based on sensor data indicating an imminent collision, potentially reducing impact severity and enhancing occupant protection. The autonomous vehicle market is projected to experience substantial growth, with Level 3 and above autonomous systems expected to represent over 15% of new vehicle production by 2030, creating a substantial addressable market for advanced safety components including next-generation pyro-fuse systems.

Furthermore, the expansion of vehicle-to-grid (V2G) technologies and bidirectional charging capabilities creates additional application opportunities for pyro-fuse systems. These applications require robust safety systems that can handle complex electrical fault scenarios in both vehicle and infrastructure applications, potentially expanding the market beyond traditional automotive applications into broader mobility and energy infrastructure segments.

AUTOMOTIVE PYRO-FUSE MARKET TRENDS

Electrification of Vehicles Driving Exponential Growth in Pyro-Fuse Demand

The global shift toward vehicle electrification represents the most powerful catalyst for automotive pyro-fuse adoption. With electric vehicles requiring robust high-voltage circuit protection systems, pyro-fuses have become indispensable safety components in battery electric vehicles (BEVs) and hybrid electric vehicles (HEVs). These devices provide critical protection by instantly disconnecting high-voltage circuits during collisions, preventing potential thermal runaway events that could lead to catastrophic fires. The market is experiencing unprecedented growth because of stringent international safety standards mandating such protection systems. For instance, global BEV sales surpassed 10 million units in 2023, creating massive demand for high-voltage safety components. This trend is further accelerated by government mandates and consumer safety awareness, making pyro-fuses a standard rather than optional component in modern electric vehicle architectures.

Other Trends

Technological Advancements in Pyro-Fuse Design

Manufacturers are continuously innovating to enhance pyro-fuse performance characteristics, including faster response times, higher voltage ratings, and improved reliability. Recent developments have focused on reducing the device’s form factor while increasing its interrupting capacity, allowing for more compact and efficient vehicle designs. The integration of smart monitoring systems represents another significant advancement, enabling continuous health monitoring of the pyro-fuse and predictive maintenance capabilities. These technological improvements are crucial as vehicle voltages continue to increase, with many new BEV platforms now operating at 800V systems compared to the traditional 400V architectures. This voltage escalation necessitates pyro-fuses capable of handling higher energy levels while maintaining instantaneous response times of less than 1 millisecond during fault conditions.

Consolidation and Strategic Partnerships Reshaping Market Landscape

The automotive pyro-fuse market is experiencing significant consolidation as established players seek to strengthen their market positions through strategic acquisitions and partnerships. This trend is particularly evident among traditional automotive safety suppliers expanding their product portfolios to include electrification safety components. The market remains highly concentrated, with the top three manufacturers controlling approximately 65% of global revenue. This concentration drives intense competition and rapid innovation as companies strive to maintain technological leadership. Recent collaborations between pyro-fuse manufacturers and automotive OEMs have resulted in custom-designed solutions tailored to specific vehicle platforms, creating stronger integration between safety systems and vehicle architectures. Furthermore, manufacturers are establishing production facilities in key automotive regions to reduce supply chain risks and better serve local markets, particularly in China and Europe where EV adoption rates are highest.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Dominance by Established Players Intensifies Through Strategic Expansions

The global Automotive Pyro-Fuse market exhibits a semi-consolidated structure, characterized by the presence of a few dominant players holding significant market share alongside several medium and smaller specialized manufacturers. This landscape is heavily influenced by the critical safety nature of pyro-fuses, requiring stringent certifications and deep automotive industry expertise, which creates high barriers to entry. European, American, and Japanese companies collectively command over 90% of the global market revenue, a testament to their technological leadership, established supply chains, and strong relationships with global automakers and battery system integrators.

Autoliv, a global leader in automotive safety systems, holds a premier position in the pyro-fuse market. Its dominance is underpinned by its extensive product portfolio for vehicle safety and its deep integration into the supply chains of major OEMs worldwide. Similarly, Daicel Corporation, with its strong background in pyrotechnics and airbag inflators, leverages its expertise to produce highly reliable pyro-fuses, securing a substantial market share, particularly in the Asian and North American markets. Pacific Engineering Corporation (PEC) completes the top three, renowned for its innovative designs and focus on the high-voltage applications essential for battery electric vehicles (BEVs). Together, these three leaders accounted for approximately 65% of the global market revenue in 2024.

Beyond the top tier, other key players are aggressively pursuing growth. Littelfuse and Eaton are strengthening their market positions by leveraging their vast experience in circuit protection and power management. They are channeling significant investments into research and development to create next-generation pyro-fuses with faster response times and higher voltage ratings to meet the evolving demands of 800V vehicle architectures. Furthermore, these companies are actively engaging in strategic partnerships and geographical expansions to capture a larger portion of the rapidly growing electric vehicle market.

Meanwhile, companies like Mersen and Miba AG are focusing on technological differentiation and material science to enhance product performance and reliability. Their growth strategies include developing proprietary technologies and securing long-term supply agreements with battery manufacturers and automotive OEMs. Chinese players, such as Xi’an Sinofuse Electric and Hangzhou Chauron Technology, are also emerging as significant competitors, primarily catering to the vast domestic EV market and increasingly expanding their reach into other regions through competitive pricing and tailored solutions.

List of Key Automotive Pyro-Fuse Companies Profiled

- Autoliv (Sweden)

- Daicel Corporation (Japan)

- Pacific Engineering Corporation (PEC) (Japan)

- Littelfuse, Inc. (U.S.)

- Mersen (France)

- Eaton (Ireland)

- Miba AG (Austria)

- MTA Group (Italy)

- Xi’an Sinofuse Electric Co., Ltd. (China)

- Joyson Electronic (China)

- Hangzhou Chauron Technology Co., Ltd. (China)

Segment Analysis:

By Type

High Voltage Segment Dominates Due to Critical Safety Requirements in Electric Vehicles

The market is segmented based on voltage rating into:

- High Voltage (Above 700V)

- Mid Voltage (400V-700V)

- Low Voltage (Below 400V)

By Application

Battery Electric Vehicles (BEV) Segment Leads Due to Rapid Electrification and Stringent Safety Standards

The market is segmented based on application into:

- Battery Electric Vehicles (BEV)

- Hybrid Electric Vehicles (HEV)

By Vehicle Type

Passenger Cars Segment Holds Largest Share Owing to High Production Volumes and Consumer Adoption of EVs

The market is segmented based on vehicle type into:

- Passenger Cars

- Commercial Vehicles

By Sales Channel

OEM Segment Dominates as Pyro-Fuses are Integrated During Vehicle Manufacturing for Optimal Performance

The market is segmented based on sales channel into:

- Original Equipment Manufacturer (OEM)

- Aftermarket

Regional Analysis: Automotive Pyro-Fuse Market

Asia-Pacific

The Asia-Pacific region is the undisputed leader in the global Automotive Pyro-Fuse market, driven by its position as the epicenter of electric vehicle manufacturing. China, in particular, dominates both production and consumption, accounting for over 60% of global EV sales in 2024. This massive scale of new energy vehicle (NEV) adoption, fueled by aggressive government subsidies and stringent safety mandates, creates unparalleled demand for pyro-fuses. Local manufacturers, such as Xi’an Sinofuse Electric and Hangzhou Chauron Technology, are expanding rapidly to serve domestic OEMs like BYD and NIO, while also competing for export opportunities. However, the market is characterized by intense price competition and a mix of high-voltage applications for premium models and cost-optimized solutions for mass-market vehicles. Japan and South Korea remain critical hubs for technological innovation and high-quality manufacturing, with key global players like Daicel and Pacific Engineering Corporation (PEC) maintaining significant production facilities and R&D centers in the region to supply both local and international automakers.

Europe

Europe represents a high-value, innovation-driven market for Automotive Pyro-Fuses, underpinned by the region’s ambitious transition to electric mobility and its rigorous automotive safety standards. Regulations such as the EU’s General Safety Regulation (GSR) and Euro NCAP protocols mandate advanced safety systems, which inherently require reliable pyro-fuse integration to protect high-voltage battery systems. The presence of premium automakers like Volkswagen, BMW, and Mercedes-Benz accelerates the adoption of high-performance, high-voltage (above 700V) pyro-fuses, particularly for their luxury EV platforms. Furthermore, the region’s strong industrial base supports leading suppliers like Autoliv, Miba AG, and MTA Group, who have established robust manufacturing and engineering capabilities within the EU. While growth is steady, the market is highly competitive and requires compliance with complex certification processes, making it a region where technological superiority and reliability are paramount over cost considerations.

North America

The North American market is experiencing robust growth, primarily driven by the rapid electrification strategies of U.S. automakers and supportive federal policies, including the Inflation Reduction Act. This legislation provides significant incentives for domestic EV production and supply chain localization, encouraging investments in safety-critical components like pyro-fuses. The United States is the largest market in the region, with Tesla being a major consumer, necessitating high-volume, reliable pyro-fuse solutions for its extensive vehicle lineup. Key global suppliers, including Littelfuse and Eaton, have a strong foothold here, leveraging their established industrial electrical component expertise to serve the automotive sector. Safety standards from organizations like SA International influence product specifications, focusing on instantaneous disconnection capabilities to prevent thermal runaway events. While the market is advanced, it remains reliant on imports for a portion of its supply, presenting opportunities for further regional manufacturing expansion.

South America

The Automotive Pyro-Fuse market in South America is nascent but holds potential for future growth as the region gradually embraces electric mobility. Brazil and Argentina are the most active markets, though EV adoption rates are currently low compared to global leaders. The primary demand stems from hybrid electric vehicles (HEVs) rather than full battery electric vehicles (BEVs), influencing a focus on mid-voltage (400V-700V) pyro-fuse applications. Economic volatility and inconsistent government support for electrification are significant barriers, causing automakers to be cautious with investments in new safety technologies. Consequently, the market is largely served by imports from international suppliers, and price sensitivity is a major factor in purchasing decisions. However, as regional trade agreements evolve and environmental awareness increases, a slow but steady shift towards greater adoption of pyro-fuses is anticipated over the long term.

Middle East & Africa

The Middle East & Africa region is an emerging market for Automotive Pyro-Fuses, with development currently concentrated in a few key nations. Countries like Israel, Turkey, and the UAE are showing the earliest signs of EV infrastructure development and adoption, driven by urban sustainability initiatives. The demand for pyro-fuses is therefore in its very early stages and is almost entirely dependent on imported vehicles and components, as local manufacturing is virtually non-existent. The high cost of EVs and a lack of comprehensive charging networks are the main restraints. However, the region’s long-term potential is tied to economic diversification plans in Gulf Cooperation Council (GCC) countries, which could eventually include local EV assembly plants. For now, the market is characterized by small volumes and a focus on low-voltage applications for initial pilot projects and luxury vehicle imports.

Report Scope

This market research report provides a comprehensive analysis of the global Automotive Pyro-Fuse market, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by voltage type (High, Mid, Low) and application (BEV, HEV) to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging safety technologies, integration with advanced battery management systems, and evolving automotive safety standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, automotive OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive Pyro-Fuse Market?

-> Automotive Pyro-Fuse Market was valued at 719 million in 2024 and is projected to reach US$ 1816 million by 2032, at a CAGR of 13.5% during the forecast period.

Which key companies operate in Global Automotive Pyro-Fuse Market?

-> Key players include Autoliv, Daicel, Pacific Engineering Corporation (PEC), Littelfuse, Mersen, Eaton, Miba AG, MTA Group, and Xi’an Sinofuse Electric, among others.

What are the key growth drivers?

-> Key growth drivers include rapid expansion of electric vehicle production, stringent automotive safety regulations, and increasing demand for high-voltage battery protection systems.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by China’s leadership in electric vehicle manufacturing, while Europe maintains significant market share due to strong automotive safety standards.

What are the emerging trends?

-> Emerging trends include integration with advanced battery management systems, development of multi-voltage platform solutions, and increased adoption in commercial electric vehicles.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...