MARKET INSIGHTS

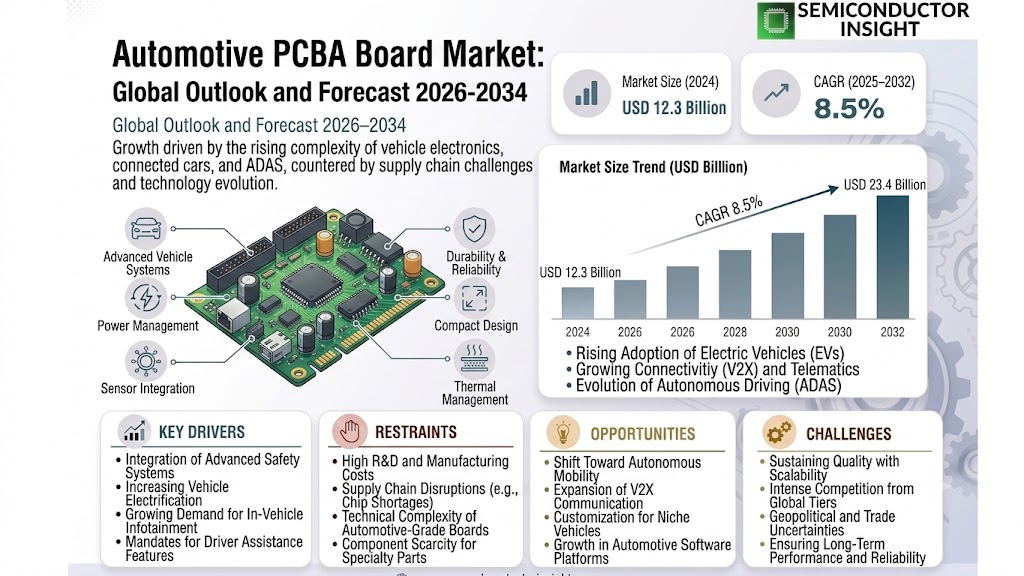

The global Automotive PCBA Board Market size was valued at US$ 12.3 billion in 2024 and is projected to reach US$ 23.4 billion by 2032, at a CAGR of 8.5% during the forecast period 2025-2032.

Automotive PCBA (Printed Circuit Board Assembly) boards are integrated electronic circuits used in vehicles to mechanically support and electrically connect components. These multilayer boards contain conductive copper pathways laminated onto non-conductive substrates, enabling complex automotive electronics including engine control units, infotainment systems, and advanced driver assistance systems (ADAS).

The market growth is driven by increasing vehicle electrification and autonomous driving technologies, with the average car now containing over 1,400 PCBA boards. While Asia dominates production with 56% market share, Europe and North America remain innovation hubs for high-reliability automotive electronics. Key challenges include material cost fluctuations and stringent automotive quality standards like IATF 16949 certification requirements.

MARKET DYNAMICS

MARKET DRIVERS

Rising Vehicle Electrification to Accelerate Automotive PCBA Demand

The automotive industry is witnessing unprecedented growth in vehicle electrification, directly driving demand for sophisticated PCBA boards. Electric vehicles (EVs) contain approximately 50% more electronic components compared to conventional internal combustion engine vehicles, translating to greater PCBA integration. The global EV market surpassed 10 million units sold in 2022, representing a 55% year-over-year increase. This surge creates substantial opportunities for multilayer PCBA boards which are essential for battery management systems, powertrain controls, and onboard charging units. High-density interconnect PCBA boards capable of handling complex automotive electronics are becoming increasingly vital as automakers compete to deliver advanced EV features.

Advanced Driver Assistance Systems (ADAS) Deployment to Fuel Market Expansion

Automotive PCBA boards are experiencing heightened demand due to the rapid adoption of ADAS technologies across all vehicle segments. Modern ADAS packages utilize 20-30 separate PCBA boards for functions including collision avoidance, adaptive cruise control, and lane keeping assistance. Current industry projections indicate that by 2025, approximately 40% of all new vehicles will feature Level 2 autonomy functionality requiring complex PCBAs. These safety-critical applications demand boards with exceptional reliability, vibration resistance, and temperature stability – specifications that are driving innovation in automotive-grade PCBA manufacturing processes and materials.

The push towards autonomous vehicles presents further growth potential, with prototype autonomous vehicles utilizing upwards of 100 interconnected PCBA boards. Automotive manufacturers are forming strategic partnerships with PCBA suppliers to ensure component reliability meets stringent automotive safety standards while managing costs.

MARKET RESTRAINTS

Global Semiconductor Shortages to Constrain Automotive PCBA Production

The automotive PCBA market continues to face significant production challenges due to persistent semiconductor supply chain disruptions. These shortages have resulted in production delays across major automakers, with some manufacturers reporting output reductions exceeding 40% during peak shortage periods. The average lead time for automotive-grade semiconductors extended to 26 weeks in 2023 compared to historical norms of 12-14 weeks. This imbalance creates production bottlenecks for PCBA manufacturers who must navigate volatile semiconductor allocations while maintaining just-in-time delivery commitments to automakers.

Stringent Automotive Certification Requirements to Limit Supplier Participation

The automotive industry’s rigorous quality and reliability standards present substantial barriers to new PCBA market entrants. Achieving IATF 16949 certification demands substantial capital investment in testing equipment, process controls, and quality management systems – costs that can exceed $3 million for a mid-sized PCBA facility. Additionally, automotive PCBAs must meet AEC-Q200 qualification standards for passive components and undergo extensive environmental stress testing. These compliance burdens restrict the supplier base primarily to established electronics manufacturers with specialized automotive divisions, potentially limiting capacity expansion during periods of peak demand.

Ongoing geopolitical tensions further complicate the certification landscape as manufacturers must navigate divergent regional standards while maintaining global supply chain flexibility.

MARKET CHALLENGES

Miniaturization Requirements to Test PCBA Manufacturing Capabilities

Vehicle design trends toward smaller, more integrated electronic packages are forcing PCBA manufacturers to overcome significant technical challenges. Automotive PCBAs must now accommodate component placements with tolerances below 0.1mm while maintaining reliability under harsh operating conditions. Advanced packaging techniques including chip-on-board and embedded component technologies require substantial process refinements. The transition to high-density interconnect PCBA designs has increased manufacturing defect rates industry-wide, with some manufacturers reporting initial yield rates below 65% for complex automotive boards.

Thermal Management Complexities to Impact Design Methodologies

Modern automotive PCBAs must dissipate 30-40% more thermal energy than previous generations due to increasing power requirements and tighter packaging constraints. These thermal challenges are particularly acute for EV powertrain applications where PCBA temperatures can exceed 125°C during operation. Traditional FR-4 board materials are being supplemented with specialized thermal management solutions including insulated metal substrates and ceramic-filled laminates. However, these advanced materials often increase production costs by 15-25% while introducing new manufacturing process compatibility issues that must be resolved at the design stage.

MARKET OPPORTUNITIES

Regional EV Supply Chain Development to Create Strategic Growth Avenues

Government policies promoting regional EV supply chain development present significant opportunities for automotive PCBA manufacturers. Major automotive markets are implementing local content requirements that incentivize domestic PCBA production. In North America, the Inflation Reduction Act’s battery sourcing requirements are accelerating investments in localized PCBA production capacity. Southeast Asia has emerged as a strategic manufacturing hub with automotive PCBA exports growing at 18% annually. These regionalization trends enable PCBA manufacturers to establish specialized production facilities catering to local automotive ecosystems while benefiting from government incentives.

Vehicle-to-Everything (V2X) Integration to Drive Next-Generation PCBA Demand

The emerging V2X communication ecosystem represents a substantial opportunity for specialized automotive PCBAs. These applications require high-frequency boards capable of stable performance in the 5.9GHz DSRC band while maintaining automotive reliability standards. Early V2X deployments indicate that dedicated communication modules require multilayer PCBA designs with strict impedance control and advanced EMI shielding. With major automotive markets mandating V2X implementation timelines, PCBA manufacturers developing specialized high-frequency expertise are positioned to capture this rapidly emerging market segment worth an estimated $1.2 billion in potential revenue by 2028.

AUTOMOTIVE PCBA BOARD MARKET TRENDS

Electrification of Vehicles Driving High-Density PCBA Innovations

The rapid shift toward vehicle electrification has become a key growth catalyst for the automotive PCBA board industry. As electric vehicle production expands globally—with over 10 million units sold in 2022—the demand for high-performance printed circuit board assemblies has surged exponentially. These boards require advanced capabilities such as high-power handling, thermal management, and miniaturization to support complex EV architectures. Recent advancements in multi-layer PCBA designs now enable better integration of power electronics, battery management systems, and onboard charging modules. Furthermore, the adoption of HDI (High-Density Interconnect) technology allows for 20-30% more compact designs without compromising electrical performance, meeting automakers’ need for space optimization in next-generation vehicles.

Other Trends

Autonomous Driving Technologies

The development of autonomous vehicle systems is creating unprecedented demand for high-reliability PCBA solutions. Modern ADAS (Advanced Driver Assistance Systems) require boards with exceptional signal integrity and EMI shielding to process data from multiple sensors simultaneously. Industry estimates suggest that Level 2+ autonomy vehicles contain approximately 50-70% more PCBA content than conventional vehicles, primarily for radar, LiDAR, and camera processing units. This trend has accelerated the development of automotive-grade rigid-flex PCBs that can withstand vibrations while maintaining electrical connections in complex mounting arrangements throughout the vehicle.

Regional Production Shifts and Supply Chain Optimization

Geopolitical factors and pandemic-induced supply chain disruptions have prompted a strategic reevaluation of PCBA manufacturing locations. While Asia currently dominates production—accounting for 68% of global automotive PCB output—many automakers are now pursuing localization strategies through near-shoring and vertical integration. This has led to increased capital expenditures in manufacturing facilities across North America and Europe, with several Tier 1 suppliers establishing dedicated automotive PCBA plants co-located with OEM assembly lines. Simultaneously, the industry is adopting Industry 4.0 practices, leveraging AI-driven quality inspection systems that have reduced PCBA defect rates by up to 40% in advanced production facilities.

COMPETITIVE LANDSCAPE

Key Industry Players

Market Leaders Expand Production Capacity as Demand for Automotive PCBA Boards Soars

The global Automotive PCBA Board market features a dynamic competitive environment with dominant Asian manufacturers holding significant market share. Victory Giant Technology and Shenzhen Kinwong emerged as clear leaders in 2024, collectively accounting for over 25% of the global market revenue. Their leadership stems from vertically integrated manufacturing capabilities and strong relationships with Chinese automakers.

Meanwhile, Avary Holding has been aggressively expanding into European automotive supply chains through its acquisition of Zollner Elektronik’s PCB division in 2023. This strategic move positions the company to capitalize on the growing electric vehicle PCB demand, particularly in Germany’s automotive hub.

The market remains highly fragmented with regional specialists like Shantou Goworld dominating commercial vehicle applications, while WUS Printed Circuit maintains technological leadership in high-reliability multilayer boards for luxury passenger vehicles.

Recent industry trends show established players like Aoshikang Technology investing heavily in HDI (High Density Interconnect) technology to meet evolving automotive electronics requirements. At the same time, smaller manufacturers are forming strategic alliances to compete in this capital-intensive market.

List of Key Automotive PCBA Board Manufacturers

- Victory Giant Technology (China)

- Shenzhen Kinwong (China)

- Avary Holding (China)

- Shantou Goworld (China)

- WUS Printed Circuit (Taiwan)

- Aoshikang Technology (China)

- Guangdong Kingshine Electronic Technology (China)

- Olimpic Circuit Technology (China)

- Bomin Electronics (China)

- Shenzhen Honglian Circuit (China)

- Palpilot International Corp (Taiwan)

- ABP Electronics Limited (China)

Segment Analysis:

By Type

Multilayer PCBA Board Segment Leads Market Due to Rising Complexity in Automotive Electronics

The Automotive PCBA Board market is segmented based on type into:

- Single-layer PCBA Board

- Double-layer PCBA Board

- Multilayer PCBA Board

- Flexible PCBA Board

- Others

By Application

Passenger Car Segment Dominates Market Share Due to Higher Electronics Integration

The market is segmented based on application into:

- Commercial Vehicle

- Passenger Car

- Electric Vehicles

- Autonomous Vehicles

- Others

By Component

ECU Application Segment Contributes Largest Share

The market is segmented based on component application into:

- Engine Control Module (ECM)

- Transmission Control Module (TCM)

- Body Control Module (BCM)

- Powertrain Control Module (PCM)

- Others

By Technology

Surface Mount Technology Gaining Traction in Automotive Electronics

The market is segmented based on manufacturing technology into:

- Through-hole Technology

- Surface Mount Technology

- Mixed Technology

- Others

Regional Analysis: Automotive PCBA Board Market

North America

The North American Automotive PCBA Board market is characterized by high adoption of advanced electronics in vehicles, driven by stringent safety regulations and consumer demand for connected car technologies. The U.S. dominates the region, accounting for over 70% of regional demand, with major automakers increasingly integrating ADAS (Advanced Driver Assistance Systems) and infotainment solutions. While production volumes have declined post-pandemic, OEMs are prioritizing high-density interconnect (HDI) PCBA boards to support next-gen electric vehicles (EVs) and autonomous driving features. However, reshoring of electronics manufacturing from Asia presents both opportunities and cost challenges for suppliers.

Europe

Europe’s market is shaped by the automotive industry’s rapid electrification, with the EU’s 2035 ban on combustion engines accelerating PCB demand for EVs. Germany remains the production hub, hosting 41% of regional OEM plants, while Eastern European nations emerge as cost-competitive manufacturing bases. Compliance with IPC-6012 automotive grade standards is mandatory, pushing suppliers toward multilayer and flex-rigid PCB solutions. The region faces material shortages, particularly for high-frequency laminates used in radar PCBs, creating supply chain vulnerabilities despite strong technical capabilities.

Asia-Pacific

As the global automotive production center, Asia-Pacific consumes 58% of Automotive PCBA Boards, with China alone representing 32% of worldwide automobile output. While Japan and South Korea lead in high-reliability boards for luxury vehicles, Chinese manufacturers dominate mass-market segments through cost leadership. The region shows diverging trends: Japanese OEMs prioritize ceramic substrates for performance, whereas Southeast Asian markets favor cost-effective FR4 materials. India’s expanding local production under the PLI scheme is driving double-digit PCB growth, though quality consistency remains a concern among domestic suppliers.

South America

Automotive PCBA Board adoption in South America trails global trends, with Brazil and Argentina relying heavily on imported electronics due to limited local PCB fabrication capabilities. The market shows potential with Brazil’s Rota 2030 automotive policy incentivizing technology upgrades, but economic instability discourages long-term investments. Most boards are simplex designs for basic vehicle functions, though multinational OEMs are introducing higher-layer count PCBs in premium models assembled locally. Currency fluctuations and import dependency create pricing volatility across the supply chain.

Middle East & Africa

This emerging market shows nascent growth, primarily serving vehicle assembly plants in Morocco, South Africa, and Turkey – the latter exporting 425,000 vehicles annually to Europe. While most PCBA Boards are imported, localized production is increasing for basic infotainment and lighting systems. The UAE’s focus on electric public transport and Saudi Arabia’s EV ambitions present future opportunities, though current demand is constrained by low automotive electronics penetration and dependence on budget vehicle imports from Asia.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Automotive PCBA Board markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Automotive PCBA Board market was valued at USD 3.2 billion in 2024 and is projected to reach USD 4.8 billion by 2032, growing at a CAGR of 5.2%.

- Segmentation Analysis: Detailed breakdown by product type (single-layer, double-layer, multilayer PCBA boards), application (commercial vehicles, passenger cars), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, with country-level analysis. Asia-Pacific currently dominates with 58% market share, followed by Europe (22%) and North America (15%).

- Competitive Landscape: Profiles of leading market participants including Palpilot International Corp, Victory Giant Technology, and Shenzhen Kinwong, covering their product offerings, R&D focus, manufacturing capacity, and recent M&A activities.

- Technology Trends & Innovation: Assessment of emerging technologies including high-density interconnect (HDI) PCBs, flexible PCBs for automotive applications, and integration with advanced driver-assistance systems (ADAS).

- Market Drivers & Restraints: Evaluation of factors such as increasing vehicle electrification (with 26 million EVs projected by 2030) and challenges like semiconductor shortages and raw material price volatility.

- Stakeholder Analysis: Strategic insights for PCB manufacturers, automotive OEMs, component suppliers, and investors regarding the evolving automotive electronics ecosystem.

Research methodology includes primary interviews with industry experts across the value chain, analysis of financial reports from key players, and data validation from industry associations including IPC and OICA.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive PCBA Board Market?

-> The global Automotive PCBA Board Market size was valued at US$ 12.3 billion in 2024 and is projected to reach US$ 23.4 billion by 2032, at a CAGR of 8.5% during the forecast period 2025-2032.

Which key companies operate in Global Automotive PCBA Board Market?

-> Key players include Palpilot International Corp, Victory Giant Technology, Shenzhen Kinwong, Camelot Electronics Technology, and ABP Electronics Limited, among others.

What are the key growth drivers?

-> Key growth drivers include increasing vehicle electrification, rising ADAS adoption (projected in 60% of new vehicles by 2030), and automotive digitalization trends.

Which region dominates the market?

-> Asia-Pacific dominates with 58% market share, driven by China’s automotive production which accounts for 32% of global output.

What are the emerging trends?

-> Emerging trends include high-frequency PCBs for 5G-connected vehicles, miniaturization of electronic components, and adoption of aluminum substrate PCBs for thermal management.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...