MARKET INSIGHTS

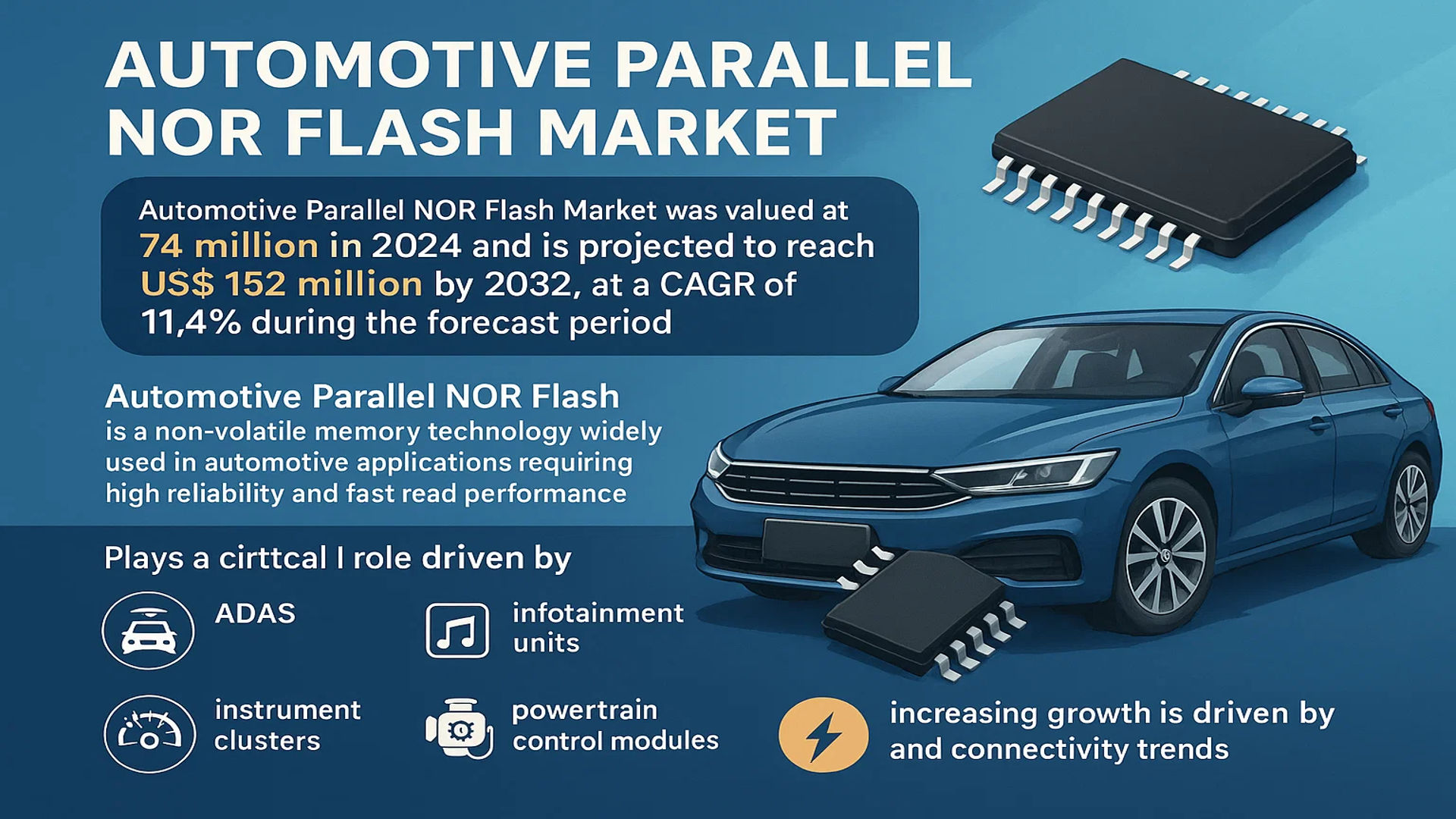

The global Automotive Parallel NOR Flash Market was valued at 74 million in 2024 and is projected to reach US$ 152 million by 2032, at a CAGR of 11.4% during the forecast period.

Automotive Parallel NOR Flash is a non-volatile memory technology widely used in automotive applications requiring high reliability and fast read performance. These memory solutions play a critical role in vehicle systems such as advanced driver-assistance systems (ADAS), infotainment units, powertrain control modules, and instrument clusters due to their ability to retain data without power and withstand harsh automotive environments.

The market growth is driven by increasing vehicle electrification and connectivity trends, along with rising demand for memory solutions in electric vehicles. While the 3.3V segment currently dominates applications, the 1.8V variant is gaining traction for low-power designs. Major manufacturers like Infineon Technologies, Micron, and Macronix continue to innovate, with recent developments focusing on higher density solutions up to 4Gb to meet the growing data storage requirements of next-generation vehicles.

MARKET DYNAMICS

MARKET DRIVERS

Increasing Vehicle Electrification and Advanced Driver-Assistance Systems (ADAS) to Propel Demand

The rapid electrification of vehicles and growing implementation of ADAS are key drivers for the Automotive Parallel NOR Flash market. Modern vehicles now integrate over 100 electronic control units powered by flash memory solutions to enable real-time data processing for critical functions. With connected car technologies projected to cover over 90% of new vehicles by 2030, the demand for high-reliability parallel NOR flash memory is set to accelerate. This memory type provides the necessary fast read speeds and data integrity required for safety-critical automotive applications operating in extreme temperature ranges.

Stringent Automotive Safety Standards Driving Adoption of Robust Memory Solutions

Global automotive safety regulations like ISO 26262 are mandating higher reliability standards for vehicle electronics, accelerating the displacement of consumer-grade memory components with automotive-grade alternatives. Parallel NOR flash meets the stringent AEC-Q100 qualification requirements for automotive electronics, offering superior endurance with 100,000 program/erase cycles and data retention exceeding 20 years. This reliability advantage positions it as the preferred solution for mission-critical systems including antilock braking, electronic stability control, and airbag deployment.

Market Expansion Supported by Regional Automotive Production Growth

The ongoing expansion of automotive manufacturing in Asia-Pacific, particularly China’s emergence as the world’s largest vehicle producer, is generating substantial demand for automotive memory solutions. Chinese automakers alone are projected to increase their parallel NOR flash adoption by 22% annually through 2032 as they transition to more sophisticated vehicle architectures. Meanwhile, North American and European markets continue to demand high-performance memory for premium vehicle applications, maintaining stable growth in developed regions.

MARKET RESTRAINTS

High Cost Structure Limits Adoption in Entry-Level Vehicles

While parallel NOR flash offers superior performance characteristics, its higher price point compared to alternative memory technologies creates adoption barriers in cost-sensitive vehicle segments. The automotive-grade qualification process adds 30-40% to component costs, making price competition challenging in emerging markets where vehicle affordability remains paramount. This cost-pressure is particularly evident in Asia’s burgeoning electric vehicle sector where manufacturers aggressively optimize bill-of-materials expenses.

Design Complexity and Extended Qualification Cycles Impact Time-to-Market

The integration of parallel NOR flash into automotive systems presents significant engineering challenges. Memory solutions must undergo extensive environmental testing spanning temperature extremes, vibration resistance, and electromagnetic compatibility – a process typically requiring 12-18 months for full automotive qualification. This extended development timeline conflicts with automakers’ accelerating product cycles, particularly in the rapidly evolving electric vehicle segment where time-to-market advantages are crucial.

Emerging Memory Technologies Present Long-Term Competitive Threat

While parallel NOR flash currently dominates safety-critical automotive applications, emerging non-volatile memory technologies like MRAM and FRAM are making inroads in certain use cases. These alternatives offer advantages in write endurance and power consumption, though they currently lack the proven reliability track record and price scalability of established NOR flash solutions. Nevertheless, continued innovation in memory technologies will require NOR flash manufacturers to accelerate their own roadmap advancements to maintain market leadership.

MARKET OPPORTUNITIES

Vehicle Digitalization Creating New Application Frontiers for High-Speed Memory

The automotive industry’s digital transformation is unlocking significant opportunities for parallel NOR flash suppliers. Modern vehicles process exponentially increasing data volumes from hundreds of sensors, requiring memory solutions that combine capacity with deterministic read performance. The transition to domain-based and zonal vehicle architectures will drive demand for distributed memory solutions capable of supporting local processing while meeting automotive reliability standards. This architectural shift presents suppliers with opportunities to develop customized memory configurations optimized for specific vehicle subsystems.

Automotive Over-the-Air (OTA) Updates Driving Need for Robust Memory Solutions

The proliferation of OTA update capabilities represents a major growth opportunity for qualified parallel NOR flash suppliers. As automakers implement field-upgradable vehicle software architectures, they require memory solutions that support both the storage and execution of firmware updates without compromising system reliability. NOR flash’s execute-in-place (XIP) capability and superior bit-error-rate performance make it ideally suited for these critical update mechanisms. Suppliers that can demonstrate proven reliability in OTA deployment scenarios stand to gain substantial market share in this high-growth segment.

Regional Market Expansion Through Localized Production

The ongoing geographic diversification of automotive supply chains creates opportunities for memory suppliers to establish localized production and qualification capabilities. Several governments are implementing policies to strengthen domestic semiconductor ecosystems for automotive applications, offering incentives for memory manufacturers to establish local testing and packaging facilities. Suppliers that can demonstrate regional value-add through localized production and support services will be well-positioned to capitalize on these emerging market opportunities while mitigating geopolitical supply chain risks.

AUTOMOTIVE PARALLEL NOR FLASH MARKET TRENDS

Advancements in Automotive Electronics Fuel Demand for Parallel NOR Flash

The automotive industry is undergoing a rapid transformation with increasing vehicle electrification and autonomous driving technologies, driving significant growth in the Automotive Parallel NOR Flash market. With a valuation of $74 million in 2024 and an expected CAGR of 11.4%, the market is projected to reach $152 million by 2032. The demand is primarily fueled by the need for fast, reliable, and durable memory solutions in critical vehicle applications such as Advanced Driver Assistance Systems (ADAS), powertrain control modules, and infotainment systems. Additionally, the integration of AI-powered ADAS and higher-level autonomous driving functionalities is pushing automakers toward high-performance Parallel NOR Flash memory, known for its superior read speeds and endurance in extreme automotive conditions.

Other Trends

Rising Adoption in Electric Vehicles (EVs)

The shift toward electric mobility is accelerating the adoption of 3.3V and 1.8V Parallel NOR Flash memory, particularly in battery management systems and energy-efficient computing modules. The 3.3V segment alone is projected to exhibit substantial growth due to its compatibility with legacy automotive systems and ability to support real-time processing requirements. Furthermore, regions like China and Europe, which account for a dominant share of EV production, are witnessing heightened investments in memory solutions that enhance vehicle performance while optimizing power consumption. As a result, semiconductor manufacturers are expanding their automotive-grade NOR Flash portfolios to cater to this evolving demand.

Expansion of Connected and Autonomous Vehicles

The push for connected and autonomous vehicles (CAVs) is another major factor boosting the Automotive Parallel NOR Flash market. As vehicles evolve into data-intensive mobility platforms, the need for robust, error-resistant memory solutions has surged. Leading automotive memory suppliers, including Infineon Technologies, Micron, and Winbond, are enhancing their product offerings with AEC-Q100 qualified NOR Flash solutions that meet stringent automotive reliability standards. Moreover, the increasing deployment of Over-The-Air (OTA) updates in modern vehicles necessitates non-volatile memory solutions with high endurance, further reinforcing the market expansion. With autonomous driving moving from L2 to L3+ automation levels, the role of Parallel NOR Flash in storing firmware and critical boot codes securely becomes increasingly indispensable.

COMPETITIVE LANDSCAPE

Key Industry Players

Memory Semiconductor Leaders Expand Automotive-Grade Offerings for Next-Generation Vehicles

The global Automotive Parallel NOR Flash market exhibits a moderately consolidated structure, with established semiconductor players competing alongside specialized memory solution providers. Infineon Technologies leads the segment, leveraging its extensive expertise in automotive electronics and robust supply chain partnerships. The company’s focus on AEC-Q100 qualified memory solutions has secured its position across European and North American automotive OEMs.

Micron Technology and Winbond collectively hold nearly 35% market share (2024 estimates), driven by their high-performance 3.3V NOR flash solutions for advanced driver assistance systems (ADAS) and vehicle networking applications. These companies continue to invest in elevated temperature tolerance (up to 125°C) and enhanced endurance cycles (>100,000 program/erase cycles) to meet stringent automotive requirements.

The competitive intensity is increasing as manufacturers expand product portfolios through both organic development and strategic partnerships. Macronix recently introduced its 1.8V ultra-low power NOR flash series specifically designed for electric vehicle battery management systems, while Microchip Technology strengthened its position through the acquisition of a NOR flash IP portfolio in 2023.

Chinese manufacturers like GigaDevice and Ingenic Semiconductor are gaining traction through cost-optimized solutions for domestic automotive applications, though they currently focus primarily on the commercial vehicle segment. These players are expected to increase global presence as automotive memory demand grows in emerging markets.

List of Key Automotive Parallel NOR Flash Manufacturers

- Infineon Technologies (Germany)

- Macronix International Co., Ltd. (Taiwan)

- Micron Technology, Inc. (U.S.)

- Winbond Electronics Corporation (Taiwan)

- GigaDevice Semiconductor (China)

- Ingenic Semiconductor (China)

- Microchip Technology Inc. (U.S.)

Segment Analysis:

By Type

3.3V Segment Dominates Due to High Compatibility with Automotive Systems

The market is segmented based on type into:

- 3.3V

- 1.8V

- Others

By Application

Passenger Cars Segment Leads Due to Growing Demand for Advanced Infotainment Systems

The market is segmented based on application into:

- Passenger Cars

- Commercial Cars

By End User

OEMs Hold Largest Share Due to Direct Integration Requirements

The market is segmented based on end user into:

- Original Equipment Manufacturers (OEMs)

- Aftermarket

By System

Infotainment Systems Maintain Strong Demand for High-Speed Flash Memory

The market is segmented based on system into:

- Engine Control Units

- Infotainment Systems

- Advanced Driver Assistance Systems

- Powertrain Control

- Safety Systems

Regional Analysis: Automotive Parallel NOR Flash Market

Asia-Pacific

Asia-Pacific is the dominant region in the Automotive Parallel NOR Flash market, accounting for the largest revenue share due to rapid automotive electrification and the presence of leading semiconductor manufacturers like Infineon Technologies, Macronix, and Winbond. China holds the highest market share, driven by its booming EV sector and government initiatives such as the “Made in China 2025” policy, which emphasizes semiconductor self-sufficiency. Japan and South Korea follow closely, with key players like Micron and Samsung catering to domestic and export demands. The region’s growth is fueled by increasing adoption of advanced driver-assistance systems (ADAS) and infotainment systems in vehicles. However, supply chain disruptions and geopolitical tensions over semiconductor trade remain key challenges.

North America

The North American market is characterized by strong demand for high-performance memory solutions in electric and autonomous vehicles, particularly in the U.S., where automakers like Tesla and Ford are integrating sophisticated ECUs and telematics systems. Strict automotive safety regulations (e.g., NHTSA mandates) and investments in autonomous driving R&D are accelerating NOR Flash adoption. Key suppliers, including Microchip Technology and Micron, are expanding production to meet the growing need for reliable flash memory in automotive applications. However, higher costs of advanced NOR Flash variants compared to NAND hinder broader adoption in cost-sensitive segments.

Europe

Europe’s market is propelled by stringent automotive safety standards (e.g., Euro NCAP) and the region’s leadership in luxury and performance vehicles. Germany, home to automakers like BMW and Mercedes-Benz, is the largest consumer of automotive NOR Flash for powertrain and safety-critical systems. The EU’s focus on reducing semiconductor dependency through the European Chips Act is also encouraging local supply chain development. Despite steady growth, slower EV adoption in Eastern Europe and competition from NAND-based solutions pose challenges for market expansion.

South America

The South American market is in early growth stages, with Brazil and Argentina showing gradual uptake of Automotive Parallel NOR Flash, primarily for legacy vehicle systems. Economic instability and lower automotive production volumes restrict investments in high-end memory solutions. However, increasing foreign automaker investments and rising demand for connected vehicles offer long-term opportunities. Local suppliers face difficulties competing with established global players due to limited technological infrastructure.

Middle East & Africa

This region exhibits nascent demand for Automotive Parallel NOR Flash, mainly driven by luxury vehicle imports and fleet modernization in Gulf Cooperation Council (GCC) countries. Limited local automotive manufacturing and reliance on imported semiconductor components constrain market growth. Nevertheless, infrastructure development projects and smart city initiatives in the UAE and Saudi Arabia could spur demand for advanced vehicle technologies in the long term.

Report Scope

This market research report provides a comprehensive analysis of the global Automotive Parallel NOR Flash market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 74 million in 2024 and is projected to reach USD 152 million by 2032, growing at a CAGR of 11.4%.

- Segmentation Analysis: Detailed breakdown by product type (3.3V, 1.8V, Others), application (Passenger Cars, Commercial Cars), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis. The U.S. market is estimated at USD million in 2024, while China is expected to reach USD million.

- Competitive Landscape: Profiles of leading market participants, including Infineon Technologies, Macronix, Micron, Winbond, GigaDevice, Ingenic Semiconductor, and Microchip Technology, their product offerings, R&D focus, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in automotive memory solutions, including integration with AI/IoT, semiconductor design trends, and evolving industry standards for high-reliability applications.

- Market Drivers & Restraints: Evaluation of factors driving market growth such as increasing vehicle electrification and advanced driver-assistance systems (ADAS), along with challenges like supply chain constraints and stringent automotive quality standards.

- Stakeholder Analysis: Insights for component suppliers, automotive OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities in automotive memory solutions.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive Parallel NOR Flash Market?

-> Automotive Parallel NOR Flash Market was valued at 74 million in 2024 and is projected to reach US$ 152 million by 2032, at a CAGR of 11.4% during the forecast period.

Which key companies operate in Global Automotive Parallel NOR Flash Market?

-> Key players include Infineon Technologies, Macronix, Micron, Winbond, GigaDevice, Ingenic Semiconductor, and Microchip Technology, among others.

What are the key growth drivers?

-> Key growth drivers include increasing vehicle electrification, demand for advanced safety systems, and growth in automotive infotainment applications.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, driven by automotive production in China and Japan, while North America remains a significant market for advanced automotive electronics.

What are the emerging trends?

-> Emerging trends include development of higher-density NOR Flash solutions, integration with vehicle networking systems, and increasing adoption in electric vehicle powertrains.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...