Automotive Microprocessor Market Insights

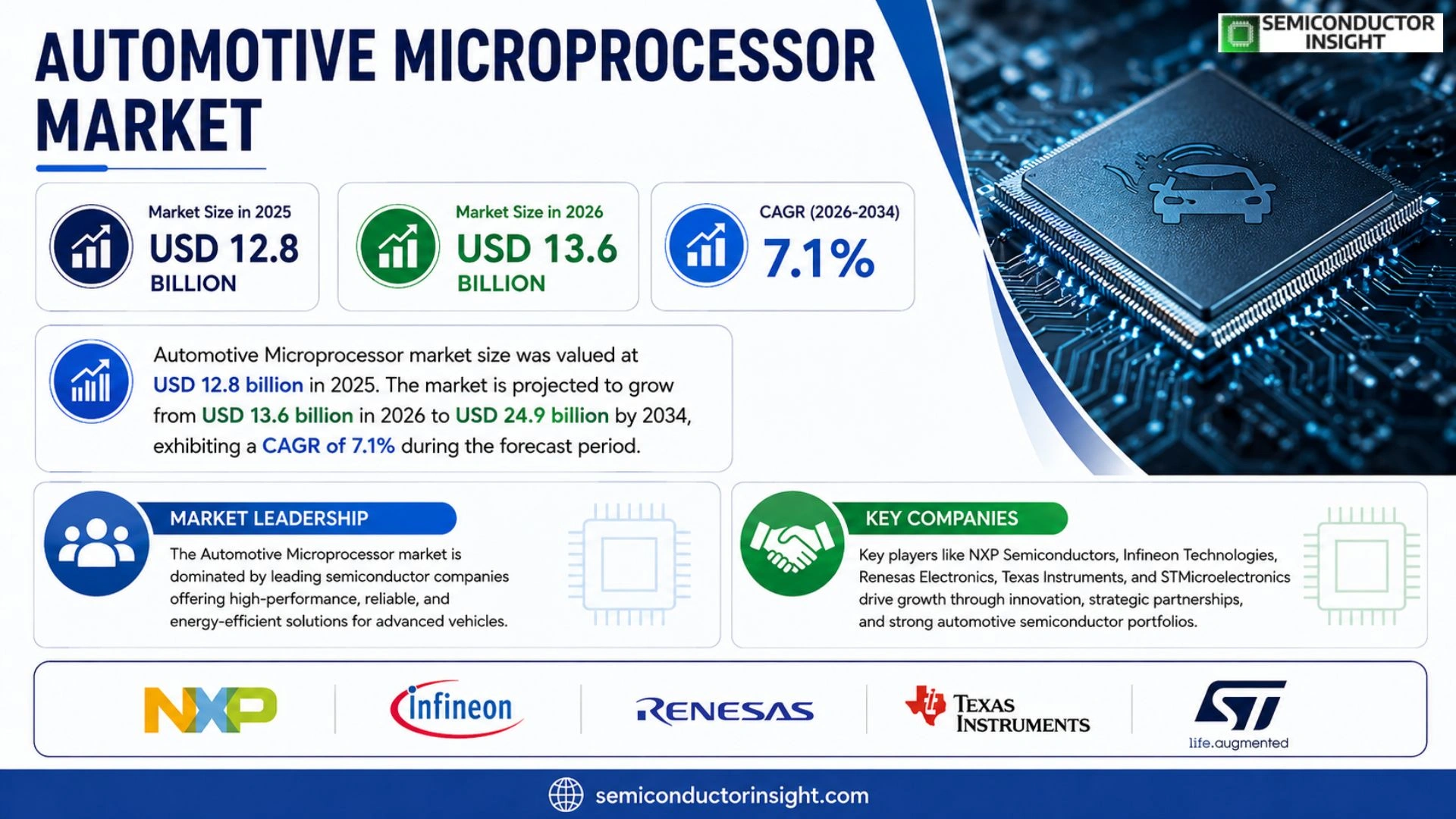

Global Automotive Microprocessor Market size was valued at USD 12.8 billion in 2025. The market is projected to grow from USD 13.6 billion in 2026 to USD 24.9 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period.

Automotive microprocessors are high‑performance computing units engineered for vehicle systems such as advanced driver‑assistance (ADAS), infotainment platforms, powertrain management and emerging autonomous‑driving functions. They combine multi‑core CPUs with graphics processing units (GPUs), neural processing units (NPUs) and built‑in safety mechanisms that comply with functional‑safety standards like ISO 26262.

The market is experiencing rapid growth because electric‑vehicle adoption accelerates demand for sophisticated power‑train controllers, while stricter safety regulations push OEMs toward more capable ADAS processors. Furthermore, the race toward Level 3–5 autonomy fuels investment in AI‑enabled chips from leading suppliers such as NXP Semiconductors, Renesas Electronics, Infineon Technologies and Texas Instruments.

MARKET DRIVERS

Electrification and Advanced Driver‑Assistance Systems (ADAS)

The rapid shift toward electric vehicles (EVs) is compelling OEMs to adopt high‑performance microprocessors that can manage battery‑management systems, powertrain control, and real‑time sensor fusion. Automotive Microprocessor Market growth is therefore anchored in the need for processors that deliver low‑latency, high‑throughput computing for EV power electronics.

Connectivity and Over‑the‑Air (OTA) Updates

5G rollout and the rising demand for connected car services require processors with integrated security modules and multi‑core architectures. This connectivity driver pushes manufacturers to source more capable chips, accelerating market adoption across passenger and commercial segments.

➤ “The convergence of electrification, autonomy, and connectivity is creating a cumulative demand for next‑generation automotive processors, projected to double the addressable market within five years.”

Regulatory pressures for emission reduction and safety compliance are also prompting the integration of sophisticated microcontrollers, further reinforcing Automotive Microprocessor Market trajectory.

MARKET CHALLENGES

Supply Chain Volatility

Global semiconductor shortages have limited the availability of critical silicon, forcing OEMs to manage lead‑times and inventory buffers, which raises production costs and hampers timely product launches.

Other Challenges

Design Complexity

Modern vehicles require heterogeneous computing platforms that combine CPUs, GPUs, and AI accelerators. Integrating these diverse components while meeting automotive safety standards adds considerable engineering overhead.

MARKET RESTRAINTS

High Development Costs

The R&D investment needed to develop automotive‑grade microprocessors,meeting functional safety (ISO 26262) and reliability requirements,is substantial, limiting participation to a few large players.

Stringent Certification Processes

Each new processor must undergo extensive validation and certification cycles, which can extend time‑to‑market and increase overall project budgets.

MARKET OPPORTUNITIES

Emerging AI‑Driven Applications

AI workloads such as predictive maintenance, in‑vehicle speech recognition, and autonomous navigation demand edge‑optimized processors. Companies that can deliver energy‑efficient AI accelerators are positioned to capture significant share of Automotive Microprocessor Market.

Expansion in Tier‑2 and Tier‑3 Cities

Growth of automotive sales in emerging economies is driving demand for cost‑effective microprocessor solutions that balance performance with affordability, opening new revenue channels for chip makers.

Automotive Microprocessor Market Trends

Rise of AI‑Enabled Processors for Advanced Driver‑Assistance

Vehicle manufacturers are accelerating the adoption of AI‑enabled microprocessors to support increasingly complex driver‑assistance functions. These chips integrate multi‑core CPUs with dedicated neural processing units that can execute deep‑learning inference for lane‑keeping, object detection, and predictive braking in real time. Suppliers such as NXP Semiconductors, Renesas Electronics, Infineon Technologies and Texas Instruments are delivering silicon that combines high compute density with low power consumption, enabling seamless integration into compact infotainment‑ADAS platforms. The convergence of high‑resolution cameras, radar and lidar data streams demands processors that can fuse sensor inputs while maintaining deterministic latency, a requirement that drives the shift toward heterogeneous architectures. As autonomous‑driving software stacks mature, the demand for scalable processor families that can be re‑programmed across vehicle generations continues to grow. Additionally, 5G connectivity is enabling over‑the‑air firmware updates and cloud‑based perception services, which require processors with secure boot and encrypted communication capabilities, further intensifying the need for robust microcontroller platforms.

Other Trends

Electric‑Vehicle Powertrain Integration

The transition to electric propulsion is reshaping processor design because power‑train controllers now require real‑time coordination of battery‑management, motor‑inverter and regenerative‑braking systems. Modern microprocessors embed high‑speed communication interfaces such as CAN‑FD and Ethernet, allowing a unified control network that reduces wiring complexity. Thermal management techniques, including on‑die temperature sensors and dynamic voltage scaling, are incorporated to maintain efficiency under high load conditions typical of EV operation. By consolidating power‑train and vehicle‑level functions onto a single chip, OEMs achieve lower bill‑of‑materials and faster development cycles, an advantage that is reflected in the increasing proportion of EV‑focused silicon in recent product roadmaps. The inclusion of integrated power‑module drivers and on‑chip voltage regulation reduces external component count and improves reliability, a trend that aligns with the modular vehicle architecture promoted by major OEM alliances.

Safety‑Centric Architecture Expansion

Regulatory pressure on functional safety is prompting manufacturers to adopt safety‑centric processor architectures that embed redundancy and error‑detection mechanisms directly in silicon. Compliance with ISO 26262 functional‑safety standards is becoming a baseline requirement, leading to the integration of lockstep cores, built‑in self‑test (BIST) circuits and deterministic memory protection. These features not only enhance crash‑avoidance capabilities but also simplify system‑level certification by reducing the need for external safety modules. As vehicle platforms evolve toward higher levels of autonomy, Automotive Microprocessor Market is expected to prioritize chips that can provide both high performance and verified safety pathways, ensuring that emerging software functions can be deployed with confidence. Upcoming safety assessment protocols, such as the enhanced Euro NCAP criteria, are also driving chip suppliers to embed advanced diagnostic telemetry, enabling continuous monitoring of safety‑critical pathways throughout the vehicle lifespan.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive Microprocessor Market – Competitive Overview

Automotive Microprocessor segment is dominated by a handful of semiconductor giants that supply multi‑core CPUs, GPUs, NPUs and functional‑safety blocks for ADAS, infotainment and powertrain control. NXP Semiconductors leads the market with its S32 automotive platform, leveraging deep relationships with Tier‑1 OEMs to capture the highest revenue share. Renesas Electronics follows closely, offering the R-Car family that combines high‑performance compute with ISO 26262‑compliant safety features. Infineon Technologies and Texas Instruments round out the top tier, providing robust power‑train and safety‑critical processors that benefit from the rapid electrification of vehicles. These leaders benefit from scale, extensive IP portfolios and long‑term engineering collaborations that create high entry barriers for new entrants.

Beyond the dominant quartet, a diverse set of niche and emerging players intensifies competition in specialized domains. STMicroelectronics supplies cost‑effective microcontrollers for body‑electronics, while Qualcomm’s Snapdragon automotive SoCs target AI‑driven infotainment and Level 3+ autonomy. MediaTek is expanding its automotive portfolio with AI‑accelerated chips for emerging markets. Intel’s Mobileye focuses on vision‑centric processors for advanced driver‑assistance, and NVIDIA leverages its DRIVE platform for high‑end autonomous‑driving workloads. Samsung Electronics, AMD, Bosch, Continental, and ON Semiconductor round out the field, each delivering differentiated IP or integration capabilities that address specific functional or regional requirements, thereby enriching the competitive landscape.

List of Key Automotive Microprocessor Companies Profiled

- NXP Semiconductors

- Renesas Electronics

- Infineon Technologies

- Texas Instruments

- STMicroelectronics

- Qualcomm

- MediaTek

- Intel (Mobileye)

- NVIDIA

- Samsung Electronics

- AMD

- Bosch

- Continental

- ON Semiconductor

- Mitsubishi Electric

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

AI‑enabled processors are emerging as the dominant type because they integrate neural processing units that support real‑time perception and decision‑making required for higher levels of vehicle autonomy.

|

| By Application |

|

ADAS and autonomous driving microprocessors drive the strategic focus of suppliers, as they must handle intensive perception workloads and safety‑critical decision logic.

|

| By End User |

|

OEMs and Tier‑1 suppliers shape the microprocessor roadmap through close collaboration with silicon vendors, demanding chips that balance performance, power efficiency and long‑term reliability.

|

| By Integration Architecture |

|

Heterogeneous integration is gaining traction as vehicle architectures demand the coexistence of compute, memory and analog functions within a compact footprint.

|

| By Safety Compliance |

|

ISO 26262 compliant processors dominate the safety‑critical segment because they embed verification mechanisms that satisfy automotive functional‑safety requirements.

|

Regional Analysis: North America

Stringent safety standards and cybersecurity concerns are key drivers, leading to a demand for microprocessors with robust security features and real-time processing capabilities.

The growing demand for connected car features and advanced infotainment systems is fueling the need for microprocessors with high processing power and seamless connectivity options.

The rise of electric vehicles necessitates specialized microprocessors for efficient battery management, motor control, and power electronics, presenting significant growth opportunities.

The development and deployment of advanced driver-assistance systems and autonomous driving technologies are driving the demand for high-performance, safety-certified microprocessors.

Europe

Automotive Microprocessor market in Europe is characterized by a strong focus on sustainability and the adoption of advanced technologies to meet stringent emission regulations. European manufacturers are actively investing in electric vehicles and developing sophisticated ADAS systems, creating a significant demand for high-performance microprocessors. Business strategies emphasize collaboration within the European supply chain and a strong commitment to environmental responsibility. The region’s automotive industry is highly innovative, with a focus on developing intelligent transportation solutions.

Asia-Pacific

Asia-Pacific represents the largest and fastest-growing market for automotive microprocessors globally. Driven by the rapid expansion of automotive production in countries like China and India, the region is witnessing significant demand for microprocessors across various vehicle segments. The focus is on cost-effective solutions and the integration of advanced features for both traditional and electric vehicles. Business strategies involve localized manufacturing, strong partnerships with local automotive players, and a focus on meeting the specific needs of the diverse Asian market.

South America

Automotive Microprocessor market in South America is an emerging market with significant growth potential. The increasing demand for vehicles and the gradual adoption of advanced technologies are driving the demand for microprocessors. The region’s automotive industry is relatively concentrated, with opportunities for regional players to cater to specific local needs. Business strategies often involve cost competitiveness and adapting to the specific regulatory environments of different South American countries.

Middle East & Africa

Automotive Microprocessor market in the Middle East & Africa is a developing market with growing opportunities. The increasing urbanization and rising disposable incomes are fueling vehicle sales and creating demand for advanced automotive features. The region is witnessing a growing interest in electric vehicles and connected car technologies, leading to increasing demand for specialized microprocessors. Business strategies involve adapting to the specific needs of the region and focusing on cost-effective solutions.

Report Scope

This market research report provides a comprehensive analysis of the Automotive Microprocessor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Automotive Microprocessor Market?

-> Automotive Microprocessor Market size was valued at USD 12.8 billion in 2025. The market is projected to grow from USD 13.6 billion in 2026 to USD 24.9 billion by 2034.

Which key companies operate Automotive Microprocessor Market?

-> Key players include NXP Semiconductors, Renesas Electronics, Infineon Technologies, and Texas Instruments, among others.

What are the key growth drivers?

-> Key growth drivers include accelerated electric‑vehicle adoption, stricter safety‑regulation requirements, and the push toward Level 3‑5 autonomous driving.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, driven by high EV production volumes and substantial semiconductor manufacturing capacity.

What are the emerging trends?

-> Emerging trends include AI‑enabled processing units, integration of neural processing units (NPUs), and increased focus on functional‑safety compliant designs (ISO 26262).

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...