Automotive film capacitor for DC-Link in traction inverter Market Insights

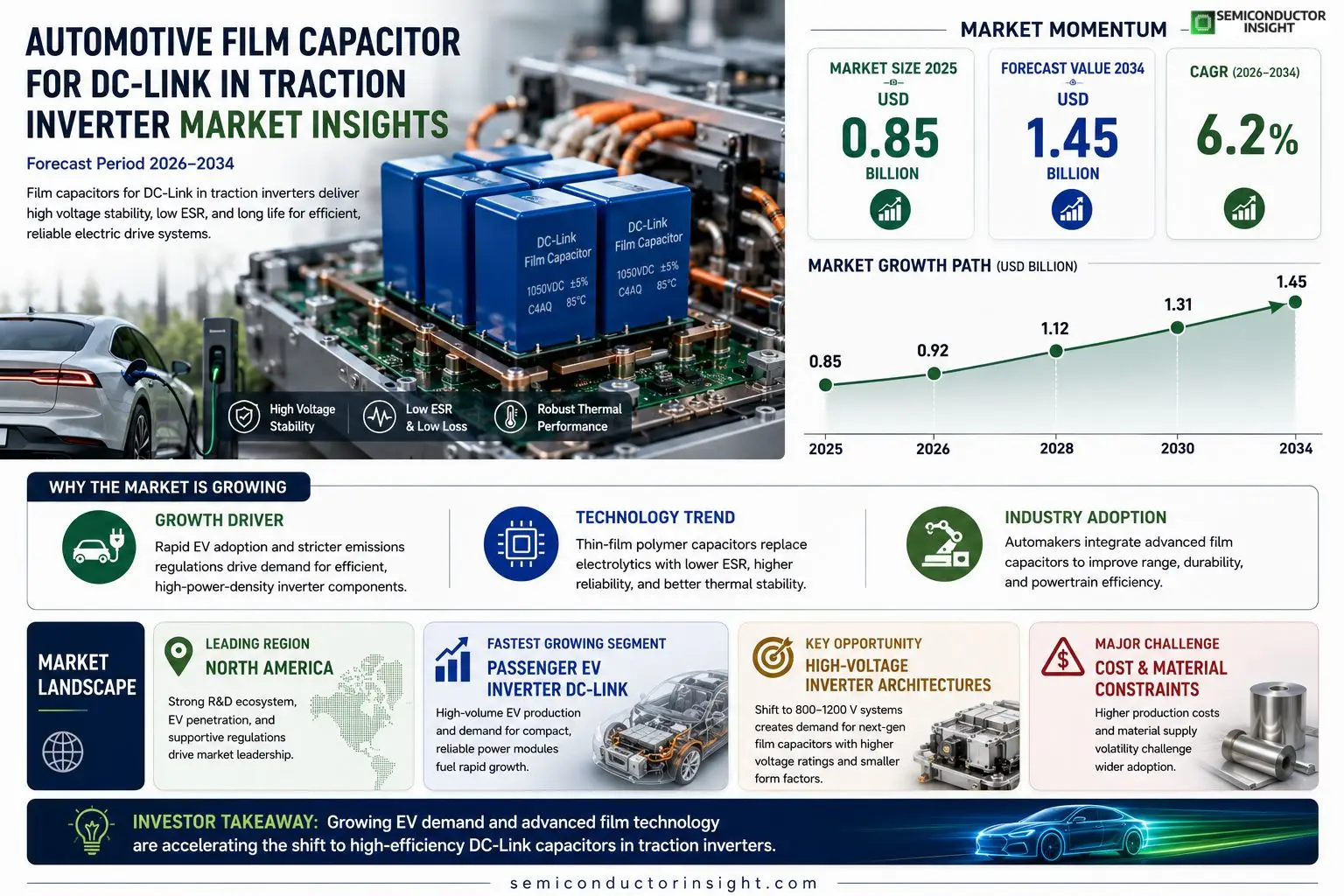

Automotive film capacitor for DC‑Link in traction inverter market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.92 billion in 2026 to USD 1.45 billion by 2034, exhibiting a CAGR of 6.2% during the forecast period.

Automotive film capacitors used as DC‑Link components in traction inverters are thin‑film polymer devices that provide high voltage stability, low ESR, and robust thermal performance required for electric‑drive systems. They replace traditional electrolytic capacitors to improve efficiency and reliability of power conversion modules.The market is experiencing rapid growth because electric‑vehicle (EV) sales are accelerating worldwide and manufacturers demand higher power density and longer lifespan for inverter modules. Furthermore, stricter emissions regulations and government incentives are driving OEMs toward advanced capacitor technologies. Key players such as KEMET Corporation, Vishay Intertechnology, Panasonic Corporation and TDK are expanding their product portfolios and investing in R&D to meet these evolving requirements.

MARKET DRIVERS

Rising Electrification of Vehicles

Automotive film capacitor for DC-Link in traction inverter Market is being propelled by the rapid expansion of electric and hybrid vehicle fleets worldwide. Governments are mandating stricter emissions targets, which drives automakers to adopt high‑efficiency power‑train components that improve range and reduce energy loss.

Stringent Efficiency Regulations

Regulatory frameworks such as CO₂ fleet‑average limits compel manufacturers to seek components with low ESR and high ripple current capability. Film capacitors fulfill these requirements, offering reliable performance under the high‑frequency switching conditions of modern traction inverters.

➤ “Advanced film dielectric materials are extending the voltage rating of Automotive capacitors, enabling higher DC‑Link voltages without compromising reliability.”

In addition, the push toward lightweight vehicle architectures encourages the adoption of film capacitors, which provide comparable energy density to electrolytic solutions while delivering superior thermal stability and longer service life.

MARKET CHALLENGES

Cost Competitiveness and Material Availability

Despite technical advantages, Automotive film capacitor for DC-Link in traction inverter Market faces steep production costs due to premium film materials and precise manufacturing tolerances. This price premium can deter cost‑sensitive OEMs, especially in emerging markets where budget constraints remain significant.

Other Challenges

Reliability Under Extreme Conditions

Automotive capacitors must endure wide temperature fluctuations and mechanical vibrations. Ensuring consistent performance over a vehicle’s lifetime requires rigorous testing and robust quality control, adding further expense and complexity to the supply chain.

MARKET RESTRAINTS

Regulatory Safety and Certification Barriers

Certification processes for Automotive components are increasingly stringent, demanding extensive validation of film capacitor behavior under crash, thermal, and electromagnetic scenarios. The time‑intensive compliance pathway can delay entry of new capacitor designs into Automotive film capacitor for DC-Link in traction inverter Market, constraining rapid adoption.

MARKET OPPORTUNITIES

Emerging High‑Voltage Inverter Architectures

Next‑generation traction inverters are moving toward higher DC‑Link voltages (up to 1,200 V) to improve power density. This shift opens a sizable niche for film capacitors engineered with enhanced dielectric strength and reduced form factor, presenting a lucrative growth avenue within Automotive film capacitor for DC-Link in traction inverter Market.

Automotive film capacitor for DC-Link in traction inverter Market Trends

Rising EV Penetration Drives Capacitor Innovation

Automotive film capacitor for DC-Link in traction inverter Market is being reshaped by the accelerating adoption of electric vehicles worldwide. OEMs are prioritizing power‑density improvements and longer module lifespans to meet consumer expectations for range and performance. Stricter emissions standards and government incentive programs are further compelling manufacturers to replace traditional electrolytic components with advanced film solutions. As a result, demand for capacitors that offer stable high‑voltage operation, low equivalent series resistance, and robust thermal characteristics has risen sharply across the power‑train supply chain.

Other Trends

Shift Toward Thin‑Film Polymer Technology

Thin‑film polymer capacitors have become the preferred DC‑Link technology in traction inverters due to their superior voltage stability and reduced heat generation. Their construction eliminates the electrolyte degradation issues that limit the lifespan of conventional capacitors, delivering a more predictable performance envelope under the high‑frequency switching conditions typical of modern inverters. The lower ESR of film devices translates directly into higher overall inverter efficiency, supporting the broader industry goal of maximizing vehicle range while minimizing energy loss.

Expansion of OEM Partnerships and R&D Investment

Key players such as KEMET Corporation, Vishay Intertechnology, Panasonic Corporation, and TDK are deepening collaborative agreements with vehicle manufacturers to co‑develop next‑generation capacitor architectures. Investment in research focused on dielectric material enhancements and package miniaturization is driving incremental performance gains. These strategic moves are positioning Automotive film capacitor for DC-Link in traction inverter Market to sustain its momentum as electric‑drive power electronics evolve toward higher power densities and stricter reliability standards.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive Film Capacitor for DC‑Link in Traction Inverter Market Overview

The market is currently dominated by a handful of large semiconductor and passive‑component manufacturers that have leveraged deep R&D capabilities to deliver thin‑film polymer capacitors meeting the high‑voltage, low‑ESR, and thermal‑stability requirements of modern traction inverters. KEMET Corporation, Vishay Intertechnology, Panasonic Corporation and TDK hold the greatest market share, each offering extensive DC‑Link product families and investing in next‑generation film‑technology platforms. Their supply chains, coupled with strategic OEM partnerships, enable them to capture the bulk of orders from major electric‑vehicle manufacturers seeking reliable inverter modules.Beyond the tier‑one leaders, a robust cohort of specialized and regionally focused firms contributes critical niche capabilities. Murata Manufacturing, AVX Corporation, Cornell Dubilier Electronics, United Chemi‑Con, Samsung Electro‑Mechanics, Hitachi Chemical, Rohm Semiconductor, Taiyo Yuden, EPCOS (TDK subsidiary), and Infineon Technologies provide differentiated thin‑film designs, custom form factors, or cost‑optimized solutions that address specific vehicle platforms and emerging market segments. Their agility in addressing bespoke specifications sustains a diversified competitive landscape.

List of Key Automotive Film Capacitor for DC‑Link in Traction Inverter Companies Profiled

- KEMET Corporation

- Vishay Intertechnology

- Panasonic Corporation

- TDK

- Murata Manufacturing

- AVX Corporation

- Cornell Dubilier Electronics

- United Chemi‑Con

- Samsung Electro‑Mechanics

- Hitachi Chemical

- Rohm Semiconductor

- Taiyo Yuden

- EPCOS (TDK subsidiary)

- Infineon Technologies

- Vishay BCM

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

High‑Temperature Polypropylene Film Capacitors

|

| By Application |

|

Passenger EV Inverter DC‑Link

|

| By End User |

|

OEMs

|

| By Voltage Rating |

|

600 V‑800 V Range

|

| By Dielectric Material |

|

Polypropylene Film

|

Regional Analysis: Automotive film capacitor for DC-Link in traction inverter Market

North America

The region showcases rapid uptake of high‑voltage film capacitors, driven by OEMs seeking compact inverter modules. Collaborative R&D programs streamline material innovations, enabling thinner laminates with enhanced dielectric strength, which directly supports higher power‑density traction systems.

A diversified supplier landscape, spanning domestic and cross‑border partners, cushions the market against raw‑material shortages. Companies are investing in localized production lines to reduce lead times and reinforce supply continuity for critical capacitor components.

Federal emissions targets and state‑level zero‑emission vehicle mandates compel automakers to integrate reliable DC‑Link capacitors. Compliance frameworks encourage the use of components that meet stringent safety and thermal performance criteria.

Established capacitor producers compete with emerging specialty firms focusing on niche film technologies. Strategic alliances and joint‑development agreements are common, fostering faster time‑to‑market for advanced traction‑inverter solutions.

Europe

European Automotive manufacturers are emphasizing sustainability, which drives demand for high‑efficiency film capacitors in traction inverters. The market benefits from coordinated EU green‑mobility policies and substantial funding for electric‑powertrain research. Manufacturers prioritize capacitors with low dielectric loss to improve overall vehicle efficiency, while regulatory standards such as the EU‑type approval process enforce strict safety and performance metrics. Market participants are also exploring circular‑economy approaches, recycling capacitor materials to align with strict environmental directives. Collaborative platforms across Germany, France, and the Nordic region accelerate technology transfer, ensuring that European OEMs maintain a competitive edge in the EV landscape.

Asia‑Pacific

Asia‑Pacific exhibits the fastest growth trajectory, propelled by massive EV production volumes in China, India, and South Korea. While the region lags in the maturity of film‑capacitor technology compared with North America, extensive government subsidies and ambitious electrification roadmaps incentivize rapid adoption. Local capacitor manufacturers are scaling up capacity, focusing on cost‑effective multilayer film solutions that meet the high‑volume demands of Tier‑1 suppliers. However, the market faces challenges related to raw‑material price volatility and varying standards across countries, prompting regional alliances to harmonize specifications and ensure consistent product quality across the supply chain.

South America

In South America, market development for Automotive film capacitor for DC-Link in traction inverter Market is nascent but gaining momentum as Brazil and Argentina expand their EV pilot programs. Limited domestic manufacturing capacity leads to reliance on imports, driving attention to cost‑competitiveness and supply‑chain reliability. Government incentives aimed at reducing urban emissions are encouraging Automotive firms to explore advanced film‑capacitor configurations that enhance inverter efficiency while maintaining affordability for emerging consumer markets.

Middle East & Africa

The Middle East & Africa region presents a mixed outlook; affluent Gulf markets are adopting luxury EVs, creating niche demand for high‑performance film capacitors in traction inverters. Meanwhile, sub‑Saharan nations face infrastructure constraints that temper broader market uptake. Stakeholders focus on developing robust, temperature‑tolerant capacitor designs to cope with harsh climatic conditions, while regional partnerships aim to establish localized assembly facilities that can gradually reduce dependence on external suppliers.

Report Scope

This market research report provides a comprehensive analysis of the Automotive film capacitor for DC-Link in traction inverter Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as Automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Automotive film capacitor for DC-Link in traction inverter Market?

-> Automotive film capacitor for DC-Link in traction inverter Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 1.45 billion by 2034.

Which key companies operate in Automotive film capacitor for DC-Link in traction inverter Market?

-> Key players include KEMET Corporation, Vishay Intertechnology, Panasonic Corporation, and TDK, among others.

What are the key growth drivers?

-> Key growth drivers include accelerating electric‑vehicle sales, demand for higher power density and longer lifespan in inverter modules, stricter emissions regulations, and government incentives for advanced capacitor technologies.

Which region dominates the market?

-> Information on the dominant region is not disclosed in the provided reference.

What are the emerging trends?

-> Emerging trends include the shift from electrolytic to thin‑film polymer capacitors, improvements in voltage stability and thermal performance, and increased integration of capacitors within EV power‑train architectures.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...