Automotive Embedded Systems Market Insights

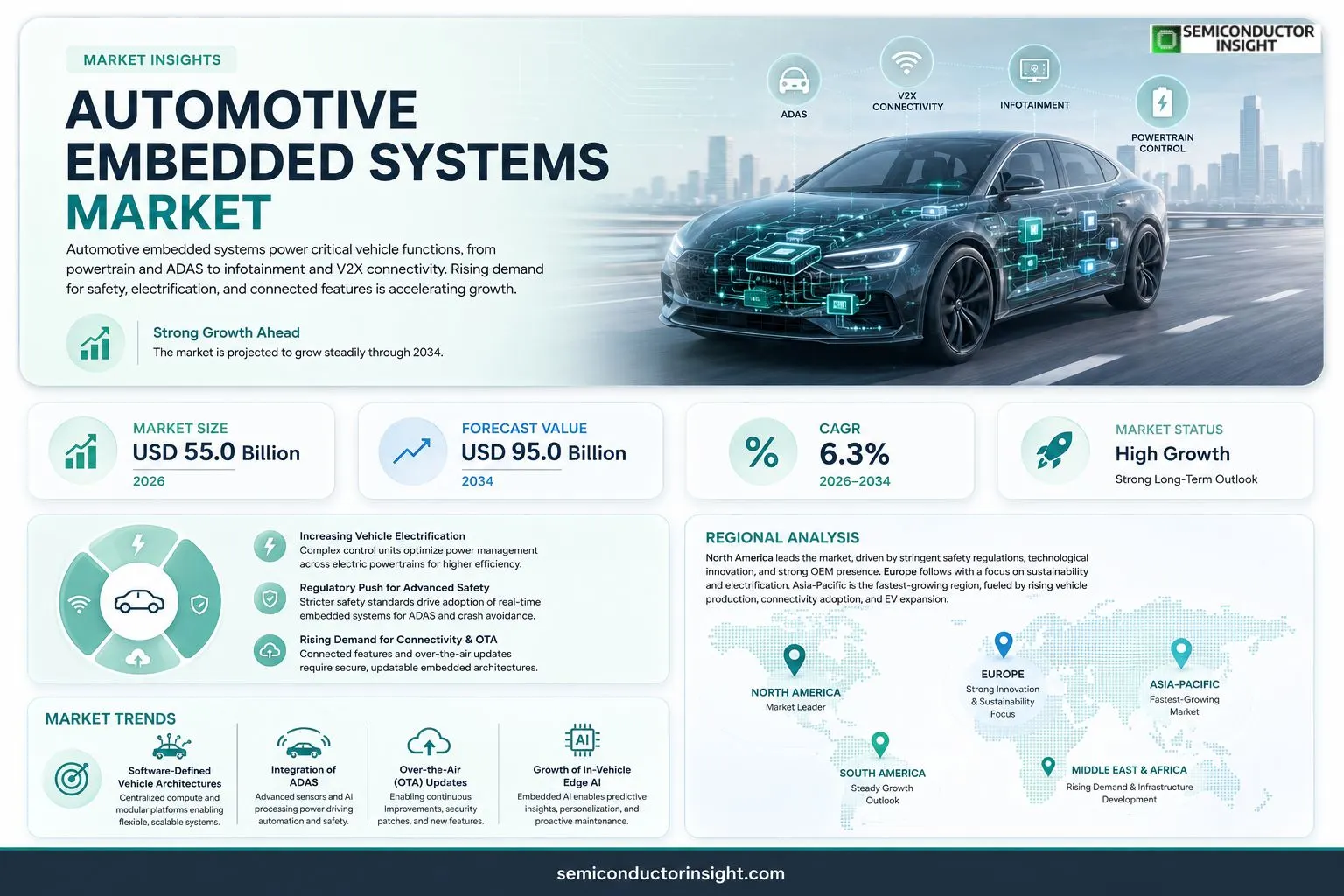

Global automotive embedded systems market size was valued at USD 55.0 billion in 2025. The market is projected to grow from USD 55.0 billion in 2025 to USD 95.0 billion by 2034, exhibiting a CAGR of 6.3% during the forecast period.

Automotive embedded systems are specialized hardware‑software platforms that control critical vehicle functions such as powertrain management, advanced driver‑assistance systems (ADAS), infotainment, and vehicle‑to‑everything (V2X) communication. These integrated solutions combine microcontrollers, sensors, real‑time operating systems, and connectivity modules to enable reliable and secure operation of modern cars.

The market is accelerating because manufacturers are investing heavily in autonomous driving technologies, electrification, and over‑the‑air updates, while consumer demand for connected features continues to rise. Furthermore, regulatory pressure for safety and emissions compliance fuels adoption of sophisticated control units. Key players such as Bosch Liebherr Automotive, Continental AG, Denso Corporation, and NXP Semiconductors are expanding their portfolios through strategic partnerships and R&D initiatives.

MARKET DRIVERS

Increasing Vehicle Electrification

The shift toward electric powertrains is creating a demand for highly integrated control units. Automotive Embedded Systems Market participants are deploying sophisticated power management modules that enable seamless coordination between battery, motor, and drivetrain components.

Regulatory Push for Advanced Safety

Stricter safety standards worldwide require real‑time processing of sensor data for functions such as autonomous emergency braking and lane‑keeping assistance. This regulatory environment drives OEMs to adopt more capable embedded platforms.

➤ “Embedded processors now handle both safety‑critical and infotainment workloads on a single silicon die, reducing bill of materials and weight.”

Additionally, the rising consumer expectation for over‑the‑air updates accelerates the need for secure, up‑datable embedded architectures, reinforcing market growth.

MARKET CHALLENGES

Complex Software Integration

Designers must reconcile heterogeneous software stacksreal‑time operating systems, AUTOSAR layers, and AI inference engineswithin constrained memory footprints. Misalignment can lead to latency issues that jeopardize safety functions.

Other Challenges

Talent Shortage

The rapid evolution of automotive software engineering outpaces the supply of engineers skilled in both automotive standards and modern embedded AI, creating hiring bottlenecks.

MARKET RESTRAINTS

High Development Costs

Developing, validating, and certifying safety‑critical embedded software involves extensive testing cycles and compliance documentation. These upfront expenditures can deter smaller suppliers from entering Automotive Embedded Systems Market.

MARKET OPPORTUNITIES

Growth of In‑Vehicle AI

Edge AI capabilities embedded directly in ECUs enable predictive maintenance, driver behavior analysis, and personalized infotainment. Companies that can offer low‑power, high‑throughput AI accelerators are positioned to capture new revenue streams.

Expansion into Connected Services

As vehicles become platforms for subscription‑based services, embedded systems must support secure connectivity, data analytics, and OTA update frameworks. This creates a fertile ground for software‑as‑a‑service models within Automotive Embedded Systems Market.

Automotive Embedded Systems Market Trends

Shift Toward Software‑Defined Vehicle Architectures

Automotive Embedded Systems Market is increasingly defined by a shift toward software‑defined vehicle architectures. OEMs are consolidating legacy electronic control units into centralized compute platforms that run real‑time operating systems and support over‑the‑air configurability. This approach reduces hardware complexity while enabling rapid deployment of new functions through software updates. Integrated microcontrollers are paired with high‑speed communication buses, allowing powertrain, infotainment, and safety domains to share processing resources. As a result, development cycles become shorter and system integration costs decline. The trend also encourages deeper collaboration between semiconductor suppliers and tier‑one integrators, fostering standardized interfaces that accelerate the adoption of modular embedded solutions across vehicle line‑ups.

Other Trends

Integration of Advanced Driver‑Assistance Systems (ADAS)

Advanced driver‑assistance systems continue to drive the evolution of Automotive Embedded Systems Market. Sensors such as lidar, radar, and camera arrays feed high‑resolution data into embedded processors that run perception algorithms in real time. The growing sophistication of lane‑keeping, adaptive cruise control, and automated emergency braking requires embedded platforms with higher compute density and deterministic latency. Manufacturers are therefore prioritizing multicore processors and dedicated AI accelerators within control units. This hardware evolution is complemented by stricter safety standards, prompting rigorous functional safety certification (ISO 26262) for embedded software. The combined pressure of consumer demand for convenience and regulatory mandates for crash avoidance solidifies ADAS as a cornerstone of future vehicle architectures.

Growth of Over‑the‑Air (OTA) Update Capabilities

Over‑the‑air (OTA) update capabilities have emerged as a critical growth vector for Automotive Embedded Systems Market. With OTA, firmware and application software can be delivered directly to the vehicle’s embedded modules without dealer intervention. This capability supports continuous improvement of vehicle performance, security patching, and the rollout of new infotainment services. Embedded systems now incorporate secure boot, encrypted communication channels, and fail‑safe mechanisms to protect against cyber threats during remote updates. The operational flexibility afforded by OTA reduces warranty expenses and extends the functional lifespan of automotive platforms. Consequently, OEMs are embedding OTA‑ready architectures from the design stage, aligning hardware selection with long‑term service strategies.

COMPETITIVE LANDSCAPEKey Industry Players

Automotive Embedded Systems Market Competitive Landscape Overview

The automotive embedded systems arena is dominated by a handful of global powerhouses that command both breadth of portfolio and depth of technology. Bosch Liebherr Automotive, Continental AG, Denso Corporation, and NXP Semiconductors together account for a substantial share of revenue, leveraging extensive R&D budgets to integrate advanced driver‑assistance systems (ADAS), powertrain control units, and V2X communication modules. Their strategic focus on over‑the‑air update capability and safety‑critical compliance positions them as primary suppliers for OEMs transitioning to autonomous and electrified platforms. These incumbents benefit from long‑standing partnerships with tier‑one manufacturers, enabling economies of scale that reinforce their market leadership while setting high barriers to entry for new entrants.Beyond the core four, a vibrant cohort of niche and emerging players enriches the competitive fabric. Companies such as Infineon Technologies, Renesas Electronics, Qualcomm Technologies, and STMicroelectronics bring specialized microcontroller and connectivity expertise that complement the wider ecosystem. Regional champions like Hyundai Mobis, Valeo, Magna International, ZF Friedrichshafen, Aptiv, and Texas Instruments contribute focused solutions for infotainment, sensor fusion, and electric powertrain integration. Their agility and targeted innovation allow them to capture market segments that demand differentiated functionality, fostering a dynamic environment where collaboration and competition drive rapid technological advancement across the automotive embedded systems landscape.

List of Key Automotive Companies Profiled

-

Bosch Liebherr Automotive

-

Continental AG

- Denso Corporation

- NXP Semiconductors

- Infineon Technologies

- Renesas Electronics

- Qualcomm Technologies

- STMicroelectronics

- Hyundai Mobis

- Valeo

- Magna International

- ZF Friedrichshafen

- Aptiv

- Texas Instruments

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Control Units are the foundational segment driving integration across vehicle functions.

|

| By Application |

|

Advanced Driver Assistance emerges as the most dynamic application area.

|

| By End User |

|

OEMs drive the strategic direction of embedded system adoption.

|

| By Technology |

|

Sensor Fusion Platforms are pivotal for creating reliable perception layers.

|

| By Vehicle Architecture |

|

Autonomous Vehicles represent the most forward‑looking architecture segment.

|

Regional Analysis: North America

North America

North America sees a strong emphasis on specialized design and development services for complex automotive embedded systems, catering to both established OEMs and Tier 1 suppliers. The demand for expertise in software development, hardware integration, and system-level engineering remains high.

The development and deployment of Advanced Driver-Assistance Systems (ADAS) and autonomous driving technologies are major drivers within the North American Automotive Embedded Systems Market. This includes advanced sensors, high-performance computing platforms, and sophisticated control algorithms.

With the rise of connected vehicles, there is a growing need for advanced connectivity and infotainment systems. This involves integrating cellular, Wi-Fi, and other communication technologies with in-vehicle entertainment and navigation platforms.

Given the increasing reliance on software and connectivity, cybersecurity has become a critical aspect of the North American Automotive Embedded Systems Market. Solutions focused on protecting vehicles from cyber threats are gaining significant traction.

North America

Automotive Embedded Systems Market in North America is characterized by a high degree of technological sophistication and a strong focus on innovation. The integration of complex embedded systems is essential for meeting evolving consumer demands for safety, convenience, and connectivity. A key trend is the increasing adoption of over-the-air (OTA) updates for software and system enhancements, enabling continuous improvement and new feature deployments. This region is also witnessing a shift towards more modular and scalable embedded architectures to accommodate future technological advancements. The convergence of software and hardware in automotive systems is a defining characteristic of this market.

Europe

Europe’s Automotive Embedded Systems Market is strongly influenced by stringent environmental regulations and a commitment to sustainable mobility. The push towards electric vehicles (EVs) is a significant driver, requiring advanced battery management systems, power electronics, and charging infrastructure control units. European OEMs are also heavily investing in connectivity and autonomous driving technologies, aligning with the region’s focus on intelligent transportation systems. The market emphasizes energy efficiency and the development of robust, reliable embedded systems capable of operating in diverse climatic conditions.

Asia-Pacific

The Asia-Pacific Automotive Embedded Systems Market is experiencing rapid growth, driven by increasing automotive production and rising disposable incomes. China is a particularly significant market, serving as both a major manufacturing hub and a large end-user market for vehicles equipped with sophisticated embedded systems. The demand for affordable yet feature-rich automotive electronics is high, leading to a focus on cost-effective solutions. The region is also witnessing growing investment in electric vehicles and connected car technologies, presenting significant opportunities for embedded systems suppliers.

South America

Automotive Embedded Systems Market in South America is showing steady growth, primarily driven by the expanding automotive industry in countries like Brazil and Argentina. The focus is on enhancing vehicle safety and functionality, with increasing adoption of ADAS features in higher-end vehicles. The market is also becoming more receptive to connected car technologies, albeit at a slower pace compared to North America and Europe. Cost sensitivity remains a key factor in this region’s market dynamics.

Middle East & Africa

Automotive Embedded Systems Market in the Middle East & Africa is witnessing growth linked to increasing vehicle ownership and infrastructure development. The demand for robust and reliable embedded systems that can withstand harsh environmental conditions is a key consideration. There is a growing interest in connected car services and the adoption of ADAS features, particularly in the luxury vehicle segment. The region presents significant potential for future growth as automotive industries continue to expand.

Report Scope

This market research report provides a comprehensive analysis of the Automotive Embedded Systems Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Automotive Embedded Systems Market?

-> Automotive Embedded Systems Market was valued at USD 55.0 billion in 2025 and is expected to reach USD 95.0 billion by 2034.

Which key companies operate in Automotive Embedded Systems Market?

-> Key players include Bosch Liebherr Automotive, Continental AG, Denso Corporation, and NXP Semiconductors, among others.

What are the key growth drivers?

-> Key growth drivers include investments in autonomous driving technologies, vehicle electrification, over‑the‑air (OTA) software updates, rising consumer demand for connected features, and regulatory pressure for safety and emissions compliance.

Which region dominates the market?

-> Regional dominance information is not explicitly stated in the reference.

What are the emerging trends?

-> Emerging trends include autonomous driving development, electrified powertrains, OTA updates, and advanced connectivity solutions such as ADAS and V2X.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...