MARKET INSIGHTS

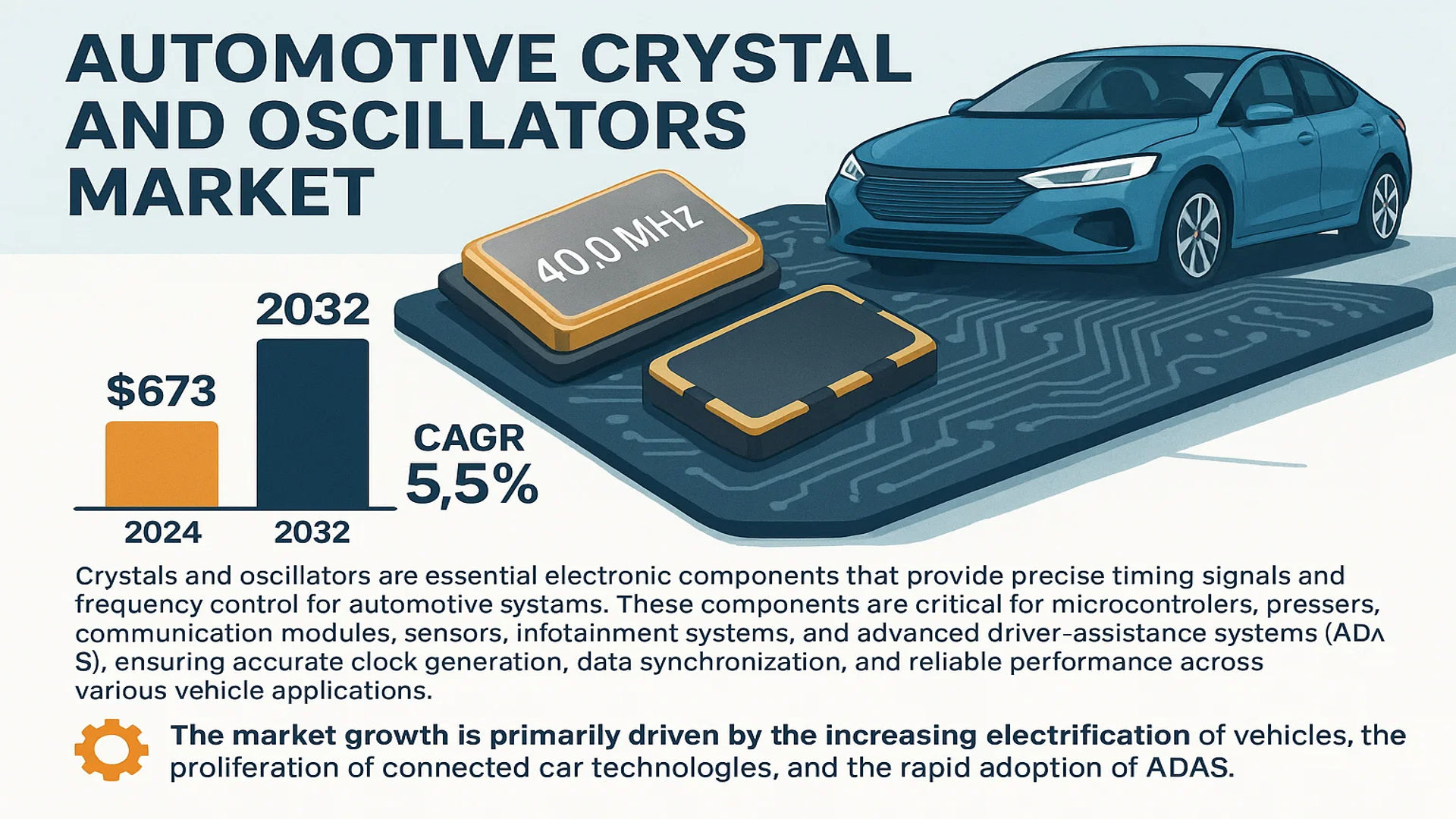

The global Automotive Crystal and Oscilators Market was valued at 673 million in 2024 and is projected to reach US$ 972 million by 2032, at a CAGR of 5.5% during the forecast period.

Crystals and oscillators are essential electronic components that provide precise timing signals and frequency control for automotive systems. These components are critical for the operation of microcontrollers, processors, communication modules, sensors, infotainment systems, and advanced driver-assistance systems (ADAS), ensuring accurate clock generation, data synchronization, and reliable performance across various vehicle applications.

The market growth is primarily driven by the increasing electrification of vehicles, the proliferation of connected car technologies, and the rapid adoption of ADAS. The expansion of electric vehicle production, which requires sophisticated electronic control units, further fuels demand. However, manufacturers face significant challenges, including the need to meet stringent automotive-grade standards like AEC-Q200 and to ensure component reliability amidst harsh operating conditions involving extreme temperatures, vibration, and electromagnetic interference.

MARKET DYNAMICS

MARKET DRIVERS

Proliferation of Advanced Driver Assistance Systems (ADAS) to Drive Market Expansion

The rapid adoption of Advanced Driver Assistance Systems (ADAS) is significantly propelling the automotive crystal and oscillators market. These systems rely on precise timing components for sensor fusion, radar operation, LiDAR scanning, and camera synchronization. With over 50 million vehicles equipped with ADAS globally in 2024, the demand for high-precision timing solutions continues to escalate. The integration of autonomous driving functionalities requires timing accuracy within nanoseconds to ensure real-time decision-making and collision avoidance. Automotive-grade crystals and oscillators provide the necessary frequency stability and phase noise performance for these critical safety applications, making them indispensable components in modern vehicle architectures.

Electric Vehicle Revolution to Accelerate Market Growth

The global transition toward electric vehicles represents a substantial growth driver for automotive crystals and oscillators. Electric vehicle production increased by approximately 35% in 2024 compared to the previous year, reaching over 14 million units worldwide. These vehicles require sophisticated battery management systems, power electronics, and motor control units that depend on precise timing components. Crystals and oscillators ensure accurate switching frequencies for power converters, synchronization for battery management systems, and timing references for vehicle control units. The complexity of electric powertrains, which can contain up to 10,000 individual electronic components, necessitates reliable timing solutions that maintain performance across varying temperature conditions and electromagnetic environments.

Vehicle Connectivity and Infotainment Systems to Boost Demand

The integration of advanced connectivity features and infotainment systems in modern vehicles is driving substantial growth in the automotive crystal and oscillators market. Current vehicle architectures incorporate multiple connectivity modules including 5G, V2X communication, GPS navigation, and Wi-Fi/Bluetooth systems, each requiring dedicated timing components. The average premium vehicle now contains approximately 15 separate timing devices to support these functions. The growing consumer demand for seamless connectivity, high-definition audio/video streaming, and real-time navigation services necessitates oscillators with low jitter and high frequency stability. Furthermore, the emergence of software-defined vehicles and over-the-air update capabilities requires robust timing solutions that can maintain synchronization across multiple electronic control units.

Moreover, regulatory mandates for vehicle safety and communication standards are expected to further fuel market growth.

➤ For instance, recent automotive safety regulations in multiple regions now require specific timing accuracy standards for vehicle-to-everything (V2X) communication systems to ensure interoperability and road safety.

Furthermore, the increasing integration of artificial intelligence and machine learning algorithms in vehicle systems is anticipated to drive additional demand for high-performance timing components throughout the forecast period.

MARKET CHALLENGES

Stringent Automotive-Grade Certification Requirements to Challenge Market Participants

The automotive crystal and oscillators market faces significant challenges related to the rigorous certification standards required for automotive applications. Components must meet AEC-Q200 qualification standards, which involve extensive testing under extreme conditions including temperature cycling from -40°C to +125°C, mechanical shock testing up to 1500G, and humidity resistance requirements. The certification process typically adds 20-30% to development costs and extends product development cycles by 6-12 months. These requirements create substantial barriers for new market entrants and smaller manufacturers who may lack the resources for comprehensive testing facilities and quality management systems.

Other Challenges

Harsh Operating Environment Constraints

Automotive electronic components must operate reliably in extremely challenging environments characterized by wide temperature variations, constant vibration, and electromagnetic interference. Crystals and oscillators are particularly sensitive to these conditions, with performance degradation occurring at temperature extremes beyond their specified ranges. Vehicle manufacturers require components that maintain frequency stability within ±50 ppm across the entire operating temperature range, which demands sophisticated compensation techniques and robust packaging solutions.

Electromagnetic Compatibility Issues

The increasing density of electronic systems in modern vehicles creates significant electromagnetic compatibility challenges. Timing components must minimize electromagnetic emissions while maintaining immunity to external interference. The proliferation of high-frequency communication systems and power electronics in electric vehicles exacerbates these challenges, requiring advanced shielding techniques and careful circuit layout considerations that add complexity and cost to component design.

MARKET RESTRAINTS

Supply Chain Constraints and Component Shortages to Deter Market Growth

The automotive crystal and oscillators market faces significant restraints due to ongoing supply chain challenges and component shortages. The global semiconductor crisis that began in recent years continues to affect timing component availability, with lead times for certain automotive-grade oscillators extending beyond 52 weeks. Automotive manufacturers require components with zero defect rates, which limits the pool of qualified suppliers and creates dependency on a few established manufacturers. The specialized manufacturing processes for quartz crystals and the limited global production capacity for high-quality quartz materials further constrain market growth. These supply chain issues have caused production delays and increased costs throughout the automotive industry.

Additionally, the concentration of manufacturing capabilities in specific geographic regions creates vulnerability to geopolitical tensions and trade restrictions. The automotive industry’s just-in-time manufacturing philosophy exacerbates these challenges, as inventory buffers remain minimal despite extended component lead times.

Furthermore, the increasing complexity of automotive electronic systems requires more specialized timing components, which limits the ability to substitute alternative products during shortage situations, thereby restraining market expansion.

MARKET OPPORTUNITIES

Emergence of Silicon-Based MEMS Oscillators to Create New Growth Opportunities

The development and adoption of silicon-based MEMS (Micro-Electro-Mechanical Systems) oscillators present significant growth opportunities for the automotive timing components market. MEMS technology offers advantages over traditional quartz-based solutions, including better shock and vibration resistance, smaller form factors, and improved scalability. The market for MEMS-based timing solutions in automotive applications is projected to grow at a compound annual growth rate exceeding 15% through 2032. These devices demonstrate performance stability within ±25 ppm across automotive temperature ranges while offering reduced susceptibility to acoustic noise and mechanical stress. Major automotive semiconductor manufacturers are investing heavily in MEMS oscillator technology, with several companies announcing new product developments specifically designed for automotive applications.

Additionally, the integration of multiple timing functions into single-chip solutions provides opportunities for component consolidation and system cost reduction. The ability to program oscillator frequencies digitally enables greater flexibility in automotive electronic design and simplifies inventory management for manufacturers.

Furthermore, advancements in packaging technology and the development of system-in-package solutions that combine oscillators with other automotive ICs are expected to create additional market opportunities while addressing space constraints in increasingly crowded vehicle electronic systems.

AUTOMOTIVE CRYSTAL AND OSCILLATORS MARKET TRENDS

Advanced Driver Assistance Systems (ADAS) and Autonomous Driving to Emerge as a Key Trend

The proliferation of Advanced Driver Assistance Systems (ADAS) and the ongoing development of autonomous driving technologies represent a dominant trend significantly accelerating demand for high-performance automotive crystals and oscillators. These components are fundamental to the precise timing and synchronization required for sensor fusion, where data from radar, LiDAR, cameras, and ultrasonic sensors must be integrated in real-time. For instance, a typical Level 2+ autonomous vehicle can utilize over 30 individual timing devices to coordinate these complex systems. The shift towards higher levels of automation, particularly Level 3 and Level 4, necessitates oscillators with exceptional frequency stability, often requiring tolerances as tight as ±10 ppm across an extended automotive temperature range of -40°C to +125°C. This is because even minor timing inaccuracies can lead to significant errors in object detection and path planning algorithms. Furthermore, the integration of V2X (Vehicle-to-Everything) communication, a cornerstone for fully autonomous ecosystems, relies heavily on highly accurate and stable reference clocks to ensure seamless and secure data exchange between vehicles and infrastructure, further cementing the critical role of these components.

Other Trends

Electrification of Powertrains

The global transition towards electric vehicles (EVs) and hybrid electric vehicles (HEVs) is creating a substantial and distinct demand vector for crystals and oscillators. Unlike traditional internal combustion engines, electric powertrains are fundamentally managed by sophisticated electronic control units (ECUs) that require precise timing for functions like battery management (BMS), inverter control, and motor drive synchronization. The BMS alone, critical for monitoring cell voltage, temperature, and state of charge, depends on accurate clock signals for its analog-to-digital converters and communication buses. The powertrain domain in an EV is estimated to consume a significantly higher number of timing components compared to a conventional vehicle. Moreover, the high-power electronics environment within an EV, characterized by significant electrical noise and rapid switching frequencies, demands oscillators with superior electromagnetic compatibility (EMC) and low jitter performance to prevent signal integrity issues that could impact vehicle efficiency and safety.

Integration of Advanced In-Vehicle Infotainment (IVI) and Connectivity

The consumer expectation for a seamless digital experience within the automobile is pushing the boundaries of in-vehicle infotainment (IVI) systems, directly influencing the specifications of associated timing components. Modern IVI systems have evolved into complex computing hubs, often featuring multiple high-resolution displays, powerful multi-core processors, and sophisticated audio systems. These systems require a variety of crystals and oscillators to manage clock generation for graphics processing, audio sampling, and video synchronization. The trend is further amplified by the integration of 5G connectivity modules, Wi-Fi 6, and Bluetooth 5.2 for high-speed internet access and device integration. Each wireless technology operates on specific frequency bands and requires dedicated, stable reference clocks to maintain robust communication links and prevent data packet loss. This convergence of high-performance computing and multi-standard connectivity within the cabin is driving demand for miniaturized, low-power, and highly reliable timing solutions that can operate flawlessly alongside other electronic systems without causing interference.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Expansion Define Market Leadership

The global automotive crystal and oscillators market exhibits a semi-consolidated competitive structure, characterized by the presence of established multinational corporations, specialized medium-sized enterprises, and emerging regional players. This dynamic is driven by the critical need for high-reliability, automotive-grade components that meet stringent industry standards like AEC-Q200. NDK (Nihon Dempa Kogyo Co., Ltd.) and Murata Manufacturing Co., Ltd. are recognized as dominant forces, leveraging their extensive R&D capabilities, robust global supply chains, and comprehensive portfolios of quartz crystals and oscillators specifically engineered for harsh automotive environments. Their leadership is further solidified by long-standing relationships with Tier-1 automotive suppliers and direct engagements with major OEMs.

Japanese manufacturers, including Seiko Epson Corp and KDS (Daishinku Corp), also command a significant portion of the market share. Their growth is intrinsically linked to decades of expertise in precision frequency control devices and a deep understanding of the quality and reliability demands of the global automotive industry. These companies consistently invest in developing products that offer enhanced resistance to vibration, extreme temperatures, and electromagnetic interference, which are paramount for applications in Advanced Driver-Assistance Systems (ADAS) and electric vehicle powertrains.

Furthermore, strategic initiatives such as capacity expansions, targeted mergers and acquisitions, and the launch of innovative, miniaturized components are expected to be key growth levers for these leading players over the forecast period. For instance, the push towards higher-frequency, low-power oscillators for 5G-enabled telematics and V2X communication modules represents a significant area of development.

Meanwhile, companies like Microchip Technology Inc. and SiTime Corporation are aggressively strengthening their market positions. They are doing so through substantial investments in MEMS (Micro-Electro-Mechanical Systems) technology, which offers advantages in shock resistance and reliability over traditional quartz. Their strategy involves forming strategic partnerships with semiconductor makers and focusing on providing highly programmable timing solutions that offer greater design flexibility for automotive engineers working on next-generation electronic control units (ECUs) and infotainment systems.

List of Key Automotive Crystal and Oscillator Companies Profiled

- NDK (Japan)

- Murata Manufacturing Co., Ltd. (Japan)

- Seiko Epson Corp (Japan)

- TXC Corporation (Taiwan)

- KDS (Daishinku Corp) (Japan)

- Microchip Technology Inc. (U.S.)

- SiTime Corporation (U.S.)

- Rakon Limited (New Zealand)

- Hosonic Electronic Co., Ltd. (Taiwan)

- Siward Crystal Technology Co., Ltd. (Taiwan)

Segment Analysis:

By Type

Crystal Oscillators Segment Dominates the Market Due to Critical Role in Advanced Automotive Electronics

The market is segmented based on type into:

- Crystal Units

- Crystal Oscillators

By Application

Passenger Car Segment Leads Due to Higher Electronics Integration and Consumer Demand for Advanced Features

The market is segmented based on application into:

- Commercial Vehicle

- Passenger Car

By Vehicle Technology

Advanced Driver Assistance Systems (ADAS) Segment Represents Significant Growth Opportunity Due to Safety Mandates

The market is segmented based on vehicle technology into:

- Advanced Driver Assistance Systems (ADAS)

- Infotainment Systems

- Powertrain Control

- Body Electronics

- Chassis Systems

By Vehicle Propulsion

Electric Vehicle Segment Shows Strong Growth Potential Driven by Electrification Trends

The market is segmented based on vehicle propulsion into:

- Internal Combustion Engine Vehicles

- Hybrid Electric Vehicles

- Battery Electric Vehicles

Regional Analysis: Automotive Crystal and Oscillators Market

Asia-Pacific

The Asia-Pacific region dominates the global automotive crystal and oscillators market, accounting for over 45% of total consumption in 2024. This leadership position is driven by China’s massive automotive manufacturing sector, which produced approximately 30 million vehicles in 2023, alongside Japan and South Korea’s advanced automotive electronics industries. The region benefits from extensive manufacturing clusters for both vehicles and electronic components, creating a robust ecosystem for timing device suppliers. While cost sensitivity remains a factor, the rapid adoption of electric vehicles – particularly in China, which represents over 60% of global EV sales – and increasing integration of ADAS features in mid-range vehicles are driving demand for higher-quality, automotive-grade crystals and oscillators. The presence of major global suppliers like TXC Corporation, NDK, and Murata Manufacturing in the region further strengthens the supply chain.

North America

North America represents a sophisticated market characterized by stringent automotive electronics standards and rapid adoption of advanced vehicle technologies. The region’s emphasis on vehicle safety and connectivity drives demand for high-reliability crystals and oscillators that meet AEC-Q200 qualifications and can withstand harsh automotive environments. The United States, with its robust automotive industry and significant investments in autonomous vehicle development, accounts for approximately 85% of the regional market. Major automotive manufacturers and tier-1 suppliers increasingly require MEMS-based oscillators for their superior performance in vibration-intensive applications. The region’s growing electric vehicle market, supported by government incentives and infrastructure investments, further accelerates demand for precision timing components in battery management and powertrain control systems.

Europe

Europe’s automotive crystal and oscillators market is characterized by rigorous quality standards and innovation-driven demand. German automotive manufacturers, particularly those in the premium segment, are leading adopters of advanced timing solutions for their sophisticated ADAS and infotainment systems. The region’s strong focus on vehicle safety and the EU’s strict regulations regarding electronic component reliability drive the adoption of automotive-grade crystals and oscillators that exceed standard industrial specifications. European automakers’ rapid transition toward electric vehicles – with several manufacturers committing to full electrification by 2030 – creates substantial opportunities for timing component suppliers. The presence of specialized manufacturers like Micro Crystal provides local sourcing options for high-precision timing solutions tailored to European automotive requirements.

South America

South America’s automotive crystal and oscillators market is developing, with Brazil and Argentina representing the primary demand centers. The region’s automotive production, while significant, tends to focus on cost-effective vehicles with less sophisticated electronics compared to other regions. This results in greater demand for standard crystal units rather than advanced oscillators. Economic volatility and currency fluctuations sometimes constrain automotive manufacturers’ ability to invest in advanced electronic systems, though the gradual modernization of vehicle fleets and increasing safety regulations are driving steady growth. Local content requirements in countries like Brazil encourage some level of regional manufacturing, though most advanced components are still imported from global suppliers.

Middle East & Africa

The Middle East & Africa region represents an emerging market for automotive crystals and oscillators, with growth primarily driven by vehicle imports rather than local manufacturing. The UAE and Saudi Arabia are the most developed markets, with luxury vehicle segments showing strongest demand for advanced timing components. South Africa maintains some automotive manufacturing capability, particularly for commercial vehicles, creating localized demand for basic timing components. The region’s challenging climate conditions, with extreme temperatures and dust, create specific requirements for components that can operate reliably under harsh environmental stress. While the market remains relatively small compared to other regions, increasing vehicle electrification and connectivity features in imported vehicles are driving gradual market expansion.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Automotive Crystal and Oscillators markets, covering the forecast period 2025–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Analysis: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive Crystal and Oscillators Market?

-> Automotive Crystal and Oscilators Market was valued at 673 million in 2024 and is projected to reach US$ 972 million by 2032, at a CAGR of 5.5% during the forecast period.

Which key companies operate in Global Automotive Crystal and Oscillators Market?

-> Key players include Seiko Epson Corp, TXC Corporation, NDK, Microchip, Murata Manufacturing, SiTime, Rakon, Hosonic Electronic, Siward Crystal Technology, and River Eletec Corporation, among others.

What are the key growth drivers?

-> Key growth drivers include vehicle connectivity expansion, Advanced Driver Assistance Systems (ADAS) adoption, electric vehicle proliferation, infotainment system demand, and compliance with automotive-grade standards.

Which region dominates the market?

-> Asia-Pacific is the dominant market region, accounting for over 45% of global market share in 2024, driven by automotive manufacturing hubs in China, Japan, and South Korea.

What are the emerging trends?

-> Emerging trends include miniaturization of components, MEMS-based oscillators, higher frequency stability requirements, integration with AI/ML systems, and development of ultra-low power consumption oscillators for next-generation automotive applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...