MARKET INSIGHTS

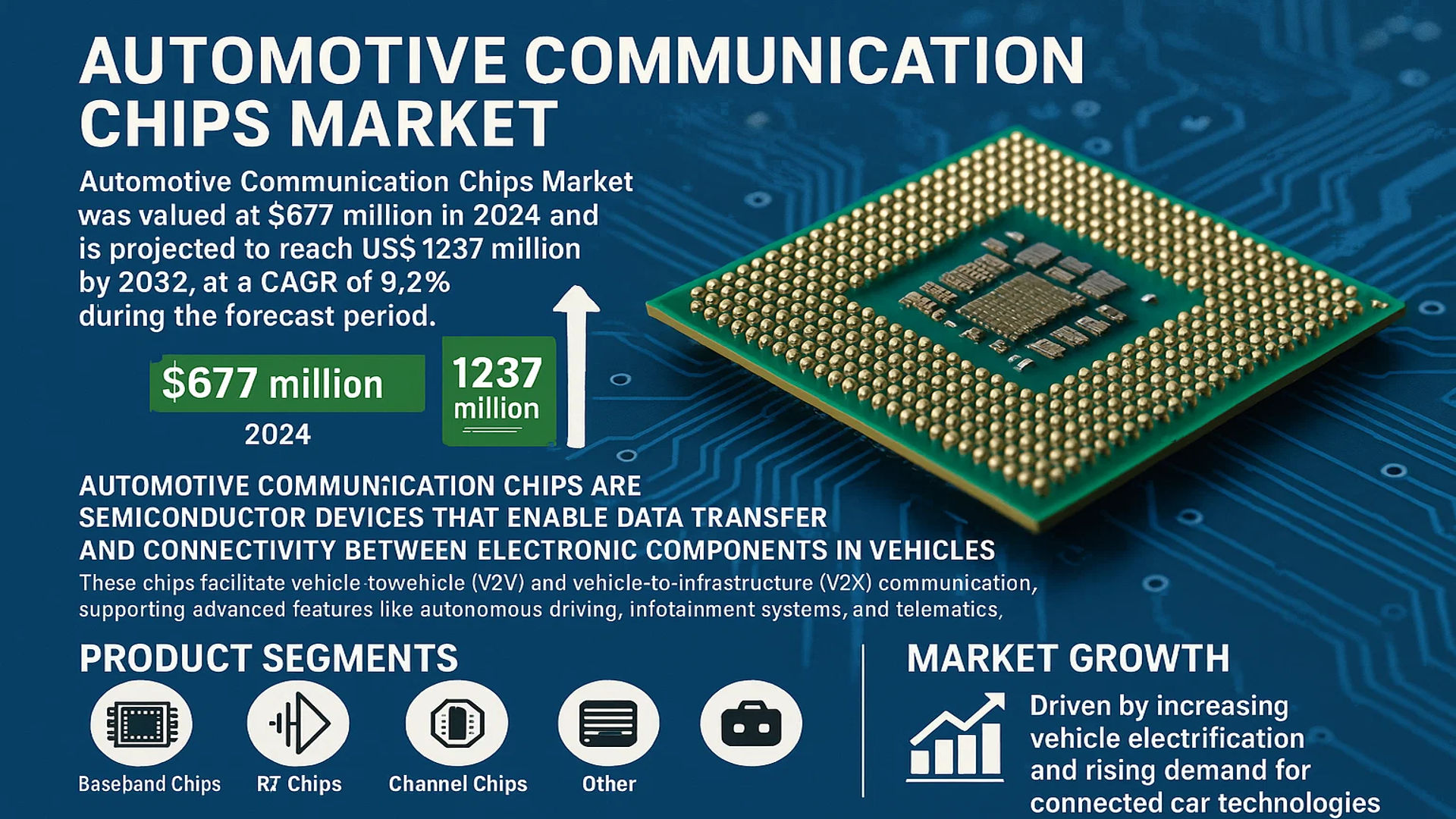

The global Automotive Communication Chips Market was valued at 677 million in 2024 and is projected to reach US$ 1237 million by 2032, at a CAGR of 9.2% during the forecast period.

Automotive communication chips are semiconductor devices that enable data transfer and connectivity between electronic components in vehicles. These chips facilitate vehicle-to-vehicle (V2V) and vehicle-to-infrastructure (V2X) communication, supporting advanced features like autonomous driving, infotainment systems, and telematics. The product segments include baseband chips, RF chips, channel chips, and other specialized communication solutions.

The market growth is driven by increasing vehicle electrification and rising demand for connected car technologies. While Asia dominates automobile production with 56% global share, North America and Europe are accelerating adoption of V2X technologies. Key industry players like Infineon Technologies and NXP Semiconductors are developing high-performance chipsets to meet the stringent automotive safety standards. Recent advancements in 5G and Ethernet backbone networks are further expanding market opportunities.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for Connected Vehicles to Fuel Market Growth

The automotive communication chips market is experiencing significant growth driven by the rapid adoption of connected vehicle technologies. Modern vehicles now incorporate advanced telematics, infotainment systems, and vehicle-to-everything (V2X) communication capabilities, all of which require specialized communication chips. The global connected car market is projected to grow at a compound annual growth rate of over 18%, creating substantial demand for automotive communication chips. These chips enable real-time data exchange between vehicles, infrastructure, and cloud platforms, enhancing safety features and enabling autonomous driving functionalities. The increasing consumer preference for connected features and government mandates for vehicle safety systems are accelerating this demand.

Transition Toward Autonomous Vehicles to Boost Market Expansion

The development of autonomous vehicle technology is creating strong demand for high-performance communication chips. Autonomous vehicles require sophisticated communication systems to process vast amounts of data from sensors, cameras, and LiDAR systems, all in real-time. The global autonomous vehicle market is expected to grow significantly, with Level 4 autonomous vehicles projected to account for substantial market share by 2030. This growth trajectory directly impacts the automotive communication chips market, as each autonomous vehicle requires multiple high-bandwidth communication chips to handle the data-intensive requirements of self-driving systems. Recent advancements in artificial intelligence processors and 5G connectivity are further enhancing the capabilities of these communication systems.

Moreover, strategic collaborations between automotive manufacturers and semiconductor companies are accelerating innovation in this space. Leading automakers are partnering with chip manufacturers to develop customized communication solutions that meet the specific requirements of next-generation vehicles.

➤ Recent vehicle launches from major automotive brands now typically include at least 50-100 semiconductor chips per vehicle, with premium models containing significantly more.

Furthermore, government initiatives supporting smart transportation infrastructure are creating additional demand for automotive communication technologies, as cities worldwide invest in intelligent traffic management systems that require vehicle connectivity.

MARKET CHALLENGES

Semiconductor Supply Chain Disruptions to Challenge Market Stability

The automotive communication chips market continues to face challenges from ongoing semiconductor supply chain disruptions. The global chip shortage that began in 2020 has particularly affected the automotive sector, forcing several manufacturers to temporarily halt production lines. While the industry is gradually recovering, lead times for certain semiconductor components remain extended, creating ongoing challenges for automakers. This situation is exacerbated by the increasing complexity of automotive communication chips, which require specialized manufacturing processes and materials. The transition to more advanced process nodes below 7nm presents additional production challenges and capacity constraints.

Other Challenges

Technical Complexity

Developing automotive-grade communication chips requires overcoming significant technical hurdles related to reliability, thermal management, and electromagnetic compatibility. These chips must operate flawlessly in harsh automotive environments while maintaining data integrity and security, raising development costs and time-to-market challenges.

Cybersecurity Concerns

As vehicles become more connected, cybersecurity becomes a critical challenge for communication chip manufacturers. Each new vehicle connectivity feature creates additional potential attack surfaces that must be secured, requiring continuous investment in hardware-based security features and authentication protocols.

MARKET RESTRAINTS

High Development Costs and Certification Requirements to Limit Market Expansion

The automotive communication chips market faces significant restraints from the high costs associated with chip development and stringent automotive certification requirements. Designing chips that meet automotive-grade reliability standards typically costs significantly more than developing consumer-grade semiconductors, with development cycles often exceeding 18-24 months. The automotive industry’s rigorous quality standards, including AEC-Q100 qualification and ISO 26262 functional safety certification, create substantial barriers to entry for new market participants. These requirements drive up research and development expenditures while extending time-to-market for new products.

Additionally, the rapid evolution of communication standards continues to challenge manufacturers. The transition from CAN and LIN buses to more advanced protocols like Automotive Ethernet requires continuous investment in new designs, while maintaining backward compatibility with legacy systems. This technological transition period creates additional development complexities and cost pressures for chip manufacturers.

MARKET OPPORTUNITIES

Emergence of Vehicle-to-Everything (V2X) Technology to Create New Growth Avenues

The development of V2X communication systems presents significant opportunities for automotive communication chip manufacturers. V2X technology enables vehicles to communicate with other vehicles, infrastructure, pedestrians, and networks, creating a new paradigm in transportation safety and efficiency. Government mandates in several countries are accelerating V2X adoption, with many regions expected to require V2X capabilities in new vehicles. This regulatory push is creating robust demand for specialized V2X communication chips that can support both short-range and cellular-based communication protocols.

Moreover, the integration of 5G technology into automotive communication systems is opening new opportunities. 5G enables ultra-reliable low-latency communication (URLLC) critical for autonomous driving applications, while also supporting enhanced mobile broadband for in-vehicle infotainment. Semiconductor companies are actively developing hybrid communication chips that combine multiple wireless technologies to address these diverse automotive connectivity requirements.

Strategic partnerships between automakers, tier-one suppliers, and semiconductor companies are driving innovation in this space. Recent collaborations have focused on developing integrated communication platforms that combine connectivity, processing, and security functions into optimized system-on-chip solutions for next-generation vehicles.

AUTOMOTIVE COMMUNICATION CHIPS MARKET TRENDS

Rising Demand for Connected Vehicles Fuels Market Expansion

The automotive communication chips market is experiencing significant growth, driven by increasing demand for connected vehicles and advanced driver-assistance systems (ADAS). With over 81.6 million vehicles produced globally in 2022, the integration of sophisticated communication technologies has become a priority for automakers. These chips enable vehicle-to-vehicle (V2V), vehicle-to-infrastructure (V2I), and vehicle-to-everything (V2X) communication, improving safety and efficiency on the road. As 5G networks expand, the automotive industry is leveraging high-speed, low-latency communication chips to support real-time data processing, enhancing navigation, autonomous driving, and infotainment features.

Other Trends

Shift Toward Electric and Autonomous Vehicles

The rapid adoption of electric vehicles (EVs) and autonomous vehicles (AVs) is accelerating the need for high-performance communication chips. EVs require seamless battery management and charging station connectivity, while AVs rely on complex sensor networks that demand ultra-reliable communication modules. With China contributing around 32% of global automobile production and leading EV adoption, Asia-Pacific remains a dominant region in this sector. Meanwhile, North America and Europe follow closely, with regulatory support and investments in autonomous mobility solutions further propelling market growth.

Emergence of Next-Generation Semiconductor Technologies

Technological advancements in semiconductor fabrication processes are reshaping the automotive communication chips market. Chip manufacturers are focusing on improving power efficiency, heat dissipation, and data throughput to meet the rigorous demands of modern vehicles. Companies like Infineon Technologies, NXP Semiconductors, and Renesas Electronics are developing system-on-chip (SoC) solutions with integrated AI processors, optimized for autonomous decision-making. Furthermore, the rise of edge computing in vehicles has encouraged innovation in RF and baseband chips, enabling faster in-car networking and cloud connectivity.

COMPETITIVE LANDSCAPE

Key Industry Players

Strategic Collaborations and Technological Advancements Drive Market Competition

The global automotive communication chips market is highly competitive, characterized by the presence of established semiconductor giants as well as specialized automotive electronics suppliers. Infineon Technologies and NXP Semiconductors dominate the landscape, collectively accounting for nearly 35% of the market share in 2024. Their leadership stems from comprehensive product portfolios covering CAN, LIN, Ethernet, and FlexRay protocols essential for modern vehicle networking.

Renesas Electronics and Texas Instruments maintain strong positions through continuous innovation in mixed-signal processing and power efficiency, which are increasingly critical for electric and autonomous vehicles. Both companies have significantly expanded their R&D budgets, with Renesas allocating over 15% of its annual revenue to automotive chip development.

Smaller but technologically agile players like Microchip Technology and onsemi are gaining traction by focusing on niche applications such as in-vehicle infotainment and advanced driver-assistance systems (ADAS). Microchip’s recent acquisition of a leading IoT communication specialist further strengthens its position in connected car solutions.

The competitive intensity is further heightened by vertical integration strategies adopted by automotive OEMs. Major automakers are increasingly partnering with chip manufacturers to develop custom solutions, as seen in STMicroelectronics’ collaboration with a leading German automaker for next-generation zone architecture controllers.

List of Key Automotive Communication Chips Manufacturers

- Infineon Technologies AG (Germany)

- NXP Semiconductors N.V. (Netherlands)

- Renesas Electronics Corporation (Japan)

- Texas Instruments Incorporated (U.S.)

- STMicroelectronics N.V. (Switzerland)

- onsemi (U.S.)

- Microchip Technology Inc. (U.S.)

- Micron Technology, Inc. (U.S.)

- Analog Devices, Inc. (U.S.)

Segment Analysis:

By Type

Baseband Chip Segment Leads the Market Owing to Rising Demand for Connected Vehicles

The market is segmented based on type into:

- Baseband Chip

- Subtypes: 4G/LTE, 5G, and others

- RF Chip

- Channel Chip

- Other

By Application

Passenger Car Segment Dominates Due to Higher Vehicle Production and IoT Integration

The market is segmented based on application into:

- Passenger Car

- Commercial Car

By Vehicle Connectivity

V2X Communication Segment Grows Rapidly with Smart City Initiatives

The market is segmented based on vehicle connectivity into:

- Vehicle-to-Vehicle (V2V)

- Vehicle-to-Infrastructure (V2I)

- Vehicle-to-Pedestrian (V2P)

- Vehicle-to-Grid (V2G)

By Communication Protocol

Ethernet Protocol Gains Traction for High-Speed Data Transmission in Modern Vehicles

The market is segmented based on communication protocol into:

- CAN (Controller Area Network)

- LIN (Local Interconnect Network)

- FlexRay

- Ethernet

- MOST

Regional Analysis: Automotive Communication Chips Market

Asia-Pacific

The Asia-Pacific region dominates the global automotive communication chips market, accounting for over 56% of total automobile production. China alone contributes approximately 32% of global vehicle manufacturing, creating massive demand for in-vehicle networking solutions. The region’s leadership stems from both domestic consumption and export-oriented manufacturing hubs in Japan (which exported 3.5 million vehicles in 2022) and South Korea. Local semiconductor manufacturers are aggressively developing cost-effective solutions for evolving vehicle architectures, particularly for electric vehicles which are growing at a 35% CAGR in China. However, the market faces challenges from geopolitical tensions affecting semiconductor supply chains and varying technology adoption rates across price segments.

North America

The North American market benefits from advanced automotive R&D ecosystems and stringent vehicle connectivity mandates. The U.S. accounts for 16% of global vehicle production, with premium OEMs driving demand for high-performance communication chips supporting 5G V2X and autonomous driving features. Regulatory pressure for standardized vehicle-to-everything (V2X) communication is accelerating adoption, with NHTSA considering mandate proposals. The region hosts key semiconductor innovators like Texas Instruments and Microchip Technology, who are developing specialized automotive-grade chips with functional safety certifications. However, cost sensitivity in mass-market segments limits penetration of advanced solutions compared to premium vehicles.

Europe

European automakers are at the forefront of implementing sophisticated in-vehicle networks, supported by 20% of global production and strong regulatory frameworks for connected mobility. The EU’s stringent automotive safety standards (ISO 26262) compel chip manufacturers like Infineon and STMicroelectronics to develop ASIL-certified communication solutions. Germany’s automotive industry – representing 30% of European production – is transitioning to zonal architectures requiring high-bandwidth Ethernet backbones. While technological sophistication is high, the market growth faces headwinds from economic uncertainties and complex multi-supplier integration challenges in next-generation vehicle platforms.

South America

The South American automotive communication chips market remains nascent but shows promise as regional production rebounds from economic volatility. Brazil leads with localized manufacturing operations from major OEMs, creating demand for basic CAN and LIN network solutions. Price sensitivity restricts adoption of advanced protocols, with most vehicles using legacy architectures. Recent trade agreements are facilitating technology transfers, particularly in Mexico which supplies the North American market. The lack of local semiconductor production creates complete import dependence, making the region vulnerable to global supply chain disruptions and currency fluctuations.

Middle East & Africa

This emerging market is witnessing gradual growth in automotive communication chip adoption, primarily driven by premium vehicle imports and localized assembly plants in countries like Turkey and South Africa. The absence of domestic semiconductor production and limited vehicle electrification creates a focus on aftermarket solutions for basic connectivity features. GCC countries are investing in smart city infrastructure that may accelerate V2X adoption. Market development is constrained by fragmented automotive standards across countries, though long-term potential exists with urbanization projects and growing middle-class vehicle ownership.

Report Scope

This market research report provides a comprehensive analysis of the global and regional Automotive Communication Chips markets, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global Automotive Communication Chips market was valued at USD 677 million in 2024 and is projected to reach USD 1,237 million by 2032, growing at a CAGR of 9.2%.

- Segmentation Analysis: Detailed breakdown by product type (Baseband Chip, RF Chip, Channel Chip, Others) and application (Passenger Cars, Commercial Vehicles) to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. Asia dominates with 56% of global automobile production.

- Competitive Landscape: Profiles of leading market participants including Infineon Technologies, NXP Semiconductors, Renesas Electronics, Texas Instruments, and STMicroelectronics, covering their market share and strategic developments.

- Technology Trends & Innovation: Assessment of emerging automotive communication technologies, integration with connected vehicle systems, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors including rising vehicle production, increasing demand for connected vehicles, and semiconductor supply chain challenges.

- Stakeholder Analysis: Insights for automotive OEMs, tier-1 suppliers, chip manufacturers, and investors regarding market opportunities and challenges.

The report employs primary and secondary research methods, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Automotive Communication Chips Market?

->Automotive Communication Chips Market was valued at 677 million in 2024 and is projected to reach US$ 1237 million by 2032, at a CAGR of 9.2% during the forecast period.

Which key companies operate in Global Automotive Communication Chips Market?

-> Key players include Infineon Technologies, NXP Semiconductors, Renesas Electronics, Texas Instruments, and STMicroelectronics, among others.

What are the key growth drivers?

-> Key growth drivers include rising vehicle production, increasing adoption of connected car technologies, and government mandates for vehicle safety features.

Which region dominates the market?

-> Asia-Pacific is the largest market, accounting for 56% of global vehicle production, with China being the world’s largest automobile manufacturer.

What are the emerging trends?

-> Emerging trends include development of high-speed communication chips for autonomous vehicles, integration of 5G connectivity, and increasing demand for electric vehicle communication systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...