Automotive AI Chip Market Insights

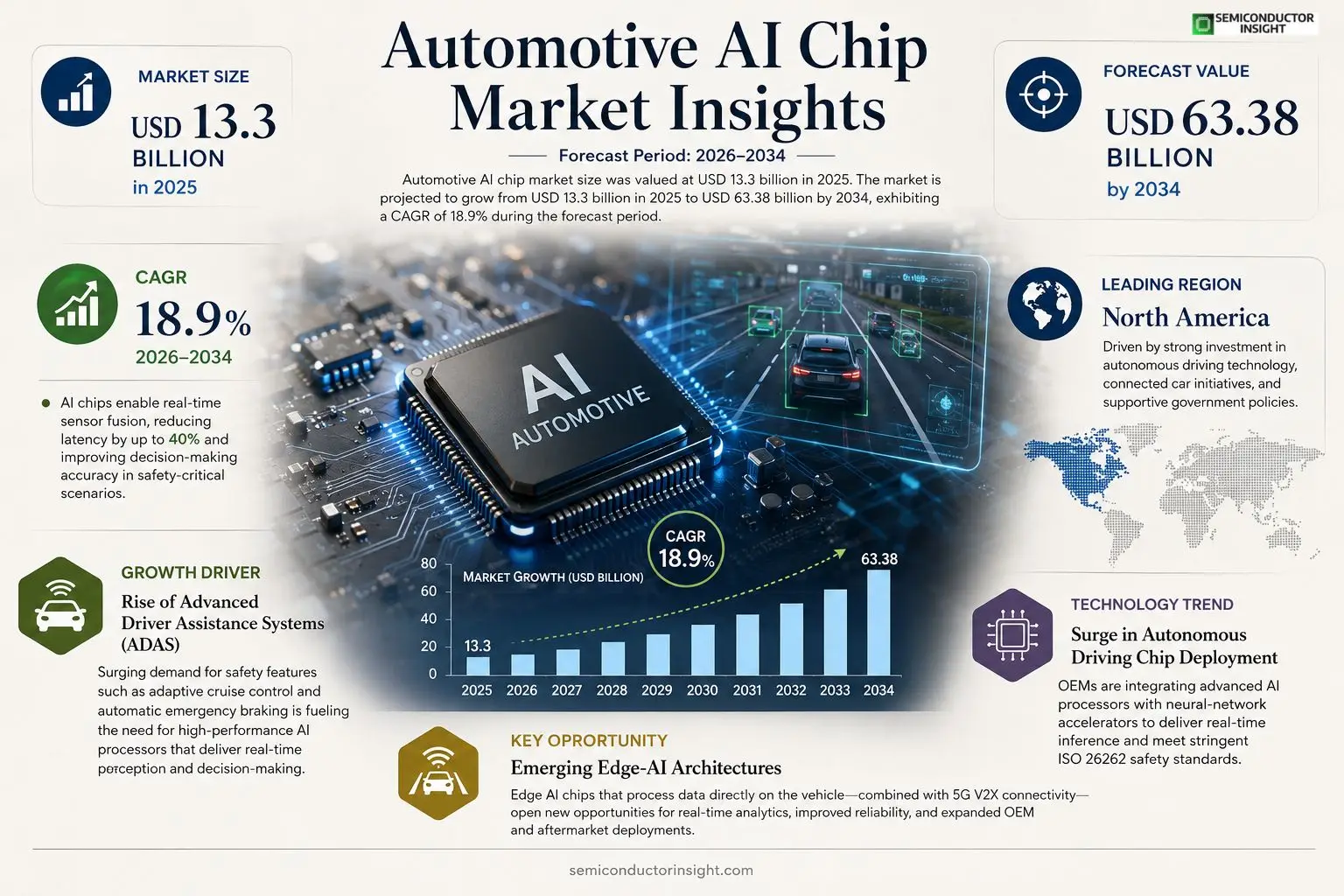

Automotive AI chip market size was valued at USD 13.3 billion in 2025.The market is projected to grow from USD 13.3 billion in 2025 to USD 63.38 billion by 2034, exhibiting a CAGR of 18.9% during the forecast period.

Automotive AI chips are high‑performance semiconductor devices engineered for on‑board artificial‑intelligence workloads such as perception, sensor fusion, path planning and advanced driver‑assistance systems (ADAS). These processors combine neural‑network accelerators, GPUs or dedicated ASICs that enable real‑time inference while complying with stringent automotive safety standards like ISO 26262.

The market is experiencing rapid growth because investment in autonomous‑vehicle research is soaring, demand for electric‑vehicle connectivity is rising, and regulators worldwide are tightening safety requirements.Hence major players,including NVIDIA, Qualcomm, Intel’s Mobileye and Samsung,are expanding their portfolios through strategic alliances.For instance, NVIDIA announced a partnership with Mercedes‑Benz in March 2024 to co‑develop next‑generation cockpit AI platforms.Furthermore, government subsidies for smart mobility projects across Europe and Asia are accelerating adoption of these chips.

MARKET DRIVERS

Rise of Advanced Driver Assistance Systems (ADAS)

The growing integration of ADAS features such as adaptive cruise control, lane‑keeping assist, and automatic emergency braking is creating a surge in demand for high‑performance AI processors. Automotive AI Chip Market players are benefiting from OEMs’ commitment to safer vehicles, driving investments in neural‑network accelerators that can process image and radar data in real time.

Electrification and Autonomous Vehicle Development

Electrified powertrains and Level‑3/4 autonomous prototypes require sophisticated on‑board computing to manage sensor fusion, path planning, and energy optimization. Automotive AI Chip Market growth is being propelled by the need for chips that deliver higher compute density while maintaining low power consumption.

➤ AI chips enable real‑time sensor fusion, reducing latency by up to 40% and improving decision‑making accuracy in safety‑critical scenarios.

Overall, the convergence of safety‑centric ADAS mandates and the push toward fully autonomous driving is establishing a robust foundation for sustained market expansion.

MARKET CHALLENGES

High Development Costs

Designing AI silicon for automotive applications involves extensive validation, functional safety certification, and long qualification cycles. These activities drive R&D expenses upward, creating a barrier for smaller entrants trying to compete in Automotive AI Chip Market.

Other Challenges

Supply Chain Constraints

Global semiconductor fab capacity remains tight, and the specialized processes required for automotive‑grade AI chips often compete with consumer‑electronics demand, leading to lead‑time extensions that can delay vehicle launch programs.

MARKET RESTRAINTS

Stringent Safety Regulations

Automotive standards such as ISO 26262 and UNECE R155 impose rigorous functional safety and cybersecurity requirements. Achieving compliance adds testing overhead and increases time‑to‑market for new AI chips, limiting rapid innovation cycles.

Manufacturers also face restrictions on the use of certain materials and processes, which can curtail the adoption of cutting‑edge semiconductor nodes in safety‑critical environments.

Furthermore, the need for long product life‑cycles,often exceeding a decade,means that chip designers must balance forward‑looking performance with legacy support, constraining flexible design choices.

MARKET OPPORTUNITIES

Emerging Edge‑AI Architectures

Edge‑computing models that process data directly on the vehicle without relying on cloud connectivity are gaining traction. This trend opens opportunities for AI chip vendors to deliver highly integrated SoCs that combine perception, planning, and control functions within a single package, reducing system cost and improving reliability.The rollout of 5G V2X (vehicle‑to‑everything) communication creates a new demand for AI chips capable of handling high‑bandwidth, low‑latency data streams. Companies that can embed AI inference engines optimized for 5G‑enabled traffic scenarios are likely to capture a sizable share of the evolving Automotive AI Chip Market.Lastly, the aftermarket segment,especially retrofitting older vehicle fleets with advanced driver assistance kits,offers a growing revenue stream. AI chipset solutions that are modular and scalable can be positioned for both OEM and aftermarket deployments, broadening market reach.

Automotive AI Chip Market Trends

Surge in Autonomous Driving Chip Deployment

Automotive AI Chip Market is witnessing a rapid acceleration as OEMs integrate advanced perception and decision‑making processors into new vehicle platforms. Recent collaborations between chip leaders and premium car manufacturers are cementing a wave of next‑generation cockpit and driver‑assistance solutions. These processors combine neural‑network accelerators with automotive‑grade GPUs, delivering real‑time inference while meeting ISO 26262 safety criteria. The shift from legacy microcontrollers toward dedicated AI silicon is driven by the need for higher bandwidth sensor fusion and low‑latency path planning, positioning the market at the core of autonomous driving development.

Other Trends

Integration with Electric Vehicle Connectivity

Electric vehicles increasingly rely on high‑speed data links for over‑the‑air updates, telematics and V2X communication. Embedding AI chips directly on the vehicle bus enables on‑board analytics for battery management, predictive maintenance and driver behavior modeling. By processing data locally, Automotive AI Chip Market supports reduced latency compared with cloud‑centric architectures, a critical factor for safety‑critical functions such as adaptive cruise control. Manufacturers are therefore standardizing AI‑enabled gateways that fuse power‑train telemetry with environmental perception, creating a seamless digital ecosystem across the vehicle lifecycle.

Regulatory Influence and Government Support

Regulators across Europe and Asia are tightening functional‑safety mandates, prompting automakers to adopt AI chips that can be validated against stringent compliance frameworks. Simultaneously, government incentive programs for smart mobility and low‑emission transports are subsidizing the deployment of AI‑driven driver assistance modules. This policy backdrop accelerates adoption rates within Automotive AI Chip Market, as suppliers align their roadmaps with upcoming certification milestones. The convergence of regulatory pressure and fiscal support not only de‑risks investment but also fosters a competitive ecosystem where innovation is rapidly translated into production‑ready silicon.

COMPETITIVE LANDSCAPE

Key Industry Players

Automotive AI Chip Market Overview

Automotive AI Chip Market is currently led by a handful of technology giants that combine deep learning acceleration with automotive‑grade safety compliance. NVIDIA, with its DRIVE platform, remains the dominant supplier for high‑performance GPU‑based inference engines, while Qualcomm’s Snapdragon Ride series provides integrated SoC solutions that balance power efficiency and compute density for ADAS and Level‑2‑3 autonomy. Intel’s Mobileye offers a differentiated vision‑centric approach through EyeQ ASICs, and Samsung contributes advanced memory‑centric AI processors that enable real‑time sensor fusion. These leaders benefit from extensive OEM partnerships,e.g., NVIDIA’s collaboration with Mercedes‑Benz and Qualcomm’s deals with Ford,creating a market structure where a few vertically integrated players capture the majority of volume and set de‑facto standards for safety certification.Beyond the headline names, a robust cohort of niche and regionally strong companies is expanding the competitive set. Renesas supplies automotive‑grade microcontrollers with embedded AI accelerators, while NXP focuses on scalable edge AI chips for infotainment and cockpit functions. Samsung’s System‑L integrates AI and high‑bandwidth memory for autonomous platforms. Graphcore delivers intelligence processing units (IPUs) optimized for sparse neural networks, and Huawei’s HiSilicon offers AI‑centric SoCs targeting the Chinese market. Additional contributors such as AMD, STMicroelectronics, Infineon, Texas Instruments, and ON Semiconductor provide specialized ASICs, DSPs, and mixed‑signal solutions that address specific sensor‑fusion or power‑budget niches, fostering a diversified ecosystem that mitigates reliance on a single supplier.

List of Key Automotive AI Chip Companies Profiled

- NVIDIA

- Qualcomm

- Intel (Mobileye)

- Samsung Electronics

- Renesas Electronics

- NXP Semiconductors

- Graphcore

- Huawei (HiSilicon)

- AMD

- STMicroelectronics

- Infineon Technologies

- Texas Instruments

- ON Semiconductor

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

ASIC drives the market with deep integration and power efficiency.

|

| By Application |

|

Advanced Driver Assistance Systems remain the primary catalyst for AI chip adoption.

|

| By End User |

|

OEMs drive strategic direction for AI chip integration.

|

| By Technology |

|

Edge Computing Solutions are favored for latency‑critical vehicular functions.

|

| By Vehicle Architecture |

|

Electric Vehicles offer a compelling platform for AI chip integration.

|

Regional Analysis: North America

North America

North America is witnessing rapid advancements in automotive AI chip technology, particularly in areas like neural processing units (NPUs) and specialized AI accelerators. Companies are focused on developing chips that can handle the computationally intensive tasks required for real-time decision-making in autonomous vehicles.

Collaboration between automotive manufacturers, technology providers, and semiconductor companies is a key trend. These partnerships are crucial for accelerating the development and deployment of Automotive AI Chips and integrating them seamlessly into vehicle platforms.

Government regulations related to autonomous driving and vehicle safety are significantly influencing the development and adoption of Automotive AI Chips. Compliance with evolving safety standards is a major focus for chip manufacturers.

Ensuring a robust and resilient supply chain for Automotive AI Chips is a critical challenge. Geopolitical factors and semiconductor shortages have highlighted the importance of diversifying sourcing and strengthening domestic manufacturing capabilities.

Europe

Europe demonstrates a strong commitment to developing a leading position in Automotive AI Chip Market. The region’s robust automotive industry, coupled with proactive government initiatives and significant R&D investments, creates a favorable ecosystem for innovation. European automakers are actively collaborating with semiconductor manufacturers and technology startups to integrate advanced AI capabilities into their vehicles. The focus in Europe is on developing energy-efficient AI chips that can meet the demands of electric and hybrid vehicles. A key driver for growth is the increasing adoption of ADAS features and the transition towards fully autonomous driving. The European Union’s regulatory framework, emphasizing safety and data privacy, is also shaping the development of Automotive AI Chips.

Asia-Pacific

Asia-Pacific is poised to become the largest market for Automotive AI Chips. Driven by the rapid growth of the automotive industry in countries like China, Japan, and South Korea, the demand for AI-powered vehicles is soaring. China, in particular, is investing heavily in autonomous driving technology and is emerging as a major center for Automotive AI Chip design and manufacturing. The region benefits from a well-established electronics manufacturing infrastructure and a large pool of skilled engineers. The focus in Asia-Pacific is on developing cost-effective AI chips that can cater to the needs of a wide range of vehicles, from mass-market cars to luxury models. The increasing adoption of electric vehicles and the growing demand for connected car services are also fueling the growth of Automotive AI Chip Market in the region.

South America

South America represents a growing but relatively nascent market for Automotive AI Chips. While the automotive industry in the region is still developing, there is increasing interest in incorporating AI-powered features into vehicles. The growth of the commercial vehicle segment and the rising demand for connected car solutions are expected to drive the adoption of Automotive AI Chips in South America. However, challenges such as limited R&D investment and a less mature automotive ecosystem may hinder the region’s growth in the short term. The increasing availability of affordable electric vehicles could also boost demand for these chips.

Middle East & Africa

The Middle East & Africa region is an emerging market with significant potential for Automotive AI Chips. The automotive industry in countries like the UAE, Saudi Arabia, and South Africa is experiencing steady growth, driven by increasing disposable incomes and infrastructure development. The demand for ADAS features and connected car services is also rising in the region. While the adoption of autonomous driving technology is still in its early stages, there is growing interest in integrating AI capabilities into vehicles. The region presents opportunities for Automotive AI Chip manufacturers to cater to the specific needs of the local market, such as developing chips that can withstand extreme temperatures and harsh road conditions.

Report Scope

This market research report provides a comprehensive analysis of the Automotive AI Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Automotive AI Chip Market?

-> Automotive AI Chip Market was valued at USD 13.3 billion in 2025 and is expected to reach USD 63.38 billion by 2034.

Which key companies operate in Automotive AI Chip Market?

-> Key players include NVIDIA, Qualcomm, Intel’s Mobileye, and Samsung, among others.

What are the key growth drivers?

-> Key growth drivers include surging investment in autonomous‑vehicle research, rising demand for electric‑vehicle connectivity, stricter safety regulations, and government subsidies for smart mobility projects in Europe and Asia.

Which region dominates the market?

-> Europe and Asia are leading regions, driven by strong regulatory support and substantial government subsidies.

What are the emerging trends?

-> Emerging trends include strategic alliances such as NVIDIA’s partnership with Mercedes‑Benz, increased integration of AI/IoT in vehicle platforms, and the development of dedicated ASICs for advanced driver‑assistance systems (ADAS).

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...