Market Insights

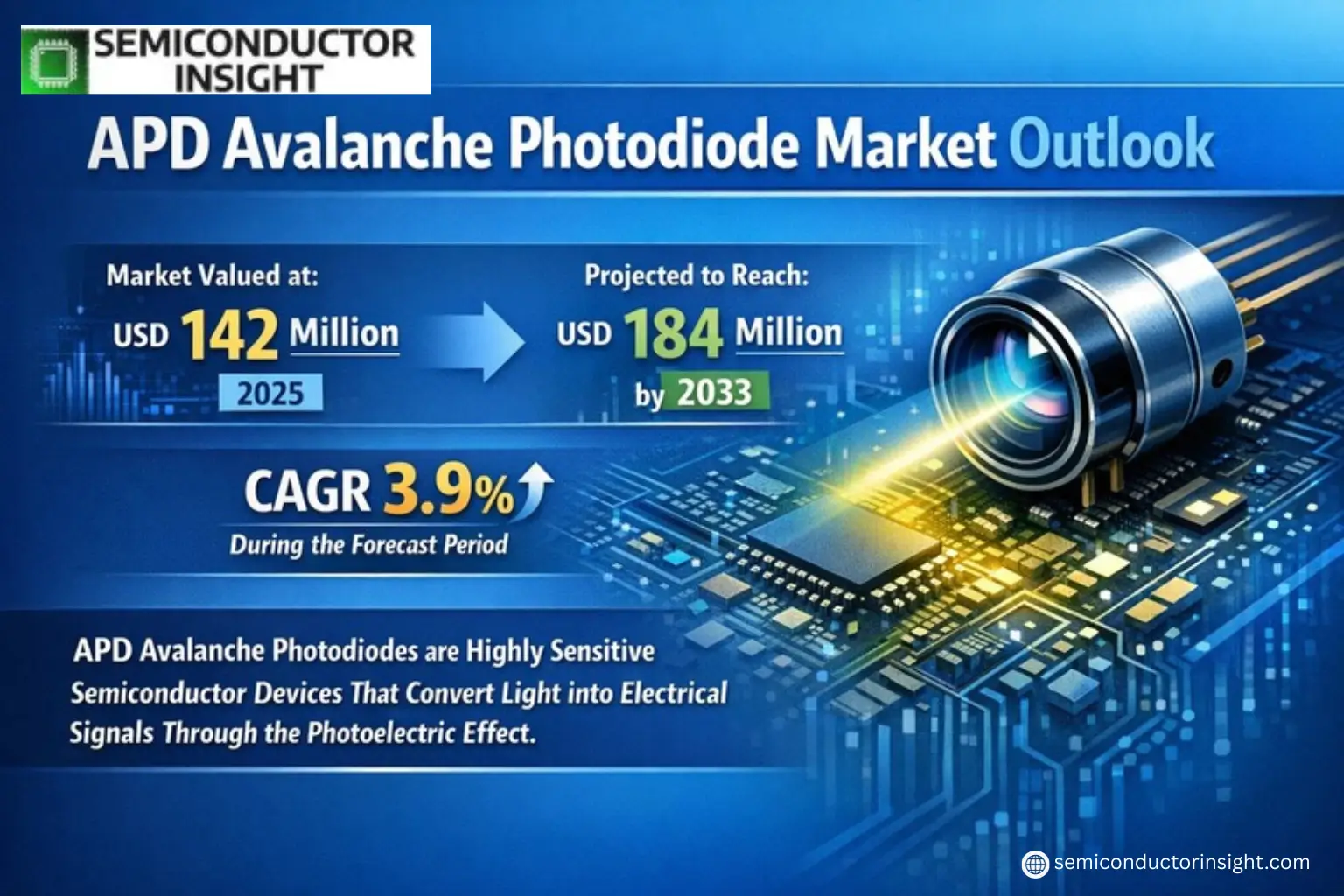

Global APD Avalanche Photodiode Market was valued at USD 142 million in 2025 and is projected to reach USD 184 million by 2033, at a CAGR of 3.9% during the forecast period.

APD Avalanche Photodiode (APDs) Market are highly sensitive semiconductor devices that convert light into electrical signals through the photoelectric effect. These components function as photodetectors with built-in gain via avalanche multiplication, making them the semiconductor equivalent of photomultiplier tubes. By applying a high reverse bias voltage, APDs achieve internal current amplification due to impact ionization. While traditional APDs have limitations, silicon-based variants utilize specialized doping and beveling techniques to sustain higher voltages before breakdown, enabling greater operational gain.

The market growth is driven by increasing demand for high-sensitivity optical detection across industries such as telecommunications, medical imaging, and autonomous mobility. Europe currently dominates with a 35% market share, followed by Japan and North America collectively holding over 45%. Silicon APDs lead product segmentation with over 50% adoption, while mobility applications represent the largest end-use sector. Key players like Hamamatsu, First Sensor, and Luna collectively control more than 45% of global supply

MARKET DRIVERS

Growing Demand in High-Speed Communication

APD Avalanche Photodiode Market is experiencing significant growth due to rising demand in high-speed optical communication networks. With data traffic increasing by approximately 30% annually, telecom operators are upgrading to next-generation systems requiring APD’s superior sensitivity.

Expansion of LiDAR Applications

Autonomous vehicles and industrial automation are driving adoption of LiDAR systems, where APD avalanche photodiodes serve as critical components. The automotive LiDAR market is projected to grow at over 20% CAGR through 2028.

Emerging quantum communication systems are creating new opportunities, with APDs being the detector of choice for single-photon detection applications.

MARKET CHALLENGES

High Development and Manufacturing Costs

The complex fabrication process of APD avalanche photodiodes results in production costs 3-5 times higher than standard photodiodes, limiting adoption in cost-sensitive applications.

Other Challenges

Thermal Management Requirements

APDs require precise temperature control systems to maintain optimal performance, adding complexity to system designs. Variations as small as 1°C can impact gain stability by up to 2%.

Competition from Alternative Technologies

Emerging technologies like silicon photomultipliers (SiPMs) are challenging APDs in certain applications, particularly where high gain and fast response are required.

MARKET RESTRAINTS

Supply Chain Constraints for Specialty Materials

APD Avalanche Photodiode Market faces constraints due to limited availability of high-purity III-V semiconductor materials. Current supply can only meet about 70% of projected demand through 2025, creating potential bottlenecks.

MARKET OPPORTUNITIES

Emerging Medical Imaging Applications

New generations of medical imaging equipment are incorporating APD avalanche photodiodes for their superior detection capabilities in PET scanners and other diagnostic systems. This segment is expected to grow at 15% annually over the next five years.

Advancements in Quantum Technologies

Quantum computing and quantum communication systems are creating new high-value applications for APD photodiodes, with the quantum technology market projected to exceed USD 2.5 billion by 2027.

APD Avalanche Photodiode Market Trends

Steady Market Growth Driven by Industrial and Mobility Applications

Global APD Avalanche Photodiode Market is projected to grow from USD 142 million in 2025 to USD 184 million by 2033, reflecting a 3.9% CAGR. This growth is primarily fueled by increasing demand in mobility and industrial applications, which collectively account for over 60% of market share. Silicon APDs dominate the product segment with 50% market penetration due to their cost-effectiveness and reliability in varied operating conditions.

Other Trends

Regional Market Concentration

Europe holds the largest share (35%) of the APD Avalanche Photodiode Market, followed by Japan and North America with a combined 45% share. This regional concentration reflects established semiconductor manufacturing ecosystems and strong R&D investments in photonics technology across these markets.

Technological Advancements in Noise Reduction

Manufacturers are focusing on improving quantum efficiency and reducing leakage current in APDs, with recent developments targeting excess noise factor (ENF) reduction. Leading companies like Hamamatsu and First-sensor are investing in alternative doping techniques to enhance gain capabilities while maintaining operational stability at higher voltages.

Other Trends

Consolidation Among Key Players

Three manufacturers control over 45% of the global APD Avalanche Photodiode Market, indicating high industry concentration. Recent mergers, such as Luna’s acquisition of Osi optoelectronics, demonstrate ongoing consolidation to strengthen technological capabilities and market reach in this specialized semiconductor segment.

Emerging Applications in Medical Imaging

While industrial and mobility remain dominant, medical applications are emerging as a growth frontier for APD technology. The ability to detect weak optical signals makes APD Avalanche Photodiodes increasingly valuable in diagnostic imaging systems, though this segment currently represents less than 15% of total market revenue.

COMPETITIVE LANDSCAPE

Key Industry Players

APD Avalanche Photodiode Market Dominated by Semiconductor Giants and Niche Specialists

Global APD Avalanche Photodiode Market is consolidated with the top three manufacturers – First-sensor, Hamamatsu Photonics, and Luna Innovations – collectively holding over 45% market share. Japanese and European players dominate production, leveraging advanced semiconductor fabrication capabilities. Hamamatsu leads in medical and industrial applications with its high-reliability Si-APD devices, while First-sensor specializes in automotive LiDAR solutions. The competitive landscape features technological differentiation in gain bandwidth products and custom wavelength configurations.

Emerging players like Kyosemi and Accelink are gaining traction with cost-competitive InGaAs APDs for telecommunications. Niche specialists such as Excelitas Technologies focus on military/aerospace applications with radiation-hardened designs. Regional leaders like NORINCO GROUP cater to domestic Chinese markets with government-backed semiconductor initiatives. The market sees increasing R&D investments for quantum sensing applications, with startups entering high-speed photon counting segments.

List of Key APD Avalanche Photodiode Companies Profiled

- First-sensor AG (Germany)

- Hamamatsu Photonics (Japan)

- KYOTO Semiconductor (Kyosemi) (Japan)

- Luna Innovations (USA)

- Excelitas Technologies (USA)

- OSI Optoelectronics (USA)

- Edmund Optics (USA)

- GCS (China)

- Accelink Technologies (China)

- NORINCO GROUP (China)

- Voxtel (USA)

- Photonis (France)

- Laser Components (Germany)

- Albis Optoelectronics (Switzerland)

- Raytheon Technologies (USA)

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Si-APD

|

| By Application |

|

Mobility

|

| By End User |

|

Automotive OEMs

|

| By Detection Range |

|

Medium Range

|

| By Gain Type |

|

Linear Mode

|

Regional Analysis: Global APD Avalanche Photodiode Market

The expanding 5G network rollout across North America significantly boosts demand for high-speed APD photodiodes in fiber optic communication systems. Telecom providers prioritize APDs for their superior performance in long-distance signal detection.

Military modernization programs drive adoption of APD sensors for night vision, threat detection, and secure communications. The region’s defense budget allocations ensure sustained demand for ruggedized avalanche photodiode solutions.

Leading medical device manufacturers incorporate APD technology into PET scanners and optical coherence tomography systems. The FDA’s supportive regulatory environment facilitates rapid adoption of new APD-based diagnostic tools.

North American autonomous vehicle initiatives create substantial opportunities for APD photodiodes in advanced driver-assistance systems. Investments from tech giants and automakers accelerate LiDAR sensor development using avalanche photodiode arrays.

Europe

Europe maintains strong positions in the APD avalanche photodiode market through its precision manufacturing capabilities and growing industrial automation sector. The region benefits from collaborative research initiatives between universities and photonics companies, particularly in Germany and France. Strict EU regulations on industrial safety and environmental monitoring drive demand for high-sensitivity APD sensors. The presence of specialized manufacturers like Hamamatsu Photonics and Excelitas Technologies supports the development of application-specific avalanche photodiodes.

Asia-Pacific

The Asia-Pacific region shows the fastest growth in APD photodiode adoption, fueled by expanding telecommunications networks and increasing defense expenditures. China’s Made in China 2025 initiative prioritizes domestic APD sensor production, while Japan maintains leadership in high-performance photodiode manufacturing. Emerging applications in consumer electronics and industrial automation create new opportunities across Southeast Asian markets.

South America

South America’s APD avalanche photodiode market grows steadily, with Brazil leading in oil & gas pipeline monitoring applications and Argentina developing astronomy research applications. Limited local manufacturing keeps the region dependent on imports, but increasing investments in scientific research infrastructure are creating niche demand for specialized photodiode solutions.

Middle East & Africa

The MEA region shows emerging potential in the APD photodiode market, particularly in oilfield monitoring and border security applications. UAE and Saudi Arabia invest in smart city projects incorporating APD-based sensors, while South Africa develops specialized photodiode applications for mineral exploration and astronomy research facilities.

Report Scope

This market research report provides a comprehensive analysis of the APD Avalanche Photodiode Market , covering the forecast period 2025–2033. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of APD Avalanche Photodiode Market?

-> APD Avalanche Photodiode Market was valued at USD 142 million in 2025 and is projected to reach USD 184 million by 2033, at a CAGR of 3.9% during the forecast period.

What is the growth rate of APD Avalanche Photodiode Market?

-> The market is projected to grow at a CAGR of 3.9% during the forecast period 2025-2033.

Which key companies operate in APD Avalanche Photodiode Market?

-> Key players include First-sensor, Hamamatsu, Luna, KYOTO(Kyosemi), Excelitas, and Osi optoelectronics, among others. Global top three manufacturers hold over 45% market share.

What are the key application areas?

-> The largest application is Mobility, followed by Industrial sectors. Other applications include Medical and various specialized uses.

Which region dominates the APD Avalanche Photodiode Market?

-> Europe is the largest market with 35% share, followed by Japan and North America which collectively hold over 45% market share.

What are the key product segments?

-> Si APD is the dominant product segment with over 50% market share, followed by InGaAs-APD and other specialized variants.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...