MARKET INSIGHTS

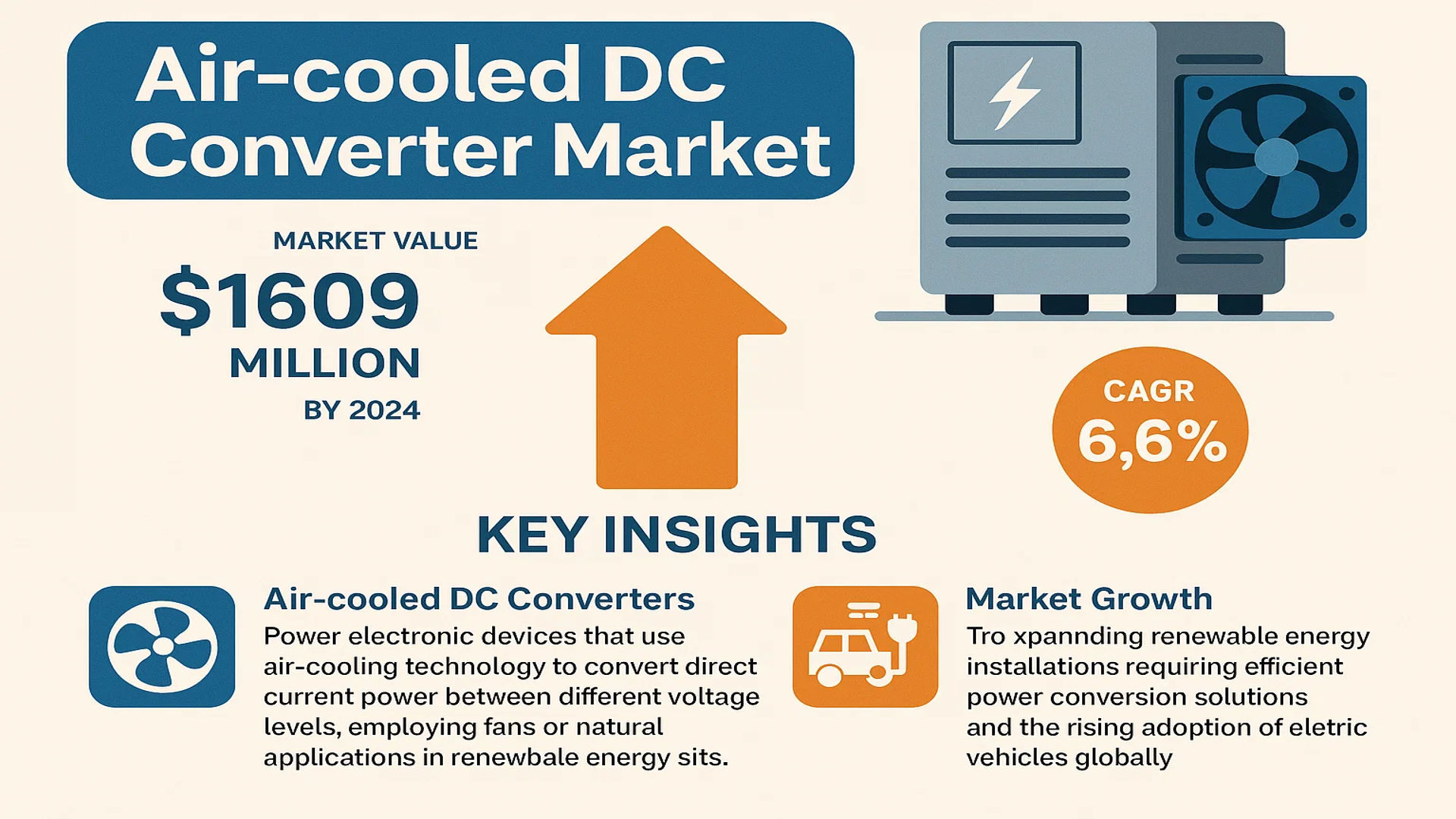

The global Air-cooled DC Converter market was valued at 1609 million in 2024 and is projected to reach US$ 2416 million by 2032, at a CAGR of 6.6% during the forecast period.

Air-cooled DC converters are power electronic devices that utilize air-cooling technology to convert direct current (DC) power between different voltage levels. These devices employ fans or natural convection for heat dissipation, eliminating the need for complex liquid cooling systems. Their simplified design offers higher reliability and lower maintenance costs compared to liquid-cooled alternatives. The technology finds extensive applications across renewable energy systems (solar/wind), electric vehicles, industrial power supplies, and telecommunications infrastructure, particularly in medium-to-low power scenarios.

The market growth is driven by expanding renewable energy installations, which require efficient power conversion solutions, and the rising adoption of electric vehicles globally. While North America maintains technological leadership, Asia-Pacific shows accelerated growth due to massive investments in green energy projects. Key industry players like Vitesco Technologies, Siemens, and Mitsubishi Electric are innovating compact, high-efficiency designs to address evolving sector requirements. The boost converter segment currently dominates applications, though buck converters are gaining traction in battery management systems.

MARKET DYNAMICS

MARKET DRIVERS

Expansion of Renewable Energy Infrastructure Boosts Demand for Air-cooled DC Converters

The global transition toward renewable energy solutions is a primary driver for the air-cooled DC converter market. Solar photovoltaic (PV) installations are projected to grow at over 8% annually through 2030, requiring efficient power conversion systems. Air-cooled solutions offer distinct advantages in solar applications because of their reliability in remote locations and minimal maintenance requirements. Unlike liquid-cooled systems, they eliminate risks associated with coolant leaks while providing adequate thermal management for mid-scale solar farms and commercial installations. The modular nature of these converters also simplifies capacity scaling as renewable projects expand.

Electric Vehicle Charging Infrastructure Development Accelerates Market Growth

Rapid deployment of electric vehicle (EV) fast-charging stations is creating sustained demand for robust DC power conversion systems. Air-cooled DC converters are increasingly favored for 50-150kW DC fast chargers due to their operational reliability and lower total cost of ownership. With governments worldwide mandating EV adoption targets, charger installations are expected to triple by 2028. The automotive industry’s shift toward 800V battery systems further amplifies requirements for voltage conversion solutions, presenting manufacturers with opportunities to develop next-generation air-cooled architectures capable of handling higher power densities efficiently.

Additionally, technological advancements are enhancing product capabilities:

➤ Recent innovations in gallium nitride (GaN) semiconductor technology have enabled 30% smaller converter footprints while maintaining thermal performance in air-cooled configurations.

Furthermore, the standardization of bi-directional charging capabilities creates additional market potential as vehicle-to-grid (V2G) applications gain traction globally.

MARKET RESTRAINTS

Thermal Limitations Hinder High-Power Applications

While air-cooled DC converters excel in mid-power applications, their inherent thermal constraints present challenges for high-density power conversion requirements. Applications exceeding 250kW typically require liquid cooling solutions, limiting market penetration in industrial and utility-scale implementations. Temperature sensitivity remains a critical concern, particularly in regions with ambient temperatures consistently above 40°C. This constraint affects reliability metrics, with some installations experiencing up to 15% reduced lifespan compared to liquid-cooled alternatives in extreme environments.

Other Restraints

Acoustic Noise Considerations

The operational noise from active cooling fans creates deployment challenges in noise-sensitive environments. Residential microgrid installations and urban charging stations frequently face regulatory noise limits between 45-55 dB, requiring additional acoustic engineering that increases unit costs by 8-12%.

Dust and Contaminant Sensitivity

Particle accumulation in air-cooled systems remains an operational challenge in industrial and desert environments. Regular maintenance intervals are typically 50% more frequent than liquid-cooled equivalents, impacting total cost calculations for operators.

MARKET CHALLENGES

Supply Chain Disruptions Impact Critical Component Availability

The semiconductor shortage continues to disproportionately affect power electronics manufacturers, with lead times for insulated-gate bipolar transistors (IGBTs) and power modules extending beyond 52 weeks in some cases. This constraint has forced converter manufacturers to maintain 6-9 months of inventory buffers, increasing working capital requirements by an average of 25%. The situation is compounded by geographical concentration of rare earth element production, with over 80% of permanent magnets for cooling fans sourced from limited regions.

Other Challenges

Standardization Fragmentation

Diverging regional standards for emissions, efficiency, and safety compliance require expensive product variants. The European Union’s updated EcoDesign regulations alone necessitated 15-20% component redesigns for many manufacturers.

Workforce Skill Gaps

The specialized knowledge required for high-frequency power electronics design remains scarce, with industry surveys indicating 40% of firms struggle to recruit qualified engineers for converter development teams.

MARKET OPPORTUNITIES

5G Infrastructure Rollout Creates New Application Verticals

Global 5G network expansion is driving unprecedented demand for distributed power solutions at telecom base stations. Air-cooled DC converters are particularly well-suited for these applications due to their compact form factors and resistance to temperature fluctuations. Telecom operators are prioritizing solutions with 97%+ efficiency ratings to minimize energy costs, creating opportunities for advanced topology designs. The transition to Open RAN architectures further expands market potential by decentralizing power infrastructure requirements across thousands of new deployment sites annually.

Additionally, technological convergence presents growth avenues:

➤ Integration of predictive maintenance algorithms using IoT sensors can reduce field failures by up to 30%, significantly improving value propositions for mission-critical installations.

Emerging markets also show strong potential, with microgrid and rural electrification projects increasingly specifying air-cooled solutions for their balance of performance and maintainability in resource-constrained environments.

AIR-COOLED DC CONVERTER MARKET TRENDS

Renewable Energy Integration Fuels Adoption of Air-cooled DC Converters

The global shift toward renewable energy sources is significantly driving the demand for air-cooled DC converters. These converters play a crucial role in efficiently managing power conversion in solar and wind energy systems, where heat dissipation must be optimized without complex cooling systems. The market for renewable energy-integrated DC converters is projected to grow at a compound annual growth rate (CAGR) of around 7.2% from 2024 to 2032. The preference for air-cooled converters in medium-power applications stems from their cost-effectiveness, low maintenance, and compact design, making them ideal for decentralized renewable installations.

Other Trends

Electrification of Transportation

The rise of electric vehicles (EVs) and hybrid vehicles is propelling the adoption of air-cooled DC converters in automotive applications. These converters are increasingly utilized in onboard charging systems and auxiliary power modules due to their reliability and ease of integration. Industry forecasts suggest that the EV segment will account for nearly 25% of the total air-cooled DC converter market by 2030, spurred by government incentives and stringent emissions regulations. Additionally, advancements in power electronics are enabling higher efficiency in converting DC power between different voltage levels, further boosting market expansion.

Telecommunications Infrastructure Expansion

The expansion of 5G and hyperscale data centers is creating heightened demand for efficient power conversion solutions. Air-cooled DC converters are widely preferred in communication base stations due to their ability to operate in harsh environments with minimal maintenance. The telecommunications sector is estimated to contribute over 18% of the global market revenue by 2025, driven by increasing data consumption and investments in next-gen network infrastructure. Moreover, compact and modular designs in air-cooled solutions are reducing footprint requirements, making them highly suitable for urban deployments with space constraints.

COMPETITIVE LANDSCAPE

Key Industry Players

Global Manufacturers Compete on Innovation and Efficiency in Air-cooled DC Converters

The global air-cooled DC converter market features a highly competitive environment, with established industrial powerhouses and specialized manufacturers vying for market share. Vitesco Technologies and Siemens currently lead the industry, leveraging their extensive experience in power electronics and global distribution networks. Their dominance stems from comprehensive product lines that serve multiple voltage ranges and applications across renewable energy, automotive, and industrial sectors.

Meanwhile, Hopewind and ROHM Semiconductor have emerged as strong regional contenders, particularly in the Asia-Pacific market. These companies have gained traction through competitive pricing strategies and customized solutions for solar power applications. Their success demonstrates how mid-sized players can carve out significant niches in this growing $1.6 billion market.

The competitive intensity continues to increase as manufacturers invest in thermal management technologies and compact designs. Mitsubishi Electric recently launched its next-generation series with 15% improved efficiency, while Fuji Electric expanded its modular converter line for electric vehicle charging stations. Such product innovations represent critical differentiators in an industry where reliability and energy efficiency directly impact customer purchasing decisions.

Partnership strategies are also reshaping the competitive dynamics. Bosch has formed alliances with renewable energy providers, while GE collaborates with automotive OEMs to develop integrated power solutions. These strategic moves help manufacturers secure long-term contracts and stabilize revenue streams despite market fluctuations.

List of Key Air-cooled DC Converter Manufacturers

- Vitesco Technologies (Germany)

- Siemens (Germany)

- Hopewind (China)

- ROHM Semiconductor (Japan)

- Mitsubishi Electric (Japan)

- Fuji Electric (Japan)

- Bosch (Germany)

- Premium PSU (U.S.)

- XP Power (UK)

- GE (U.S.)

- Wakefield Thermal (U.S.)

- Tame-Power (Germany)

- Toshiba (Japan)

- Infineon (Germany)

- Danfoss (Denmark)

Segment Analysis:

By Type

Boost Converter Segment Leads the Market Due to High Efficiency in Power Conversion

The market is segmented based on type into:

- Boost Converter

- Buck Converter

- Boost-Boost Converter

By Application

Automotive Industry Segment Dominates Due to Growing EV Adoption and Power Management Needs

The market is segmented based on application into:

- Communications Industry

- Electronics Industry

- Transportation Industry

- Automotive Industry

By Cooling Method

Forced Air Cooling Segment Holds Major Share Due to Better Thermal Management

The market is segmented based on cooling method into:

- Natural Convection Cooling

- Forced Air Cooling

By Power Range

Medium Power Segment Leads as It Meets Most Industrial Application Requirements

The market is segmented based on power range into:

- Low Power

- Medium Power

- High Power

Regional Analysis: Air-cooled DC Converter Market

Asia-Pacific

The Asia-Pacific region dominates the global air-cooled DC converter market, driven by China‘s rapid industrialization and increasing investments in renewable energy infrastructure. Countries like India and Japan are also contributing significantly due to expanding telecom networks and automotive electrification initiatives. The region benefits from cost-effective manufacturing capabilities and a strong presence of local players like Hopewind and Toshiba, which cater to both domestic and export demands. While the adoption of advanced power electronics is accelerating, price sensitivity remains a key consideration for buyers in emerging markets.

North America

With stringent energy efficiency standards and growing EV adoption, North America represents a high-value market for air-cooled DC converters. The U.S. accounts for over 70% of regional demand, supported by federal incentives for clean energy projects and 5G infrastructure expansion. Major players like GE and XP Power focus on innovative cooling technologies to meet industrial and telecom sector requirements. Canada’s focus on sustainable power solutions further complements market growth, though competition from liquid-cooled alternatives persists in high-power applications.

Europe

Environmental regulations and the push for carbon neutrality are shaping Europe’s air-cooled DC converter landscape. Germany leads in industrial applications, while the UK and France show strong demand for converters in renewable energy systems. EU directives on energy efficiency drive innovation among manufacturers like Siemens and Bosch. However, the market faces challenges from space constraints in urban installations where compact, high-efficiency designs are prioritized. The region’s mature manufacturing base ensures quality but increases price pressures from Asian competitors.

Middle East & Africa

This emerging market benefits from telecom tower expansions and off-grid power projects across GCC countries. Saudi Arabia and the UAE lead in adopting air-cooled solutions for oil & gas infrastructure due to their reliability in harsh environments. While investments in data centers and solar farms create opportunities, the market growth is tempered by budget constraints in African nations and preference for cheaper alternatives. Local partnerships with global firms like Mitsubishi Electric are key to technology transfer.

South America

Brazil and Argentina show moderate but steady growth, primarily in industrial and transportation sectors. The market is characterized by delayed technology adoption due to economic instability, though renewable energy projects are gradually increasing converter demand. Local manufacturers compete with Chinese imports on price, while multinationals focus on high-end applications in mining and utilities. Infrastructure challenges and volatile currencies remain barriers to rapid market expansion.

Report Scope

This market research report provides a comprehensive analysis of the Global Air-cooled DC Converter Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The global market was valued at USD 1,609 million in 2024 and is projected to reach USD 2,416 million by 2032, growing at a CAGR of 6.6%.

- Segmentation Analysis: Detailed breakdown by product type (Boost Converter, Buck Converter, Boost-boost Converter), application (Communications, Electronics, Transportation, Automotive), and end-user industry to identify high-growth segments.

- Regional Outlook: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa. The U.S. and China are key growth markets.

- Competitive Landscape: Profiles of leading market participants, including Vitesco Technologies, Siemens, Bosch, Mitsubishi Electric, and Fuji Electric, with analysis of their market share, product portfolios, and strategic initiatives.

- Technology Trends & Innovation: Assessment of emerging technologies in power electronics, thermal management solutions, and efficiency improvements in DC conversion systems.

- Market Drivers & Restraints: Evaluation of factors such as renewable energy adoption, EV market growth, and industrial automation demand, along with challenges in thermal management and high-power applications.

- Stakeholder Analysis: Strategic insights for component suppliers, OEMs, system integrators, and investors regarding market opportunities and competitive positioning.

The report employs both primary and secondary research methodologies, including interviews with industry experts and analysis of verified market data, to ensure accuracy and reliability.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global Air-cooled DC Converter Market?

-> Air-cooled DC Converter market was valued at 1609 million in 2024 and is projected to reach US$ 2416 million by 2032, at a CAGR of 6.6% during the forecast period.

Which key companies operate in this market?

-> Key players include Vitesco Technologies, Siemens, Bosch, Mitsubishi Electric, Fuji Electric, ROHM Semiconductor, and Infineon, among others.

What are the key growth drivers?

-> Key growth drivers include increasing renewable energy adoption, growth in electric vehicles, expansion of telecom infrastructure, and industrial automation trends.

Which region dominates the market?

-> Asia-Pacific leads in market share due to rapid industrialization, while North America shows strong growth in EV and renewable energy applications.

What are the emerging trends?

-> Emerging trends include higher efficiency designs, integration with smart grid systems, and development of compact, high-power density converters.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...