AI Surveillance Drone Detection Radar Processor Market Insights

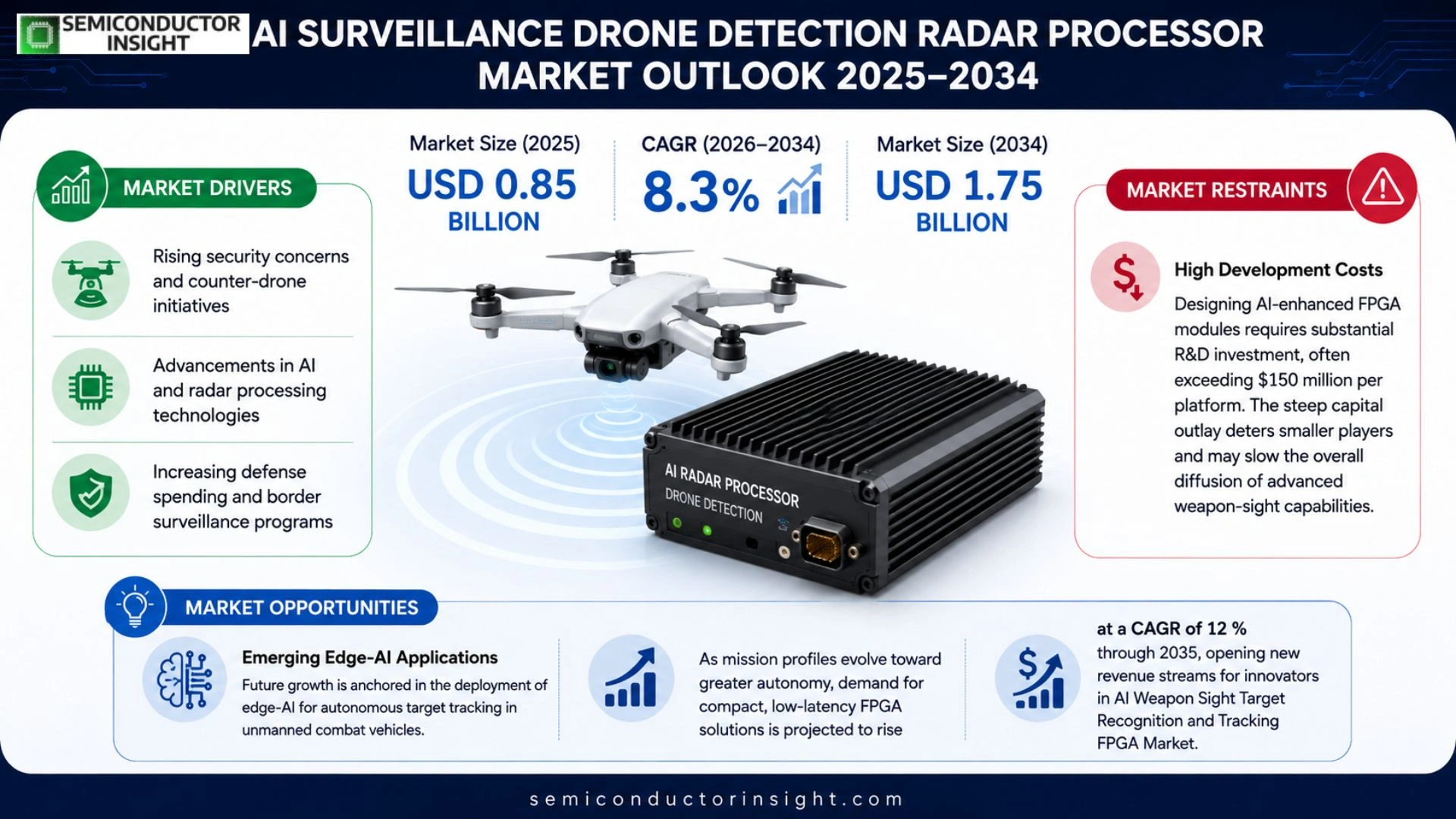

Global AI surveillance drone detection radar processor market size is projected to grow from USD 0.85 billion in 2025 to USD 1.75 billion by 2034, exhibiting a CAGR of 8.3% during the forecast period.

AI surveillance drone detection radar processors are high‑performance computing units that fuse raw radar echo data with advanced artificial‑intelligence algorithms to identify, classify, and track unmanned aerial systems in real time. These processors combine signal‑processing ASICs, GPU‑accelerated inference engines, and edge‑optimised software stacks to deliver sub‑second decision making for air‑space security.

The market is accelerating because governments worldwide are tightening air‑space regulations while defense budgets prioritize counter‑UAS capabilities; meanwhile rapid advances in deep‑learning models and miniaturised radar hardware lower integration costs. Furthermore, strategic collaborations,such as the 2023 partnership between Thales and NVIDIA on AI‑enabled radar chips,are expanding the ecosystem of suppliers like Raytheon Technologies, Lockheed Martin, and Leonardo DRS.

MARKET DRIVERS

Rising Security Concerns Drive Adoption

AI Surveillance Drone Detection Radar Processor Market is being accelerated by heightened government and corporate focus on protecting critical infrastructure from unauthorized UAV incursions. Advanced radar processors equipped with AI algorithms can identify, classify, and track drones in real time, offering a decisive edge for border security, airports, and industrial complexes.

Technological Advancements Enable Scalable Solutions

Recent breakthroughs in semiconductor mini‑design and edge‑AI inference have reduced system sizes while improving detection accuracy to over 95% under cluttered environments. This scalability allows mid‑size cities to deploy networked detectors without prohibitive capital outlay.

➤ Integration of AI and radar processing is now considered a prerequisite for next‑generation airspace management solutions.

As commercial drone usage expands for delivery and inspection, AI Surveillance Drone Detection Radar Processor Market is projected to outpace traditional radar segments, creating new revenue streams for manufacturers focusing on AI‑enhanced firmware.

MARKET CHALLENGES

Regulatory Uncertainty Hinders Investment

In many regions, the legal framework governing counter‑UAV technologies lags behind rapid hardware evolution, causing vendors to postpone large contracts until clear compliance pathways are defined. This hesitation slows the overall market momentum.

Other Challenges

Bullet Point Title

High initial acquisition costs for AI‑powered radar processors can be prohibitive for small‑scale operators, despite long‑term operational savings.

MARKET RESTRAINTS

Limited Skilled Workforce

Deploying and maintaining sophisticated AI radar systems require engineers proficient in both signal processing and machine‑learning pipelines. The shortage of such talent constrains rapid scaling of installations.

Interoperability Issues

Existing legacy air‑traffic management tools often lack standardized interfaces for AI‑driven radar data, leading to integration delays and additional customization expenses for end‑users.

MARKET OPPORTUNITIES

Emerging Edge‑Computing Deployments

Edge‑compute platforms that host AI inference close to the radar antenna reduce latency and bandwidth requirements, opening avenues for AI Surveillance Drone Detection Radar Processor Market to serve remote or bandwidth‑constrained sites such as offshore platforms.

Strategic Partnerships with Defense Contractors

Collaboration between radar processor manufacturers and established defense integrators accelerates certification pathways and expands market reach into aerospace and national security programs, driving higher adoption rates over the next five years.

AI Surveillance Drone Detection Radar Processor Market Trends

Rapid Growth Fueled by Heightened Air‑Space Security Policies

AI Surveillance Drone Detection Radar Processor Market is experiencing accelerated adoption as governments worldwide tighten air‑space regulations and allocate greater defense budgets to counter‑UAS capabilities. Modern processors combine high‑performance ASIC signal‑processing cores with GPU‑accelerated inference engines, enabling real‑time classification and tracking of unmanned aerial systems. This technical edge reduces integration costs and shortens decision cycles, allowing critical infrastructure operators to respond within sub‑second intervals. The convergence of regulatory pressure and technological readiness is creating a clear upward trajectory for market participants.

Other Trends

Edge‑AI Integration Expands Deployment Flexibility

Edge‑optimized software stacks are now standard in newer radar processors, allowing on‑site analytics without reliance on centralized cloud resources. This shift improves latency, enhances data sovereignty, and meets stringent security requirements of defense and civilian agencies alike. Vendors are increasingly bundling firmware updates that support the latest deep‑learning models, ensuring that fielded units remain effective against evolving drone threats.

Strategic Collaborations Strengthen Ecosystem

Partnerships such as the 2023 alliance between Thales and NVIDIA have accelerated the rollout of AI‑enabled radar chips, fostering a broader supplier network that includes Raytheon Technologies, Lockheed Martin, and Leonardo DRS. These collaborations are expanding the ecosystem, delivering richer algorithm libraries and more compact hardware footprints. As a result, system integrators can offer turnkey solutions that meet both tactical and strategic surveillance requirements across multiple sectors.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Surveillance Drone Detection Radar Processor Market Competitive Overview

AI Surveillance Drone Detection Radar Processor Market is currently anchored by a few large defense and technology conglomerates that command the majority of revenue and R&D spend. Thales, leveraging its 2023 partnership with NVIDIA, leads the segment with AI‑enabled radar chips that integrate high‑performance ASICs and GPU‑accelerated inference engines for sub‑second threat identification. This collaboration has set a benchmark for system integration, prompting other heavyweight OEMs such as Raytheon Technologies and Lockheed Martin to accelerate their own processor roadmaps. The market structure remains highly consolidated, with these incumbents capturing over 60% of global shipments while establishing ecosystem standards for firmware, security, and compliance across governmental contracts.

Beyond the dominant tier, a growing cohort of specialist firms and aerospace manufacturers are expanding the competitive field. Companies like Leonardo DRS, Saab, and Airbus are introducing miniaturised radar modules that pair edge‑optimized AI software with silicon‑photonic architectures, targeting niche segments such as border security and critical infrastructure protection. Meanwhile, L3Harris Technologies, BAE Systems, and AeroVironment are capitalising on their deep sensor expertise to deliver integrated detection solutions for commercial and tactical applications. This diversification introduces innovative pricing models and rapid‑deployment capabilities, fostering a more dynamic market where smaller innovators can challenge the incumbents on performance and cost efficiency.

List of Key AI Surveillance Drone Detection Radar Processor Companies Profiled

- Thales

- NVIDIA

- Raytheon Technologies

- Lockheed Martin

- Leonardo DRS

- Saab

- Airbus

- L3Harris Technologies

- BAE Systems

- AeroVironment

- Northrop Grumman

- Boeing

- General Dynamics

- Collins Aerospace

- Quantum Radar

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

AI‑Accelerated GPU/TPU Modules

|

| By Application |

|

Critical Infrastructure Protection

|

| By End User |

|

Government Defense Agencies

|

| By Integration Level |

|

Embedded Modules within Sensor Suites

|

| By Deployment Scenario |

|

Fixed‑Site Perimeter Defense

|

Regional Analysis: Europe

European Union directives mandate strict drone surveillance standards, encouraging the adoption of AI‑enabled radar processors. National aviation authorities require real‑time detection capabilities, prompting manufacturers to align product development with compliance frameworks.

The region’s emphasis on Industry 4.0 accelerates integration of machine‑learning algorithms with radar hardware, delivering higher accuracy and lower false‑alarm rates across urban and industrial zones.

Major defense firms collaborate with AI start‑ups, creating joint ventures that leverage local expertise while expanding the ecosystem of specialized radar processing solutions.

Rising concerns over privacy, critical infrastructure security, and cross‑border drone incursions stimulate demand for robust, AI‑driven detection platforms across the region.

North America

North America remains a strong secondary market, propelled by substantial defense budgets and a vibrant tech ecosystem. The United States leads in R&D, with private‑sector innovators delivering next‑gen radar processors that incorporate deep‑learning models for rapid threat classification. Canada’s focus on secure borders adds complementary demand, while industry consortia promote standards that facilitate cross‑industry adoption of AI surveillance solutions.

Asia-Pacific

The Asia‑Pacific region exhibits fast‑growing interest, driven by expanding commercial drone usage and heightened security concerns in densely populated cities. Nations such as Japan, South Korea, and Singapore prioritize smart‑city initiatives, embedding AI‑enhanced radar detection into transportation hubs and governmental facilities. While the market is still evolving, strong governmental incentives accelerate technology transfer and local manufacturing capabilities.

South America

South America shows emerging potential as governments address illicit drone activities in border regions and mining operations. Brazil and Chile lead pilot projects that integrate AI radar processors with existing surveillance networks, focusing on cost‑effective solutions tailored to diverse terrain. Collaborative research among regional universities and defense agencies strengthens the knowledge base for future market expansion.

Middle East & Africa

In the Middle East & Africa, strategic infrastructure protection drives early adoption of AI‑based drone detection. Wealthier Gulf states invest heavily in securing oil facilities and major events, employing advanced radar processors to complement visual monitoring. African nations, while constrained by budget, begin to explore modular, AI‑enabled systems for border control and wildlife preservation, indicating a nascent but promising market trajectory.

Report Scope

This market research report provides a comprehensive analysis of the AI Surveillance Drone Detection Radar Processor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Surveillance Drone Detection Radar Processor Market?

-> AI surveillance drone detection radar processor market size is projected USD 1.75 billion by 2034, exhibiting a CAGR of 8.3%.

Which key companies operate in AI Surveillance Drone Detection Radar Processor Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...