AI Smart Home Hub Processor Market Insights

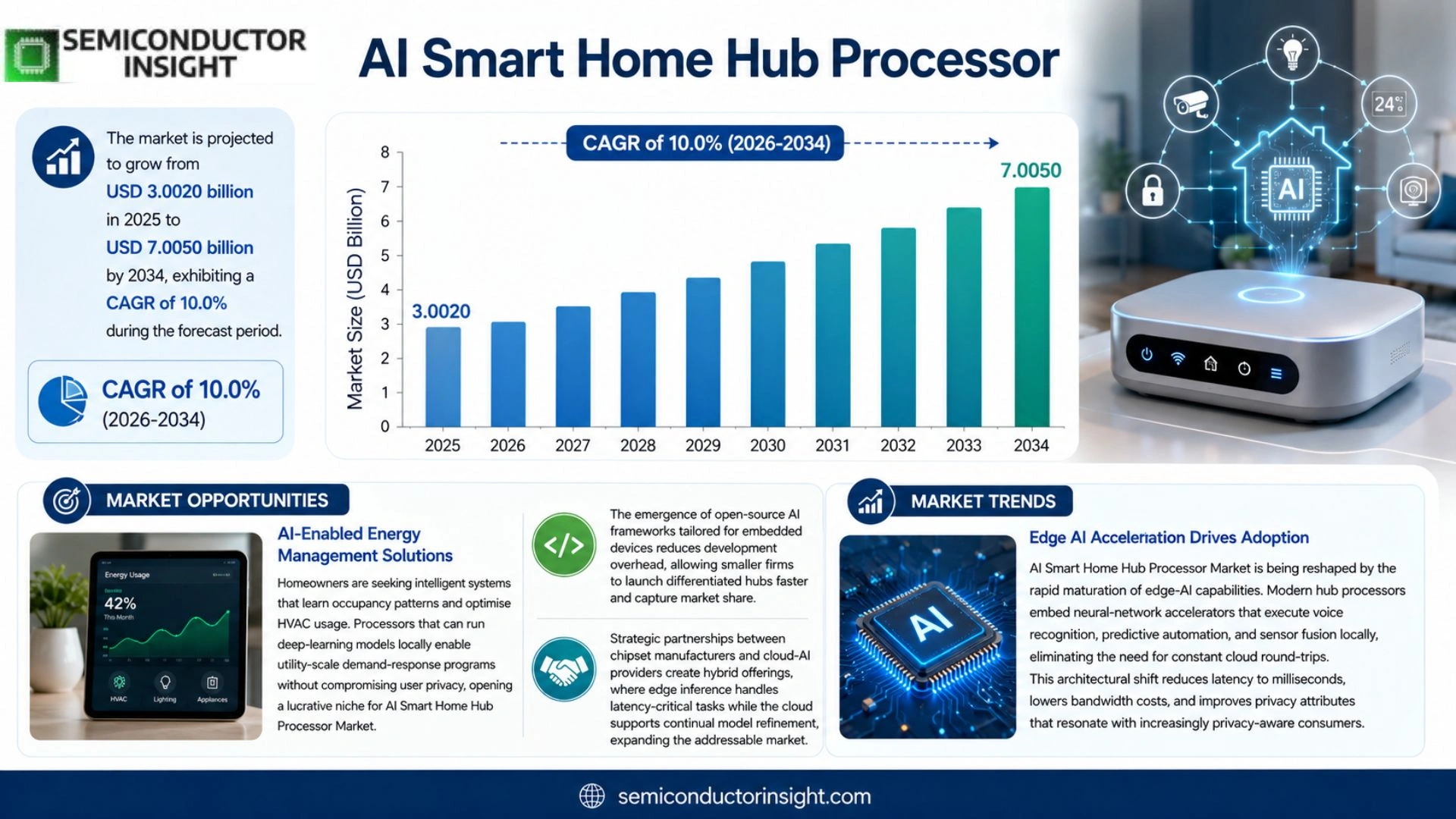

Global AI Smart Home Hub Processor market size is projected to grow from USD 3.0020 billion in 2025 to USD 7.0050 billion by 2034, exhibiting a CAGR of 10.0% during the forecast period.

AI Smart Home Hub Processors are specialized micro‑processors that embed artificial‑intelligence accelerators and low‑power cores to enable on‑device voice recognition, predictive automation, and seamless coordination of IoT appliances within residential environments.

The market is accelerating due to rising consumer adoption of connected home ecosystems, increasing demand for edge‑AI performance that reduces latency and bandwidth costs, and strategic collaborations such as Qualcomm’s partnership with Amazon announced in March 2024 to co‑develop next‑generation hub chips.

MARKET DRIVERS

Edge‑AI Integration in Home Devices

The proliferation of on‑device AI chips enables real‑time voice recognition, gesture control, and predictive lighting without relying on cloud latency. Manufacturers are therefore prioritising processors that combine low power consumption with high inference throughput, a trend that directly fuels the growth of AI Smart Home Hub Processor Market.

Consumer Demand for Seamless Interoperability

Homeowners increasingly expect a single hub to coordinate security cameras, thermostats, and entertainment systems. Unified platforms that support multiple wireless standards (Matter, Thread, Zigbee) are driving suppliers to embed versatile AI cores, accelerating market adoption.

➤ “By 2028, edge AI processors will power over 70% of new smart‑home hubs, reducing cloud reliance and enhancing privacy.”

In parallel, the rise of subscription‑based AI services for energy optimization and health monitoring creates recurring revenue streams, encouraging OEMs to invest in advanced processors that can host these services locally.

MARKET CHALLENGES

Design Complexity and Firmware Fragmentation

Integrating heterogeneous AI workloads alongside legacy communication stacks demands sophisticated PCB layouts and rigorous testing. Development cycles are lengthening, and smaller vendors struggle to keep pace with rapid firmware updates.

Other Challenges

Security Assurance

Ensuring end‑to‑end encryption while supporting OTA updates adds layers of validation, raising certification costs and potentially slowing time‑to‑market.

MARKET RESTRAINTS

High Cost of Advanced Silicon

The latest AI accelerators command premium pricing, which can push the overall bill of materials beyond the willingness‑to‑pay threshold for mid‑range smart‑home devices. Cost‑sensitive segments therefore remain reliant on older, less capable processors.

Supply‑chain bottlenecks for specialized substrates and packaging technologies further constrain volume availability, limiting the ability of manufacturers to scale production quickly.

Regulatory hurdles related to data privacy and electromagnetic compliance add additional layers of approval, elongating product launch timelines.

MARKET OPPORTUNITIES

AI‑Enabled Energy Management Solutions

Homeowners are seeking intelligent systems that learn occupancy patterns and optimise HVAC usage. Processors that can run deep‑learning models locally enable utility‑scale demand‑response programs without compromising user privacy, opening a lucrative niche for AI Smart Home Hub Processor Market.

The emergence of open‑source AI frameworks tailored for embedded devices reduces development overhead, allowing smaller firms to launch differentiated hubs faster and capture market share.

Strategic partnerships between chipset manufacturers and cloud‑AI providers create hybrid offerings, where edge inference handles latency‑critical tasks while the cloud supports continual model refinement, expanding the addressable market.

AI Smart Home Hub Processor Market Trends

Edge AI Acceleration Drives Adoption

AI Smart Home Hub Processor Market is being reshaped by the rapid maturation of edge‑AI capabilities. Modern hub processors embed neural‑network accelerators that execute voice recognition, predictive automation, and sensor fusion locally, eliminating the need for constant cloud round‑trips. This architectural shift reduces latency to milliseconds, lowers bandwidth costs, and improves privacy,attributes that resonate with increasingly privacy‑aware consumers. At the same time, power‑efficient designs enable continuous operation on low‑voltage platforms, supporting longer device lifecycles and smaller form factors. As homeowners integrate more connected appliances, the demand for processors that can coordinate dozens of protocols while maintaining real‑time responsiveness is rising sharply. Industry analysts observe that the convergence of on‑device AI performance and energy efficiency is the primary catalyst behind current procurement decisions across OEMs and system integrators.

Other Trends

Strategic Partnerships Expand Ecosystem

Collaborations between semiconductor leaders and cloud service providers are accelerating ecosystem maturity. Notable joint efforts, such as the 2024 partnership announced by Qualcomm and Amazon, focus on co‑developing next‑generation hub chips that blend custom AI cores with seamless access to voice‑assistant services. MediaTek’s alliance with leading smart‑home platform vendors enables a shared SDK that simplifies integration of third‑party devices, while Google’s Tensor portfolio continues to embed advanced machine‑learning models directly into hub silicon. These partnerships reduce time‑to‑market for new products and create standardized interfaces, which in turn lower integration costs for device manufacturers. The resulting network effect encourages a broader range of consumer electronics to adopt AI‑enhanced hub processors, reinforcing the market’s upward trajectory.

Emerging Competitive Landscape

Competition is intensifying as established chipmakers and emerging startups vie for differentiated feature sets. Companies are investing heavily in proprietary AI kernels, security enclaves, and multi‑protocol radios to differentiate their offerings. Apple’s recent integration of custom‑designed processors into its HomePod line illustrates a trend toward tightly controlled hardware‑software stacks, while smaller firms are leveraging open‑source AI frameworks to accelerate development cycles. Market participants are also focusing on modular architectures that allow OEMs to scale performance across product tiers without redesigning the entire hardware platform. Analysts anticipate that this blend of strategic collaboration and fierce innovation will drive continued diversification of solutions, ensuring that AI Smart Home Hub Processor Market remains dynamic and responsive to evolving consumer expectations.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Smart Home Hub Processor Market Competitive Overview

AI Smart Home Hub Processor market is anchored by a handful of semiconductor leaders that combine advanced edge‑AI accelerators with low‑power system‑on‑chip designs. Qualcomm, leveraging its Snapdragon and Cloud‑AI platforms, has secured a prominent position through a strategic partnership with Amazon announced in March 2024, targeting next‑generation hub chips that integrate voice‑first capabilities and on‑device inference. This alliance exemplifies the consolidation trend where large integrated device manufacturers collaborate with cloud service providers to deliver differentiated solutions. Meanwhile, MediaTek’s Dimensity series and Google’s Tensor SoC extend the competitive landscape by offering cost‑effective, AI‑optimized processors that enable manufacturers of mid‑range smart hubs to embed sophisticated automation without escalating bill‑of‑materials. The market structure reflects a tiered dynamic: a core of well‑capitalized firms dominate high‑performance segments, while a broader set of niche players service specialized or price‑sensitive applications.

Beyond the dominant tier, several companies are carving out meaningful niches. Apple’s custom‑designed silicon, although primarily focused on its HomePod ecosystem, underscores the importance of tightly integrated hardware‑software stacks for premium user experiences. Samsung Electronics and NXP Semiconductors provide mixed‑signal and connectivity‑centric solutions that complement AI cores, catering to OEMs seeking modular architectures. Intel and AMD are re‑orienting their product lines toward edge AI, delivering Xeon‑based and Ryzen‑derived processors that prioritize security and scalability for enterprise‑grade smart home hubs. Emerging contributors such as STMicroelectronics, Texas Instruments, Huawei, Alibaba Cloud, LG Electronics, and Broadcom diversify the supply chain with specialized sensor interfaces, power‑management ICs, and AI‑enhanced networking chips, reinforcing a competitive ecosystem that encourages rapid innovation and price competition.

List of Key AI Smart Home Hub Processor Companies Profiled

- Qualcomm

- MediaTek

- Google (Tensor)

- Apple

- Samsung Electronics

- NXP Semiconductors

- Intel

- AMD

- STMicroelectronics

- Texas Instruments

- Huawei

- Alibaba Cloud

- LG Electronics

- Broadcom

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Edge‑AI Processors

|

| By Application |

|

Home Security

|

| By End User |

|

Tech‑Savvy Families

|

Regional Analysis: AI Smart Home Hub Processor Market

North America’s R&D hubs, centered in Silicon Valley and Boston, foster breakthrough AI algorithms that enhance hub processor efficiency. Companies prioritize low‑power neural accelerators, enabling always‑on voice assistants and real‑time environmental sensing. Collaborative research with universities accelerates adoption of next‑gen machine‑learning models, ensuring that regional products remain at the forefront of functionality and energy optimization.

The region’s integrated supply chain links design houses, foundries, and test facilities under a single geographic umbrella. Proximity to leading semiconductor fabs shortens time‑to‑market for new processor nodes, while robust logistics networks ensure rapid component delivery. This cohesion reduces lead times and production costs, granting manufacturers flexibility to scale volumes in response to shifting consumer trends.

Regulatory frameworks in the United States emphasize data security and interoperability, encouraging manufacturers to embed privacy‑by‑design principles in hub processors. Standards such as Matter and Thread receive strong endorsement, facilitating cross‑brand compatibility. These policies not only protect consumers but also create a predictable environment for innovators to introduce advanced AI features without legal ambiguity.

Consumer readiness for AI‑driven home automation is highest in North America, with households increasingly adopting smart speakers, thermostats, and security cameras. The confluence of disposable income and tech‑savvy demographics accelerates demand for sophisticated hub processors capable of local AI inference. This heightened adoption fuels continuous feedback loops that inform product refinements and drive iterative enhancements.

Europe

Europe remains a significant contributor to AI Smart Home Hub Processor Market, distinguished by its emphasis on sustainability and stringent data‑protection regulations. European manufacturers prioritize energy‑efficient designs, aligning processor development with EU green‑tech directives. Collaborative initiatives across the EU, such as the Horizon Europe program, fund joint research projects that explore edge‑AI capabilities and low‑latency networking. While consumer adoption lags slightly behind North America, the region’s strong focus on privacy, standards compliance, and eco‑friendly solutions cultivates a niche market for premium smart home hubs that cater to environmentally conscious consumers and enterprise‑level building management systems.

Asia‑Pacific

The Asia‑Pacific region is emerging as a dynamic arena for AI Smart Home Hub Processor growth, propelled by rapid urbanization and a burgeoning middle class eager for connected living. Countries like China, Japan, and South Korea host extensive semiconductor manufacturing bases, enabling cost‑effective production of AI‑optimized processors. Local OEMs are integrating voice‑activated assistants and intelligent lighting controls into affordable home devices, expanding market reach. Government incentives for smart city initiatives further stimulate demand for integrated hub solutions that support edge‑AI processing and seamless IoT interoperability. Although regulatory landscapes vary, the region’s scale‑driven manufacturing capacity and consumer appetite position it as a critical growth engine for the market.

South America

South America shows steady progress in AI Smart Home Hub Processor Market, driven largely by Brazil and Mexico’s expanding digital infrastructure. Increasing broadband penetration and rising consumer awareness of smart‑home conveniences are encouraging adoption of AI‑enabled hubs. Regional manufacturers are focusing on cost‑efficient processor designs that balance performance with affordability, catering to price‑sensitive markets. Partnerships with global chip suppliers facilitate technology transfer, enhancing local production capabilities. While regulatory frameworks are still evolving, emerging standards around data security are beginning to shape product development, ensuring that future offerings meet both consumer expectations and compliance requirements.

Middle East & Africa

The Middle East & Africa region presents a nascent yet promising landscape for AI Smart Home Hub Processor Market. Wealthier Gulf states invest heavily in smart‑city projects, creating demand for high‑performance hub processors that can manage complex AI workloads locally. In contrast, African nations are witnessing gradual adoption as mobile broadband expands and affordable smart devices become more accessible. Regional distributors are collaborating with international chip makers to introduce processors that support multilingual voice assistants and robust security protocols suitable for diverse market conditions. Although overall market size remains modest, the combination of government‑driven smart‑infrastructure initiatives and growing consumer curiosity signals a trajectory of incremental growth.

Report Scope

This market research report provides a comprehensive analysis of the AI Smart Home Hub Processor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Smart Home Hub Processor Market?

-> AI Smart Home Hub Processor Market was valued at USD 3.20 billion in 2025 and is expected to reach USD 7.50 billion by 2034.

Which key companies operate in AI Smart Home Hub Processor Market?

-> Key players include MediaTek, Google (Tensor), Apple, and Qualcomm, among others.

What are the key growth drivers?

-> Key growth drivers include rising consumer adoption of connected home ecosystems, increasing demand for edge‑AI performance that reduces latency and bandwidth costs, and strategic collaborations such as Qualcomm’s partnership with Amazon.

Which region dominates the market?

-> The market is globally dispersed, with strong activity in North America, Europe, and Asia‑Pacific, where the majority of chipset development and consumer adoption occurs.

What are the emerging trends?

-> Emerging trends include on‑device voice recognition, predictive automation, and the integration of AI accelerators in low‑power micro‑processors for enhanced edge computing capabilities.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...