AI Ship Autonomous Navigation Radar Processor Market Insights

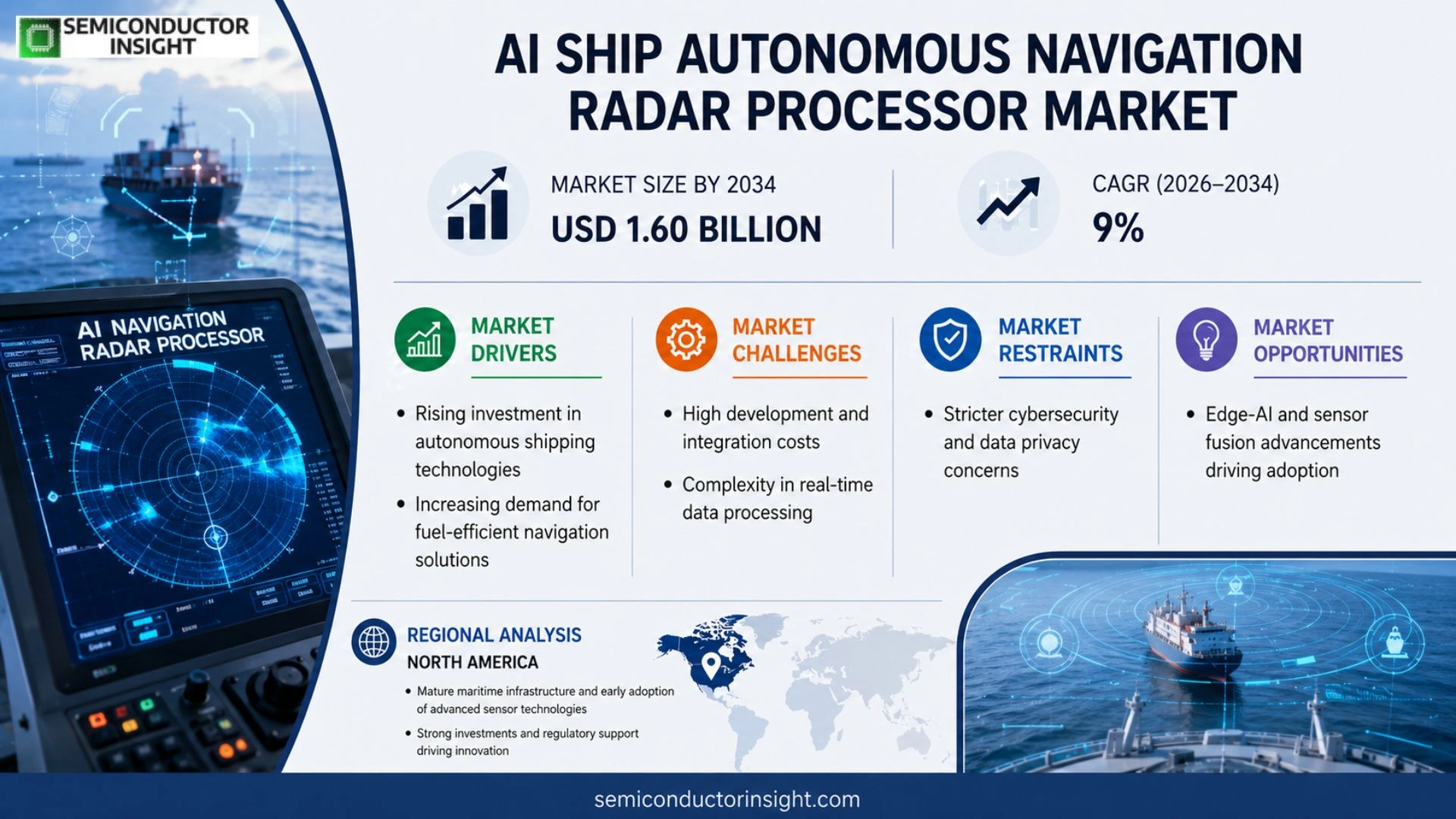

Global AI Ship Autonomous Navigation Radar Processor market size is projected to grow from USD 0.70 billion in 2025 to USD 1.60 billion by 2034, exhibiting a CAGR of 9 % during the forecast period.

AI Ship Autonomous Navigation Radar Processors are high‑performance computing units that fuse radar sensor data with artificial‑intelligence algorithms to enable precise vessel positioning, collision avoidance, and route optimization under diverse maritime conditions.

The market is experiencing rapid growth because of rising investment in autonomous shipping technologies, stricter safety regulations, and increasing demand for fuel‑efficient navigation solutions.

Furthermore, advancements such as edge‑AI integration and real‑time sensor fusion are accelerating adoption.

MARKET DRIVERS

Growing Adoption of Autonomous Vessels

AI Ship Autonomous Navigation Radar Processor Market is being propelled by the rising demand for fully autonomous cargo ships, which promise up to a 20% reduction in fuel consumption and a 30% decrease in crew‑related costs. Shipping companies are investing heavily in integrated radar processing solutions that can fuse sensor data with machine‑learning algorithms for real‑time route optimization.

Regulatory Incentives for Safety Enhancements

International maritime regulators are introducing tighter safety standards that require advanced collision‑avoidance capabilities. This regulatory pressure creates a favorable environment for vendors offering AI‑driven radar processors capable of detecting small objects at ranges exceeding 10 nm, thereby enhancing compliance and reducing insurance premiums.

➤ “Integrating AI with radar data has cut decision latency from 250 ms to under 50 ms, a critical factor for high‑speed autonomous navigation.”

Furthermore, the surge in smart‑port initiatives is driving the need for interoperable navigation systems. Operators are seeking processors that can seamlessly exchange data with shore‑based traffic‑management platforms, positioning AI Ship Autonomous Navigation Radar Processor Market for sustained double‑digit growth through 2032.

MARKET CHALLENGES

High Initial Capital Expenditure

Deploying AI‑enabled radar processors requires substantial upfront investment in hardware upgrades and software integration, which deters smaller fleet owners. The average cost of a complete autonomous navigation suite can exceed $2 million per vessel, limiting rapid market penetration.

Other Challenges

Data Quality and Sensor Fusion

Accurate AI decision‑making depends on high‑quality sensor inputs. In harsh marine environments, radar signal degradation and electromagnetic interference can compromise data fidelity, necessitating robust preprocessing algorithms that increase system complexity.

Cybersecurity concerns also loom large, as the increased connectivity of autonomous navigation systems presents new attack vectors. Companies must invest in end‑to‑end encryption and continuous threat monitoring, further elevating operational costs.

MARKET RESTRAINTS

Limited Skilled Workforce

Implementing and maintaining AI radar processors requires engineers proficient in both maritime systems and advanced machine learning. The global shortage of such dual‑skill talent creates a bottleneck that slows deployment timelines and raises labor expenses.

The pace of standardization for autonomous navigation protocols remains uneven across regions. Without a unified framework, shipbuilders face divergent certification requirements, hampering economies of scale.

In addition, legacy vessel fleets lack the structural accommodations needed for modern radar arrays, making retrofitting both technically challenging and economically unattractive for many operators.

MARKET OPPORTUNITIES

Expansion into Emerging Trade Lanes

Rapid growth in Asian and African maritime corridors opens new avenues for AI‑based radar processors. Operators targeting these routes anticipate a 15% increase in cargo volume, creating demand for navigation systems that can handle higher traffic density and variable weather conditions.

Partnerships between technology firms and shipyards are fostering modular processor designs that can be scaled across vessel sizes, from offshore supply vessels to ultra‑large container ships. This modularity reduces customization costs and accelerates time‑to‑market.

Finally, advances in edge‑computing hardware are enabling higher‑resolution radar analytics with lower power consumption, positioning AI Ship Autonomous Navigation Radar Processor Market to capture a larger share of the next generation of smart maritime logistics.

AI Ship Autonomous Navigation Radar Processor Market Trends

Accelerated Adoption Driven by Regulatory Pressure

AI Ship Autonomous Navigation Radar Processor Market is experiencing a pronounced surge as maritime operators respond to tighter safety mandates and heightened scrutiny of autonomous vessel performance. Governments worldwide have introduced stricter certification standards for unmanned navigation, prompting ship owners to invest in radar processors capable of delivering deterministic collision‑avoidance outcomes. Concurrently, fuel‑efficiency targets are pushing fleets toward AI‑enhanced route optimization, which directly reduces operational costs while meeting emissions commitments. These regulatory and economic drivers together create a fertile environment for advanced radar processing units that fuse high‑resolution sensor streams with sophisticated machine‑learning models, offering real‑time situational awareness across variable sea states.

Other Trends

Edge‑AI Integration Advances

Edge‑AI integration represents the next evolution in AI Ship Autonomous Navigation Radar Processor Market, enabling processors to execute inference locally on the vessel rather than relying on shore‑based cloud resources. By embedding low‑latency neural accelerators within the radar module, manufacturers achieve sub‑millisecond decision cycles essential for high‑speed maneuvering in congested waterways. Real‑time sensor fusion frameworks now combine radar returns with lidar and AIS data, delivering a unified maritime picture that reduces false positives and improves obstacle classification. This architectural shift not only enhances reliability under intermittent connectivity but also aligns with industry calls for robust, self‑contained autonomy solutions.

Strategic Partnerships Bolster Portfolio Expansion

Key players such as Kongsberg Maritime, Raytheon Technologies, Thales Group, and Siemens are deepening their market presence through collaborative ventures that blend domain expertise with cutting‑edge AI research. Joint development programs focus on reducing processing latency, expanding algorithmic robustness against adverse weather, and simplifying integration with existing bridge systems. These alliances accelerate product rollouts by leveraging shared test‑bed vessels and joint certification pathways, thereby shortening time‑to‑market for next‑generation radar processors. As a result, AI Ship Autonomous Navigation Radar Processor Market is poised for sustained growth, driven by coordinated innovation and a collective commitment to safe, efficient autonomous shipping.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Ship Autonomous Navigation Radar Processor Market Competitive Overview

AI Ship Autonomous Navigation Radar Processor Market is presently shaped by a handful of large, vertically integrated firms that combine advanced radar hardware with cutting‑edge artificial‑intelligence algorithms. Kongsberg Maritime, Raytheon Technologies, Thales Group and Siemens dominate the segment, leveraging extensive defense and maritime portfolios to secure multi‑billion‑dollar contracts with global shipowners and classification societies. Their offerings emphasize low‑latency sensor fusion, edge‑AI processing and compliance with emerging safety regulations, allowing them to capture the majority of the projected USD 1.60 billion market by 2034. These incumbents are further reinforcing their positions through strategic collaborations with chipset manufacturers and software‑defined networking providers, thereby accelerating product cycles and reducing time‑to‑market for next‑generation autonomous navigation solutions.

Beyond the core quartet, a robust ecosystem of niche innovators contributes specialized expertise that enriches the overall value chain. Companies such as L3Harris Technologies, Northrop Grumman, Lockheed Martin and Baidu are investing in high‑performance computing platforms and deep‑learning models tailored for maritime environments. NEC Corporation, Saab Group, Wärtsilä, Furuno Electric, Yaskawa Electric, Caterpillar Marine and OceanServer Technology focus on complementary technologies,including predictive maintenance, power‑efficient propulsion integration and compact radar modules,creating diversified options for vessel operators seeking customized solutions. This breadth of participation fuels competitive pressure, drives cost reductions and promotes rapid adoption of autonomous navigation across commercial and defense fleets.

List of Key AI Ship Autonomous Navigation Radar Processor Companies Profiled

- Kongsberg Maritime

- Raytheon Technologies

- Thales Group

- Siemens

- L3Harris Technologies

- Northrop Grumman

- Lockheed Martin

- Baidu

- NEC Corporation

- Saab Group

- Wärtsilä

- Furuno Electric

- Yaskawa Electric

- Caterpillar Marine

- OceanServer Technology

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Edge‑AI processors are emerging as the preferred choice because they enable localized decision‑making with minimal latency.

|

| By Application |

|

Collision avoidance systems drive the most intense innovation focus, as safe navigation is paramount for autonomous vessels.

|

| By End User |

|

Commercial shipping lines are rapidly adopting integrated radar processors to meet emerging autonomy mandates.

|

| By System Integration |

|

Integrated navigation suites are gaining traction as shipbuilders seek holistic packages that reduce integration complexity.

|

| By Regulatory Focus |

|

Safety‑certified processors dominate strategic road‑maps because maritime authorities demand demonstrable reliability.

|

Regional Analysis: AI Ship Autonomous Navigation Radar Processor Market

Persistent demand for fuel‑efficient shipping, coupled with government incentives for low‑emission vessels, fuels investment in AI‑enabled radar processors. Industry consortia focus on integrating sensor fusion and predictive analytics, driving rapid adoption across both commercial and defense sectors.

Advances in machine‑learning models and high‑resolution radar arrays are reshaping navigation capabilities. Start‑ups are leveraging cloud‑based training pipelines to enhance object detection accuracy, positioning North America at the frontier of autonomous maritime innovation.

The U.S. Coast Guard’s evolving framework emphasizes safety certification while allowing sandbox environments for experimentation. This balanced approach encourages manufacturers to test AI radar processors without stifling innovation.

Established defense contractors and emerging silicon‑chip firms dominate the competitive arena, often partnering with maritime technology firms to co‑develop bespoke AI radar solutions for autonomous vessels.

Europe

Europe’s maritime clusters, particularly in the Nordics and the United Kingdom, are nurturing AI Ship Autonomous Navigation Radar Processor Market through strong public‑private partnerships. Funding programs such as Horizon Europe support research into sensor fusion and AI safety verification. Port authorities are piloting autonomous cargo ships equipped with next‑generation radar processors, emphasizing interoperability across EU waters. While regulatory harmonization remains a work‑in‑progress, the European Union’s focus on decarbonization aligns with the market’s push for greener navigation technologies, prompting shipowners to explore AI‑driven systems that reduce fuel consumption and emissions.

Asia‑Pacific

The Asia‑Pacific region shows rapid momentum as major shipbuilding nations invest heavily in autonomous navigation capabilities. Countries such as Japan, South Korea, and Singapore are integrating AI radar processors into new vessel classes, driven by competitive pressures and government initiatives aimed at enhancing maritime safety. Trade corridors in the South China Sea serve as real‑world testing grounds, offering dense traffic scenarios that refine detection algorithms. Although the market faces varied regulatory environments, the collective emphasis on digital transformation accelerates adoption across commercial fleets and offshore support vessels.

South America

South America’s growing port infrastructure and expanding offshore oil activities create fertile ground for AI Ship Autonomous Navigation Radar Processor Market. Brazil and Chile are piloting autonomous patrol vessels equipped with advanced radar processing to improve maritime domain awareness. While capital availability is more constrained compared to North America, regional development banks are beginning to fund technology projects that enhance navigation safety and operational efficiency, signaling a gradual but steady market entry.

Middle East & Africa

In the Middle East and Africa, strategic maritime routes such as the Red Sea and the Gulf of Aden drive interest in autonomous navigation solutions. Gulf Cooperation Council states are allocating resources toward smart port initiatives, which include trial deployments of AI‑enhanced radar processors for cargo ships. African coastal nations are exploring partnerships with international technology providers to bolster vessel safety in congested waterways, positioning the region for incremental growth as regulatory frameworks evolve.

Report Scope

This market research report provides a comprehensive analysis of the AI Ship Autonomous Navigation Radar Processor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Ship Autonomous Navigation Radar Processor Market?

-> AI Ship Autonomous Navigation Radar Processor market size is projected to grow from USD 0.70 billion in 2025 to USD 1.60 billion by 2034, exhibiting a CAGR of 9 %

Which key companies operate in AI Ship Autonomous Navigation Radar Processor Market?

-> Key players include Kongsberg Maritime, Raytheon Technologies, Thales Group, and Siemens, among others.

What are the key growth drivers?

-> Key growth drivers include rising investment in autonomous shipping technologies, stricter safety regulations, demand for fuel‑efficient navigation solutions, edge‑AI integration, and real‑time sensor fusion.

Which region dominates the market?

-> The reference does not specify a dominant region for this market.

What are the emerging trends?

-> Emerging trends include edge‑AI integration, real‑time sensor fusion, strategic collaborations, and product innovations aimed at reducing latency and enhancing reliability.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...