AI Server Power Semiconductor Market Insights

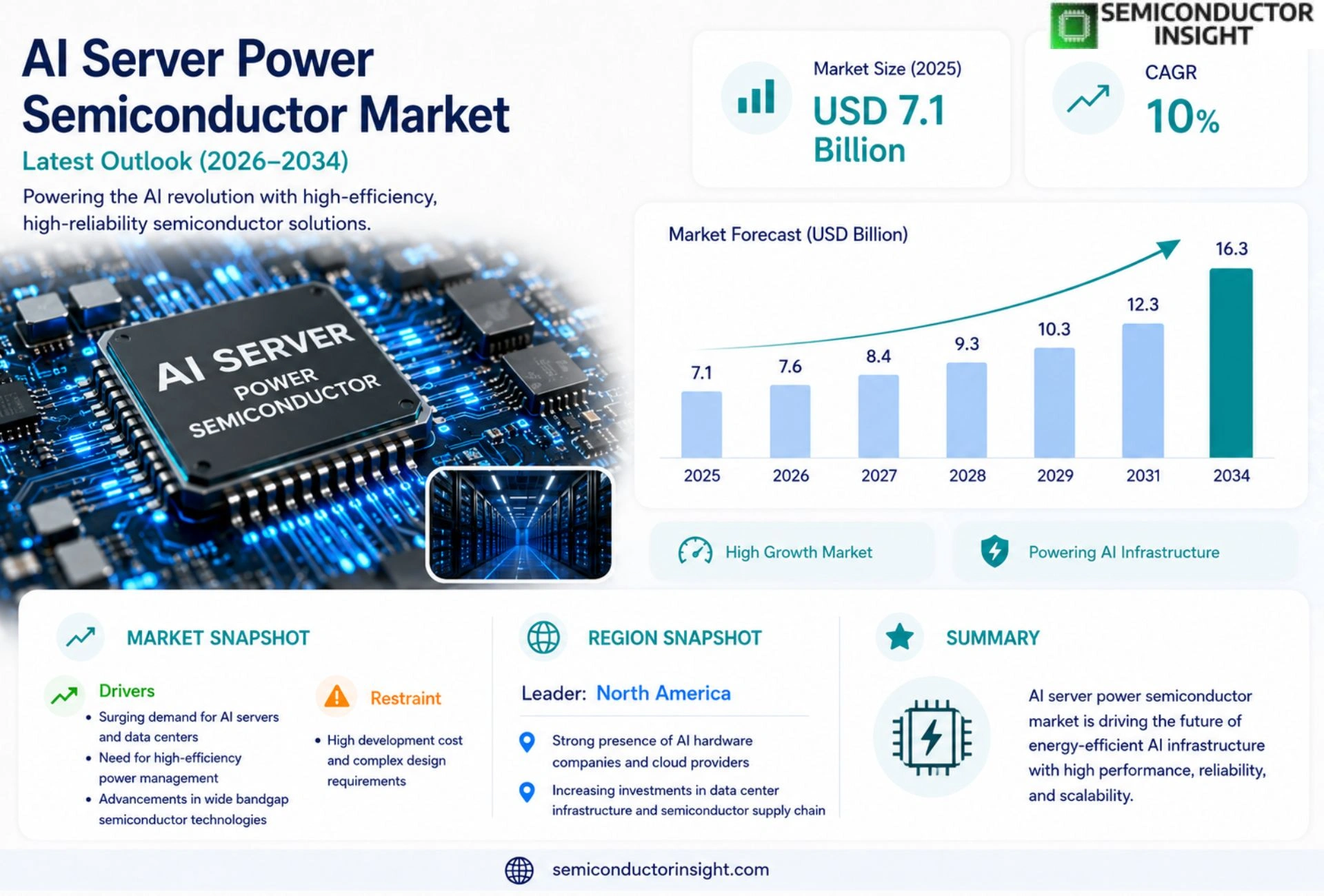

Global AI Server Power Semiconductor Market size was valued at USD 7.1 billion in 2025. The market is projected to grow from USD 7.6 billion in 2026 to USD 16.3 billion by 2034, exhibiting a CAGR of 10% during the forecast period.

AI server power semiconductors comprise advanced silicon‑carbide (SiC) and gallium‑nitride (GaN) devices that deliver high‑efficiency voltage regulation and rapid switching for artificial‑intelligence workloads in data centers. These components replace traditional silicon‑based power ICs, enabling lower energy consumption, reduced heat dissipation, and higher performance density within AI‑optimized servers.

The market is accelerating because enterprises are scaling up AI compute capacity while seeking greener operations; consequently, demand for energy‑efficient power conversion has surged.

Furthermore, major chipmakers such as Infineon Technologies and Texas Instruments have expanded their SiC/GaN portfolios specifically for AI servers. In February 2024, Infineon announced a new line of SiC MOSFETs engineered for sub‑50 ns switching speeds tailored to hyperscale data centers. Similarly, Nvidia’s partnership with TSMC on advanced packaging solutions has spurred adoption of high‑power GaN modules across next‑generation GPU clusters. These initiatives together drive robust growth across the sector.

MARKET DRIVERS

Rising Demand for Compute‑Intensive AI Workloads

AI Server Power Semiconductor Market is being propelled by an unprecedented surge in AI model training and inference workloads. Data centers worldwide are expanding capacity to support generative AI services, which require power‑efficient semiconductor solutions that can sustain multi‑teraflop performance while keeping energy consumption below 300 W per server rack.

Energy Efficiency Regulations and Sustainability Goals

Governments and corporate ESG commitments are mandating stricter power‑usage effectiveness (PUE) targets. Manufacturers that integrate gallium nitride (GaN) and silicon‑carbide (SiC) devices gain a competitive edge, delivering up to 30 % lower leakage currents compared with traditional silicon technologies.

➤ Global AI server shipments are projected to exceed 1.2 million units by 2027, driving power semiconductor revenues above $8 billion.

These dynamics create a virtuous cycle: higher AI demand stimulates investment in next‑generation power semiconductors, which in turn enable more scalable and greener AI server deployments.

MARKET CHALLENGES

High Capital Expenditure for Advanced Node Integration

Adopting 5‑nm and sub‑5‑nm process nodes for AI server power modules demands substantial R&D spend and equipment upgrades. Smaller geometries increase design complexity and yield uncertainty, potentially stretching project timelines for OEMs seeking rapid time‑to‑market.

Other Challenges

Supply Chain Volatility

Geopolitical tensions and raw‑material shortages have raised component lead times, forcing manufacturers to maintain larger safety stocks and negotiate long‑term contracts, which can inflate overall system cost.

MARKET RESTRAINTS

Thermal Management Constraints in High‑Density Servers

As AI accelerators concentrate computational power, heat flux per unit area rises sharply. Conventional cooling solutions struggle to dissipate >150 W per chip, limiting the adoption of higher‑voltage power semiconductors unless innovative thermal interface materials or liquid‑cooling architectures are deployed.

MARKET OPPORTUNITIES

Emerging Wide‑Bandgap Materials

GaN and SiC technologies present a high‑growth opportunity, offering faster switching speeds and superior thermal resilience. Early adopters are expected to capture a 20 % market share by 2028, as server manufacturers prioritize power‑dense designs that can sustain AI workloads without exceeding rack power limits.

AI Server Power Semiconductor Market Trends

Rapid Adoption of SiC and GaN Devices

AI Server Power Semiconductor Market is witnessing a decisive shift toward silicon‑carbide (SiC) and gallium‑nitride (GaN) technologies. These devices provide higher efficiency voltage regulation and ultra‑fast switching, which are essential for the intense compute workloads of modern artificial‑intelligence applications. By replacing traditional silicon‑based power ICs, SiC and GaN components reduce overall energy consumption, lower heat dissipation, and enable greater performance density within server racks. Enterprises expanding AI workloads are increasingly selecting these power semiconductors to meet both computational demands and sustainability targets, creating a strong upward momentum for the market.

Other Trends

Energy‑Efficiency‑Driven Procurement

Data‑center operators are prioritizing energy‑efficiency when sourcing power conversion solutions. The transition to SiC and GaN reduces the power loss per conversion stage, translating into measurable electricity savings at scale. This efficiency advantage aligns with corporate carbon‑reduction goals and improves total cost of ownership for AI‑focused facilities. As a result, procurement cycles now favor suppliers that can demonstrate verified power‑saving performance, prompting a competitive environment among semiconductor manufacturers.

Strategic Partnerships and Portfolio Expansion

Major chipmakers are actively expanding their AI‑server‑specific portfolios. Infineon Technologies introduced a new line of SiC MOSFETs engineered for sub‑50 ns switching speeds, specifically targeted at hyperscale data centers, while Texas Instruments broadened its GaN product range to support higher voltage ratings. Concurrently, Nvidia’s collaboration with TSMC on advanced packaging has accelerated the adoption of high‑power GaN modules across next‑generation GPU clusters. These strategic initiatives reinforce the market’s growth trajectory by delivering ready‑to‑integrate solutions that meet the rigorous performance and reliability standards of AI server architectures.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Server Power Semiconductors: Market Dynamics and Competitive Overview

AI Server Power Semiconductor Market is anchored by a few dominant OEMs that control the majority of silicon‑carbide (SiC) and gallium‑nitride (GaN) supply chains for hyperscale data centers. Infineon Technologies leads with its new SiC MOSFET family optimized for sub‑50 ns switching, positioning it as the primary source for energy‑efficient power modules in AI‑focused servers. Texas Instruments follows closely, leveraging its extensive analog portfolio and recent GaN device launches to capture a sizable share of the mid‑range server segment. Both companies benefit from deep R&D investments and strategic partnerships with hyperscale cloud providers, which reinforce a market structure characterized by high barriers to entry and concentration around vertically integrated design‑to‑fab capabilities.

Beyond the core leaders, a diverse set of niche players contributes specialized expertise that fuels innovation across the value chain. ON Semiconductor and NXP Semiconductors provide robust SiC power ICs for edge‑AI workloads, while STMicroelectronics and ROHM Semiconductor focus on compact GaN solutions for dense rack deployments. Smaller but technically aggressive firms such as Cree/Wolfspeed, Qorvo, and Skyworks Solutions target high‑frequency switching applications, and companies like Mitsubishi Electric and Analog Devices supply complementary driver and control circuits that enable system‑level efficiency gains. This broader ecosystem of semi‑specialists ensures competitive pressure, facilitates rapid technology diffusion, and supports the sustained double‑digit growth projected for the sector.

List of Key AI Server Power Semiconductor Companies Profiled

- Infineon Technologies

- Texas Instruments

- ON Semiconductor

- NXP Semiconductors

- STMicroelectronics

- ROHM Semiconductor

- Cree/Wolfspeed

- Qorvo

- Skyworks Solutions

- Mitsubishi Electric

- Analog Devices

- Microchip Technology

- Broadcom Inc.

- GlobalFoundries

- Toshiba Electronic Devices & Storage Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Silicon‑Carbide (SiC) Devices

|

| By Application |

|

Data Center AI Servers

|

| By End User |

|

Cloud Service Providers

|

| By Power Architecture |

|

Integrated Power Modules

|

| By Deployment Model |

|

Hyperscale Data Centers

|

Regional Analysis: North America

The primary drivers for the North American AI Server Power Semiconductor Market include the expanding cloud computing sector, the increasing adoption of edge AI, and the growing demand for energy-efficient data centers. Advancements in AI algorithms necessitate more powerful and sophisticated power semiconductors for optimal server performance.

Significant technological advancements in power electronics, such as wide bandgap semiconductors (SiC and GaN), are enabling the design of more efficient and compact AI server power supplies. These advancements are crucial for addressing the power density challenges associated with high-performance AI processors.

The competitive landscape is characterized by a mix of established semiconductor manufacturers and emerging players focused on AI-specific power solutions. Companies are investing heavily in R&D to develop next-generation power semiconductors that meet the evolving demands of AI servers.

Future trends in the North American AI Server Power Semiconductor Market will likely focus on further integration of power management ICs, increased emphasis on thermal management solutions, and the development of power semiconductors optimized for specific AI workloads.

United States

The United States represents the largest market within North America, driving a significant portion of the demand for AI Server Power Semiconductors. The mature technology infrastructure and leading AI research institutions within the country provide a strong foundation for market growth. Significant government funding for AI initiatives further accelerates adoption. The strong presence of major data centers and cloud service providers in the US contributes substantially to the market’s overall size.

Canada

Canada exhibits a steadily growing market for AI Server Power Semiconductors, benefiting from close ties with the US and a burgeoning tech sector. Government support for innovation and a skilled workforce are contributing factors to this growth. The Canadian market is increasingly focused on supporting AI applications in areas such as healthcare and finance.

Mexico

Mexico’s AI Server Power Semiconductor Market is emerging, driven by increasing investments in data centers and a growing adoption of AI technologies. The country’s strategic location and relatively lower labor costs present opportunities for manufacturing and assembly of AI server components. The market is expected to experience moderate growth in the coming years.

General Observations

The North American AI Server Power Semiconductor Market is expected to continue its strong growth trajectory through 2034, driven by ongoing advancements in AI technology and increasing demand for high-performance computing. Energy efficiency and power density will remain key considerations in product development. Collaboration between industry, academia, and government will be crucial for sustaining innovation and achieving optimal market growth.

Report Scope

This market research report provides a comprehensive analysis of the AI Server Power Semiconductor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high‑growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country‑level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market‑entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real‑time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Server Power Semiconductor Market?

-> AI Server Power Semiconductor Market size was valued at USD 7.1 billion in 2025. The market is projected to grow from USD 7.6 billion in 2026 to USD 16.3 billion by 2034

Which key companies operate AI Server Power Semiconductor Market?

-> Key players include Infineon Technologies, Texas Instruments, Nvidia, and TSMC, among others.

What are the key growth drivers?

-> Key growth drivers include increasing AI compute capacity, demand for energy‑efficient power conversion, and greener data‑center operations.

Which region dominates the market?

-> The reference does not specify a dominant region; the market is described on a global basis.

What are the emerging trends?

-> Emerging trends include development of high‑speed SiC MOSFETs for hyperscale data centers and adoption of high‑power GaN modules through advanced packaging partnerships.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...