AI Semiconductor Fab Airborne Molecular Contamination Sensor Array Processor Market Insights

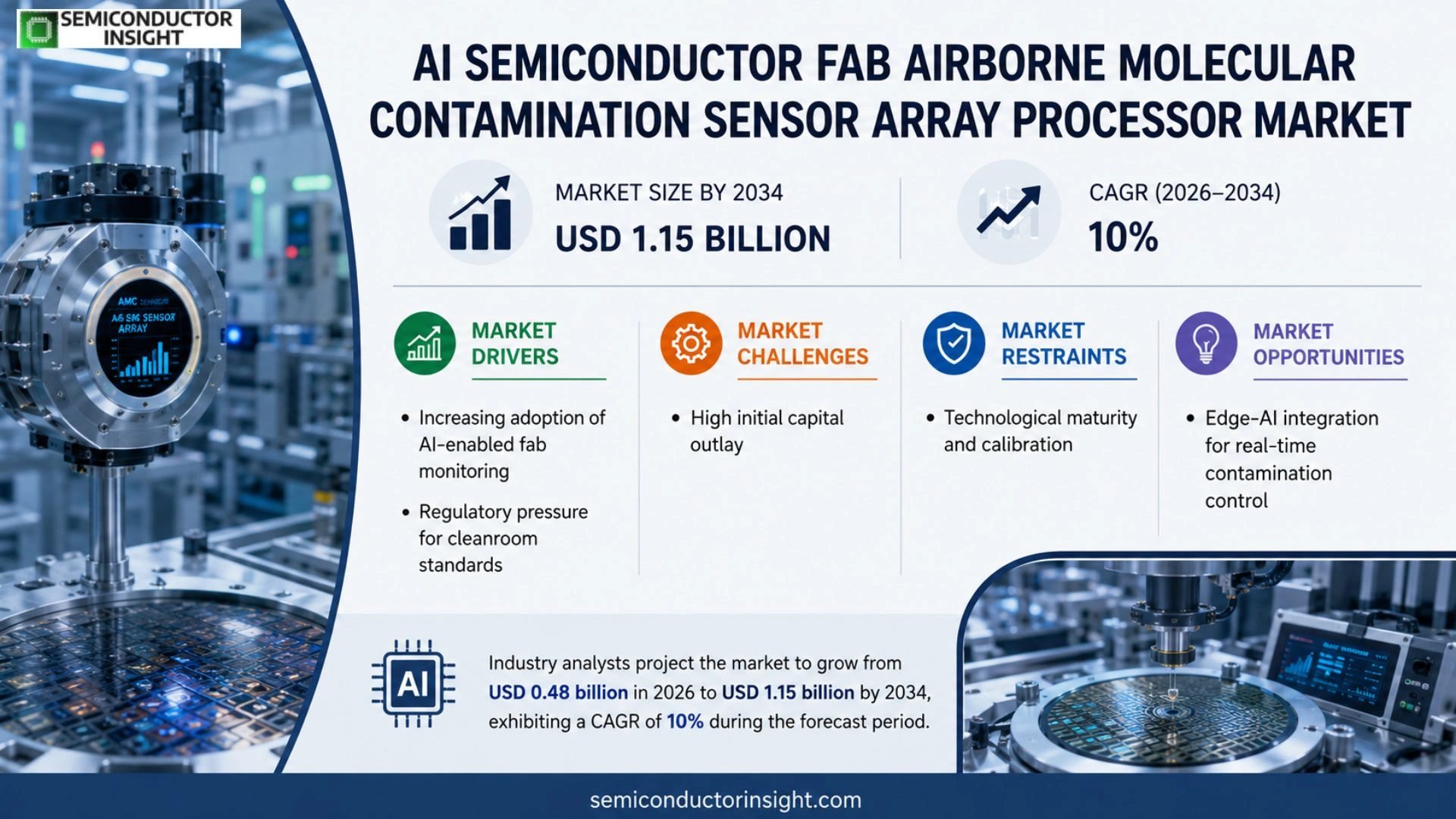

Global AI Semiconductor Fab Airborne Molecular Contamination Sensor Array Processor market size was valued at USD 0.46 billion in 2025. The market is projected to grow from USD 0.48 billion in 2026 to USD 1.15 billion by 2034, exhibiting a CAGR of 10 % during the forecast period.

The processors integrate advanced AI algorithms with high‑precision airborne molecular contamination (AMC) sensors deployed within semiconductor fabs, enabling real‑time detection of sub‑part‑per‑trillion contaminants such as moisture, organics, and metallic particles across wafer surfaces.

The market is accelerating because fab owners are investing heavily in yield‑enhancement technologies, while stricter contamination standards drive adoption of intelligent monitoring solutions.

MARKET DRIVERS

Increasing Adoption of AI‑Enabled Fab Monitoring

Semiconductor fabs are integrating AI algorithms to predict contamination events, driving demand for high‑precision sensor arrays. The need for real‑time data has pushed manufacturers to invest in airborne molecular contamination (AMC) sensor processors that can handle massive data streams while maintaining sub‑ppm detection limits. AI semiconductor fab airborne molecular contamination sensor array processor market revenues are projected to surpass $1.2 billion by 2030.

Regulatory Pressure for Cleanroom Standards

Stringent ISO 14644‑1 amendments and upcoming government mandates require fabs to demonstrate continuous contamination control. Compliance costs are encouraging fab operators to deploy advanced sensor processors that provide auditable data trails. As a result, capital expenditure on AMC detection systems is expected to grow at a compound annual growth rate (CAGR) of 12‑15 %.

➤ “Investments in AI‑driven contamination monitoring are reducing defect densities by up to 30 % in leading foundries.”

Furthermore, the convergence of AI edge computing with sensor hardware is shortening decision cycles, enabling immediate corrective actions. This synergy is a core catalyst for market expansion across both mature and emerging fabs.

MARKET CHALLENGES

High Initial Capital Outlay

Deploying an integrated sensor array processor requires substantial upfront investment in hardware, software licensing, and staff training. Small‑to‑medium fabs often face budget constraints that delay adoption, limiting market penetration in certain regions.

Other Challenges

Data Integration Complexity

Merging sensor outputs with legacy fab management systems demands custom interfaces and robust cybersecurity measures, increasing project timelines and cost overruns.

MARKET RESTRAINTS

Technological Maturity and Calibration

Accurate AMC detection hinges on precise calibration routines that can be time‑consuming and require specialized expertise. Inconsistent calibration standards across equipment vendors create interoperability risks, restraining broader market acceptance.

MARKET OPPORTUNITIES

Edge‑AI Integration for Real‑Time Contamination Control

Embedding AI inference engines within sensor processors enables on‑device anomaly detection, reducing latency and network bandwidth usage. This edge‑AI capability opens new revenue streams for vendors offering turnkey solutions to high‑volume fabs.

Expansion into Emerging Semiconductor Hubs

Rapid fab construction in Southeast Asia and Eastern Europe creates a fertile landscape for next‑generation contamination monitoring systems. Early‑stage partnerships with local manufacturers can capture market share before competitors establish footholds.

AI Semiconductor Fab Airborne Molecular Contamination Sensor Array Processor Market Trends

Rising Adoption Driven by Yield‑Enhancement Investments

AI Semiconductor Fab Airborne Molecular Contamination Sensor Array Processor Market is experiencing accelerated uptake as semiconductor fabs prioritize yield‑enhancement technologies. Revenue is projected to climb from roughly USD 0.48 billion in 2025 to about USD 1.15 billion by 2034, reflecting strong demand for real‑time contaminant monitoring. Advanced processors combine sophisticated AI models with high‑precision airborne molecular contamination (AMC) sensors, enabling detection of sub‑part‑per‑trillion moisture, organic, and metallic particles across wafer surfaces. This capability aligns with tighter contamination standards and the industry’s pursuit of incremental yield gains, positioning the market as a critical enabler for next‑generation chip production.

Other Trends

Strategic Partnerships Accelerate Innovation

Collaboration among leading equipment suppliers underscores the momentum of AI Semiconductor Fab Airborne Molecular Contamination Sensor Array Processor Market. In March 2024, Applied Materials announced a joint development effort with Intel’s AI chip division to co‑create next‑generation AMC sensor arrays. Such alliances leverage complementary expertise, shorten time‑to‑market, and expand the functional envelope of AI‑enabled contamination detection. Key participants,including KLA Corporation, ASML Holding, Thermo Fisher Scientific, and Advantest,are actively pursuing similar partnerships to broaden their portfolio and meet the growing expectations of fab operators.

Enhanced AI Algorithms Boost Detection Precision

Continuous refinement of AI algorithms is sharpening the accuracy of contaminant identification within AI Semiconductor Fab Airborne Molecular Contamination Sensor Array Processor Market. Emerging models now process sensor data at higher frame rates, reducing false‑positive rates and delivering actionable insights within seconds of detection. This improvement supports tighter process control, minimizes scrap, and reinforces the business case for integrating intelligent monitoring solutions across high‑volume manufacturing lines. As fabs adopt these smarter processors, the market is poised to sustain robust growth while reinforcing overall chip quality and reliability.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Semiconductor Fab Airborne Molecular Contamination Sensor Array Processor Market Overview

The market is anchored by a small number of vertically integrated giants that combine AI‑accelerated ASIC design with proprietary airborne molecular contamination (AMC) sensor arrays. Applied Materials, together with Intel’s AI chip division, leads the ecosystem through a strategic partnership that delivers next‑generation sensor‑processor modules for high‑volume fabs. KLA Corporation follows with its advanced yield‑inspection platforms that now embed AI‑driven AMC analytics, while ASML Holding leverages its lithography roadmap to embed contamination sensing directly into exposure equipment. Thermo Fisher Scientific supplies precision metrology hardware and the associated AI processing stack, and Advantest offers test solutions that incorporate real‑time contamination feedback. These tier‑one players control the majority of design IP, supply chain relationships, and high‑value fab contracts, shaping the market’s competitive dynamics and pricing power.

Niche but technically influential companies are expanding the competitive perimeter. Lam Research and Tokyo Electron contribute specialized wafer‑processing tools that integrate AI‑enhanced AMC sensors for process modules such as etch and deposition. NXP Semiconductors and Marvell Technology provide low‑power AI edge processors that enable distributed sensing across fab cleanrooms. Broadcom, Qualcomm and Texas Instruments supply the connectivity and signal‑conditioning ASICs that feed sensor data into central analytics platforms. ON Semiconductor and Analog Devices round out the ecosystem with high‑performance analog front‑ends and precision timing solutions, supporting emerging modular sensor architectures and custom AI inference pipelines.

List of Key AI Semiconductor Fab Airborne Molecular Contamination Sensor Array Processor Companies Profiled

- Applied Materials

- Intel

- KLA Corporation

- ASML Holding

- Thermo Fisher Scientific

- Advantest

- Lam Research

- Tokyo Electron

- NXP Semiconductors

- Marvell Technology

- Broadcom

- Qualcomm

- Texas Instruments

- ON Semiconductor

- Analog Devices

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Hybrid Sensor Arrays are emerging as the preferred type because:

|

| By Application |

|

Wafer Process Monitoring drives adoption because:

|

| By End User |

|

Fab Operators are the dominant user group, given their need to:

|

| By Integration Architecture |

|

Edge AI Processors dominate because they:

|

| By Functional Focus |

|

Contamination Detection remains the core focus, delivering:

|

Regional Analysis: AI Semiconductor Fab Airborne Molecular Contamination Sensor Array Processor Market

North America

The push for higher yield, stringent quality standards, and the need for predictive maintenance are compelling fabs to adopt AI‑enabled contamination sensors. Robust demand from high‑value logic and memory nodes fuels investment in sensor array processors that can detect sub‑ppm molecular traces, thereby protecting critical process steps.

U.S. and Canadian regulatory bodies encourage cleanroom compliance through guidelines that indirectly promote advanced monitoring solutions. While formal standards for airborne molecular detection are emerging, existing environmental health regulations create a favorable backdrop for sensor adoption.

Integration of edge AI processors with sensor arrays enables real‑time analytics on the fab floor. Early adopters report reduced downtime and faster root‑cause analysis, driving broader diffusion across downstream and upstream process modules.

A mix of established semiconductor equipment vendors and specialized sensor startups compete on performance, size, and AI capabilities. Strategic alliances and joint R&D programs are common, accelerating product refresh cycles and market penetration.

Europe

European fabs, particularly in Germany, the Netherlands, and France, are witnessing a steady rise in AI‑driven contamination monitoring as the region emphasizes Industry 4.0 initiatives. Collaborative research programs funded by the EU foster innovation in sensor miniaturization and AI model optimization. While regulatory pressure is moderate compared with North America, sustainability targets and carbon‑neutral manufacturing agendas push operators toward more efficient, data‑centric solutions, creating a fertile environment for AI Semiconductor Fab Airborne Molecular Contamination Sensor Array Processor Market to expand across the continent.

Asia‑Pacific

The Asia‑Pacific region, led by China, Taiwan, South Korea, and Japan, is rapidly scaling its semiconductor capacity, which is translating into heightened interest in advanced contamination sensors. Government incentives for smart factories and aggressive fab construction pipelines encourage early adoption of AI‑enabled sensor arrays. Local manufacturers benefit from close proximity to sensor component suppliers, enabling faster iteration and cost‑effective integration, thereby positioning the region as a high‑growth frontier for the market.

South America

South American semiconductor activities remain nascent, yet Brazil and Colombia are investing in pilot lines that prioritize quality control. The adoption of AI Semiconductor Fab Airborne Molecular Contamination Sensor Array Processor technologies is being driven by the desire to meet international export standards and to reduce reliance on imported defect‑analysis services. Partnerships with North American technology providers are facilitating knowledge transfer, laying the groundwork for gradual market uptake.

Middle East & Africa

In the Middle East and Africa, emerging fab initiatives in the United Arab Emirates and South Africa are exploring AI‑based contamination monitoring as part of broader diversification strategies. While overall market size is modest, strategic government funding and the establishment of technology hubs are creating early‑stage demand for sensor array processors. These efforts aim to build local expertise and attract multinational semiconductor firms seeking a foothold in new geographies.

Report Scope

This market research report provides a comprehensive analysis of the AI Semiconductor Fab Airborne Molecular Contamination Sensor Array Processor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Semiconductor Fab Airborne Molecular Contamination Sensor Array Processor Market?

-> Global AI Semiconductor Fab Airborne Molecular Contamination Sensor Array Processor market is projected to grow from USD 0.48 billion in 2026 to USD 1.15 billion by 2034.

Which key companies operate in AI Semiconductor Fab Airborne Molecular Contamination Sensor Array Processor Market?

-> Key players include KLA Corporation, ASML Holding, Thermo Fisher Scientific, and Advantest.

What are the key growth drivers?

-> Key growth drivers include heavy investments by fab owners in yield‑enhancement technologies, stricter contamination standards, and strategic collaborations to develop next‑generation AMC sensor arrays.

Which region dominates the market?

-> The reference does not specify a dominant region; the market is assessed on a global basis.

What are the emerging trends?

-> Emerging trends include integration of advanced AI algorithms with high‑precision AMC sensors and collaborative development of next‑generation sensor arrays.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...