AI Processor Thermal Interface Material Market Insights

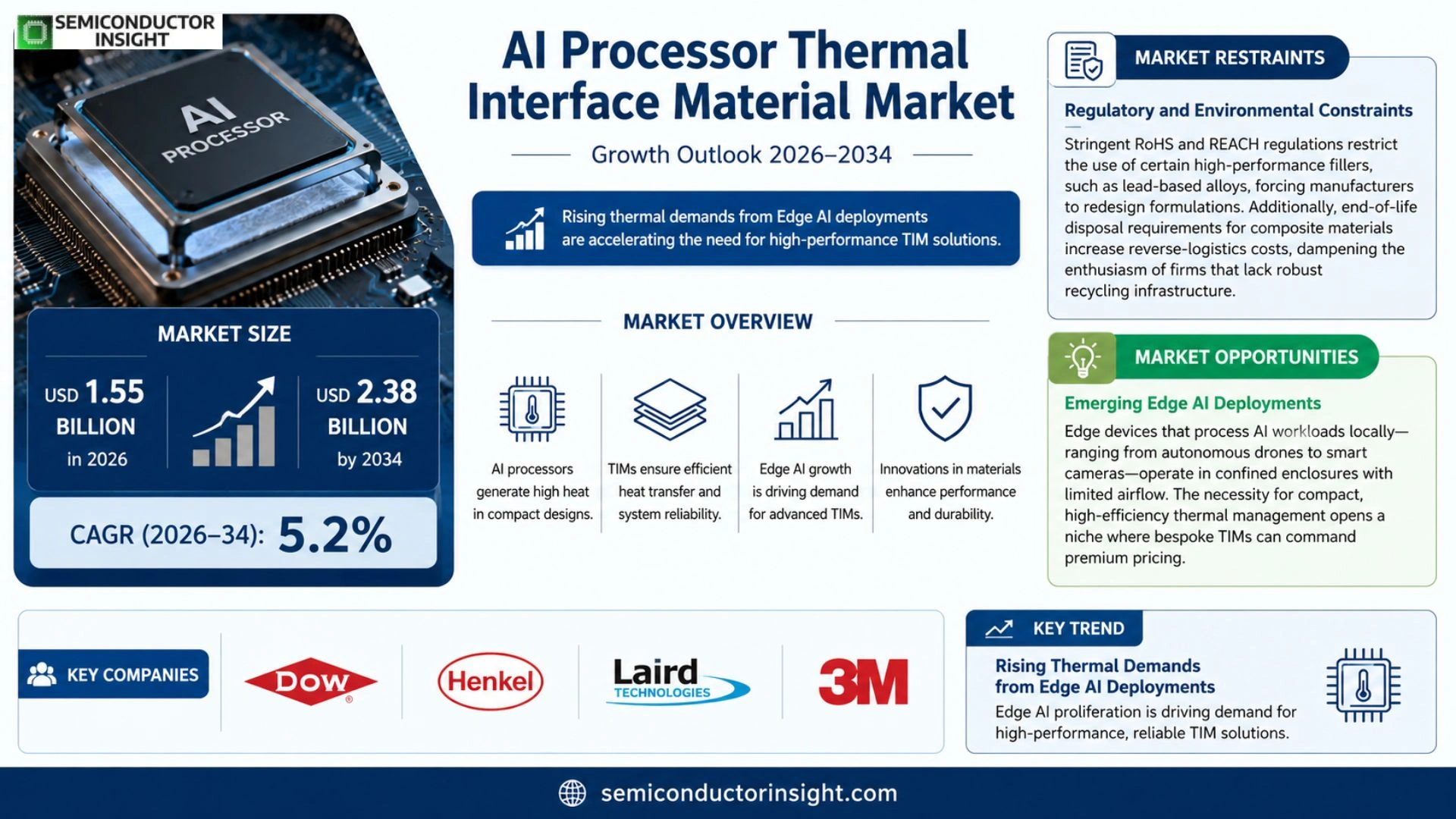

AI Processor Thermal interface Interface Material market size was valued at USD 1.45 billion in 2025. The market is forecasted to increase from USD 1.55 billion in 2026 to USD 2.38 billion by 2034, exhibiting a CAGR of 5.2% during the forecast period.

AI processor thermal interface materials are engineered compounds,such as silicone‑based greases, phase‑change materials, and graphite pads,designed to bridge the gap between high‑performance processors and heat sinks, thereby reducing thermal resistance and maintaining optimal operating temperatures under intensive workloads.

The expansion of edge‑computing devices and the rise of transformer‑size models demand efficient heat dissipation solutions; consequently, manufacturers are investing in low‑thermal‑conductivity formulations while also seeking materials compatible with advanced packaging technologies.

Major suppliers such as Dow Chem, Henkel and Laird Technologies have introduced next‑generation TIMs that tolerate temperatures above 200 °C, enabling AI accelerators in data centers and autonomous vehicles to sustain peak performance.

MARKET DRIVERS

Escalating Thermal Demands of AI Chipsets

AI Processor Thermal Interface Material Market is being pulled forward by unprecedented power densities in modern AI accelerators. As silicon architectures shrink and integrate billions of transistors, heat fluxes exceed 200 W/cm² in some designs, making conventional cooling insufficient. Engineers are therefore prioritizing TIMs that deliver low thermal resistance while maintaining mechanical compliance, a combination that directly influences compute throughput and reliability.

Advancements in Material Science

Recent breakthroughs in nanocomposites, such as vertically aligned graphene sheets and functionalized polymer matrices, have elevated the performance ceiling for thermal interface solutions. These innovations enable conductivity gains of 30 % over legacy silicone greases, while preserving flexibility needed for dynamic mounting pressures. The material‑level progress translates into faster time‑to‑market for AI hardware, reinforcing the market’s upward trajectory.

➤ “Thermal bottlenecks now define the competitive edge of AI hardware, prompting manufacturers to allocate up to 15 % of product development budgets to TIM research.”

Combined, the pressure to manage heat efficiently and the rapid maturation of high‑conductivity materials create a dual engine that fuels investment, collaboration, and product launches across AI Processor Thermal Interface Material Market.

MARKET CHALLENGES

Manufacturing Complexity

Scaling nanostructured TIMs from laboratory batches to high‑volume fabs requires precise control over filler dispersion, cure cycles, and surface finish. Any deviation can compromise thermal pathways, leading to yield loss and warranty claims. The steep learning curve for new processes deters smaller suppliers from entering the space.

Other Challenges

Cost Sensitivity

While performance gains are measurable, the price premium of advanced TIMs can exceed 40 % compared with traditional alternatives. OEMs weighing total cost of ownership must justify the incremental expense against marginal efficiency improvements, a calculation that often stalls adoption in cost‑constrained segments.

MARKET RESTRAINTS

Regulatory and Environmental Constraints

Stringent RoHS and REACH regulations restrict the use of certain high‑performance fillers, such as lead‑based alloys, forcing manufacturers to redesign formulations. Additionally, end‑of‑life disposal requirements for composite materials increase reverse‑logistics costs, dampening the enthusiasm of firms that lack robust recycling infrastructure.

MARKET OPPORTUNITIES

Emerging Edge AI Deployments

Edge devices that process AI workloads locally,ranging from autonomous drones to smart cameras,operate in confined enclosures with limited airflow. The necessity for compact, high‑efficiency thermal management opens a niche where bespoke TIMs can command premium pricing. Companies that tailor solutions for ruggedized, low‑power edge platforms stand to capture a growing slice of AI Processor Thermal Interface Material Market.

AI Processor Thermal Interface Material Market Trends

Rising Thermal Demands from Edge AI Deployments

The proliferation of edge‑computing nodes equipped with AI accelerators is reshaping heat‑removal strategies. As devices shift from data‑center back‑ends to on‑premise or remote locations, designers encounter tighter packaging constraints and limited airflow. Consequently, the interface between processors and heat sinks must convey heat more efficiently while occupying minimal volume. Vendors that can deliver low‑viscosity, high‑conductivity compounds gain a competitive edge because system integrators prioritize reliability under variable ambient conditions. The trend forces OEMs to evaluate thermal interface material (TIM) performance early in the product development cycle, influencing bill‑of‑materials allocation and warranty assumptions.

Other Trends

Material Innovation for Extreme Environments

Automotive and aerospace applications are pushing TIM specifications beyond traditional temperature ceilings. Recent releases from Dow Chem, Henkel and Laird Technologies demonstrate formulations that retain structural integrity above 200 °C, enabling AI processors in autonomous vehicles to sustain peak workloads during prolonged operation. These high‑temperature solutions also exhibit reduced outgassing, a critical factor for sealed enclosures. Suppliers that combine thermal stability with mechanical compliance open new revenue streams as manufacturers transition to ruggedized AI platforms, prompting shifts in supply‑chain negotiations and longer contract horizons.

Integration with Advanced Packaging Technologies

Advanced chip‑stacking techniques such as 3D‑ICs and fan‑out wafer‑level packaging demand TIMs that conform to irregular topographies while preserving low thermal resistance. The industry’s move toward heterogeneous integration amplifies the need for materials compatible with both copper and silicon interposers. Companies investing in nano‑structured fillers report measurable reductions in hotspot formation, which translates into higher processor yields and lower cooling‑system capital expenditures for end users. This alignment of material science with packaging evolution drives collaborative R&D programs, reshaping the competitive landscape and prompting strategic alliances between semiconductor fabs and specialty chemistry firms.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive Dynamics in AI Processor TIMs

AI Processor Thermal interface material arena, tier‑one chemical conglomerates dominate the supply chain. Dow, Henkel, and Laird Technologies command the bulk of high‑temperature silicone greases, phase‑change compounds, and graphite‑based pads that enable AI accelerators to operate above 200 °C. Their advantage derives from deep R&D pipelines, the ability to scale production for data‑center and autonomous‑vehicle contracts, and collaborations with leading silicon‑chip designers. By embedding TIM expertise into next‑generation packaging platforms, these firms lock in long‑term revenue streams while shaping specification standards that smaller vendors must follow. The market structure therefore resembles a concentrated core that supplies the majority of volume while setting performance baselines for the entire segment.

Beyond the core, a diverse set of specialists injects differentiation and fuels material innovation. 3M leverages its expertise in engineered films to offer flexible, low‑profile graphene sheets; Fujipoly supplies high‑conductivity silicone gels optimized for edge‑device footprints. Shin‑Etsu’s polymer‑based TIMs emphasize moisture resistance, whereas Bergquist focuses on liquid‑metal alloys for extreme power densities. Aremco Products and Parker Hannifin cater to aerospace and high‑reliability niches with custom‑cure formulations. Momentive and Thermacore push the envelope on filler technology, delivering composites that balance viscosity with conductivity. Asian players such as Taiyo Nippon Sanso and Wacker Chemie are expanding local production capacities to meet the surge in regional AI chip fab activity. Collectively, these firms pressure incumbents to broaden their portfolios, accelerate time‑to‑market, and price competitively, creating a vibrant ecosystem where innovation is a primary differentiator.

List of Key AI Processor Thermal Interface Material Companies Profiled

- Dow

- Henkel

- Laird Technologies

- 3M

- Fujipoly

- Shin‑Etsu Chemical

- Bergquist

- Aremco Products

- Parker Hannifin

- Momentive

- Thermacore

- Wacker Chemie

- Taiyo Nippon Sanso

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Thermal Conductivity Optimizers

|

| By Application |

|

High‑Performance Compute

|

| By End User |

|

Strategic End‑User Adoption

|

| By Material Formulation |

|

Formulation‑Driven Differentiation

|

| By End Deployment Environment |

|

Environmental Resilience

|

Regional Analysis: AI Processor Thermal Interface Material Market

Companies are experimenting with nano‑filled silicate gels that maintain low viscosity while delivering thermal conductivities above 10 W/m·K, a threshold previously limited to metallic interfaces. These innovations reduce pump‑down cycles in assembly lines and support slimmer system designs.

The region’s diversified supplier base mitigates raw‑material shortages. Strategic warehousing of silicone precursors and copper‑based fillers enables manufacturers to honor tight launch windows for AI processors without compromising quality.

Joint development agreements with leading chipset designers foster co‑engineered TIMs that align with specific die‑to‑package geometries, enhancing heat spread and flattening temperature gradients across high‑density cores.

Energy‑efficiency standards adopted by federal agencies incentivize the use of thermally active materials that lower overall system power consumption, driving broader acceptance among enterprise data‑center operators.

Europe

European manufacturers benefit from a tightly regulated market that emphasizes sustainability, prompting the adoption of bio‑based thermal compounds with reduced VOC emissions. The region’s strong automotive sector fuels demand for TIMs capable of withstanding harsh temperature cycles in autonomous‑driving platforms. Concurrently, the emergence of edge‑computing hubs in Germany and France creates niche opportunities for customized, low‑profile interfaces that support compact AI modules. Suppliers are therefore aligning their product portfolios with both environmental certifications and the performance expectations of Tier 1 automotive OEMs.

Asia‑Pacific

Asia‑Pacific’s ascent is propelled by rapid expansion of AI‑focused semiconductor fabs in China, South Korea, and Taiwan. Local OEMs prioritize cost‑effective TIMs that do not sacrifice thermal performance, resulting in a surge of hybrid polymer‑metal blends. Additionally, the region’s burgeoning data‑center construction drives interest in high‑conductivity greases that can be retrofitted into existing cooling loops. Governmental push for domestic chip capabilities further accelerates investment in material‑science research, positioning the area as a future source of breakthrough thermal interface technologies.

South America

South America’s market remains embryonic, yet the rise of AI‑enabled agricultural equipment is reshaping demand. Companies in Brazil and Argentina seek TIMs that tolerate wide temperature swings while maintaining electrical insulation, a requirement unique to field‑deployed processors. Limited local manufacturing capabilities mean most suppliers import products, but emerging partnerships with regional distributors are beginning to establish localized stockpiles, reducing lead‑time concerns for equipment integrators.

Middle East & Africa

In the Middle East & Africa, the primary driver is the deployment of AI‑powered surveillance and smart‑city infrastructure, which imposes strict thermal constraints on edge devices. Operators favor TIMs that resist dust ingress and maintain performance under high ambient temperatures. While import dependence remains high, the United Arab Emirates is launching a pilot program to develop a regional testing lab, which could catalyze localized formulation tweaks and foster a modest but growing ecosystem of suppliers.

Report Scope

This market research report provides a comprehensive analysis of the AI Processor Thermal Interface Material Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia‑Pacific, Latin America, and the Middle East & Africa, including country‑level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market‑entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real‑time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Processor Thermal Interface Material Market?

-> AI Processor Thermal Interface Material Market was valued at USD 1.45 billion in 2025 and is expected to reach USD 2.38 billion by 2034.

Which key companies operate AI Processor Thermal interface Material Market?

-> Key players include Dow Chem, Henkel, Laird Technologies, among others.

What are the key growth drivers?

-> Key growth drivers include expansion of edge‑computing devices, rise of transformer‑size AI models, and demand for efficient heat‑dissipation solutions.

Which region dominates the market?

-> Asia‑Pacific is the fastest‑growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include low‑thermal‑conductivity formulations, materials compatible with advanced packaging, and TIMs tolerating temperatures above 200 °C.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...