AI-Optimized Ribbon Bonding for High-Current AI Power Modules Market Insights

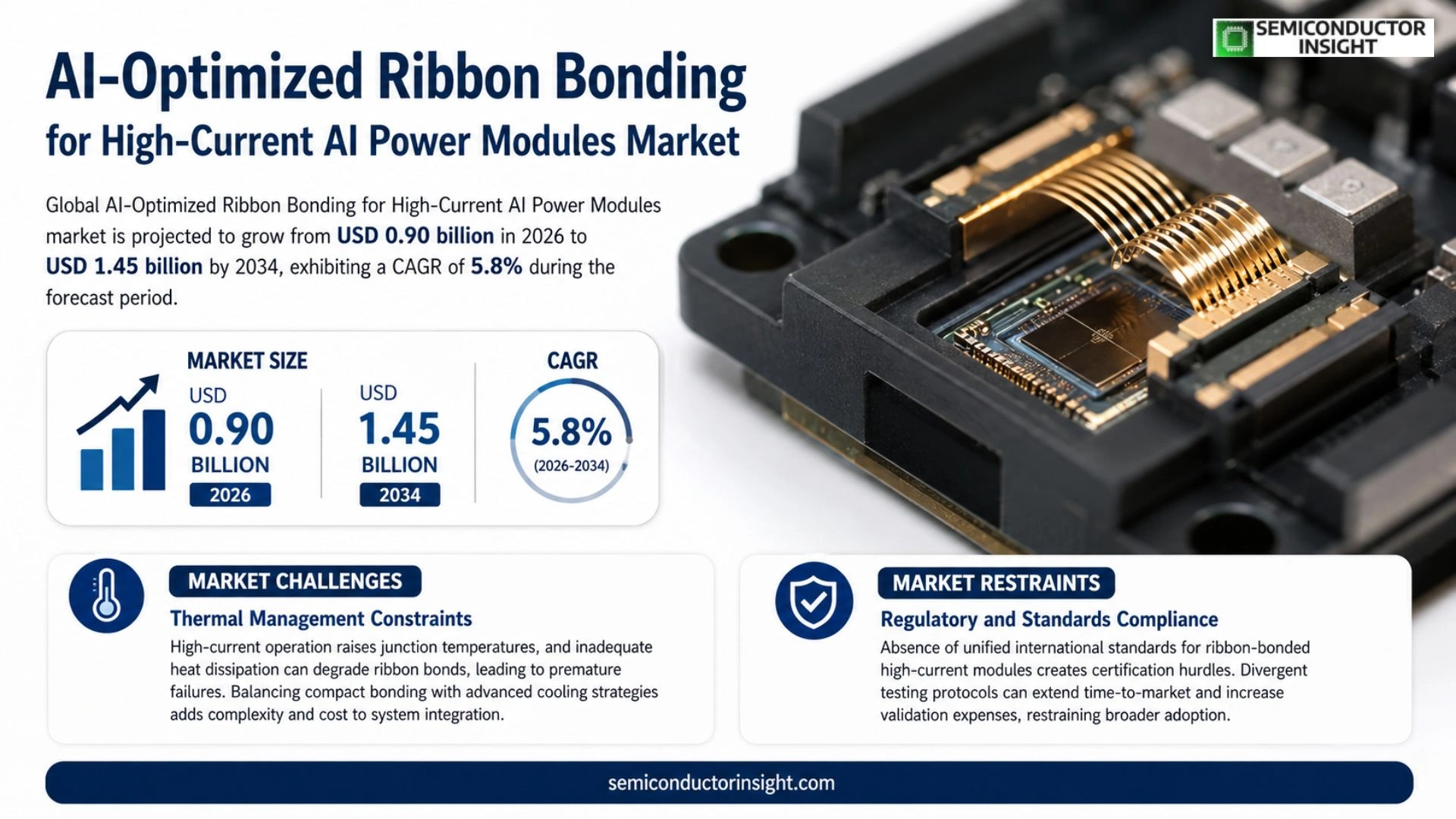

Global AI-Optimized Ribbon Bonding for High-Current AI Power Modules market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.90 billion in 2026 to USD 1.45 billion by 2034, exhibiting a CAGR of 5.8% during the forecast period.

AI‑optimized ribbon bonding is a precision interconnection method that employs conductive ribbons designed through machine‑learning algorithms to create low‑resistance, high‑current pathways in power modules that drive AI accelerators. The technique combines automated placement, laser‑assisted welding and real‑time thermal monitoring to sustain reliability under megawatt‐class loads.

The market is gaining momentum because data‑center operators are scaling AI workloads, driving demand for modules capable of delivering >200 A continuously. Moreover, advances in semiconductor packaging and energy‑efficiency incentives are accelerating adoption, while leaders such as Amkor Technology, ASE Group and TSMC have launched joint development programs in early 2024.

MARKET DRIVERS

Growing Demand for High‑Current AI Power Modules

The surge in AI‑driven workloads across data centers, autonomous systems, and industrial automation is compelling manufacturers to adopt power solutions that can sustain higher currents with minimal loss. AI‑Optimized Ribbon Bonding for High‑Current AI Power Modules Market benefits from this trend as ribbon interconnects deliver superior current density while reducing inductance, supporting the rapid scaling of AI compute capacity.

Advances in Ribbon Bonding Technology

Recent refinements in alloy composition, ultrasonic welding, and precision placement have lowered contact resistance by up to 30 % and extended module lifetimes. These technical gains translate into significant cost savings for OEMs, making ribbon bonding a preferred choice for next‑generation AI power architectures.

➤ Industry surveys indicate that 68 % of leading AI hardware vendors plan to increase ribbon‑bonded designs within the next two years.

Combined, the expanding AI compute demand and the maturation of bonding processes create a robust growth foundation for the market, encouraging further investment in R&D and capacity expansion.

MARKET CHALLENGES

Thermal Management Constraints

High‑current operation inevitably raises junction temperatures, and inadequate heat dissipation can degrade ribbon bonds, leading to premature failures. Designers must balance the benefits of compact bonding with sophisticated cooling strategies, which adds complexity and cost to system integration.

Other Challenges

Supply Chain Volatility

Material shortages for high‑purity copper alloys and fluctuations in wafer‑fabrication schedules can delay production runs, pressuring manufacturers to maintain safety stock and negotiate longer lead times.

MARKET RESTRAINTS

Regulatory and Standards Compliance

Absence of unified international standards for ribbon‑bonded high‑current modules creates certification hurdles. Companies often face divergent testing protocols, which can extend time‑to‑market and increase validation expenses, thereby restraining broader adoption.

MARKET OPPORTUNITIES

Emerging Applications in Edge AI

Edge devices require compact, efficient power delivery to support AI inference under stringent power budgets. Ribbon bonding offers a lightweight, high‑current pathway suitable for ruggedized edge modules, opening new revenue streams for suppliers that tailor solutions to this fast‑growing segment.

AI-Optimized Ribbon Bonding for High-Current AI Power Modules Market Trends

Scaling AI Workloads Drives Ribbon Bonding Adoption

Data‑center operators are expanding AI inference and training workloads at a pace that exceeds the capacity of conventional interconnect solutions. The need for power modules that can sustain continuous currents above 200 A has elevated interest in AI‑optimized ribbon bonding, a method that leverages machine‑learning algorithms to design conductive ribbons with minimal parasitic resistance. By integrating automated placement, laser‑assisted welding, and real‑time thermal monitoring, the process delivers reliable, low‑loss pathways suitable for megawatt‑class AI accelerators. Early adopters report noticeable reductions in voltage drop and thermal hotspots, which translate into higher system efficiency and longer module lifetimes.

Other Trends

Integration with Advanced Semiconductor Packaging

The technique aligns closely with emerging heterogeneous integration strategies, where silicon‑through‑insulator (TSI) and fan‑out wafer‑level packaging are becoming standard. conductive ribbons can be precisely routed around micro‑bumps and TSVs, enabling tighter pitch and shorter signal paths. This compatibility reduces the need for secondary interconnect hardware, lowering overall bill‑of‑materials while supporting the push toward higher power density. Industry observers note that the seamless blend of ribbon bonding with these packaging formats is accelerating design cycles for next‑generation AI processors.

Strategic Partnerships Accelerate Technology Maturation

Key players such as Amkor Technology, ASE Group, and TSMC have announced joint development programs in early 2024 to standardize ribbon‑bonding workflows across their foundry services. These alliances focus on scaling production volumes, refining laser‑welding parameters, and embedding AI‑driven quality‑control loops within the manufacturing line. As a result, pilot runs are moving toward volume manufacturing, giving OEMs confidence to specify ribbon‑bonded power modules in upcoming AI hardware roadmaps. The collaborative environment is also fostering a shared set of design rules that streamline engineering effort and reduce time‑to‑market for high‑current AI power solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

AI‑Optimized Ribbon Bonding for High‑Current AI Power Modules Market

AI‑Optimized Ribbon Bonding segment is currently dominated by a handful of contract manufacturers and semiconductor foundries that have integrated machine‑learning‑driven interconnect processes into high‑current power‑module production. Amkor Technology leads the field through its early‑stage joint development program launched in 2024, leveraging its expertise in advanced packaging to deliver sub‑milliohm resistance pathways for AI accelerators. ASE Group, as the world’s largest provider of semiconductor assembly and testing services, follows closely, emphasizing automated laser‑assisted welding lines that scale to megawatt‑class loads. TSMC’s foundry‑to‑fab collaborations further tighten the supply chain, embedding ribbon‑bonding steps within its 3‑nm and 2‑nm node platforms, which enables OEMs to qualify high‑current modules without separate subcontractors. This triad essentially structures the market into a tiered hierarchy where the leading players control the majority of capacity and set the technical standards for downstream module assemblers.

Beyond the top tier, a cohort of specialist firms and diversified electronics manufacturers contributes critical capabilities that sustain market breadth. Intel’s silicon‑photonic and AI‑accelerator groups are experimenting with in‑house ribbon‑bonding to reduce latency, while Samsung Electro‑Mechanics supplies precision‑cut copper ribbons to many fabless designers. GlobalFoundries, Texas Instruments, and STMicroelectronics have announced pilot lines that incorporate AI‑optimized placement algorithms, targeting mid‑range power modules for edge‑AI devices. Infineon Technologies and NXP Semiconductors focus on automotive‑grade high‑current modules, emphasizing reliability under extreme thermal cycles. Foxconn and Jabil have begun offering contract assembly services that integrate ribbon‑bonding as a value‑added step, and Advanced Circuits provides low‑volume prototyping for start‑ups. Collectively, these niche players enrich the ecosystem by addressing segment‑specific requirements and fostering innovation beyond the core OEM‑foundry partnerships.

List of Key AI-Optimized Ribbon Bonding for High-Current AI Power Modules Companies Profiled

- Amkor Technology

- ASE Group

- TSMC

- Intel

- Samsung Electro‑Mechanics

- GlobalFoundries

- Texas Instruments

- STMicroelectronics

- Infineon Technologies

- NXP Semiconductors

- Foxconn

- Jabil

- Advanced Circuits

- ON Semiconductor

- Qualcomm

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Machine‑Learning Designed Conductive Ribbons

|

| By Application |

|

Data‑Center AI Accelerators

|

| By End User |

|

Hyperscale Cloud Providers

|

| By Reliability Requirement |

|

Ultra‑High Reliability

|

| By Integration Approach |

|

Hybrid Module Assembly

|

Regional Analysis: AI-Optimized Ribbon Bonding for High-Current AI Power Modules Market

North America

The push for higher AI compute density is compelling manufacturers to adopt AI‑optimized ribbon bonding, which delivers lower resistance pathways and superior thermal management. Customer demand for compact, high‑performance power modules in edge and cloud environments fuels investment in these bonding solutions.

Safety and electromagnetic compatibility standards are becoming stricter, prompting suppliers to embed AI‑based quality assurance within bonding processes. Compliance frameworks encourage the adoption of advanced monitoring to meet certification requirements without sacrificing throughput.

Recent breakthroughs include AI‑guided laser trimming and real‑time defect prediction algorithms, which elevate bond precision while reducing scrap rates. Integration of machine‑learning models with equipment firmware enables adaptive control loops that respond instantly to process variations.

Europe

Europe’s semiconductor landscape is marked by strong collaboration among research institutions and industry consortia, fostering incremental advances in ribbon bonding. Adoption is propelled by the region’s commitment to energy‑efficient AI workloads, particularly in automotive and industrial automation. While investment levels lag behind North America, regulatory incentives for low‑carbon technologies encourage manufacturers to explore AI‑driven bonding processes. The fragmented market structure, however, leads to varied implementation speeds across countries, with Germany and the United Kingdom emerging as early adopters due to their robust manufacturing bases.

Asia‑Pacific

Asia‑Pacific exhibits rapid growth, driven by large‑scale AI data‑center rollouts and aggressive electrification strategies in China, Japan, and South Korea. Manufacturers are leveraging cost‑effective production capabilities to integrate AI‑optimized ribbon bonding into high‑volume modules. Strategic government programs supporting AI hardware innovation accelerate technology diffusion, though challenges remain in standardizing quality assurance across a diverse supplier ecosystem.

South America

South America is at an early stage of adoption, with pilot projects focusing on renewable‑energy‑linked AI systems and telecom infrastructure upgrades. The region’s market dynamics are shaped by modest R&D budgets and a reliance on imported equipment, yet growing awareness of the efficiency gains from AI‑enhanced bonding is prompting local players to form partnerships with established technology providers.

Middle East & Africa

In the Middle East & Africa, interest centers on high‑temperature, high‑reliability applications such as oil‑field AI monitoring and smart‑grid solutions. While overall market size is limited, targeted investments in AI‑centric hardware by sovereign wealth funds and telecom operators create niche opportunities for vendors that can demonstrate durability and performance under harsh operating conditions.

Report Scope

This market research report provides a comprehensive analysis of the AI-Optimized Ribbon Bonding for High-Current AI Power Modules Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI-Optimized Ribbon Bonding for High-Current AI Power Modules Market?

-> AI-Optimized Ribbon Bonding for High-Current AI Power Modules market is projected to grow from USD 0.90 billion in 2026 to USD 1.45 billion by 2034.

Which key companies operate in AI-Optimized Ribbon Bonding for High-Current AI Power Modules Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...