AI Optical Interconnect Market Insights

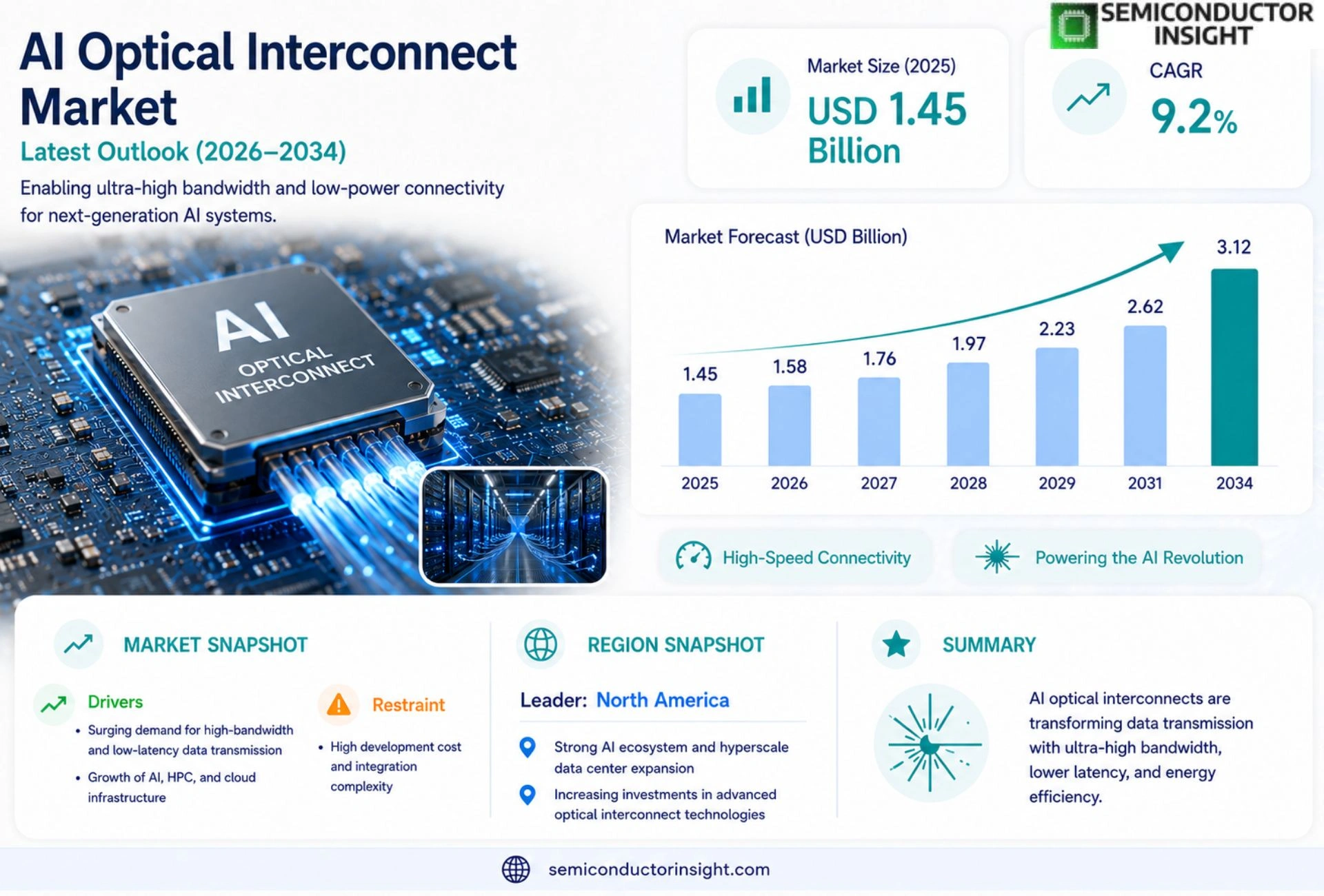

AI Optical Interconnect Market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.58 billion in 2026 to USD 3.12 billion by 2034, exhibiting a CAGR of 9.2% during the forecast period.

AI optical interconnect technologies employ silicon‑photonic waveguides, micro‑ring resonators and integrated lasers to transmit data using light rather than electrical signals. By converting electrical signals from GPUs or ASICs into photons, these solutions deliver ultra‑high bandwidth (exceeding terabits per second) while dramatically reducing latency and power consumption compared with traditional copper links.

The market is experiencing rapid expansion because generative‑AI workloads demand ever‑greater data‑center throughput and lower energy footprints. Furthermore, advances in CMOS‑compatible photonic manufacturing are driving cost reductions that make large‑scale deployment feasible. Initiatives by leading vendors are also accelerating adoption; for instance, in February 2024 Intel announced a strategic partnership with Lightmatter to co‑develop next‑generation photonic interconnect modules for hyperscale clouds. Cisco Systems, IBM Corp., Nvidia Corp., and Lumentum Holdings are among the key players delivering end‑to‑end solutions that span design, packaging and integration.

MARKET DRIVERS

Increasing Data Center Bandwidth Requirements

The rapid growth of AI workloads in hyperscale data centers is pushing demand for higher‑speed, low‑latency interconnects. AI Optical Interconnect Market solutions enable terabit‑per‑second links that keep pace with evolving model sizes, ensuring that compute resources are efficiently utilized.

Advancements in Photonic Integration

Recent breakthroughs in silicon photonics and heterogeneous integration are reducing component costs while improving power efficiency. These technological gains make it feasible for enterprises to replace traditional copper fabrics with optical alternatives, accelerating adoption across AI optical interconnect market.

➤ Industry analysts project that seamless optical links will become the de‑facto backbone for AI‑driven infrastructures within the next five years.

Coupled with strong OEM commitments and expanding standards for AI‑centric networking, these drivers collectively create a robust growth trajectory for the market.

MARKET CHALLENGES

High Initial Capital Expenditure

Deploying optical interconnects requires significant upfront investment in transceivers, waveguide assemblies, and specialized testing equipment. While the long‑term total cost of ownership improves, the initial outlay can deter smaller operators from early adoption.

Other Challenges

Manufacturing Complexity

Achieving consistent performance at scale demands precise lithography and stringent quality controls. Variability in process yields can increase lead times and affect supply reliability for AI optical interconnect market.

MARKET RESTRAINTS

Limited Skilled Workforce

The specialized nature of photonic design and integration creates a talent gap. Organizations often struggle to recruit engineers with combined expertise in optics, AI algorithms, and high‑speed signaling, which can slow product development cycles.

MARKET OPPORTUNITIES

Emerging AI Edge Applications

Growth of AI at the edge,such as autonomous vehicles, smart factories, and remote sensing,requires compact, low‑power optical links to overcome bandwidth bottlenecks. These niches present untapped avenues for AI optical interconnect market to expand beyond traditional data center environments.

AI Optical Interconnect Market Trends

Growing Demand from Generative AI Workloads

The surge in generative‑AI model training is reshaping data‑center architecture. Operators are seeking interconnect solutions that can sustain multi‑terabit per second throughput while keeping power budgets low. Silicon‑photonic waveguides combined with micro‑ring resonators now enable direct optical links between GPUs and ASICs, eliminating the electrical bottlenecks of traditional copper. As a result, latency drops dramatically and the overall energy consumption per bit is cut by more than half compared with legacy electrical connections. This performance shift is the primary catalyst driving adoption across hyperscale cloud providers. Data‑center operators report that optical links reduce cooling demand by up to 30 % per rack, translating into measurable OPEX savings. Early adopters such as major hyperscale providers have already migrated 20 % of their high‑performance computing fabric to optical solutions, citing improved scalability and lower latency as decisive factors.

Other Trends

Integration with CMOS Photonic Processes

CMOS‑compatible photonic manufacturing is reducing component costs and enabling volume production. Foundries now embed silicon waveguide layers directly within standard logic wafers, which shortens the supply chain and improves yield. The cost per optical module has fallen to a level comparable with high‑speed electrical transceivers, making large‑scale deployment economically viable. Moreover, the thermal stability of integrated lasers is improving, allowing data‑center racks to operate without additional cooling overhead. These manufacturing advances are solidifying the supply side and encouraging data‑center operators to replace legacy interconnects with optical alternatives. The integration of photonic components into standard CMOS lines also benefits from mature design automation tools, allowing chip designers to co‑optimize electrical and optical pathways. As yield improves, the price premium for photonic interconnects shrinks, encouraging even midsize data centers to consider upgrades.

Strategic Partnerships Accelerating Adoption

Leading semiconductor and photonics firms are forming joint ventures to accelerate time‑to‑market. In February 2024 Intel announced a strategic partnership with Lightmatter to co‑develop next‑generation photonic interconnect modules targeted at hyperscale cloud environments. Cisco and Lumen Technologies are integrating silicon‑photonic transceivers into their networking portfolios, while Nvidia’s AI accelerator roadmap now includes dedicated optical I/O paths. These collaborations reduce development risk and provide customers with end‑to‑end solutions that combine design, packaging, and integration expertise. For AI optical interconnect market, such alliances create a clear pathway for rapid scaling, ensuring that emerging AI workloads can be supported with the requisite bandwidth and energy efficiency. Analysts project that within the next five years, the majority of new AI‑focused data‑center builds will specify optical interconnects as a default option. This shift is reinforced by regulatory pressures on energy consumption, prompting operators to adopt greener connectivity solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Optical Interconnect Market: Competitive Overview

AI optical interconnect market is dominated by a handful of large silicon‑photonic vendors that have integrated photonic transceivers into data‑center ecosystems. Intel, leveraging its foundry capabilities and recent partnership with Lightmatter, leads the development of high‑density, CMOS‑compatible optical modules that target hyperscale cloud operators. Cisco Systems complements this effort with end‑to‑end networking solutions that embed optical interconnects into its switching portfolio, while Nvidia’s acquisition of Mellanox and its own photonic research position it as a key supplier of GPU‑centric optical links. Lumentum Holdings, as a major supplier of tunable lasers and passive components, provides the essential building blocks for these solutions, enabling terabit‑per‑second transmission with low power consumption. Collectively, these incumbents control a significant share of the market’s revenue and dictate the technology road‑map through extensive R&D investments and strategic alliances. These firms operate across the full value chain,from wafer‑scale photonic IC design to packaging and system integration,thereby creating high entry barriers for newcomers. Standardization efforts led by the Open Compute Project further consolidate the market around a few interoperable optical link specifications, reinforcing the dominance of the established players.

Beyond the tier‑one manufacturers, a diverse set of niche innovators contributes specialized IP and component portfolios that enable differentiated optical interconnect solutions. II‑VI Incorporated supplies high‑performance laser sources while Acacia Communications (now part of Juniper Networks) offers programmable coherent modules for long‑haul data‑center links. Marvell Technology (through its Inphi acquisition) focuses on silicon‑photonic engine ASICs that integrate transceiver functionality on a single die, reducing latency and cost. Broadcom’s acquisition of the optical‑interconnect business from Brocade adds switch‑level photonic ports to its Ethernet portfolio. Emerging startups such as Axsun Technologies and Ayar Labs are commercializing near‑invisibility silicon‑photonic transceivers for rack‑scale deployment, and Ciena’s optical‑packet‑switching platform incorporates AI‑enabled routing over photonic fabrics. Together, these players expand the ecosystem, fostering competition on performance, power efficiency and price, and they are positioned to capture market share as data‑center operators seek more granular, software‑defined interconnect options.

List of Key AI Optical Interconnect Companies Profiled

- Intel

- Cisco Systems

- Nvidia Corp.

- Lumentum Holdings

- Lightmatter

- IBM Corp.

- Broadcom Inc.

- Marvell Technology (Inphi)

- Axsun Technologies

- Ayar Labs

- Ciena Corp.

- Acacia Communications

- II‑VI Incorporated

- Juniper Networks

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Silicon Photonic Links

|

| By Application |

|

Data Center Interconnects

|

| By End User |

|

Hyperscale Cloud Providers

|

| By Architecture |

|

Multi‑Stage Switch Fabric

|

| By Deployment Model |

|

Managed Services

|

Regional Analysis: North America

North America

The expansion of data centers across North America is a primary driver. These facilities are increasingly reliant on high-speed optical interconnects to support the growing demand for data processing and storage associated with AI applications.

The North American HPC sector is actively seeking advanced optical interconnects to enhance the performance of AI-driven simulations and modeling. This is critical for scientific research and engineering applications.

Telecom providers in North America are upgrading their networks with optical interconnects to support the increasing bandwidth demands of AI applications and services. This is crucial for 5G and future network deployments.

North America boasts a vibrant ecosystem for AI chip development, directly influencing the demand for specialized AI optical interconnect solutions. Strong partnerships between chip manufacturers and optical component suppliers are fostering innovation.

North America

The market within North America is characterized by a strong focus on innovation and early adoption of advanced technologies. Several key players are investing heavily in research and development to create cutting-edge AI optical interconnect solutions. The region’s well-established supply chains and skilled workforce further support market growth. Government initiatives aimed at fostering technological advancement are also contributing to the expansion of AI optical interconnect market. The demand pipeline is robust, driven by ongoing investments in AI infrastructure and the increasing complexity of AI algorithms. The focus extends beyond just hardware to encompass software and system-level optimizations designed to maximize the performance of AI workflows. This creates a fertile ground for specialized solutions.

Europe

Europe presents a steadily growing market for AI Optical Interconnects, closely following North America’s advancements. Initiatives like the European Green Deal are emphasizing energy-efficient data centers, which indirectly drives demand for lower-power optical interconnects. The region’s emphasis on data privacy and security also influences the design and deployment of these technologies. Key areas of focus include AI applications in healthcare, finance, and manufacturing, creating targeted demand for specific optical interconnect solutions. The European Union’s investments in digital infrastructure are also contributing to market expansion.

Asia-Pacific

Asia-Pacific is poised to become the largest and fastest-growing market for AI Optical Interconnects. Driven by rapid adoption of AI across various industries, including e-commerce, manufacturing, and telecommunications, the region presents significant opportunities. China, in particular, is investing heavily in AI infrastructure and optical networking technologies. The region’s burgeoning data center industry and increasing demand for cloud computing services further fuel market growth. Government support for technological innovation is also a key factor in the region’s expansion. The sheer scale of the digital economy in Asia-Pacific creates immense potential for AI Optical Interconnects.

South America

South America represents an emerging market, with moderate growth potential for AI Optical Interconnects. The expansion of digital infrastructure and increasing adoption of cloud services are creating demand. E-commerce growth is a significant driver, requiring robust network connectivity to support online transactions. While the market is currently smaller compared to North America and Asia-Pacific, it presents attractive long-term opportunities. Government initiatives aimed at improving internet access and digital literacy are expected to contribute to future market expansion.

Middle East & Africa

The Middle East & Africa region is an early-stage market for AI Optical Interconnects but with promising growth prospects. Significant investments in digital transformation initiatives and the development of smart cities are driving demand. The region’s growing telecommunications sector is also contributing to market expansion. The increasing adoption of AI in sectors like oil and gas, finance, and healthcare is creating specific application-driven demand for optical interconnects. Infrastructure development projects are also playing a supportive role.

Report Scope

This market research report provides a comprehensive analysis of the AI Optical Interconnect Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Optical Interconnect Market?

-> AI optical interconnect market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.58 billion in 2026 to USD 3.12 billion by 2034.

Which key companies operate in AI Optical Interconnect Market?

-> Key players include Axalta Coating Systems, AkzoNobel, BASF SE, PPG, Sherwin-Williams, and 3M, among others.

What are the key growth drivers?

-> Key growth drivers include railway infrastructure investments, urbanization, and demand for durable coatings.

Which region dominates the market?

-> Asia-Pacific is the fastest-growing region, while Europe remains a dominant market.

What are the emerging trends?

-> Emerging trends include bio-based coatings, smart coatings, and sustainable rail solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...