AI-Native Network Processor Market Insights

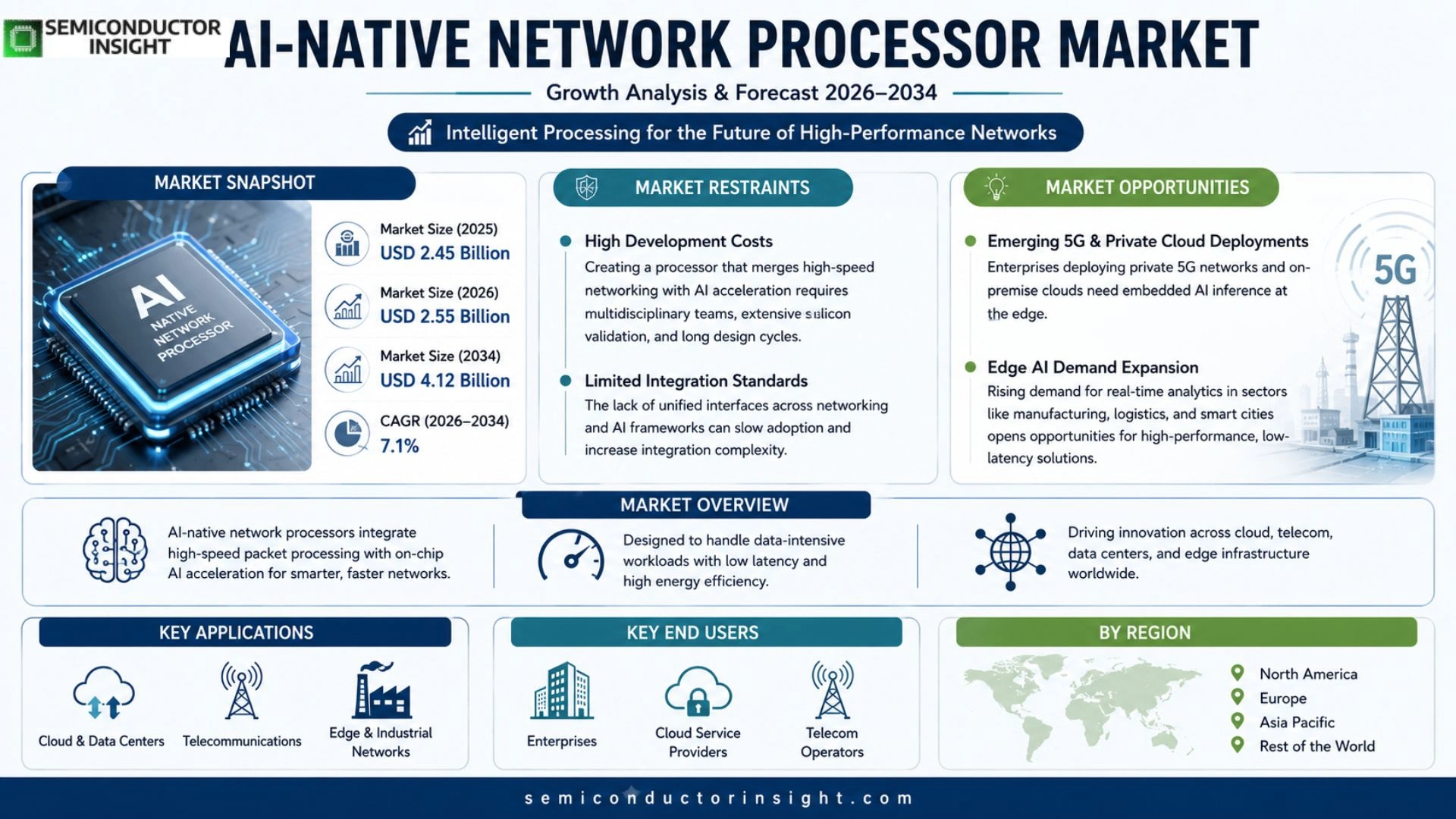

Global AI-Native Network Processor market size was valued at USD 2.45 billion in 2025. The market is projected to grow from USD 2.55 billion in 2026 to USD 4.12 billion by 2034, exhibiting a CAGR of 7.1% during the forecast period.

AI‑native network processors are specialized silicon designed to execute artificial‑intelligence workloads directly within networking equipment. They combine high‑throughput packet processing with tensor‑level inference capabilities, enabling functions such as intelligent routing, real‑time security analytics and edge inferencing without off‑loading data to separate accelerators.

The market momentum stems from surging data‑center traffic, escalating demand for low‑latency AI services and the rise of autonomous edge devices. Moreover, strategic collaborations,such as Nvidia’s March 2024 partnership with Microsoft Azure for AI‑enhanced networking and Intel’s introduction of its Agilex FPGA integrated with AI NPU,are expanding adoption across hyperscale operators and telecom carriers.

MARKET DRIVERS

Increasing Data‑Center Demand for Edge AI

The surge in real‑time analytics and inference workloads is forcing hyperscale operators to place AI capabilities closer to the source of data. AI‑Native Network Processor Market participants that can deliver sub‑microsecond latency while sustaining high throughput are seeing heightened interest from cloud providers seeking to differentiate their services. This trend is less about raw compute power and more about the ability to offload AI inference directly within the switching fabric, thereby reducing traffic overhead and operational expense.

Integration of Specialized ASICs in Telecom Infrastructure

Telecom operators are modernizing base stations to support massive‑MIMO and network‑slicing functions that rely heavily on on‑board AI acceleration. Processors that embed dedicated tensor cores within the packet‑processing pipeline enable operators to run predictive algorithms for traffic steering without external CPUs. This integration shortens the decision loop for dynamic resource allocation, which directly translates into higher network efficiency and new revenue streams.

➤ “When AI inference moves from the data‑center to the edge of the network, the value proposition shifts from sheer horsepower to intelligent traffic shaping.”

Summarily, the convergence of edge‑centric AI workloads and telecom‑grade ASIC adoption creates a feedback loop: higher demand for intelligent routing fuels deeper processor integration, which in turn accelerates the rollout of AI‑enhanced services across the AI‑Native Network Processor Market.

MARKET CHALLENGES

Performance‑Power Trade‑off

Designers are forced to balance raw inference speed against the thermal envelope of network equipment. While silicon advances permit higher FLOPS per watt, the cumulative power draw of densely packed line cards remains a limiting factor for tier‑1 carriers. Over‑engineering for peak performance can inflate OPEX, prompting some operators to favor incremental upgrades over wholesale processor replacement.

Other Challenges

Software Ecosystem Maturity

A fragmented set of SDKs and limited compiler support hampers rapid deployment of AI models. Vendors that provide a unified development stack, including model quantization tools and pre‑validated libraries, gain a decisive advantage because customers can reduce time‑to‑market and avoid costly integration projects.

MARKET RESTRAINTS

High Development Costs

Creating a processor that merges high‑speed networking with AI acceleration requires multidisciplinary teams, extensive silicon validation, and long design cycles. Capital outlays often exceed the thresholds of midsized OEMs, limiting market entry to a few well‑funded players.

Talent scarcity compounds the cost issue; engineers with expertise in both network ASIC design and AI workloads are rare, driving up salary premiums and extending recruitment timelines.

Regulatory scrutiny over data locality and security in multi‑tenant environments adds another layer of compliance expense, especially for providers operating across jurisdictions with divergent privacy statutes.

MARKET OPPORTUNITIES

Emerging 5G & Private Cloud Deployments

Enterprises establishing private 5G networks for manufacturing, logistics, and campus environments are seeking processors that can embed AI inference at the edge of the radio access network. The demand for on‑premise analytics creates a niche where AI‑Native Network Processor Market vendors can command premium pricing for tailored solutions that satisfy latency and security requirements.

Open‑source AI frameworks such as ONNX Runtime and TVM are gaining traction among network equipment manufacturers. When these runtimes are optimized for network‑processor instruction sets, integration time shrinks dramatically, opening a pathway for rapid adoption in cross‑industry verticals.

Geographic expansion into regions investing heavily in digital infrastructure,particularly Southeast Asia and Africa,offers untapped revenue. Local carriers, backed by government‑led broadband initiatives, are evaluating AI‑enhanced switches to future‑proof their networks, presenting a clear sales avenue for vendors willing to adapt to regional standards.

AI-Native Network Processor Market Trends

AI Functionality Embedded in Network Silicon

The most visible shift in the AI‑Native Network Processor Market is the migration of inference workloads from isolated accelerators to the packet‑processing plane itself. Modern silicon now couples line‑rate traffic handling with tensor engines, allowing decisions such as path selection, threat mitigation, or workload routing to be made within microseconds. This architectural convergence eliminates the latency penalty of shuttling data between a switch and a separate AI chip, a constraint that has historically limited real‑time analytics in high‑speed environments. For hyperscale data centers, the result is a smoother pipeline for AI‑driven services, where the network not only transports data but also augments it with contextual intelligence. Telecom operators similarly benefit, as the same processor can support both traditional routing and edge‑level inference for autonomous devices, reducing bill‑of‑materials and simplifying firmware stacks.

Other Trends

Strategic Alliances Fuel Rapid Adoption

Recent collaborations illustrate how ecosystem partnerships are delivering the necessary momentum for broader uptake. Nvidia’s March 2024 agreement with Microsoft Azure integrates an AI‑enhanced networking stack directly into Azure’s backbone, giving customers access to inference‑ready routing without bespoke hardware design. Intel’s roll‑out of Agilex FPGAs that embed an AI‑focused neural‑processing unit mirrors this approach, offering a programmable foundation that can be tuned for specific carrier or cloud workloads. These joint efforts lower the barrier to entry for organizations that lack in‑house silicon expertise, while also creating a feedback loop where software developers can target a common hardware abstraction. The practical upshot is a faster transition from pilot projects to production deployments across both cloud and telecom segments.

Edge‑Centric Intelligence Becomes a Core Service Offering

As autonomous devices proliferate at the network edge, the demand for localized AI processing has sharpened. Network processors that incorporate AI cores enable edge nodes to perform tasks such as video analytics, anomaly detection, or predictive maintenance without relying on distant cloud resources. This shift not only curtails round‑trip latency but also reduces bandwidth consumption, a critical consideration for operators managing massive IoT deployments. Companies that embed these capabilities into their routing platforms can monetize new service tiers,think real‑time video filtering for smart cameras or instant fraud detection for edge‑based payment terminals. Consequently, the AI‑Native Network Processor Market is seeing a diversification of revenue streams, where hardware sales are complemented by recurring software and support contracts tied to edge AI functionalities.

COMPETITIVE LANDSCAPE

Key Industry Players

AI‑Native Network Processor Market: Competitive Overview

The leadership tier is anchored by Nvidia, whose BlueField DPUs combine ASIC packet handling with integrated tensor cores, giving hyperscale operators a single‑chip solution for routing, security inspection and edge inference. Nvidia’s aggressive firmware roadmap and the Azure partnership have forced rivals to accelerate their own integration cycles, creating a tiered structure where the top three vendors,Nvidia, Intel and Broadcom,command the bulk of design wins in both data‑center and telecom deployments. Their scale enables multi‑year supply agreements and joint‑development programs that lock in ecosystems around common SDKs, effectively raising the entry barrier for smaller innovators.

Beyond the dominant trio, a cadre of niche specialists is carving out differentiated value. Marvell’s Octeon TX line targets programmable, low‑latency workloads for carrier‑grade routers, while Xilinx (now part of AMD) leverages its adaptive FPGA fabric to embed AI accelerators directly into network ASICs. Companies such as Pensando, Innovium and Netronome focus on disaggregated software‑defined networking stacks, offering customers the flexibility to retrofit existing chassis with AI‑ready processors. Emerging entrants like Cerebras Systems and Graphcore are experimenting with wafer‑scale engine concepts that could redefine throughput ceilings, though commercialization remains early. The breadth of approaches,from fixed‑function silicon to reconfigurable fabrics,suggests a market that will continue to reward architectural agility and close collaboration with cloud and telecom partners.

List of Key AI-Native Network Processor Companies Profiled

- Nvidia Corporation

- Intel Corporation

- Broadcom Inc.

- Marvell Technology Group Ltd.

- Advanced Micro Devices (AMD)

- Pensando Systems Inc.

- Innovium Inc.

- Netronome Systems Inc.

- Cerebras Systems Inc.

- Graphcore Ltd.

- Qualcomm Technologies Inc.

- Huawei Technologies Co., Ltd.

- Samsung Electronics Co., Ltd.

- MediaTek Inc.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

ASIC‑Based Processors

|

| By Application |

|

Data‑Center Networking

|

| By End User |

|

Cloud Service Providers

|

| By Functionality |

|

Intelligent Routing

|

| By Deployment Model |

|

Cloud‑Native

|

Regional Analysis: AI-Native Network Processor Market

Silicon designers in the United States and Canada are experimenting with heterogeneous architectures that blend traditional packet‑processing pipelines with AI accelerators. By co‑locating inference engines beside ASIC switches, vendors reduce data movement costs and unlock new use‑cases such as real‑time video analytics at the network edge. This approach is gaining traction among carriers seeking to differentiate their 5G services.

The North American ecosystem benefits from vertically integrated fabs and advanced packaging facilities, which shorten time‑to‑market for AI‑enhanced chips. Close proximity between design houses and manufacturing sites also eases risk mitigation when new process nodes are introduced, ensuring a steadier flow of production capacity.

Policy frameworks emphasize both national security and innovation incentives, prompting a wave of public‑private partnerships. Grants aimed at AI‑driven networking solutions stimulate early‑stage R&D, while export‑control guidelines shape how companies approach global collaborations.

Universities and research labs in the region produce a pipeline of engineers fluent in both machine learning and high‑speed digital design. This cross‑disciplinary talent pool underpins the rapid prototyping cycles that characterize the market’s evolution.

Europe

European manufacturers leverage strong standards‑driven networks to position AI‑Native Network Processors as enablers of open‑source interoperability. Collaborative consortia such as the European Telecoms Technology Forum drive consensus on APIs that allow multiple vendors to integrate AI capabilities without locking into a single silicon provider. At the same time, policy initiatives that fund AI research in conjunction with communications infrastructure create a fertile environment for startups focused on security‑first, edge‑oriented processors. The region’s nuanced balance between regulation and innovation encourages operators to adopt modular solutions that can be upgraded as AI models evolve.

Asia‑Pacific

In Asia‑Pacific, the market is shaped by the sheer scale of mobile traffic and the urgency of 5G rollouts. Companies in China, South Korea, and Japan are embedding AI accelerators into base‑station hardware to manage massive uplink streams while performing on‑the‑fly analytics. The competitive pressure of regional carriers fuels a race to integrate proprietary neural‑network kernels directly into network processors, seeking to reduce latency for immersive applications. Meanwhile, governmental subsidies for AI‑driven networking infrastructure accelerate adoption across both private and public sectors.

South America

South American operators are increasingly viewing AI‑Native Network Processors as a lever to bridge the digital divide in remote locations. By deploying edge‑centric processors that combine inference with routing, providers can deliver localized content recommendation and predictive maintenance without relying on distant cloud resources. The regional push for sovereign technology, driven by concerns over data residency, encourages partnerships with local design firms that tailor AI models to specific linguistic and cultural contexts.

Middle East & Africa

The Middle East & Africa region is witnessing a strategic shift toward AI‑enabled networking as part of broader smart‑city initiatives. Investments in high‑capacity undersea cables and satellite backbones are complemented by the deployment of AI‑Native Network Processors that can dynamically adjust routing based on real‑time traffic patterns and security threats. Emerging market entrants are attracted by the promise of reduced operational expenditures, while governments view the technology as a catalyst for digital transformation across sectors ranging from finance to energy.

Report Scope

This market research report provides a comprehensive analysis of the AI-Native Network Processor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI-Native Network Processor Market?

-> AI-Native Network Processor market is projected to grow from USD 2.55 billion in 2026 to USD 4.12 billion by 2034, exhibiting a CAGR of 7.1%

Which key companies operate in AI-Native Network Processor Market?

-> Key players include NVIDIA, Intel, Broadcom, Marvell Technology Group, Qualcomm, and Xilinx (AMD), among others.

What are the key growth drivers?

-> Key growth drivers include surging data‑center traffic, rising demand for low‑latency AI services, proliferation of edge inferencing, and strategic collaborations such as Nvidia‑Microsoft Azure and Intel‑Agilex FPGA integrations.

Which region dominates the market?

-> North America holds a significant share due to early adoption of AI‑enhanced networking, while Asia‑Pacific is emerging as the fastest‑growing region driven by robust semiconductor manufacturing and telecom investments.

What are the emerging trends?

-> Emerging trends include integration of AI NPUs into ASICs, development of AI‑optimized network silicon, increased edge AI deployments, and the rise of AI‑enabled security analytics within network processors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...