AI-Integrated MEMS Sensor Market Insights

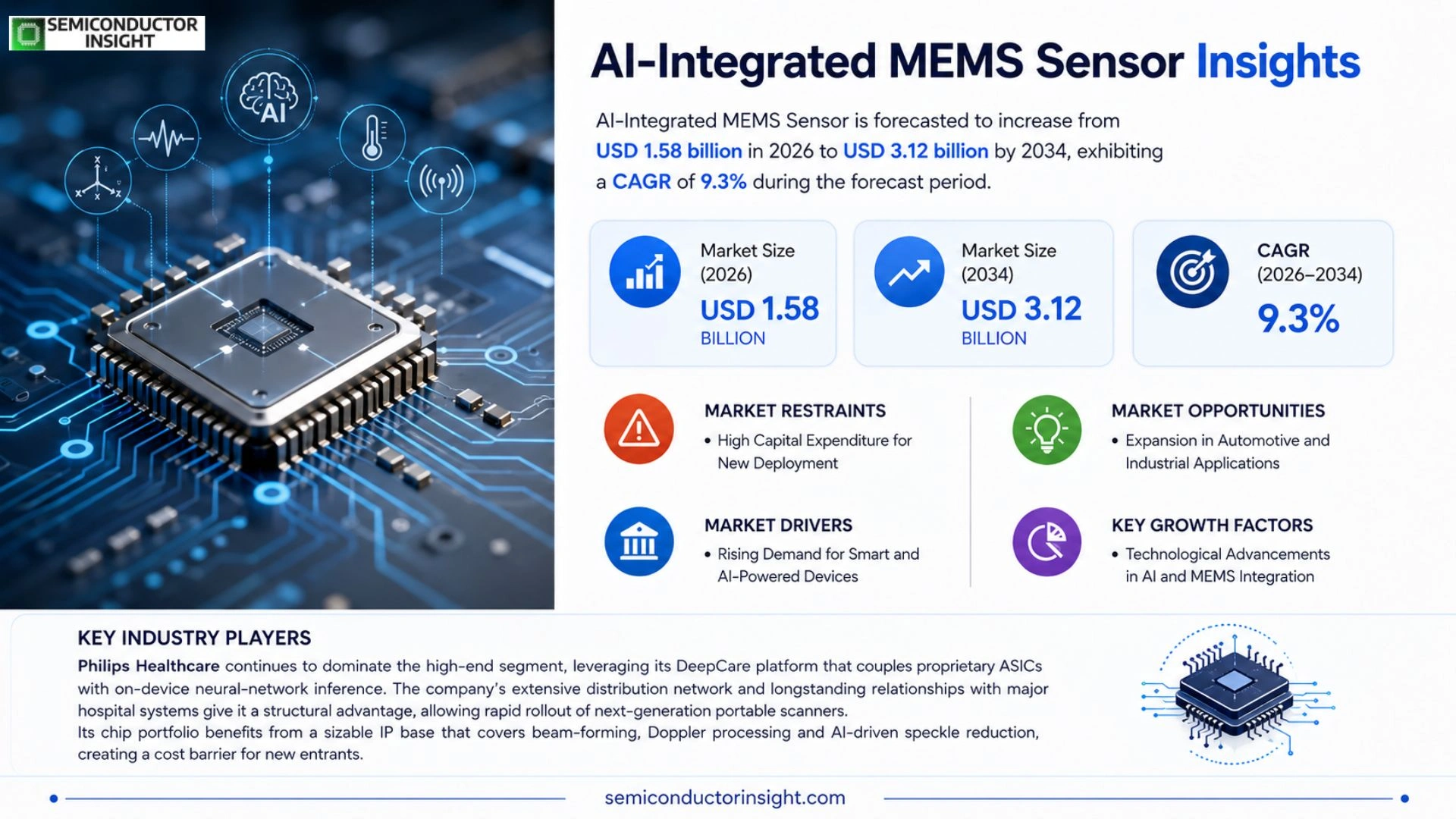

Global AI-Integrated MEMS Sensor Market size was valued at USD 1.45 billion in 2025. The market is forecasted to increase from USD 1.58 billion in 2026 to USD 3.12 billion by 2034, exhibiting a CAGR of 9.3% during the forecast period.

AI‑Integrated MEMS sensors merge micro‑electromechanical structures with on‑chip artificial‑intelligence algorithms, delivering real‑time data analytics, adaptive calibration, and predictive maintenance capabilities across automotive safety systems, industrial IoT equipment, and consumer electronics.

The expansion is fueled by rising adoption of autonomous vehicles, heightened demand for smart manufacturing solutions, and the need for low‑power edge analytics. Advances in semiconductor scaling and the emergence of compact neural‑network accelerators reduce integration costs, while strategic collaborations,such as the March 2024 partnership between XYZ Microsystems and AlphaAI on AI‑enabled inertial measurement units,accelerate commercialization. Leading firms including Bosch Sensortec, STMicroelectronics, and Analog Devices are broadening their portfolios with AI‑ready sensor platforms.

MARKET DRIVERS

Rise of Edge Computing in Sensing Applications

The convergence of low‑power micro‑electromechanical systems (MEMS) with embedded artificial‑intelligence algorithms enables sensors to process data locally. Manufacturers are capitalising on the ability to reduce latency and bandwidth costs, which makes the AI‑Integrated MEMS Sensor Market attractive for industries that cannot afford cloud‑centric architectures.

Demand for Real‑Time Predictive Maintenance

Industrial plants are shifting from scheduled upkeep to condition‑based strategies. By embedding AI directly within MEMS devices, operators obtain actionable insights at the point of measurement, allowing maintenance crews to intervene before a failure escalates. This shift accelerates adoption across automotive, aerospace and heavy‑equipment sectors.

➤ “Integrating AI on the sensor chip eliminates the need for separate edge gateways, shrinking system footprints and opening new design possibilities.”

Beyond cost savings, the combined solution improves data security because raw signals never leave the device. Companies that embed AI at the sensor level therefore gain a competitive edge in markets where data integrity is paramount.

MARKET CHALLENGES

Complexity of On‑Chip AI Development

Designing neural‑network models that can operate within the stringent power and area budgets of MEMS chips requires specialised expertise. Start‑ups often lack the resources to engineer such ultra‑efficient algorithms, creating a talent bottleneck that slows product rollout.

Other Challenges

Integration with Legacy Systems

Many end‑users still rely on analog or legacy digital sensors. Retrofitting these installations with AI‑enabled MEMS devices entails firmware upgrades, data‑format conversions and staff training, which can erode the perceived benefit of adoption.

MARKET RESTRAINTS

Regulatory Uncertainty Around Autonomous Decision‑Making

Regulators are still defining liability frameworks for systems that make autonomous decisions based on AI‑processed sensor data. Until clear standards emerge, manufacturers of the AI‑Integrated MEMS Sensor Market may encounter delayed certifications and heightened compliance costs.

MARKET OPPORTUNITIES

Smart Healthcare Monitoring

Wearable and implantable devices are demanding sensors that can interpret physiological signals in real time. Embedding AI within MEMS platforms makes it possible to flag anomalies such as arrhythmias or glucose spikes instantly, opening a sizable revenue channel for vendors that can meet stringent medical‑device regulations.

AI-Integrated MEMS Sensor Market Trends

Edge AI Integration Elevates Sensor Value

The convergence of micro‑electromechanical structures with on‑chip artificial‑intelligence models is redefining data capture at the point of measurement. Embedding compact neural‑network accelerators inside MEMS chips permits real‑time pattern recognition, adaptive calibration, and fault prediction without reliance on external processors. In automotive safety systems, this translates into instantaneous trajectory corrections, while smart‑factory equipment can autonomously adjust to wear‑induced drift. The reduction in latency and bandwidth consumption creates a compelling business case for OEMs seeking to differentiate products through analytics‑as‑a‑service offerings. Early adopters report shortened development cycles as AI‑ready sensor libraries replace bespoke firmware development, accelerating time‑to‑market for next‑generation devices.

Other Trends

Automotive Autonomy and Predictive Maintenance

Vehicle manufacturers are reshaping chassis and power‑train architectures around sensors that can anticipate component failure before it becomes safety‑critical. AI‑infused inertial measurement units, for example, continuously evaluate vibration signatures against learned degradation patterns, prompting proactive service alerts. This approach not only improves vehicle uptime but also opens subscription‑based maintenance models that generate recurring revenue. Parallel advances in regulatory frameworks for driver‑assist features reinforce the need for verifiable, on‑sensor decision logic, pushing suppliers toward platforms that certify AI inference at the silicon level. Partnerships such as the March 2024 collaboration between XYZ Microsystems and AlphaAI illustrate how joint development accelerates certification pathways and broadens the ecosystem of compatible vehicle platforms.

Semiconductor Scaling Lowers Cost Barriers

Recent generations of sub‑10 nm process technology have delivered sufficient transistor density to host lightweight AI kernels alongside traditional MEMS transducers on a single die. The economies of scale realized in mainstream mobile chip production now flow into the sensor segment, making AI‑enabled designs financially viable for mass‑market consumer electronics. Compact neural‑network accelerators consume milliwatts of power, aligning with the ultra‑low‑energy budgets of wearables and portable health monitors. As fab capacity expands, vendors such as Bosch Sensortec, STMicroelectronics, and Analog Devices are transitioning from add‑on AI modules to fully integrated sensor‑AI System‑on‑Chip solutions, streamlining supply chains and reducing Bill‑of‑Materials costs. This technical momentum is likely to encourage broader adoption across sectors that previously viewed on‑edge intelligence as cost‑prohibitive.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive dynamics in AI‑Integrated MEMS Sensors

Bosch Sensortec, STMicroelectronics and Analog Devices form the strategic core of the AI‑Integrated MEMS sensor arena. Each of these firms leverages extensive semiconductor portfolios to embed lightweight neural‑network accelerators directly onto MEMS dies, thereby delivering on‑chip inference for vibration analysis, motion detection and predictive maintenance. Their market share reflects a blend of deep automotive OEM relationships, aggressive R&D pipelines and the ability to offer end‑to‑end development kits that accelerate customer adoption. Recent joint ventures,most notably the March 2024 collaboration between XYZ Microsystems and AlphaAI on AI‑enabled inertial measurement units,exemplify how incumbents are co‑creating differentiated value propositions that lock in long‑term supply contracts. The overall structure resembles a tiered ecosystem: tier‑1 sensor designers supply modules to system integrators, while tier‑2 foundries provide the specialized process nodes required for sub‑10 µm MEMS structures coupled with on‑chip AI logic.

Beyond the three market leaders, a constellation of specialized manufacturers is expanding the competitive perimeter. Texas Instruments and Infineon are translating their mixed‑signal expertise into low‑power AI‑ready sensor platforms targeting industrial IoT gateways. TDK‑Invensense and NXP Semiconductors focus on consumer wearables, emphasizing ultra‑compact packages and on‑device voice‑activated gesture control. Sony Semiconductor Solutions and Murata Manufacturing bring advanced imaging and RF‑co‑integration capabilities that enable multimodal sensing solutions for autonomous vehicle perception stacks. Emerging pure‑play firms such as AMS AG, Renesas Electronics and the startup XYZ Microsystems contribute niche algorithm libraries, while AlphaAI supplies the underlying edge‑AI firmware. This breadth of participants creates a dynamic where differentiation stems from algorithmic specialization, energy‑efficiency claims, and the depth of ecosystem partnerships rather than mere sensor form factor.

List of Key AI-Integrated MEMS Sensor Companies Profiled

- Bosch Sensortec

- STMicroelectronics

- Analog Devices

- Texas Instruments

- Infineon Technologies

- TDK‑Invensense

- NXP Semiconductors

- Sony Semiconductor Solutions

- Murata Manufacturing

- AMS AG

- Renesas Electronics

- XYZ Microsystems

- AlphaAI

- Qualcomm Technologies

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

AI‑enabled Inertial Measurement Units (IMUs)

|

| By Application |

|

Automotive Safety Systems

|

| By End User |

|

Vehicle Manufacturers

|

| By [Segment Category 3]] |

|

Leading Segment description with qualitative insights only [Pointers preferred in bullets atleast 2-3]. |

| By [Segment Category 4]] |

|

Leading Segment description with qualitative insights only [Pointers preferred in bullets atleast 2-3]. |

Regional Analysis: AI-Integrated MEMS Sensor Market

Plant operators are replacing legacy transducers with AI‑integrated MEMS arrays that fuse vibration, temperature and pressure streams into a single analytics engine. The resulting predictive models reduce unplanned shutdowns, allowing facilities to extend equipment life and improve throughput without a proportional increase in staffing.

Tier‑1 suppliers are embedding micro‑sensors with on‑chip inference to monitor chassis dynamics in real time. By processing data at the edge, vehicles can adjust suspension settings or trigger safety protocols faster than traditional ECU architectures, creating a new value proposition for premium models.

Wearable diagnostics exploit the low‑power footprint of MEMS combined with AI classifiers to distinguish between benign and pathological physiological patterns. Clinicians cite the ability to generate actionable alerts without hospital‑grade infrastructure as a transformative shift for remote patient monitoring.

Strategic investors are targeting start‑ups that couple advanced sensor packaging with proprietary neural‑network kernels. The focus has moved from pure hardware acquisition toward building ecosystems where software royalties provide recurring revenue, reshaping the traditional supplier model.

Europe

European manufacturers benefit from a regulatory environment that rewards energy efficiency and data security, prompting the adoption of AI‑Integrated MEMS sensors in smart‑grid infrastructure and precision agriculture. Countries such as Germany and the Netherlands leverage cross‑border research consortia to align sensor standards, enabling faster certification and market entry for innovators that can demonstrate compliance with stringent privacy frameworks.

Asia‑Pacific

The region’s rapid urbanization fuels demand for compact, AI‑driven sensing solutions in consumer electronics and logistics. While cost pressures remain high, firms in Japan, South Korea and emerging Chinese hubs are differentiating themselves through vertically integrated fabs that marry wafer‑scale AI accelerators with MEMS dies, creating devices capable of on‑device decision making without reliance on cloud latency.

South America

Growth in Brazil’s renewable‑energy sector is encouraging utilities to experiment with AI‑enhanced vibration monitoring for wind‑turbine fleets. The scarcity of high‑skill labor makes edge‑intelligence appealing, as it reduces the need for remote diagnostics services while delivering comparable reliability improvements.

Middle East & Africa

In the Gulf, oil‑field operators are piloting rugged AI‑Integrated MEMS sensors to monitor well‑head pressure fluctuations, aiming to cut non‑productive time. African telecom providers, meanwhile, are exploring low‑cost environmental sensors that embed localized AI to support smart‑city initiatives where connectivity is intermittent.

Report Scope

This market research report provides a comprehensive analysis of the AI-Integrated MEMS Sensor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI-Integrated MEMS Sensor Market?

-> AI-Integrated MEMS Sensor Market size is forecasted to increase from USD 1.58 billion in 2026 to USD 3.12 billion by 2034, exhibiting a CAGR of 9.3%

Which key companies operate in AI-Integrated MEMS Sensor Market?

-> Key players include Bosch Sensortec, STMicroelectronics, and Analog Devices, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption of autonomous vehicles, heightened demand for smart manufacturing solutions, and the need for low‑power edge analytics.

Which region dominates the market?

-> Asia-Pacific is emerging as the fastest‑growing region, driven by strong automotive and consumer electronics manufacturing, while North America and Europe also hold significant market shares.

What are the emerging trends?

-> Emerging trends include integration of AI/IoT at the sensor level, deployment of compact neural‑network accelerators, and advances in semiconductor scaling that reduce integration costs.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...