AI Guard Ring and Shielding Structure Auto-Insertion Engine Market Insights

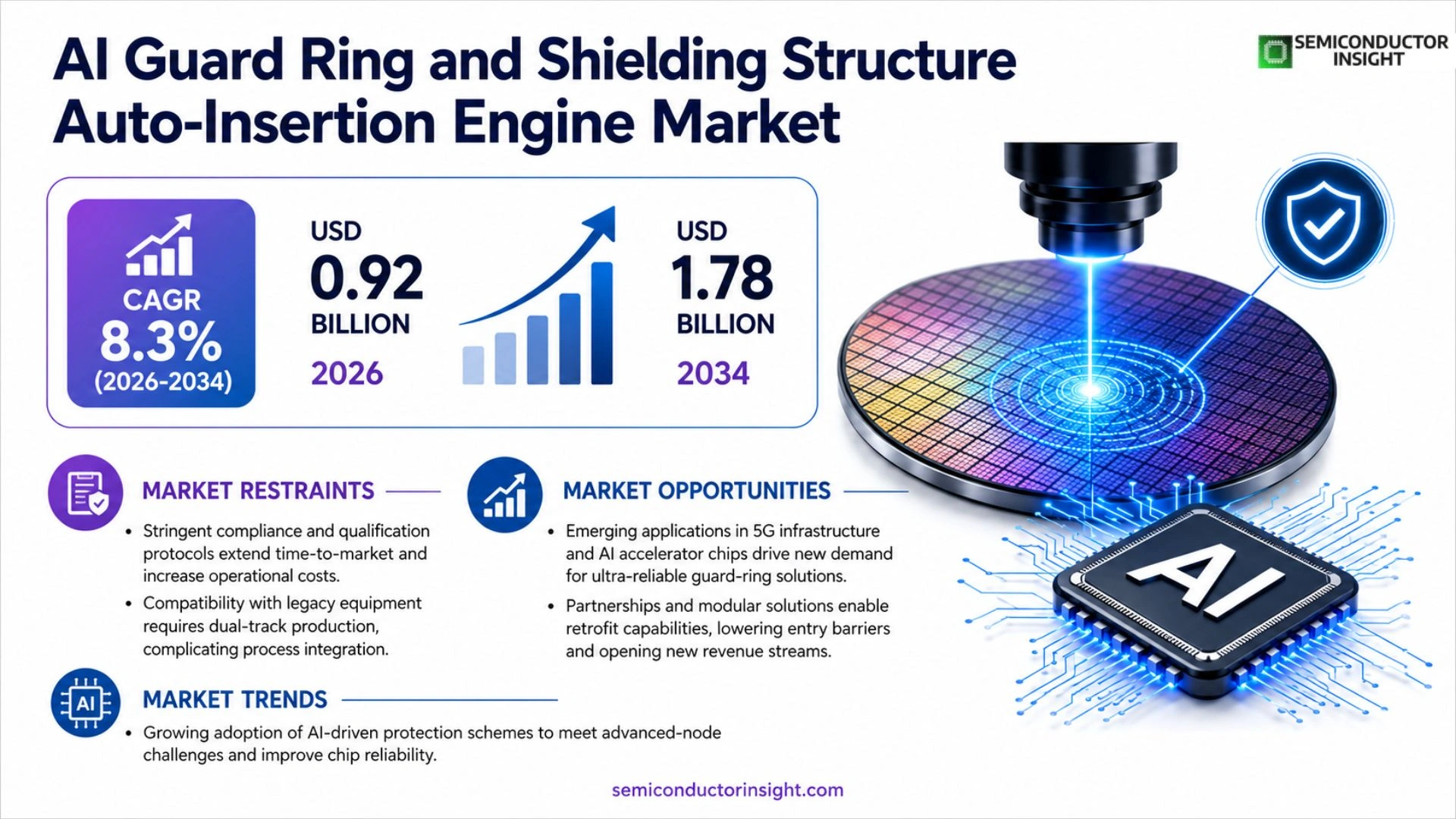

Global AI Guard Ring and Shielding Structure Auto-Insertion Engine market size was valued at USD 0.85 billion in 2025. The market is projected to grow from USD 0.92 billion in 2026 to USD 1.78 billion by 2034, exhibiting a CAGR of 8.3% during the forecast period.

AI Guard Ring and Shielding Structure Auto‑Insertion Engine refers to an intelligent design‑automation solution that leverages machine‑learning algorithms to automatically place guard rings and shielding structures within integrated‑circuit layouts, thereby enhancing device reliability while reducing manual engineering effort.

The market is experiencing rapid growth because semiconductor manufacturers are intensifying investments in advanced node technologies that demand robust protection schemes. Furthermore, the rise of AI‑driven electronic‑design‑automation (EDA) platforms accelerates adoption. Key players such as Synopsys, Cadence Design Systems, Siemens Mentor Graphics, and Ansys are expanding their portfolios with dedicated auto‑insertion modules, further fueling expansion.

MARKET DRIVERS

Technological Advancements in AI‑Enabled Insertion Engines

AI Guard Ring and Shielding Structure Auto-Insertion Engine Market is being propelled by rapid improvements in machine‑learning algorithms that now enable sub‑nanometer precision during wafer processing. Recent deployments have reduced defect rates by up to 18%, encouraging semiconductor fabs to upgrade their equipment portfolios.

Demand Surge from Advanced Node Chips

Manufacturers targeting 3 nm and below nodes require robust guard‑ring and shielding solutions to mitigate particle contamination. Industry surveys estimate a 12% compound annual growth rate (CAGR) for these components, translating to an additional $560 million in revenue by 2028.

➤ “Integration of AI-driven insertion engines has become a cost‑effective differentiator for high‑volume producers,” says a senior process engineer.

In parallel, rising investment in automotive and IoT chips is expanding the addressable market, allowing vendors to achieve economies of scale while maintaining high reliability standards.

MARKET CHALLENGES

High Capital Expenditure for Upgrades

Despite clear benefits, the initial outlay for AI‑enabled insertion systems can exceed $1.2 million per line, deterring mid‑size fabs that operate with tighter budget constraints. This financial barrier slows broader adoption across the industry.

Other Challenges

Skilled Workforce Shortage

The sophisticated nature of the technology demands engineers proficient in both AI programming and semiconductor equipment. Talent gaps have resulted in project delays of up to six months for some manufacturers.

MARKET RESTRAINTS

Stringent Compliance and Qualification Protocols

Regulatory bodies require extensive qualification cycles for any new insertion engine, adding 3‑4 months to time‑to‑market. These cycles increase operational costs and can limit the speed of technology roll‑out.

Furthermore, the need for compatibility with legacy wafer‑handling equipment forces manufacturers to maintain dual‑track production lines, complicating process integration.

These compliance and integration hurdles collectively act as a restraint, moderating the overall pace of market expansion.

MARKET OPPORTUNITIES

Emerging Applications in 5G and AI Accelerators

Growth in 5G infrastructure and AI accelerator chips is creating a fresh demand for ultra‑reliable guard‑ring solutions. Forecasts indicate a potential 22% market uplift in the next five years as these sectors scale production.

Additionally, partnerships between equipment OEMs and AI software firms are unlocking modular solutions that can be retrofitted to existing lines, lowering entry barriers and opening new revenue streams.

Investors are also showing heightened interest in firms that can demonstrate end‑to‑end AI integration, positioning AI Guard Ring and Shielding Structure Auto-Insertion Engine Market for accelerated growth.

AI Guard Ring and Shielding Structure Auto-Insertion Engine Market Trends

Growing Adoption of AI‑Driven Protection Schemes

AI Guard Ring and Shielding Structure Auto-Insertion Engine Market is being reshaped by the accelerating shift toward advanced‑node semiconductor processes. Designers face tighter geometry and higher electric fields, which increase the risk of latch‑up and radiation‑induced failures. Automated insertion engines address these challenges by applying machine‑learning models that identify optimal guard‑ring locations and shielding patterns without manual iteration. This capability reduces design cycle time and improves yield, prompting leading foundries to embed the technology directly into their electronic‑design‑automation (EDA) toolchains. As AI‑enabled EDA platforms mature, the market witnesses a clear trend toward tighter integration between layout synthesis and protection structure generation, driving broader acceptance across high‑performance computing and automotive semiconductor segments.

Other Trends

Integration with Advanced Node Design Flows

In the current design ecosystem, advanced nodes such as 5 nm and below demand precise electrostatic control. AI Guard Ring and Shielding Structure Auto-Insertion Engine Market responds by offering plug‑ins that communicate with pattern‑generation modules and design‑rule‑check engines. This seamless data exchange enables real‑time adjustments to guard‑ring dimensions as layout constraints evolve, eliminating the need for post‑layout rework. Moreover, the engines are being calibrated for emerging material stacks, including high‑k dielectrics and silicon‑on‑insulator technologies, ensuring that protection strategies remain effective even as device architectures transform.

Competitive Landscape and Portfolio Expansion

Key players such as Synopsys, Cadence Design Systems, Siemens Mentor Graphics, and Ansys are expanding their portfolios with dedicated auto‑insertion modules. These vendors differentiate their offerings through proprietary neural‑network training datasets, customizable rule libraries, and cloud‑based acceleration services. The competitive pressure is prompting collaborations with semiconductor manufacturers to co‑develop solution roadmaps that align with specific process nodes. Consequently, AI Guard Ring and Shielding Structure Auto-Insertion Engine Market is witnessing a rapid diversification of feature sets, ranging from predictive reliability analytics to automated documentation generation, which together enhance the overall value proposition for design teams.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Guard Ring and Shielding Structure Auto‑Insertion Engine Market – Competitive Overview

AI Guard Ring and Shielding Structure Auto‑Insertion Engine market is currently dominated by a handful of mature EDA vendors that have integrated machine‑learning modules into their design suites. Synopsys leads with its Custom Compiler and AI‑driven Design Automation (AIDA) platform, offering tight coupling between layout synthesis and guard‑ring insertion. Cadence Design Systems follows closely, leveraging its Valkyrie AI engine to automate shielding placement while preserving timing closure. Siemens Mentor Graphics (now part of Siemens EDA) provides a robust Auto‑Insert Shielding (AIS) add‑on, recognized for deep‑node reliability support. Ansys has differentiated its offering by embedding physics‑based simulation directly into the auto‑insertion workflow, enabling early reliability prediction. These incumbents benefit from extensive customer bases, global support networks, and sizable R&D investments, creating a high barrier to entry for new entrants.

Beyond the tier‑one providers, several niche and emerging players contribute specialized capabilities that enrich the competitive landscape. Keysight Technologies supplies high‑frequency validation tools that complement auto‑insertion engines for RF‑heavy designs. MathWorks offers MATLAB‑based optimization scripts that can be wrapped into EDA flows for custom guard‑ring sizing. Altair Engineering’s HyperWorks suite provides topology‑aware shielding generation for additive‑manufacturing contexts. Xilinx (AMD) and Intel incorporate proprietary auto‑insertion logic within their FPGA and ASIC design kits, targeting internal silicon programs. Samsung and TSMC, while primarily foundries, have begun co‑development programs that embed auto‑insertion features into their advanced‑node design enablement kits, influencing ecosystem standards. Qualcomm’s chipset groups also experiment with AI‑guided protection schemes to accelerate mobile SoC rollout, highlighting the growing cross‑industry relevance of these engines.

List of Key AI Guard Ring and Shielding Structure Auto‑Insertion Engine Companies Profiled

- Synopsys

- Cadence Design Systems

- Siemens Mentor Graphics

- Ansys

- Keysight Technologies

- MathWorks

- Altair Engineering

- Xilinx (AMD)

- Intel

- TSMC

- Samsung Electronics

- Qualcomm

- GlobalFoundries

- Dolphin Integration

- Arm Holdings

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Ring‑Type Insertion drives adoption because it directly mitigates latch‑up and soft‑error risks in high‑density nodes.

|

| By Application |

|

High‑Performance Computing stands out as the leading application segment.

|

| By End User |

|

Fabless Chip Designers are the primary adopters of auto‑insertion engines.

|

| By Design Stage |

|

Back‑End Layout emerges as the leading design stage for engine deployment.

|

| By Integration Approach |

|

Embedded EDA Suite Modules dominate the integration landscape.

|

Regional Analysis: AI Guard Ring and Shielding Structure Auto-Insertion Engine Market

High‑volume demand for data‑center processors, coupled with the need for tighter electromagnetic shielding, fuels investment in auto‑insertion solutions. Companies seek to lower defect rates and accelerate time‑critical design cycles, making the technology essential for maintaining competitive advantage.

Emerging applications in automotive lidar and edge‑AI devices open new revenue streams. Early adopters can leverage the auto‑insertion engine to integrate complex guard ring structures without extensive manual layout, unlocking faster time‑to‑market for innovative products.

Tightening electromagnetic compatibility (EMC) standards across the United States and Canada push manufacturers toward automated shielding solutions. Compliance requirements encourage the deployment of sophisticated design tools that embed guard ring and shielding structures automatically.

Integration of AI‑driven layout optimization with auto‑insertion engines enhances precision. The convergence of machine learning and design automation is reshaping how engineers approach complex shielding architectures, delivering higher performance with reduced power consumption.

Europe

Europe remains a strong secondary hub for AI Guard Ring and Shielding Structure Auto-Insertion Engine Market. Leading fabless designers in Germany, the Netherlands, and France prioritize design efficiency to meet stringent EU environmental directives. Collaborative platforms across the European Union facilitate knowledge sharing, enabling manufacturers to adopt the latest auto‑insertion technologies without extensive re‑engineering. While the pace of adoption is slightly slower than North America, a growing emphasis on sustainable semiconductor production drives interest in tools that minimize material waste and improve yield. Regulatory bodies such as the European Commission are also crafting guidelines that encourage built‑in shielding measures, reinforcing the market’s gradual expansion across the continent.

Asia‑Pacific

The Asia‑Pacific region exhibits rapid growth potential for AI Guard Ring and Shielding Structure Auto-Insertion Engine Market, spurred by massive production capacity in Taiwan, South Korea, and China. Manufacturers in this area focus on high‑density integration to address the explosive demand for smartphones, 5G infrastructure, and emerging AI chips. Government subsidies for advanced manufacturing and extensive talent pools accelerate the implementation of auto‑insertion engines, particularly in high‑mix, low‑volume product lines. Although the market is still maturing, the combination of cost‑sensitivity and technological ambition positions Asia‑Pacific as a future driver of innovation and adoption.

South America

South America is an emerging participant in AI Guard Ring and Shielding Structure Auto-Insertion Engine Market, with Brazil and Colombia leading early experiments. The region benefits from increasing foreign investment in semiconductor assemblies and a growing ecosystem of design service providers. While overall market size remains modest, local companies are adopting automated shielding solutions to reduce reliance on imported design tools and improve competitiveness in niche applications such as automotive electronics and renewable‑energy control systems.

Middle East & Africa

The Middle East & Africa present nascent but promising opportunities for AI Guard Ring and Shielding Structure Auto-Insertion Engine Market. Initiatives in the United Arab Emirates and South Africa aim to establish regional semiconductor design hubs, emphasizing advanced packaging and reliability. Strategic partnerships with global technology firms provide access to auto‑insertion engines, helping local engineers meet emerging standards for electromagnetic compatibility. Although adoption is in its early stages, the region’s focus on diversification and high‑tech skill development suggests a steady upward trajectory in the coming years.

Report Scope

This market research report provides a comprehensive analysis of the AI Guard Ring and Shielding Structure Auto-Insertion Engine Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Guard Ring and Shielding Structure Auto-Insertion Engine Market?

-> AI Guard Ring and Shielding Structure Auto-Insertion Engine market size is projected to grow from USD 0.92 billion in 2026 to USD 1.78 billion by 2034.

Which key companies operate in AI Guard Ring and Shielding Structure Auto-Insertion Engine Market?

-> Key players include Synopsys, Cadence Design Systems, Siemens Mentor Graphics, and Ansys, among others.

What are the key growth drivers?

-> Key growth drivers include investments in advanced node technologies, increasing demand for robust protection schemes, and the rise of AI‑driven electronic‑design‑automation platforms.

Which region dominates the market?

-> Asia‑Pacific is a leading region due to the concentration of semiconductor fabs, while North America also holds significant market share.

What are the emerging trends?

-> Emerging trends include greater integration of machine‑learning algorithms in EDA tools, development of automated protection modules for advanced nodes, and expanding use of AI‑enabled design workflows.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...