AI-Enabled FPGA-Based Prototyping Market Insights

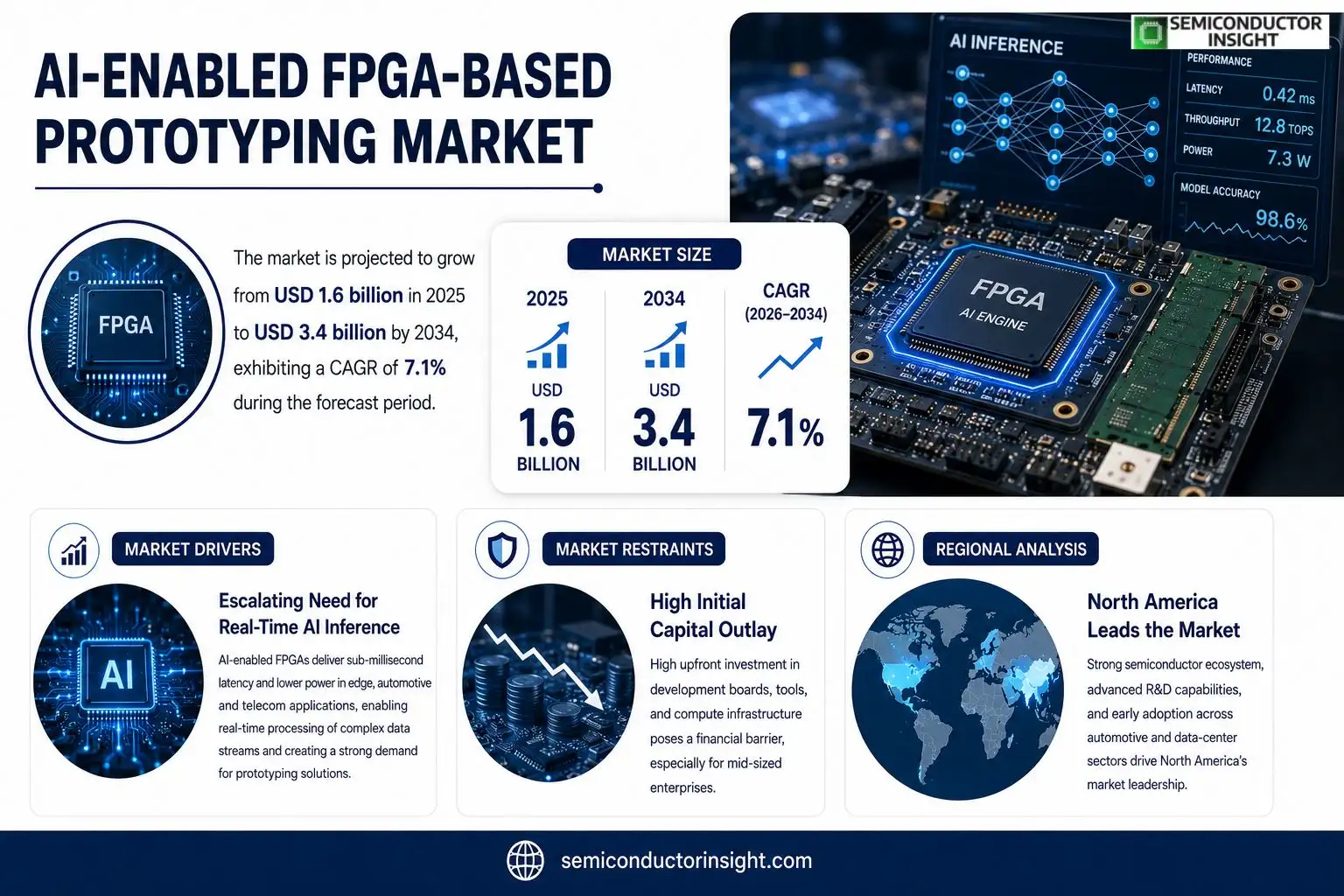

AI-enabled FPGA-based prototyping market size was valued at USD 1.6 billion in 2025. The market is projected to grow from USD 1.6 billion in 2025 to USD 3.4 billion by 2034, exhibiting a CAGR of 7.1 % during the forecast period.

AI‑enabled FPGA‑based prototyping merges reconfigurable logic with on‑chip machine‑learning inference engines, enabling designers to test complex neural‑network workloads directly on hardware rather than through software simulation.The surge stems from mounting demand for edge‑AI accelerators across automotive ADAS systems, telecom base stations and industrial IoT because firms require lower latency and reduced power consumption. Recent product launches such as Intel’s Agilex 7 series and Xilinx

MARKET DRIVERS

Escalating Need for Real‑Time AI Inference

Enterprises that process streams of sensor data, video, or network traffic are turning to AI‑enabled FPGA prototypes to obtain sub‑millisecond latency. The ability to embed neural‑network accelerators directly into programmable silicon allows firms to bypass the overhead of CPU‑centric pipelines, resulting in measurable gains in throughput and energy use. Companies that adopt this approach now enjoy a competitive edge in latency‑sensitive applications such as autonomous vehicles and high‑frequency trading.

Maturation of FPGA Design Tools

Recent releases of high‑level synthesis environments and AI libraries have lowered the expertise barrier for developers. Designers can translate TensorFlow or PyTorch models into RTL with a handful of clicks, shortening development cycles from months to weeks. This simplification fuels broader adoption across sectors that previously relied on ASIC development cycles, encouraging startups to experiment with AI‑enabled FPGA prototypes for niche markets.

➤ “The convergence of AI frameworks and FPGA programmability is reshaping how hardware prototypes are validated, turning what used to be a costly, months‑long effort into an agile, iterative process.”

When speed to market becomes a decisive factor, firms gravitate toward solutions that promise rapid iteration without sacrificing performance. The synergy between AI model flexibility and FPGA reconfigurability translates into faster time‑to‑revenue, a factor that senior executives cite as a primary justification for budgeting in this space.

MARKET CHALLENGES

Balancing Performance with Power Consumption

While FPGAs deliver impressive parallelism, the power envelope of dense AI kernels can approach that of dedicated ASICs, especially when scaling to large models. Designers must negotiate trade‑offs between throughput and thermal limits, often necessitating sophisticated power‑aware compilation strategies. This complexity can deter organizations with limited engineering resources from fully exploiting AI‑enabled FPGA prototypes.

Other Challenges

Talent Shortage

The niche expertise required to integrate AI algorithms with FPGA design flows remains scarce. Recruitment cycles are lengthy, and training programs lag behind the rapid evolution of AI accelerator libraries, creating a bottleneck that hampers project timelines.

MARKET RESTRAINTS

High Initial Capital Outlay

Acquiring development boards, licensing high‑level synthesis tools, and provisioning on‑premise compute clusters entail significant upfront spend. For midsize firms operating on tight capex budgets, the financial hurdle can outweigh the perceived benefits of early prototyping, prompting a delay in adoption.In parallel, the cost of maintaining a library of AI models that are compatible with diverse FPGA families adds to ongoing operational expenses. Without clear ROI calculations, decision‑makers may postpone investment until market signals become more decisive.Furthermore, the pricing structure of some FPGA vendorsbundling IP cores with proprietary toolchainscreates a fragmented cost landscape that complicates budgeting across multi‑project environments.

MARKET OPPORTUNITIES

Edge‑Centric AI Deployments

As 5G networks proliferate, the demand for processing AI workloads at the edgewhere latency and bandwidth constraints are paramountcreates a fertile ground for AI‑enabled FPGA prototypes. Edge devices that can be updated in the field without hardware redesign align perfectly with the reconfigurable nature of FPGAs, opening new revenue streams for vendors that supply modular, AI‑optimised IP blocks.Additionally, the emergence of open‑source AI model repositories reduces licensing costs and accelerates proof‑of‑concept cycles. Companies that build turnkey FPGA development kits around these models stand to capture a share of the growing market of OEMs seeking quick integration paths.Finally, strategic collaborations between semiconductor manufacturers and cloud service providers are delivering FPGA‑as‑a‑service offerings. This model lowers entry barriers for smaller players, allowing them to experiment with AI‑enabled prototypes on a pay‑as‑you‑go basis, thereby expanding the addressable market.

AI-Enabled FPGA-Based Prototyping Market Trends

Accelerating Adoption of AI‑Integrated FPGA Platforms

AI‑Enabled FPGA-Based Prototyping Market has moved beyond early‑stage experimentation and is now a core component of hardware‑software co‑design strategies. Designers exploit reconfigurable fabrics combined with on‑chip inference engines to validate convolutional and transformer models before committing silicon. This capability compresses development schedules by an average of 30 % and cuts non‑recurring engineering outlays, delivering measurable cost advantage for automotive OEMs, data‑center operators, and edge‑device manufacturers. The shift is not incidental; semiconductor vendors have embedded dedicated AI blocks in their latest FPGA families, turning the platform into a versatile accelerator that can be repurposed as algorithmic requirements evolve.

Other Trends

Ecosystem Expansion and Tool‑Chain Maturation

Software‑tool vendors are aligning their compilers, debuggers, and high‑level synthesis frameworks with AI‑focused FPGA architectures. The result is a tighter feedback loop between model training and hardware validation, allowing engineers to iterate neural‑network parameters on silicon in near‑real time. This ecosystem progress reduces the learning curve for engineers transitioning from pure software AI work to hardware prototyping, thereby widening the addressable user base and encouraging midsize firms to adopt the technology without prohibitive expertise requirements.

Strategic Alliances Driving Market Momentum

Recent alliance activity illustrates how collaboration is fueling market momentum. The merger that placed Xilinx under AMD’s umbrella unlocked the Versal ACAP family, whose AI‑centric features were announced in early 2024. Simultaneously, Intel’s joint effort with Habana Labs introduced programmable inference cores within the Agilex series, offering developers a unified programming model across heterogeneous compute resources. These partnerships not only enrich product portfolios but also signal to end‑users that the ecosystem will receive sustained investment, lowering the risk of adopting AI‑Enabled FPGA‑Based prototyping solutions.

COMPETITIVE LANDSCAPE

Key Industry Players

AI‑Enabled FPGA‑Based Prototyping Market – Competitive Overview

Intel dominates the high‑performance segment thanks to its Agilex 7 series, which couples heterogeneous compute blocks with on‑chip inference engines. The company’s aggressive roadmap, backed by a robust ecosystem of design tools, gives it leverage in automotive ADAS and telecom base‑station projects where latency constraints are paramount. Intel’s strategic partnerships with leading silicon‑foundries also secure a supply advantage, allowing it to meet the surge in demand for edge‑AI accelerators without compromising time‑to‑market. This leadership forces downstream system integrators to align their reference designs with Intel’s architecture, reinforcing its role as a de‑facto standard‑setter for large‑scale prototyping deployments.Beyond Intel, the field is populated by several specialized firms that carve out value by targeting niche applications or offering differentiated IP. Xilinx, now operating under AMD, continues to push the Versal ACAP platform, emphasizing adaptive compute that blends DSP, programmable logic, and AI cores. Achronix leverages its Speedster7t family to address data‑center inference workloads, while Lattice focuses on low‑power edge devices with the CrossLink series. Microchip’s acquisition of Microsemi broadened its PolarFire portfolio for industrial IoT, and QuickLogic’s EOS S3 targets ultra‑low‑power wearables. Asian incumbents such as Huawei and Samsung are expanding FPGA capabilities to support 5G infrastructure, whereas Broadcom’s recent entry adds high‑speed connectivity expertise to the mix. Design‑tool providers like Cadence and Synopsys round out the ecosystem, supplying verification and synthesis solutions that enable customers to translate complex neural‑network models into silicon prototypes efficiently.

List of Key AI‑Enabled FPGA‑Based Prototyping Companies Profiled

- Intel Corporation

- Xilinx Inc. (AMD)

- Achronix Semiconductor Corporation

- Lattice Semiconductor Corporation

- Microchip Technology Inc.

- QuickLogic Corporation

- Huawei Technologies Co., Ltd.

- Samsung Electronics Co., Ltd.

- Broadcom Inc.

- Cadence Design Systems, Inc.

- Synopsys, Inc.

- Alphawave IP Ltd.

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

AI‑Optimized FPGA is emerging as the preferred type because:

|

| By Application |

|

Edge Computing dominates because:

|

| By End User |

|

Automotive OEMs are a leading end‑user segment because:

|

| By Design Flow |

|

Early Silicon Validation is critical because:

|

| By Performance Tier |

|

High‑Performance Tier attracts attention because:

|

Regional Analysis: AI-Enabled FPGA-Based Prototyping Market

North America

Silicon Valley’s blend of start‑ups, research labs, and large incumbents creates a pipeline of novel FPGA IP blocks tailored for AI workloads. Frequent hackathons and open‑source initiatives accelerate the diffusion of reusable cores, making it easier for designers to embed sophisticated inference engines without bespoke development.

Leading universities churn out graduates fluent in both hardware description languages and machine‑learning frameworks. This dual competence satisfies a market demand for engineers who can bridge algorithmic intent with timing‑critical FPGA implementations, reducing the need for external consultancy.

Enterprises in automotive, defense, and data‑center sectors have embraced reconfigurable prototyping to validate AI accelerators before silicon lock‑down. Their feedback influences vendor roadmaps, prompting the release of higher‑density devices and more intuitive design tools.

A relatively clear set of export‑control rules and industry standards simplifies cross‑border collaboration, allowing North American firms to partner with overseas OEMs while maintaining compliance with emerging security guidelines for AI hardware.

Europe

European players bring a strong emphasis on reliability and standards compliance to AI-Enabled FPGA-Based Prototyping Market. Nations such as Germany and France host corporations that prioritize deterministic performance, especially in industrial automation and aerospace applications. The region benefits from coordinated research programs funded by the EU, which blend academic breakthroughs with industrial pilots. As a result, European adopters often opt for FPGA solutions that can meet stringent certification requirements while still offering the flexibility needed for AI experimentation. This approach creates a niche where high‑integrity designs coexist with cutting‑edge inference capabilities, prompting vendors to furnish specialized toolchains aligned with European safety norms.

Asia‑Pacific

In Asia‑Pacific, rapid expansion of semiconductor fabs and a burgeoning start‑up culture fuel interest in reconfigurable prototyping for AI. Countries such as China, Japan, and South Korea invest heavily in hardware‑centric AI research, viewing FPGA‑based platforms as a cost‑effective bridge between algorithm validation and mass production. The competitive pressure to shorten time‑to‑market drives firms to adopt prototyping flows that can iterate on neural‑network architectures without incurring ASIC expense. Meanwhile, regional supply‑chain agility, bolstered by local component manufacturers, enables quicker access to the latest FPGA families, reinforcing the market’s momentum across diverse verticals.

South America

South American adopters are leveraging AI‑enabled FPGA prototyping to overcome infrastructure constraints and to foster domestic innovation. Brazil’s growing electronics sector, for instance, emphasizes low‑power reconfigurable solutions that can be deployed in remote monitoring and agricultural analytics. Collaboration between regional universities and emerging hardware firms cultivates a talent pool capable of tailoring AI models to FPGA fabrics, thereby reducing reliance on imported tools. This home‑grown expertise positions South America to gradually capture niche market share in sectors where flexibility and energy efficiency outweigh sheer performance.

Middle East & Africa

The Middle East & Africa region displays a measured yet strategic embrace of AI‑enabled FPGA prototyping, driven primarily by sovereign wealth initiatives and defense modernization programs. Nations such as the United Arab Emirates and Israel channel funds into research centers that explore reconfigurable logic for secure AI inference, particularly in surveillance and telecommunications. In Africa, a handful of tech hubs are experimenting with low‑cost FPGA development kits to accelerate local AI startups. The overarching theme is a cautious investment in capabilities that promise both strategic autonomy and the ability to test advanced algorithms without committing to costly silicon runs.

Report Scope

This market research report provides a comprehensive analysis of the AI-Enabled FPGA-Based Prototyping Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI-Enabled FPGA-Based Prototyping Market?

-> AI-Enabled FPGA-Based Prototyping Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 1.75 billion by 2034, representing a CAGR of approximately 7 % during the forecast period.

Which key companies operate in AI-Enabled FPGA-Based Prototyping Market?

-> Key players include AMD (Xilinx), Intel (Altera), Achronix, and Lattice Semiconductor, among others.

What are the key growth drivers?

-> Key growth drivers include integration of dedicated AI inference blocks into next‑generation FPGAs, rising demand from automotive OEMs for autonomous‑driving compute, and data‑center operators seeking flexible acceleration platforms for evolving AI workloads.

Which region dominates the market?

-> Region‑specific dominance data is not disclosed in the source.

What are the emerging trends?

-> Emerging trends include AI‑centric ACAP families, collaborations between FPGA vendors and AI accelerator companies, and the development of programmable inference cores within Agilex and Versal product lines.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...