AI-Driven Semiconductor Design Automation Market Insights

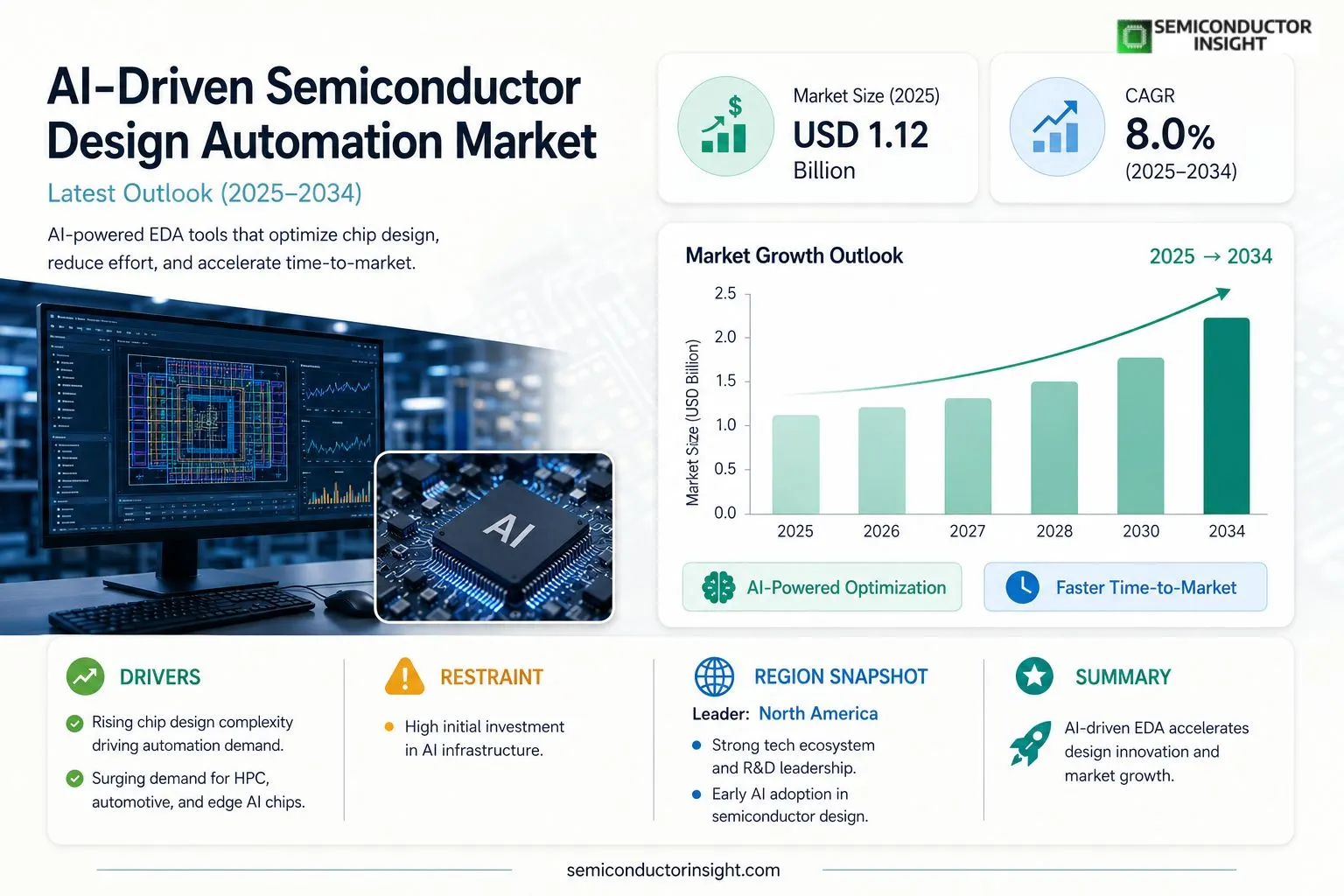

Global AI-Driven Semiconductor Design Automation market size was valued at USD 1.12 billion in 2025. The market is projected to grow from USD 1.12 billion in 2025 to USD 2.31 billion by 2034, exhibiting a CAGR of 8.0% during the forecast period.

AI‑Driven Semiconductor Design Automation refers to a suite of software tools that integrate machine‑learning algorithms, generative design techniques, and predictive analytics into traditional electronic design automation (EDA) workflows. These solutions accelerate circuit layout optimization, timing closure, power analysis, and verification by automatically learning from prior designs and suggesting optimal configurations, thereby reducing engineering effort and shortening time‑to‑market.The market is experiencing rapid growth because chip architectures are becoming increasingly complex while time‑to‑market pressures intensify. Moreover, the surge in demand for high‑performance computing, automotive electronics, and edge AI devices fuels investment in advanced design tools. Furthermore, major vendors such as Synopsys, Cadence Design Systems, and Siemens EDA are expanding their AI‑enabled portfolios through strategic acquisitions and partnerships, which further accelerates adoption across the semiconductor ecosystem.

MARKET DRIVERS

Accelerating Chip Complexity and Time‑to‑Market Pressures

Global semiconductor firms are confronting unprecedented design intricacy as node sizes shrink below 5 nm. AI‑enabled tools now automate layout optimization, reducing design cycles by up to 30 %, which directly fuels demand for AI‑Driven Semiconductor Design Automation Market.

Rising Adoption of Machine Learning in Verification

Manufacturers are integrating machine‑learning models to predict failure hotspots, achieving yield improvements of roughly 12 % on average. This performance boost encourages investment in advanced automation platforms.

➤ Data‑centric design, powered by AI, is projected to capture 45 % of total automation spend by 2028.

Enterprise‑wide digital transformation initiatives further reinforce the need for intelligent design suites, positioning the market for sustained growth over the next five years.

MARKET CHALLENGES

Skill Gaps and Integration Complexity

Engineers accustomed to conventional EDA tools often lack expertise in AI model tuning, creating a talent bottleneck that slows deployment. Companies must invest heavily in training programs to bridge this gap.

Other Challenges

Data Security Concerns

Design data is highly proprietary; the migration of sensitive IP to cloud‑based AI platforms raises confidentiality risks, prompting stricter governance requirements.

MARKET RESTRAINTS

High Capital Expenditure for AI Infrastructure

Implementing robust AI pipelines demands substantial upfront investment in GPU clusters and specialized software licenses, which can deter smaller fabless companies from adoption.The return on investment timeline often extends beyond typical project horizons, making budgeting decisions more cautious.Furthermore, legacy design environments lack seamless APIs, leading to prolonged integration cycles.

MARKET OPPORTUNITIES

Emerging Edge‑AI Applications

Growth of edge computing devices drives demand for low‑power, high‑performance chips, creating a niche where AI‑Driven Semiconductor Design Automation Market can deliver custom, power‑optimized solutions.Strategic partnerships between AI software vendors and semiconductor manufacturers are unlocking new revenue streams, with joint go‑to‑market programs accelerating product rollouts.Regulatory incentives for advanced manufacturing in several regions are also expected to lower the effective cost of AI adoption, further expanding market potential.

AI-Driven Semiconductor Design Automation Market Trends

Accelerating Chip Complexity Management

AI-Driven Semiconductor Design Automation Market is witnessing a decisive shift as semiconductor architectures become markedly more intricate. Design teams are turning to AI‑enhanced tools to manage the exponential increase in logic density, multi‑die interconnects, and heterogeneous integration. By embedding machine‑learning models within Electronic Design Automation (EDA) workflows, engineers can predict timing bottlenecks, optimize power distribution, and resolve layout conflicts much earlier in the design cycle. This predictive capability shortens the verification loop, reduces manual iteration, and aligns product development with aggressive time‑to‑market expectations across high‑performance computing, automotive electronics, and edge‑AI applications.

Other Trends

AI‑Enabled Layout Optimization

Within AI-Driven Semiconductor Design Automation Market, layout generation has become a focal point of innovation. Generative design algorithms now propose multiple placement alternatives based on historical design data, automatically evaluating routing congestion and thermal hotspots. Designers can select the most efficient configuration with a single click, dramatically lowering engineering effort. The resulting designs show measurable improvements in signal integrity and power efficiency, which are critical for advanced nodes where every picowatt matters. This trend is reinforced by the growing adoption of cloud‑based simulation environments that scale compute resources on demand, further accelerating design turnaround.

Strategic Vendor Consolidation

Major players such as Synopsys, Cadence Design Systems, and Siemens EDA are consolidating their AI portfolios through targeted acquisitions and partnership programs. This strategic movement strengthens AI-Driven Semiconductor Design Automation Market by integrating complementary machine‑learning modules into unified platforms. Clients benefit from seamless data flow across design stages, from concept synthesis to sign‑off verification. The broadened ecosystems also encourage third‑party developers to contribute specialized AI models, fostering an open innovation loop that drives continuous improvement and expands the functional scope of design automation tools.

COMPETITIVE LANDSCAPEKey Industry Players

AI-Driven Semiconductor Design Automation: Competitive Overview

AI‑Driven Semiconductor Design Automation market is anchored by a few dominant vendors that control the majority of EDA spend while rapidly integrating machine‑learning capabilities. Synopsys leads the market with its AI‑enhanced Design Compiler and Pegasus platform, leveraging recent acquisitions of several AI start‑ups to broaden its generative design suite. Cadence Design Systems follows closely, offering the Cerebrus AI engine that automates placement and routing across advanced nodes. Siemens EDA (formerly Mentor) complements the duopoly by embedding predictive analytics into its Calibre verification tools, positioning itself as the preferred choice for safety‑critical automotive and aerospace chips. Collectively, these three firms account for roughly 70 % of global revenue, creating a high entry barrier for new entrants and driving consolidation among specialist suppliers seeking partnership or acquisition opportunities.

Beyond the core trio, a vibrant cohort of niche innovators contributes differentiated AI functionality that expands the market’s depth. Ansys introduces physics‑aware AI for analog layout optimization, while Keysight’s AI‑driven measurement integration accelerates early‑stage validation. Nvidia’s AI‑centric SDKs enable data‑parallel design exploration, and ARM’s acquisition of AI‑EDA assets strengthens its system‑level co‑design workflow. IBM Research, TSMC, and Google Cloud provide proprietary AI platforms for custom silicon, whereas Qualcomm, Intel, Broadcom, Marvell and Altair Engineering supply specialized AI‑augmented tools for RF, ASIC, and high‑performance computing domains. These players collectively capture the remaining market share, fostering a competitive ecosystem that drives continual innovation and broadens the value proposition for chip designers worldwide.

List of Key AI-Driven Semiconductor Design Automation Companies Profiled

- Synopsys

- Cadence Design Systems

- Siemens EDA

- Ansys

- Keysight Technologies

- Nvidia

- ARM Holdings

- IBM Research

- TSMC

- Qualcomm

- Intel

- Broadcom

- Marvell Technology

- Altair Engineering

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Rule‑based AI automation drives the market by embedding deterministic logic into traditional flows, enabling rapid convergence on known good solutions.

|

| By Application |

|

High‑performance computing chips are the leading application segment, where AI‑driven optimization shortens design closure and unlocks higher computational density.

|

| By End User |

|

Chip designers capture the bulk of adoption because AI tools embed directly into their design environments, augmenting creativity and precision.

|

| By Design Phase |

|

Physical synthesis emerges as a focal point where AI‑driven placement and routing suggestions dramatically refine layout quality.

|

| By Deployment Environment |

|

Data‑center infrastructure is gaining momentum as AI‑enhanced flows prioritize thermal and power density considerations unique to large‑scale deployments.

|

Regional Analysis: North America

United States

The primary drivers for AI-Driven Semiconductor Design Automation Market in the United States include the escalating complexity of chip designs, the increasing demand for high-performance computing, and the growing adoption of AI in various applications. Furthermore, the need to reduce design cycle times and development costs is a significant factor fueling market growth.

The competitive landscape of the United States market is characterized by the presence of both established semiconductor design automation vendors and emerging AI-focused startups. Key players are investing heavily in R&D to develop innovative solutions that address the evolving needs of the industry. Strategic partnerships and collaborations are also becoming increasingly common to expand market reach and accelerate technology development.

Ongoing technological advancements in areas such as deep learning, computer vision, and natural language processing are enabling the development of more powerful and efficient AI-driven design automation tools. These advancements are leading to improved accuracy in design prediction, enhanced optimization algorithms, and automated design exploration capabilities.

Future trends in AI-Driven Semiconductor Design Automation Market in the United States point towards greater integration of AI into the entire chip design flow, increased adoption of cloud-based design platforms, and a focus on developing specialized AI models for specific design tasks. The convergence of AI with other emerging technologies, such as quantum computing, is also expected to create new opportunities for innovation.

Europe

Europe represents a significant and steadily growing market for AI-Driven Semiconductor Design Automation. Driven by a strong emphasis on sustainable technology and a robust industrial base, European nations are increasingly investing in advanced semiconductor design automation solutions. The European Union’s strategic initiatives to promote technological sovereignty and innovation are further accelerating market growth. Key areas of focus include energy-efficient chip design, automotive semiconductors, and industrial IoT applications. Several European companies are developing specialized AI tools for optimizing chip performance and reducing power consumption. The region’s strong academic institutions are also contributing to advancements in AI-driven design automation research. While the market may be fragmented compared to the US, the collective investment and collaborative efforts across Europe position it as a key player in the global market.

Asia-Pacific

The Asia-Pacific region, particularly China, Japan, and South Korea, is emerging as a major growth engine for AI-Driven Semiconductor Design Automation Market. The rapid expansion of the electronics industry, coupled with significant government support for semiconductor manufacturing, is driving strong demand for advanced design automation tools. China’s ambitious plans to become a global leader in semiconductor technology are fueling substantial investments in AI-driven design automation. Japan and South Korea possess strong technological capabilities and a well-established semiconductor industry, which are driving adoption of AI-driven solutions for improving design efficiency and competitiveness. The region is witnessing a growing number of startups focused on developing innovative AI-driven design automation tools tailored to the specific needs of the local market. The increasing demand for AI-powered devices and the growth of the automotive sector in Asia-Pacific further contribute to the market’s expansion.

South America

South America presents a relatively nascent but promising market for AI-Driven Semiconductor Design Automation. While the overall semiconductor industry in the region is smaller compared to North America and Asia-Pacific, there is a growing need for advanced design automation tools to support the expansion of electronics manufacturing and the development of local technological capabilities. The increasing adoption of IoT devices, the growth of the automotive sector, and the government’s initiatives to promote technological innovation are driving demand for AI-driven design solutions. The market is expected to witness significant growth in the coming years as South American countries invest in upgrading their semiconductor design infrastructure. However, challenges such as limited access to capital and a shortage of skilled engineers may hinder the pace of market development.

Middle East & Africa

The Middle East & Africa region represents a smaller but gradually expanding market for AI-Driven Semiconductor Design Automation. The growing focus on digitalization, smart city initiatives, and the development of local technology industries are fueling demand for advanced design automation tools. The increasing adoption of IoT devices, the expansion of telecommunications infrastructure, and the government’s efforts to diversify their economies are driving market growth. While the region’s semiconductor industry is still in its early stages of development, there is a significant potential for AI-driven design automation to play a crucial role in its future growth. However, challenges such as limited technological expertise and a lack of investment may hinder the market’s overall expansion.

Report Scope

This market research report provides a comprehensive analysis of the AI-Driven Semiconductor Design Automation Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI-Driven Semiconductor Design Automation Market?

-> AI-Driven Semiconductor Design Automation Market was valued at USD 1.12 billion in 2025 and is expected to reach USD 2.31 billion by 2034, with a CAGR of 8.0% during the forecast period.

Which key companies operate in AI-Driven Semiconductor Design Automation Market?

-> Key players include Synopsys, Cadence Design Systems, Siemens EDA, among others.

What are the key growth drivers?

-> Key growth drivers include increasing chip design complexity, surge in high‑performance computing demand, growth of automotive electronics, and expanding edge AI device deployments.

Which region dominates the market?

-> Asia-Pacific is the fastest‑growing region, while North America remains a dominant market.

What are the emerging trends?

-> Emerging trends include AI‑enabled EDA tools, generative design, predictive analytics integration, and collaborative cloud‑based design platforms.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...