MARKET INSIGHTS

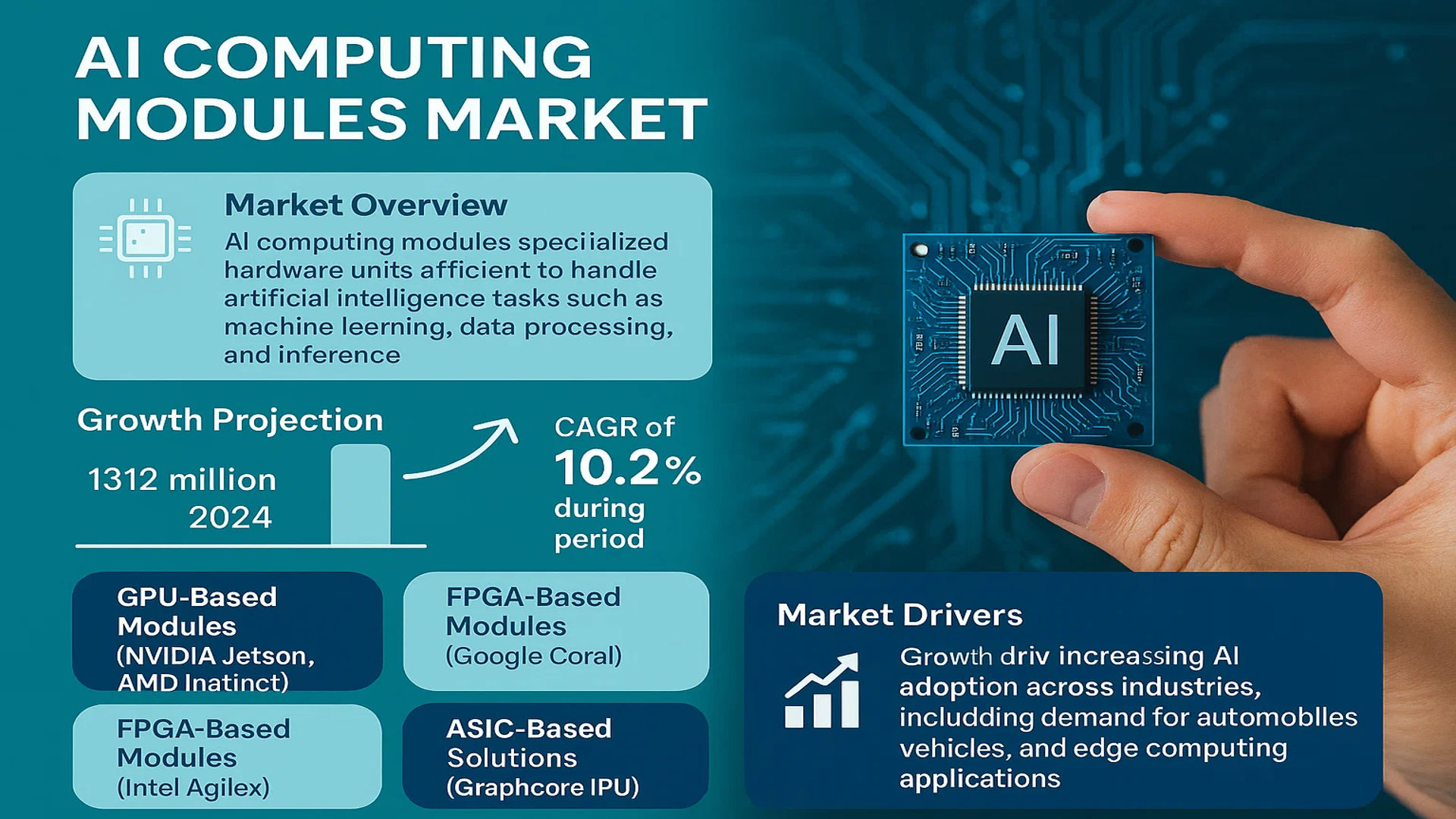

The global AI Computing Modules Market was valued at 1312 million in 2024 and is projected to reach US$ 2527 million by 2032, at a CAGR of 10.2% during the forecast period.

AI computing modules are specialized hardware units designed to efficiently handle artificial intelligence tasks such as machine learning, data processing, and inference. These modules integrate high-performance processors (CPUs, GPUs, or AI accelerators), memory, and storage into compact form factors, enabling efficient deployment of AI algorithms in edge devices, data centers, and embedded systems. Key variants include GPU-based modules (NVIDIA Jetson, AMD Instinct), TPU-based modules (Google Coral), FPGA-based modules (Intel Agilex), and ASIC-based solutions (Graphcore IPU).

The market growth is driven by increasing AI adoption across industries, with particular demand from autonomous vehicles (projected 30% of automotive AI hardware spending by 2025) and edge computing applications. Recent advancements in neural processing units (NPUs) and energy-efficient architectures are enabling deployment in IoT devices. NVIDIA leads the market with 60% share in AI accelerator modules, while emerging players like Kneron and Mythic AI are gaining traction with low-power edge AI solutions. The Asia-Pacific region dominates demand growth, accounting for 42% of 2024 module shipments.

MARKET DYNAMICS

MARKET DRIVERS

Rising Demand for AI-Powered Edge Computing to Drive Market Expansion

The increasing adoption of edge computing, which processes data closer to its source rather than in centralized cloud systems, is revolutionizing AI deployment across industries. AI computing modules are becoming indispensable components in edge devices due to their ability to deliver low-latency processing, enhanced security, and reduced bandwidth costs. Applications in autonomous vehicles, industrial IoT, and smart cities are fueling demand—autonomous vehicles alone are projected to generate petabytes of data daily, requiring real-time AI processing at the edge. Additionally, advancements in 5G networks are creating new possibilities for distributed AI architectures, further propelling module adoption.

Growth of Computer Vision Applications Accelerating Market Adoption

Computer vision has emerged as one of the fastest-growing AI applications, with implementations spanning security surveillance, medical imaging, retail analytics and quality inspection. The technology requires specialized processing capabilities that conventional CPUs cannot efficiently provide. AI modules with optimized GPU/TPU architectures are experiencing surging demand as they can process complex visual data at high speeds while maintaining power efficiency—critical for mobile and embedded systems. Retail sector adoption has been particularly strong, with smart cameras and shelf-monitoring systems utilizing AI modules to analyze customer behavior and inventory changes in real-time.

Healthcare Digital Transformation Creating Robust Demand for AI Modules

The healthcare industry’s rapid digital transformation is driving significant investments in AI-powered diagnostic equipment and patient monitoring systems. Medical AI applications require specialized computing modules that can handle sensitive patient data securely while delivering the processing power needed for complex algorithms. Growth in telemedicine, combined with regulatory approvals for AI-based diagnostic tools, is creating sustained demand. Portable medical devices equipped with AI modules capable of processing medical imaging are seeing particularly strong adoption, as they enable point-of-care diagnostics without compromising accuracy.

MARKET RESTRAINTS

Technical Challenges in AI Module Miniaturization Constraining Adoption

While demand for compact AI solutions grows, shrinking module footprints while maintaining performance presents substantial engineering challenges. Thermal dissipation becomes increasingly difficult as components are packed more densely, potentially leading to throttling performance or reduced lifespan. Power efficiency remains another critical constraint—many edge applications require modules to operate within strict thermal design power (TDP) limits while delivering substantial computational throughput. These miniaturization challenges are particularly acute in consumer electronics and wearable applications where space and power budgets are extremely limited.

Other Restraints

Cost Sensitivity in Industrial Applications

Unlike cloud-based solutions where costs can be distributed across users, embedded AI modules represent fixed hardware investments that can deter price-sensitive manufacturers. While costs have been decreasing, the premium for AI-optimized modules compared to standard computing solutions remains a consideration factor, especially in high-volume manufacturing scenarios where unit cost differences scale significantly.

Interoperability and Standardization Gaps

The lack of universal standards for AI module interfaces creates integration challenges that slow adoption. Equipment manufacturers often need to develop custom firmware and software adaptations for different module vendors, increasing development costs and time-to-market. This fragmentation is particularly evident in industrial automation applications where long equipment lifecycles require stable hardware ecosystems.

MARKET CHALLENGES

Supply Chain Vulnerabilities Impacting Module Production and Availability

The AI computing module market faces persistent supply chain challenges stemming from concentrated semiconductor manufacturing and complex component sourcing. Advanced modules typically incorporate specialized processors, high-bandwidth memory, and other components sourced from limited suppliers, creating single points of failure. Geopolitical factors can disrupt these fragile supply networks, as seen in recent trade restrictions affecting advanced chip production. Long lead times for custom silicon components exacerbate these challenges, forcing some manufacturers to redesign products mid-cycle based on component availability rather than optimal technical specifications.

Other Challenges

Proliferation of Competing Architectures

The lack of a dominant architecture standard requires module manufacturers to support multiple processor types (GPUs, TPUs, FPGAs, ASICs), increasing development costs and complicating product roadmaps. New entrants continue introducing novel architectures claimed to offer better performance or efficiency, forcing vendors to continuously evaluate and potentially adopt emerging technologies at considerable expense.

Security Concerns in Edge Deployments

Unlike cloud deployments where security can be centrally managed, AI modules deployed at the edge represent numerous potential attack surfaces. Ensuring secure firmware, encrypted communications, and protection against physical tampering requires significant engineering investment whereas breaches could erode confidence in embedded AI solutions generally.

MARKET OPPORTUNITIES

Emerging Generative AI Applications Creating New Module Demand

The explosive growth of generative AI is driving innovation in specialized hardware capable of efficiently running large language models and diffusion models outside traditional data centers. While current focus remains on cloud deployment, there is growing interest in edge implementations that could benefit from dedicated AI modules. Applications like real-time media generation, personalized content creation, and on-device AI assistants present significant opportunities for module vendors. Early implementations in smartphones and automotive infotainment systems demonstrate the viability of this approach and point to potential expansion into other consumer and enterprise applications.

Growth of AI-Enabled Robotics Opening New Markets

The robotics sector is undergoing fundamental transformation as AI capabilities move from research labs to practical applications. Next-generation service, logistics and industrial robots require compact, power-efficient AI modules that can perform complex perception and decision-making tasks in real-time. The combination of advanced computer vision, sensor fusion and motion planning algorithms creates substantial demand for specialized computing hardware. Collaborative robots (cobots) designed to work alongside humans represent a particularly promising segment as they require sophisticated AI for safety and adaptability in unstructured environments.

Government Initiatives Accelerating AI Hardware Adoption

National strategies promoting AI development and adoption are driving significant public and private sector investment in AI infrastructure. Multiple governments have identified AI hardware as strategic technology area, leading to funding programs and procurement policies that favor domestic AI module solutions. These initiatives often focus on critical applications like defense, smart city infrastructure, and healthcare modernization where specialized AI hardware offers clear advantages. The strategic importance of sovereign AI capabilities is also prompting investments in alternative supply chains and manufacturing ecosystems that could reshape the supplier landscape.

AI COMPUTING MODULES MARKET TRENDS

Edge AI and Hybrid Cloud Deployments Drive Market Growth

The AI computing modules market is experiencing a significant boost due to the rapid adoption of edge AI solutions. Unlike traditional cloud-based AI, edge computing processes data locally on devices, significantly reducing latency and bandwidth requirements. This trend is particularly strong in applications like autonomous vehicles and industrial IoT, where real-time decision-making is critical. More than 65% of enterprises are now implementing some form of edge computing for their AI workloads, with AI modules enabling compact, efficient processing in constrained environments. Hybrid cloud deployments, combining edge and cloud AI, are also gaining traction—with modular AI solutions allowing seamless transitions between on-device and cloud-based processing as needed.

Other Trends

Accelerated Adoption in Healthcare Diagnostics

The healthcare sector is increasingly leveraging AI computing modules to power advanced diagnostic tools such as medical imaging analysis and predictive diagnostics. Portable medical devices equipped with AI modules can now analyze X-rays with over 95% accuracy at the point of care, dramatically reducing diagnosis times. This trend is supported by regulatory approvals for AI-assisted medical devices—more than 50 AI-based medical algorithms received FDA clearance in 2024 alone. AI computing modules are also enabling next-generation wearable health monitors capable of detecting early signs of chronic conditions with minimal power consumption.

Energy-Efficient AI Architectures Reshape Market

Power efficiency has become a critical differentiator in the AI computing modules market, particularly for battery-powered devices. Companies are developing specialized low-power AI accelerators that consume up to 80% less energy than traditional GPU solutions while maintaining competitive performance—an essential requirement for smart city deployments and mobile applications. These efficiency gains are achieved through architectural innovations like neuromorphic computing and sparsity-aware processing. Cloud service providers are also driving demand for efficient modules in data centers—with projections indicating AI workloads could consume up to 15% of global data center power by 2032 without optimization technologies.

COMPETITIVE LANDSCAPE

Key Industry Players

Technological Innovation and Strategic Alliances Drive Market Competition

The global AI Computing Modules market exhibits a dynamic competitive environment, characterized by both established technology giants and emerging innovators. With the market projected to grow at a CAGR of 10.2% from 2024 to 2032, reaching $2.5 billion, companies are aggressively expanding their capabilities to capture larger shares. The landscape is moderately consolidated, with the top five players accounting for a significant portion of the revenue, while smaller firms continue to carve out niches through specialized solutions.

NVIDIA dominates the market, leveraging its advanced GPU-based AI modules and comprehensive software ecosystems. The company’s recent breakthroughs in AI accelerators, coupled with strong penetration in data centers and automotive sectors, solidify its leadership. Meanwhile, Intel and AMD maintain robust positions through their diversified portfolios, which integrate CPUs, FPGAs, and customized AI chips for edge computing applications.

Meanwhile, Qualcomm and Google are gaining traction with their energy-efficient AI modules tailored for mobile and IoT devices. Google’s TPU-based solutions are particularly influential in cloud and enterprise AI deployments. These players are actively forming strategic partnerships with OEMs and cloud service providers to enhance market penetration.

Emerging contenders like Cerebras Systems and Graphcore are disrupting the market with novel architectures designed for high-performance AI workloads. Their focus on scalable, low-latency modules for data centers and industrial automation is reshaping competitive dynamics, compelling incumbents to accelerate R&D investments.

List of Key AI Computing Modules Companies Profiled

- NVIDIA Corporation (U.S.)

- Intel Corporation (U.S.)

- Qualcomm Technologies, Inc. (U.S.)

- Advanced Micro Devices, Inc. (AMD) (U.S.)

- Google LLC (U.S.)

- Apple Inc. (U.S.)

- Micron Technology, Inc. (U.S.)

- Cerebras Systems (U.S.)

- Mythic AI (U.S.)

- Kneron (U.S.)

- Graphcore (U.K.)

- Arm Holdings (U.K.)

- NXP Semiconductors (Netherlands)

- Baikal Electronics (Russia)

- Samsung Electronics (South Korea)

- MediaTek Inc. (Taiwan)

- Huawei Technologies (China)

Segment Analysis:

By Type

GPU-based AI Modules Lead Due to High-Performance Computing Capabilities

The market is segmented based on type into:

- GPU-based AI Modules

- Subtypes: NVIDIA CUDA, AMD ROCm, and others

- TPU-based AI Modules

- FPGA-based AI Modules

- Subtypes: Xilinx FPGAs, Intel FPGAs, and others

- ASIC-based AI Modules

By Application

Data Centers Dominate as AI Workload Processing Accelerates

The market is segmented based on application into:

- Data Centers

- Autonomous Vehicles

- Medical Devices

- Telecommunications

- Industrial Automation

- Others

By Processing Power

High-Performance Modules in Demand for Complex AI Workloads

The market is segmented based on processing power into:

- Low-Power Modules (Below 20W)

- Mid-Range Modules (20-100W)

- High-Performance Modules (Above 100W)

By End-Use Industry

Technology Sector Accounts for Largest Adoption

The market is segmented based on end-use industry into:

- Technology & Software

- Healthcare

- Automotive

- Manufacturing

- Others

Regional Analysis: AI Computing Modules Market

North America

North America leads the global AI computing modules market, driven by the U.S. due to its robust semiconductor industry and heavy investments in AI research. The region houses key players like NVIDIA, Intel, and Qualcomm, which dominate GPU-based and TPU-based AI module production. Rapid adoption of AI in autonomous vehicles (supported by regulatory approvals for testing in states like California) and smart healthcare systems fuels demand. Additionally, data center expansions by tech giants like Google and Amazon, along with increasing AI deployment in defense applications, position North America as the innovation hub for high-performance AI modules. However, tight export controls on advanced AI hardware pose challenges for international supply chains.

Asia-Pacific

The Asia-Pacific region, led by China, Japan, and South Korea, is the fastest-growing market for AI computing modules. China’s aggressive AI development strategy—supported by government initiatives like the New Generation AI Development Plan—propels local giants such as Huawei and Baidu to invest in domestic ASIC-based modules. Japan focuses on robotics and industrial automation, while South Korea’s Samsung and LG integrate AI modules into consumer electronics. Despite cost sensitivity favoring mid-range FPGA-based solutions, the region’s manufacturing scale and edge-computing adoption in smart factories ensure steady growth, though U.S.-China tech tensions create supply chain uncertainties.

Europe

Europe prioritizes ethical AI and energy-efficient computing, with the EU’s Artificial Intelligence Act shaping module design standards. Countries like Germany and France leverage AI modules for Industry 4.0, while the U.K. excels in financial services AI applications. Collaboration between academic institutions and firms such as Graphcore (U.K.) and NXP Semiconductors (Netherlands) drives innovation in low-power, explainable AI hardware. However, reliance on non-European suppliers for advanced GPUs and slower 5G rollout compared to Asia limit scalability in some sectors.

Middle East & Africa

This emerging market shows potential through smart city projects (e.g., UAE’s Dubai 2030 initiative) and oil/gas sector automation. While Israel’s startup ecosystem develops niche AI modules for cybersecurity, Gulf nations import high-end solutions for infrastructure projects. Limited local manufacturing and fragmented R&D investments hinder self-sufficiency, but partnerships with global vendors like NVIDIA indicate long-term growth as digital transformation accelerates.

South America

Brazil and Argentina are focal points for AI module adoption in agriculture and telemedicine, though economic instability delays large-scale investments. Local startups collaborate with Intel and MediaTek to tailor cost-effective modules for regional needs. Lack of domestic semiconductor fabrication and reliance on imports remain critical bottlenecks, but governmental support for AI in public services offers incremental opportunities.

Report Scope

This market research report provides a comprehensive analysis of the Global AI Computing Modules Market, covering the forecast period 2024–2032. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments. The Global AI Computing Modules Market was valued at USD 1,312 million in 2024 and is projected to reach USD 2,527 million by 2032, growing at a CAGR of 10.2%.

- Segmentation Analysis: Detailed breakdown by product type (GPU-based, TPU-based, FPGA-based, ASIC-based), technology, application (Data Centers, Autonomous Vehicles, Medical Devices, Telecommunications, Financial Services, Retail & E-commerce, Industrial Automation, Smart Cities, Others), and end-user industry to identify high-growth segments and investment opportunities.

- Regional Outlook: Insights into market performance across North America (U.S., Canada, Mexico), Europe (Germany, France, U.K., Italy, Russia), Asia-Pacific (China, Japan, South Korea, India), Latin America (Brazil, Argentina), and Middle East & Africa (Saudi Arabia, UAE, Turkey).

- Competitive Landscape: Profiles of leading market participants including NVIDIA, Intel, Qualcomm, AMD, Google, Apple, Micron Technology, Cerebras Systems, Mythic AI, and Kneron, covering their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments.

- Technology Trends & Innovation: Assessment of emerging technologies in AI computing modules, including advancements in chip architecture, integration of AI accelerators (TPUs, FPGAs), edge computing solutions, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth (increasing AI adoption across industries, demand for edge computing, autonomous systems development) along with challenges (high development costs, supply chain constraints, regulatory issues).

- Stakeholder Analysis: Insights for semiconductor manufacturers, OEMs, system integrators, investors, and policymakers regarding the evolving AI hardware ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Global AI Computing Modules Market?

-> AI Computing Modules Market was valued at 1312 million in 2024 and is projected to reach US$ 2527 million by 2032, at a CAGR of 10.2% during the forecast period.

Which key companies operate in Global AI Computing Modules Market?

-> Key players include NVIDIA, Intel, Qualcomm, AMD, Google, Apple, Micron Technology, Cerebras Systems, Mythic AI, and Kneron, among others.

What are the key growth drivers?

-> Key growth drivers include rising adoption of AI across industries, increasing demand for edge computing solutions, development of autonomous systems, and advancements in semiconductor technology.

Which region dominates the market?

-> North America currently leads in market share, while Asia-Pacific is expected to witness the fastest growth due to increasing investments in AI infrastructure.

What are the emerging trends?

-> Emerging trends include development of specialized AI chips, integration of neuromorphic computing, edge AI deployment, and energy-efficient AI hardware solutions.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...