AI Chip Organic Substrate Market Insights

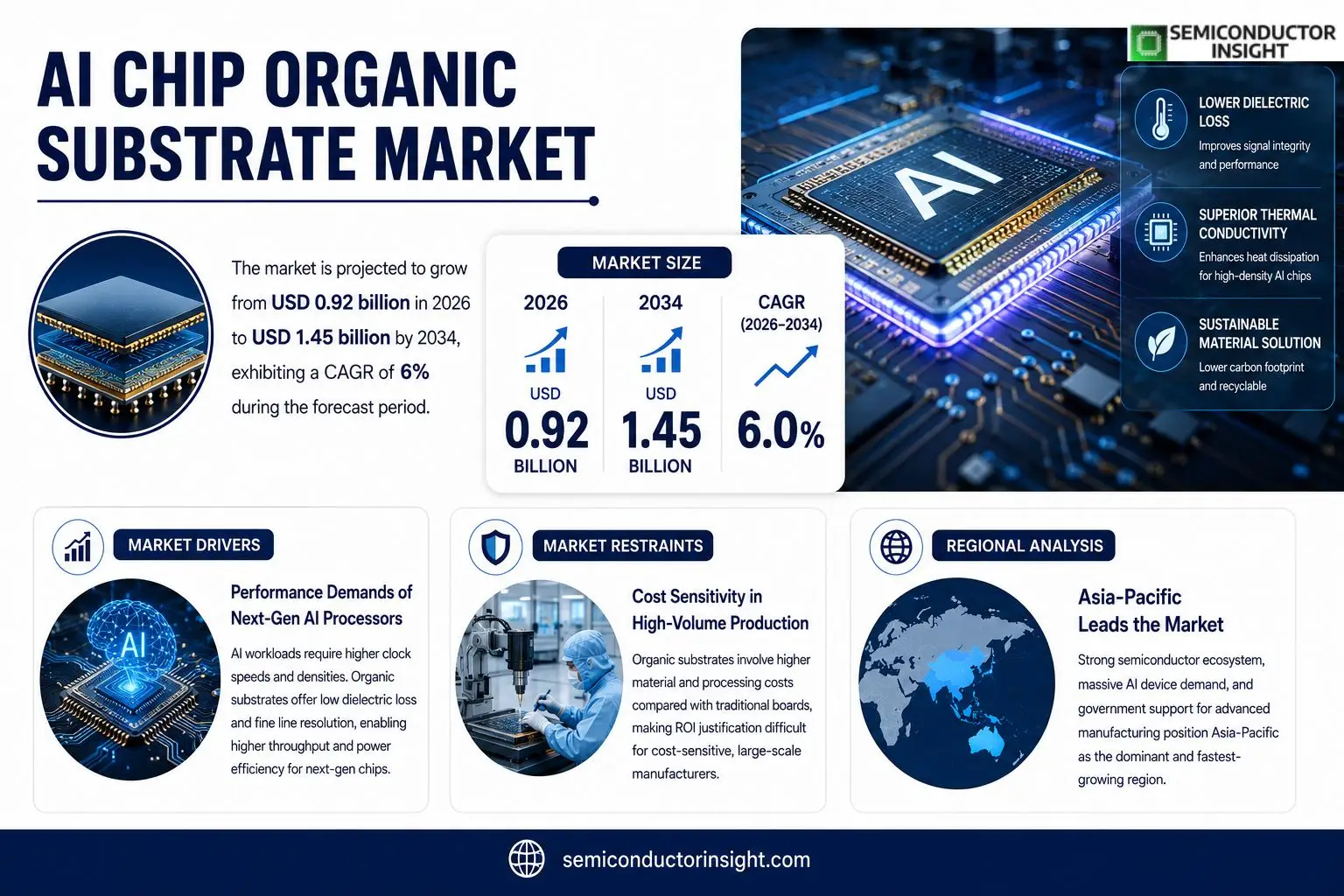

AI Chip Organic Substrate market size was valued at USD 0.85 billion in 2025. The market is expected to rise from USD 0.92 billion in 2026 to USD 1.45 billion by 2034, reflecting a compound annual growth rate of approximately 6 % over the forecast horizon.

AI Chip Organic Substrate denotes chemically engineered polymer or composite layers that replace traditional inorganic silicon interposers within artificial‑intelligence processors. These substrates provide lower dielectric constants, superior thermal conductivity, and flexibility that enable tighter transistor packing and reduced power loss.The expansion is linked to mounting demand for energy‑efficient AI accelerators across cloud‑scale servers and edge‑computing nodes because manufacturers seek higher performance per watt. Moreover, recent collaborations,such as the joint development program announced in March 2024 between a leading semiconductor fab and an advanced materials supplier,are accelerating qualification cycles and lowering entry barriers for new entrants.

MARKET DRIVERS

Performance Demands of Next‑Gen AI Processors

AI workloads that combine deep‑learning inference with real‑time sensor fusion are forcing silicon designers to push clock speeds and channel densities beyond the limits of conventional substrates. Organic substrates deliver the low dielectric loss and fine line resolution required for high‑frequency signaling, which translates into measurable gains in throughput and power efficiency. This technical edge is prompting leading fabless firms to re‑evaluate their material stacks, positioning AI Chip Organic Substrate Market at the core of next‑generation processor roadmaps.

Sustainability Pressures Across the Supply Chain

Regulatory bodies and corporate ESG commitments are nudging manufacturers toward greener alternatives. Compared with traditional epoxy‑based boards, organic substrates generate a smaller carbon footprint during production and enable easier end‑of‑life recycling. The convergence of environmental policy and brand‑reputation concerns is encouraging OEMs to allocate budget for material upgrades, thereby reinforcing demand growth.

➤ “Adopting organic substrates allows designers to shave 15‑20 % off power consumption while meeting the thermal budget of dense AI cores.”

Beyond performance and sustainability, the rollout of 5G and edge‑computing infrastructure is expanding the geographic footprint of AI accelerators. Deployments in telecom hubs and autonomous‑vehicle testbeds require compact, high‑reliability boards,attributes that organic substrates naturally provide. Consequently, multiple market participants are accelerating R&D pipelines to capture this emerging application space.

MARKET CHALLENGES

Cost Sensitivity in High‑Volume Production

While organic substrates excel in performance, their raw material and processing expenses exceed those of conventional FR‑4 laminates. For manufacturers operating on razor‑thin margins, the incremental cost must be justified by a clear return on investment. This financial calculus often delays adoption, especially in segments where price elasticity remains high.

Other Challenges

Manufacturing Yield Consistency

Achieving repeatable etch depths and layer uniformity on organic films requires tighter process controls. Variability in yield can erode profitability and deter early‑stage pilots from scaling up.

MARKET RESTRAINTS

Limited Supplier Base

The ecosystem of qualified organic substrate manufacturers is concentrated in a few regions, creating bottlenecks when large orders surge. This geographic concentration amplifies exposure to trade restrictions and logistics disruptions, thereby restraining broader market expansion.

MARKET OPPORTUNITIES

Customization for Edge‑AI Devices

Edge deployments demand substrates that can be tailored for specific form‑factor constraints, electromagnetic shielding, and thermal management. Companies that develop modular organic substrate platforms stand to capture a niche yet rapidly expanding segment, leveraging design flexibility as a competitive differentiator.

Strategic Partnerships with Foundries

Collaborations between substrate producers and advanced silicon foundries can streamline qualification cycles, reduce time‑to‑market, and lower engineering overhead. Such alliances are poised to unlock new revenue streams for both parties while mitigating the cost and risk barriers identified earlier.

AI Chip Organic Substrate Market Trends

Rising Demand for Energy‑Efficient AI Accelerators

AI Chip Organic Substrate Market is moving beyond niche applications as cloud operators and edge providers prioritize power‑aware performance. The polymer‑based interposer technology reduces dielectric constant and improves heat dispersion, allowing transistor densities to climb without a proportional rise in power draw. This engineering advantage translates into lower total cost of ownership for data‑center owners who face tightening electricity budgets. Recent financial disclosures indicate that the market reached USD 0.85 billion in 2025, climbed to USD 0.92 billion in 2026, and is slated to hit USD 1.45 billion by 2034, reflecting an average annual increase of roughly six percent. The trajectory is anchored in the need for processors that can sustain higher inference workloads while preserving efficiency margins.

Other Trends

Material Innovation and Thermal Management

Manufacturers are experimenting with nanocomposite blends that incorporate graphene or boron nitride fillers. These additives raise thermal conductivity by up to 30 % compared with conventional polymers, which directly mitigates hotspot formation in high‑frequency AI cores. The shift is supported by joint development programs announced in early 2024, where a leading fab partnered with an advanced materials supplier to qualify new substrate formulations under automotive‑grade reliability standards. By shortening the qualification timeline, the collaboration lowers entry barriers for smaller chip designers and widens the supply chain, encouraging broader adoption across diverse device categories.

Supply‑Chain Consolidation and Cost Pressure

While demand expands, the upstream ecosystem faces pressure to rationalize raw‑material sourcing. Silicon‑free substrates rely on specialty resins that historically required multiple vendors, creating price volatility. Recent consolidation among polymer producers has introduced larger volume contracts, which dampen price swings and enable more predictable budgeting for chip manufacturers. This emerging stability invites legacy semiconductor firms to evaluate a transition from silicon interposers, as the total material cost differential narrows. Consequently, AI Chip Organic Substrate Market is likely to see a gradual shift in procurement strategies, with broader participation from both established and emerging players seeking to capture efficiency gains without sacrificing cost discipline.

COMPETITIVE LANDSCAPE

Key Industry Players

AI Chip Organic Substrate Market – Competitive Overview

The sector is anchored by a handful of integrated circuit foundries that have translated their silicon‑on‑insulator expertise into polymer‑based interposers. TSMC leverages its advanced packaging platform to qualify high‑frequency organic substrates for AI accelerators, positioning the company as the de‑facto benchmark for performance‑per‑watt metrics. Samsung Electronics follows a similar trajectory, coupling its memory‑centric fabs with a dedicated materials R&D hub that accelerates throughput for edge devices. Intel’s acquisition of a niche substrate start‑up has allowed it to embed organic layers directly into its Xe‑HPC line, creating a vertical supply chain that narrows time‑to‑market. These three giants together command the majority of wafer‑scale volume, while smaller fabless players rely on their ability to source custom‑engineered films from specialist suppliers.Beyond the dominant fabs, a constellation of materials companies supplies the polymer chemistries, dielectric formulations, and thermal‑interface films that make organic substrates viable. Murata Manufacturing and JSR Corporation have introduced low‑k epoxy blends that address signal‑integrity concerns in densely packed AI cores. BASF and Solvay contribute high‑conductivity fillers that mitigate heat buildup without compromising flexibility. Nitto Denko and 3M focus on adhesive technologies that simplify stack‑up assembly, while Xperi and SK Hynix invest in joint development programs to align substrate specifications with next‑generation AI chip architectures. The collaborative ecosystem shortens qualification cycles and creates entry points for emerging innovators seeking to differentiate through substrate engineering.

List of Key AI Chip Organic Substrate Companies Profiled

- TSMC

- Samsung Electronics

- Intel Corporation

- Murata Manufacturing

- JSR Corporation

- BASF SE

- Solvay SA

- Nitto Denko Corporation

- 3M Company

- Xperi Holding Corp.

- SK Hynix Inc.

- Foundries Inc.

- Applied Materials, Inc.

- ASM International NV

- Lam Research Corporation

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Polymer‑based substrates

|

| By Application |

|

Cloud data‑center accelerators

|

| By End User |

|

Semiconductor manufacturers

|

| By Integration Approach |

|

Direct wafer bonding

|

| By Performance Requirement |

|

High‑performance AI training

|

Regional Analysis: AI Chip Organic Substrate Market

Private equity and corporate R&D budgets are converging on organic substrate platforms, attracted by the prospect of differentiating product lines. Recent funding rounds demonstrate confidence in the technology’s ability to unlock cost efficiencies for AI chip manufacturers.

The supply chain benefits from proximity to established silicon fabs, yet faces bottlenecks in specialty polymer sourcing. Companies are mitigating risk through dual‑sourcing agreements with both domestic and Canadian suppliers.

Federal initiatives on advanced manufacturing incentives and export‑control clarity provide a relatively stable policy backdrop, encouraging long‑term capital commitments to substrate R&D facilities.

End‑users in data‑center and edge‑computing segments prioritize thermal efficiency and form‑factor reduction, driving demand for organic substrate solutions that align with low‑power AI workloads.

Europe

European firms are capitalising on coordinated research programmes funded by the EU Horizon agenda, which emphasise sustainable materials for AI hardware. Nations such as Germany and the Netherlands host niche players that specialise in low‑temperature curing processes, aligning with the continent’s environmental standards. While the market size lags behind North America, a steady influx of cross‑border collaborations is fostering a knowledge base that could translate into niche advantages in automotive and medical AI applications.

Asia-Pacific

The Asia‑Pacific region exhibits a rapid translation of prototype substrates into volume production, spurred by massive demand from smartphone and IoT device manufacturers. China’s state‑backed semiconductor initiatives and Taiwan’s established foundry network create a fertile ecosystem, though intellectual‑property concerns temper some foreign investment. The region’s emphasis on cost‑effective scaling tends to drive organic substrate designs that balance performance with manufacturability, positioning it as a pragmatic growth engine for AI Chip Organic Substrate Market.

South America

South American activity remains modest, yet Brazil’s emerging semiconductor parks are attracting early‑stage ventures focused on flexible organic substrates for agricultural drones and remote‑sensing platforms. Government incentives aimed at diversifying the technology portfolio are encouraging pilot projects, though limited access to high‑precision equipment constrains rapid scaling.

Middle East & Africa

In the Middle East & Africa, the market is in its nascent phase, with the United Arab Emirates establishing a research hub that explores organic material resilience under extreme temperatures. African nations are primarily consumers, importing substrates for niche AI research facilities. The primary challenge lies in building a local supply chain, but strategic partnerships with Asian manufacturers hint at incremental progress.

Report Scope

This market research report provides a comprehensive analysis of the AI Chip Organic Substrate Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI Chip Organic Substrate Market?

-> AI Chip Organic Substrate Market was valued at USD 0.85 billion in 2025 and is expected to reach USD 1.45 billion by 2034, reflecting a compound annual growth rate of approximately 6 % over the forecast horizon.

Which key companies operate in AI Chip Organic Substrate Market?

-> Key players are not disclosed in the provided reference material.

What are the key growth drivers?

-> Key growth drivers include rising demand for energy‑efficient AI accelerators in cloud‑scale servers and edge‑computing nodes, and strategic collaborations that accelerate qualification cycles and lower market entry barriers.

Which region dominates the market?

-> Regional dominance is not specified in the referenced data.

What are the emerging trends?

-> Emerging trends comprise joint development programs between semiconductor fabs and advanced material suppliers, driving faster adoption of organic substrates in AI processors.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...