AI-Based Radar Processor Market Insights

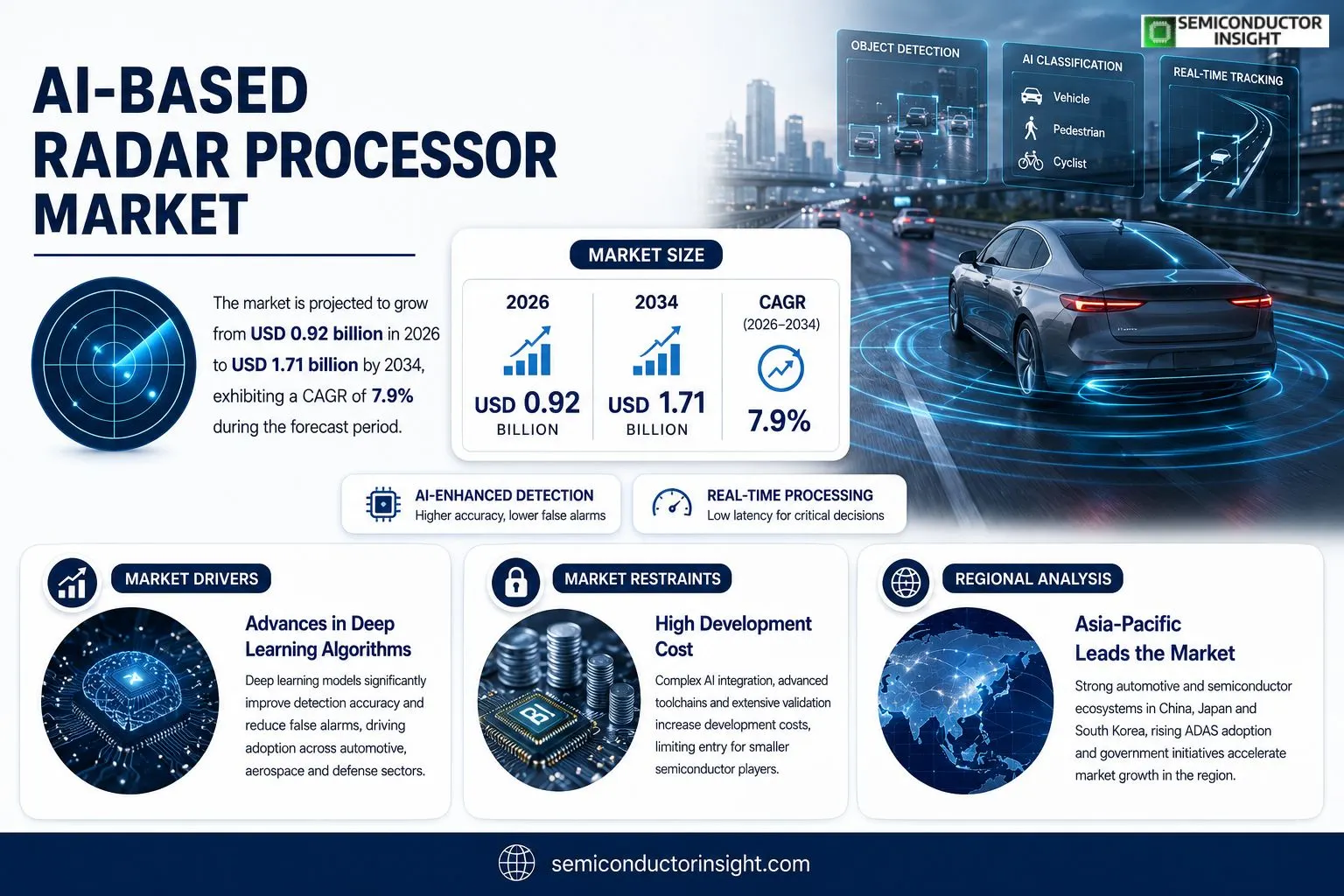

AI-Based Radar Processor market size was valued at USD 0.84 billion in 2025. The market is projected to grow from USD 0.92 billion in 2026 to USD 1.71 billion by 2034, exhibiting a CAGR of 7.9% during the forecast period.

AI‑Based Radar Processors are specialized semiconductor solutions that embed machine‑learning algorithms directly into radar signal‑processing chains, delivering real‑time object detection, classification and tracking for automotive ADAS, autonomous vehicles, aerospace and security domains. By fusing high‑resolution FMCW front‑ends with neural‑network inference engines, these processors cut latency while boosting detection accuracy under challenging weather conditions.The market accelerates because automotive OEMs allocate substantial budgets toward advanced driver assistance systems and defense agencies fund next‑generation situational awareness platforms. Recent collaborationssuch as NXP Semiconductors partnering with NVIDIA in March 2024 to integrate AI inference cores into its radar chipset suiteand Analog Devices’ launch of the ADAR1000 AI‑radar processor illustrate how leading firms expand their portfolios. As power‑efficient architectures mature and software ecosystems evolve, adoption spreads across multiple sectors.

MARKET DRIVERS

Advances in Deep Learning Algorithms

The infusion of convolutional neural networks and transformer models into radar signal chains has lifted detection precision to levels previously reserved for optical sensors. Manufacturers now claim false‑alarm rates that are an order of magnitude lower, a development that directly fuels demand for newer radar processing platforms across automotive and aerospace sectors. This technical leap aligns tightly with the strategic priorities of AI-Based Radar Processor Market, prompting early‑adopter programs to accelerate.

Rise of Sensor‑Fusion Requirements

Automakers and defense integrators are consolidating radar data with lidar, camera, and inertial measurements to construct a unified perception layer. The need for processors that can reconcile heterogeneous data streams in real time has become a decisive factor in system architecture decisions. Companies that embed AI‑enhanced radar cores are positioned to capture a larger share of the integration budget.

➤ “The value proposition of AI‑enabled radar lies not merely in detection, but in the ability to interpret complex environments without human intervention.”

Consequently, OEMs are reallocating R&D spend toward platforms that support on‑chip learning, edge inference, and over‑the‑air model updates. This reallocation is reshaping vendor relationships and setting a new benchmark for competitive performance in the industry.

MARKET CHALLENGES

Computational Complexity Constraints

AI models that deliver superior accuracy also demand substantial processing horsepower and memory bandwidth. Many legacy radar ASICs lack the parallelism required for real‑time inference, forcing designers to adopt hybrid architectures that add latency and increase bill‑of‑materials costs. This tension between performance and power envelope represents a core obstacle for widespread rollout.

Other Challenges

Regulatory Hurdles

The deployment of autonomous sensing systems in public airspace and on roadways is subject to evolving safety standards. Certification bodies are still defining test protocols for AI‑augmented radar, creating uncertainty for suppliers who must design to criteria that may shift before mass production starts.

MARKET RESTRAINTS

High Development Cost

Engineering a radar processor that can host deep neural networks while satisfying automotive-grade reliability incurs sizable upfront investment. Toolchain licensing, silicon prototyping, and extensive validation campaigns collectively push entry barriers higher than for conventional DSP‑based solutions, limiting participation to firms with deep cash reserves.

MARKET OPPORTUNITIES

Emerging Defense Contracts

National security agencies are commissioning next‑generation air‑defense radars that require AI‑driven threat classification and clutter suppression. These programs allocate multi‑year budgets toward processors capable of on‑board learning, presenting a lucrative avenue for vendors that can certify their silicon under stringent military standards. The synergy between defense spend and commercial technology transfer is poised to expand the addressable market for AI‑based radar solutions.

AI-Based Radar Processor Market Trends

Integration of AI Inference Cores into Radar Chipsets

The recent partnership between NXP Semiconductors and NVIDIA, announced in March 2024, illustrates a decisive shift toward embedding machine‑learning accelerators directly within radar front‑ends. By marrying NVIDIA’s AI inference cores with NXP’s FMCW radar suite, OEMs can now achieve sub‑millisecond latency while preserving the high‑resolution range‑Doppler maps required for advanced driver‑assistance systems. This technical convergence matters because the latency envelope has long constrained real‑time object classification, especially in adverse weather where conventional radar returns become noisy. The combined solution not only trims processing delay but also leverages on‑chip neural‑network inference to distinguish pedestrians from cyclists with greater confidence, a capability that directly influences safety certifications and consumer acceptance of autonomous features. In the defense arena, the same architecture streamlines situational‑awareness pipelines, allowing platforms to fuse radar data with visual and infrared feeds without overwhelming onboard compute budgets.

Other Trends

Power‑Efficient Architectures Expanding Adoption

Analog Devices’ launch of the ADAR1000 AI‑radar processor underscores a parallel trend toward ultra‑low‑power designs. The chip delivers comparable neural‑network throughput to larger counterparts while drawing less than half the power, a critical metric for electric vehicles whose range budgets are already tight. Power‑efficiency also eases thermal management in aerospace payloads, where cooling mass directly impacts launch costs. As semiconductor processes advance to sub‑5 nm nodes, the AI‑Based Radar Processor Market witnesses a cascade of offerings that balance computational depth with energy constraints, encouraging OEMs to replace legacy analog pipelines with fully digital, AI‑enabled stacks.

Cross‑Sector Ecosystem Consolidation

Beyond hardware, the market is reshaping its software landscape. Open‑source perception frameworks, once confined to autonomous‑driving labs, are now being adapted for maritime patrol and perimeter security applications. This convergence creates a shared development pool, reducing time‑to‑market for niche players and enabling larger firms to monetize firmware updates as recurring revenue streams. For investors, the implication is clear: companies that nurture a robust SDK and foster third‑party integration stand to capture a disproportionate share of future demand, as end‑users across automotive, aerospace, and security sectors seek turnkey solutions that can be rapidly customized to mission‑specific threat models. Consequently, strategic alliances and joint‑development programs are likely to dominate the next investment cycle within the AI‑Based Radar Processor Market.

COMPETITIVE LANDSCAPE

Key Industry Players

Competitive dynamics in the AI‑Based Radar Processor market

The field is anchored by a handful of semiconductor powerhouses that have woven artificial‑intelligence capabilities into traditional radar front‑ends. NXP Semiconductors, bolstered by its 2024 alliance with NVIDIA, has leveraged AI inference cores to deliver a family of radar chipsets that marry low‑latency processing with high‑resolution detection, positioning it as a go‑to supplier for tier‑one automotive OEMs. Analog Devices follows closely, expanding its ADAR series to include native neural‑network blocks that appeal to defense integrators seeking compact situational‑awareness modules. Texas Instruments, with its long‑standing analog expertise, has introduced a mixed‑signal AI radar processor that narrows the power envelope, a critical factor for electric‑vehicle platforms. Across these leaders, a common structural trait is the convergence of silicon‑level AI accelerators with established radar IP, enabling customers to source a single component rather than stitching together disparate processors and MCU logic.Beyond the marquee names, a cohort of niche innovators is shaping the market’s breadth. Infineon Technologies and STMicroelectronics have each launched AI‑enhanced radar modules aimed at mid‑range ADAS applications, where cost efficiency outweighs extreme performance. Qualcomm is repurposing its mobile‑AI GPUs for automotive radar, betting on its software ecosystem to attract OEMs looking for rapid integration. European suppliers Bosch and Continental are embedding AI radar in their sensor suites to complement lidar and camera arrays, while Hella and Skyworks Solutions provide specialty RF front‑ends that feed AI‑ready data pipelines to larger system integrators. The diversity of these participants reflects a strategy of vertical specializationsome concentrate on power‑critical automotive segments, others on high‑end aerospace or security, creating a layered competitive environment where partnerships and ecosystem alignment often dictate market share.

List of Key AI‑Based Radar Processor Companies Profiled

- NXP Semiconductors

- NVIDIA

- Analog Devices

- Texas Instruments

- Infineon Technologies

- Qualcomm

- STMicroelectronics

- Intel (Mobileye)

- Bosch

- Continental

- Hella

- Skyworks Solutions

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

DSP‑Centric AI Radar

|

| By Application |

|

Advanced Driver‑Assistance Systems (ADAS)

|

| By End User |

|

Automotive OEMs

|

| By Technology |

|

Neural‑Network‑Accelerated FMCW Radar

|

| By Deployment Scenario |

|

Vehicle‑Integrated Radar Modules

|

Regional Analysis: AI-Based Radar Processor Market

North America

The Department of Defense’s shift toward multi‑mode radar systems mandates processors that can execute AI inference on the edge. Procurement officers now evaluate suppliers on their ability to deliver firmware that updates threat‑recognition models without hardware redesign, accelerating fielded capability cycles.

Tier‑1 manufacturers are integrating AI‑enabled radar processors directly into vehicle electronics architectures, reducing latency between sensor capture and decision making. This integration supports advanced driver‑assist features such as predictive braking and adaptive cruise control in complex urban environments.

Leading OEMs are co‑developing proprietary AI models with processor vendors, ensuring that the silicon is tuned for specific automotive radar signatures. Such partnerships lower development risk and create differentiated safety portfolios for end‑users.

Recent component shortages have prompted manufacturers to diversify silicon sourcing across North American fabs, tightening supply loops and reducing lead times for mission‑critical radar processor shipments.

Europe

European nations benefit from coordinated research initiatives such as the European Defence Fund, which earmarks resources for AI‑augmented radar technologies. German automotive firms, in particular, prioritize modular processor designs that can be re‑used across multiple vehicle platforms, fostering economies of scale. Meanwhile, the United Kingdom’s focus on unmanned aerial systems drives demand for lightweight processors capable of on‑board learning, encouraging collaborations between defense contractors and AI startups. Regulatory frameworks around data privacy also shape processor architectures, compelling vendors to embed privacy‑preserving inference mechanisms within the radar pipeline.

Asia‑Pacific

Rapid expansion of smart city projects and autonomous public transport in China, Japan, and South Korea fuels interest in AI‑based radar processors that can handle dense traffic scenarios. Governments are issuing subsidies for domestic semiconductor production, which accelerates the rollout of locally fabricated AI chips. Competitive pressure among regional OEMs results in aggressive road‑mapping that targets full sensor‑fusion solutions, pushing processor vendors to deliver higher throughput while maintaining power efficiency for electric‑vehicle platforms.

South America

In Brazil and Argentina, emerging defense modernization programs are beginning to replace legacy radars with AI‑enhanced processors that can adapt to diverse terrain. Although market size remains modest, the region’s growing aerospace manufacturing sector encourages partnerships with North American firms to transfer technology. Automotive markets, still in early adoption phases, view AI radar processors as a differentiator for premium vehicle segments, prompting import‑focused strategies that rely on established distribution channels.

Middle East & Africa

The Middle East’s strategic emphasis on advanced air‑defense capabilities stimulates procurement of AI‑driven radar processors capable of operating in extreme temperature ranges. Collaborative trials between local defense ministries and multinational chip makers aim to validate AI models that detect low‑observable threats. In Africa, pilot projects for autonomous mining equipment highlight the need for cost‑effective radar processors that can operate on limited power supplies, prompting interest in low‑power AI inference cores that balance performance with affordability.

Report Scope

This market research report provides a comprehensive analysis of the AI-Based Radar Processor Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI-Based Radar Processor Market?

-> AI-Based Radar Processor Market was valued at USD 0.84 billion in 2025 and is expected to reach USD 1.71 billion by 2034, exhibiting a CAGR of 7.9% over the forecast period.

Which key companies operate in AI-Based Radar Processor Market?

-> Key players include NXP Semiconductors, NVIDIA, Analog Devices, Texas Instruments, Infineon Technologies, and STMicroelectronics, among others.

What are the key growth drivers?

-> Key growth drivers include increasing adoption of advanced driver‑assistance systems (ADAS) and autonomous vehicle platforms, rising defense spending on situational‑awareness radar, demand for high‑resolution and low‑latency sensing, and the convergence of AI inference with radar signal processing.

Which region dominates the market?

-> Asia-Pacific dominates the market, driven by strong automotive and semiconductor ecosystems in China, Japan, and South Korea, while North America remains a significant secondary hub.

What are the emerging trends?

-> Emerging trends include integration of AI inference engines directly on radar chips, development of chiplet‑based heterogeneous architectures, software‑defined radar platforms, and multi‑function sensors that combine radar with lidar and camera data for sensor‑fusion applications.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...