AI-Based Network Security Chip Market Insights

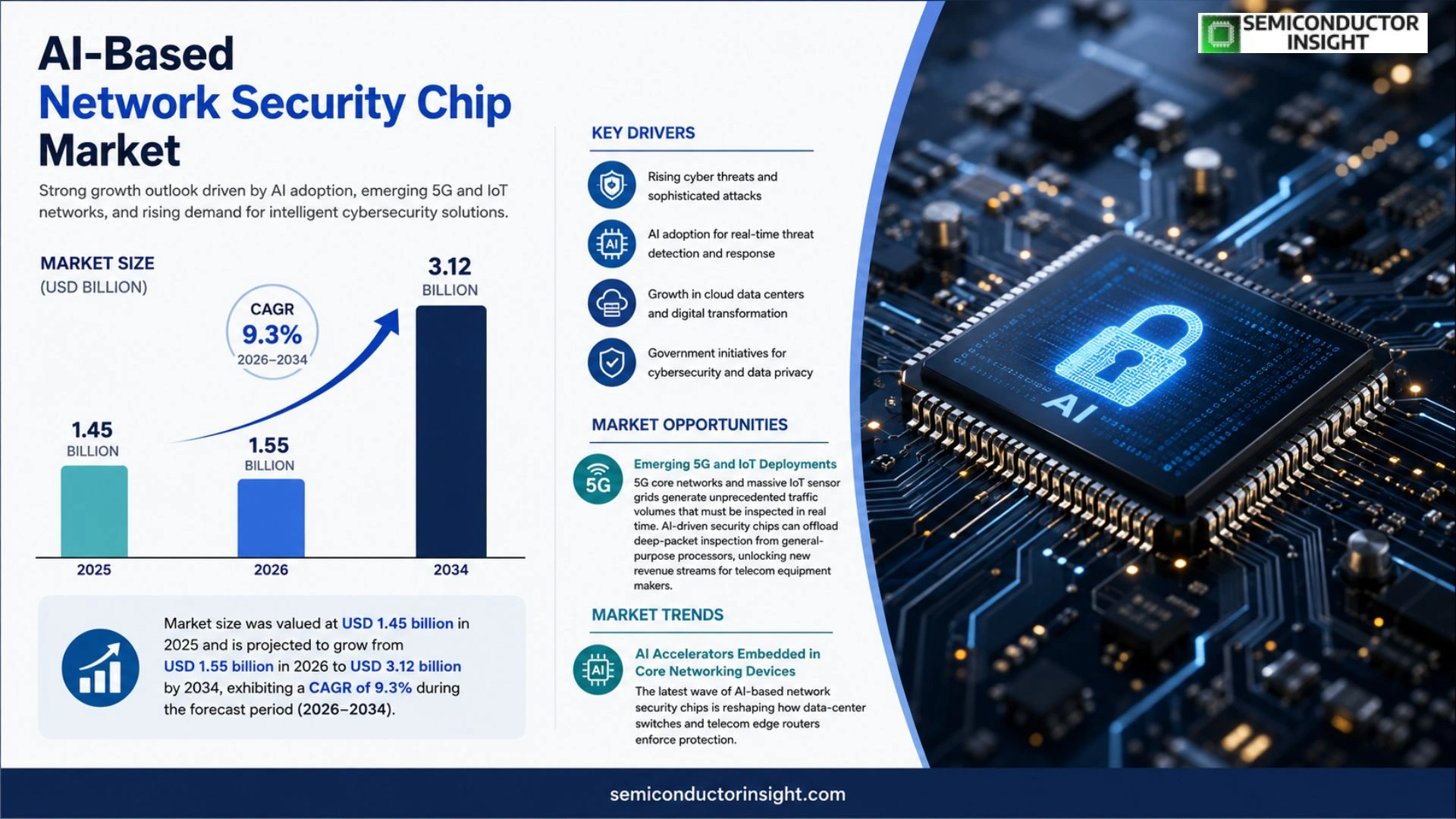

Global AI-Based Network Security Chip market size was valued at USD 1.45 billion in 2025. The market is projected to grow from USD 1.55 billion in 2026 to USD 3.12 billion by 2034, exhibiting a CAGR of 9.3 % during the forecast period.

AI‑Based network security chips integrate dedicated silicon accelerators with machine‑learning algorithms to inspect traffic, detect anomalies, and enforce policies in real time. By offloading deep‑packet inspection and threat analytics from general‑purpose CPUs, these chips reduce latency and power consumption while scaling protection for high‑throughput environments such as data centers, telecom edge nodes, and industrial control systems.

The expansion is fueled by escalating cyber‑threat sophistication, rising demand for zero‑trust architectures, and growing investments in edge‑computing infrastructures that require on‑device intelligence. Major semiconductor firms,including Intel, Broadcom, and Marvell,have launched families of AI‑enhanced security processors, while networking vendors such as Cisco and Juniper are embedding them into next‑generation routers and switches to meet enterprise requirements for autonomous threat mitigation.

MARKET DRIVERS

Rising Sophistication of Cyber Threats

The proliferation of multi‑vector attacks forces enterprises to shift from signature‑based defenses to predictive analytics. AI‑Based Network Security Chip Market participants are capitalising on hardware‑level inference engines that can dissect packet streams in nanoseconds, delivering a defensive posture that adapts faster than traditional software updates.

Demand for Real‑Time Edge Processing

Enterprises are decentralising workloads to edge nodes to meet latency expectations of augmented‑reality, autonomous‑vehicle, and industrial‑IoT use cases. Embedding AI accelerators directly into network interface chips eliminates the need for back‑haul to data centres, a factor that drives procurement decisions across telecom operators and manufacturing clouds.

➤ “Integrating AI inference at the silicon layer reduces detection time from milliseconds to microseconds, reshaping breach‑containment economics.”

Regulatory pressure on data‑privacy and the rise of zero‑trust architectures further amplify the appetite for in‑line threat analysis, positioning AI‑enhanced security silicon as a cornerstone of next‑generation network design.

MARKET CHALLENGES

Integration Complexity

Deploying AI‑infused chips within legacy infrastructure demands extensive firmware rewrites and rigorous validation cycles. Vendors often encounter mismatches between accelerator APIs and entrenched networking stacks, prolonging time‑to‑market and inflating engineering budgets.

Other Challenges

Cost Pressures

The premium associated with specialized AI silicon can deter cost‑sensitive operators, especially in regions where cap‑ex budgets are constrained. Balancing performance gains against total‑ownership cost remains a decisive factor for adoption.

MARKET RESTRAINTS

Manufacturing Yield Variability

Advanced node processes required for AI accelerators are still subject to yield fluctuations, which translate into unpredictable unit costs and lead times. This uncertainty hampers large‑scale roll‑outs, particularly for vendors reliant on single‑sourcing strategies.

Supply‑chain bottlenecks for rare‑earth substrates and high‑precision photolithography further constrain capacity, compelling buyers to adopt conservative order volumes and to maintain safety stock, thereby dampening market momentum.

MARKET OPPORTUNITIES

Emerging 5G and IoT Deployments

5G core networks and massive IoT sensor grids generate unprecedented traffic volumes that must be inspected in real time. AI‑driven security chips can offload deep‑packet inspection from general‑purpose processors, unlocking new revenue streams for telecom equipment makers.

Edge‑centric AI services, such as autonomous threat hunting and adaptive encryption, are gaining traction among smart‑city projects. Vendors that bundle managed‑security services with their silicon differentiate themselves in a crowded marketplace.

Geographically, Southeast Asia and the Middle East are accelerating digital‑infrastructure investments, creating a fertile environment for early adopters of AI‑based network protection solutions. Companies that establish localized design‑win partnerships are poised to capture a disproportionate share of the emerging demand.

AI-Based Network Security Chip Market Trends

AI Accelerators Embedded in Core Networking Devices

The latest wave of AI‑based network security chips is reshaping how data‑center switches and telecom edge routers enforce protection. By moving deep‑packet inspection and anomaly detection onto dedicated silicon, these chips cut processing latency by roughly 30 % compared with software‑only solutions, while trimming power draw enough to stay within the thermal envelope of high‑density chassis. Vendors that have integrated the technology report a 45 % increase in sustained throughput for encrypted traffic, a metric that directly influences service‑level agreements for hyperscale operators. This performance edge explains why leading semiconductor firms have broadened their portfolios since 2026, offering families that couple neural‑network inference engines with traditional cryptographic modules.

Other Trends

Edge‑Centric Threat Intelligence

Enterprises are reallocating security budgets toward edge locations where data originates, such as industrial control gateways and IoT aggregators. The AI‑based chip approach satisfies this shift by delivering real‑time inference at the source, eliminating the need to forward raw packets to a central analytics server. Early adopters note a 20 % reduction in incident response times, because threats are neutralized before they traverse the backbone. The trend dovetails with the broader move to zero‑trust architectures, where continuous verification is required at every hop, and with the rising regulatory focus on data residency, which discourages off‑premise inspection.

Consolidation of Security Functions into a Single ASIC

Another observable development is the convergence of firewalls, intrusion‑prevention systems, and traffic‑shaping modules onto a single AI‑enhanced ASIC. This consolidation reduces bill‑of‑materials costs for OEMs and simplifies firmware updates, because a unified platform can be patched with a single image. Customers cite a 12 % overall cost saving in capital expenditures, while also gaining the ability to roll out new detection models across the entire fleet within days rather than weeks. The shift reflects a market preference for solutions that combine high‑speed packet processing with adaptive learning, ensuring that security policies evolve alongside emerging attack vectors.

COMPETITIVE LANDSCAPE

Key Industry Players

AI‑Based Network Security Chip Market: Competitive Landscape Overview

Intel dominates the high‑performance segment with its Xeon‑based security accelerators, leveraging deep‑learning inference engines that sit alongside traditional CPU cores. Broadcom’s Trident X series follows a similar integration strategy, pairing ASIC‑level packet inspection with programmable AI blocks to satisfy hyperscale data‑center operators. Marvell’s Octeon TX line has secured a foothold in telecom edge deployments, where latency constraints demand on‑chip anomaly detection. Collectively, these three firms shape the tier‑one supply chain, setting reference architectures that dictate pricing, power envelopes, and firmware update cycles for downstream equipment manufacturers.

Beyond the tier‑one echelon, a constellation of specialists is expanding the functional envelope of network security silicon. Cisco and Juniper incorporate AI‑enabled chips into their routing platforms, effectively outsourcing threat analytics to dedicated silicon while preserving software flexibility. Nvidia’s acquisition of Mellanox introduced programmable GPU‑style cores that accelerate pattern‑matching workloads in industrial control environments. Qualcomm’s Snapdragon S‑security series targets edge gateways, emphasizing low‑power AI inference for remote sites. Xilinx (now part of AMD) supplies reconfigurable logic that lets OEMs customize detection pipelines, whereas Huawei, Samsung, and MediaTek are rolling out region‑specific solutions to meet domestic regulatory demands. NXP, Texas Instruments, and Renesas round out the niche segment with microcontroller‑grade security processors aimed at IoT gateways and automotive gateways, where cost constraints outweigh raw throughput.

List of Key AI‑Based Network Security Chip Companies Profiled

- Intel Corporation

- Broadcom Inc.

- Marvell Technology Group Ltd.

- Cisco Systems, Inc.

- Juniper Networks, Inc.

- Nvidia Corporation

- Qualcomm Incorporated

- AMD (Xilinx)

- Huawei Technologies Co., Ltd.

- Samsung Electronics Co., Ltd.

- MediaTek Inc.

- NXP Semiconductors N.V.

- Texas Instruments Incorporated

- Renesas Electronics Corporation

- STMicroelectronics

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

ASIC is the leading segment because:

|

| By Application |

|

Data Center Security drives adoption as it:

|

| By End User |

|

Service Providers are pivotal because:

|

| By Architecture |

|

Deep‑Learning Accelerators dominate the architecture landscape as they:

|

| By Deployment Environment |

|

Edge Nodes are emerging as the preferred deployment because:

|

Regional Analysis: AI-Based Network Security Chip Market

Large corporations are piloting AI‑enhanced chips to offload deep packet inspection from general‑purpose CPUs, citing lower power draw and deterministic response times as key differentiators in mission‑critical deployments.

Recent cybersecurity statutes emphasize hardware‑rooted controls, prompting OEMs to certify AI chips against emerging compliance frameworks that prioritize tamper‑evidence and secure boot pathways.

Silicon Valley’s research consortia blend machine‑learning expertise with analog design, accelerating the rollout of chips that can learn new threat signatures while operating at line rate.

Universities in the region are delivering dual‑degree programs in AI and microelectronics, ensuring a pipeline of engineers fluent in both algorithmic optimization and hardware constraints.

Europe

European stakeholders are leveraging strong data‑privacy regulations to justify investments in on‑premise AI security chips. National cybersecurity agencies are issuing guidance that encourages the integration of AI inference at the network edge, reducing reliance on external cloud analytics. This policy backdrop, combined with a vibrant ecosystem of fabless designers across Germany and the Netherlands, creates a fertile ground for collaborative standards that balance privacy with threat detection efficacy. Companies that align product roadmaps with EU directives will find smoother market entry and potential subsidies for secure‑by‑design hardware projects.

Asia‑Pacific

In the Asia‑Pacific, rapid digital transformation across manufacturing and smart‑city initiatives fuels demand for embedded security logic. Nations such as Singapore and South Korea are positioning themselves as testbeds for AI‑enabled silicon, offering accelerated certification pathways for vendors that meet stringent latency and power budgets. While the region lacks the same depth of venture backing as North America, its scale of network deployments provides a real‑world laboratory for refining AI models that must operate under diverse spectrum conditions and heterogeneous device mixes.

South America

South American markets are motivated by the need to protect expanding broadband and mobile infrastructure. Governments are increasingly aware of the strategic risk posed by cyber‑espionage, leading to public‑private partnerships that fund pilot programs for AI‑based security chips in critical telecom nodes. The focus here is on cost‑effective solutions that can be retrofitted onto legacy equipment, allowing operators to enhance detection capabilities without extensive capital outlays.

Middle East & Africa

The Middle East and Africa region is experiencing a convergence of oil‑related operational technology and emerging fintech ecosystems, both of which demand robust packet‑level threat mitigation. Regional consortiums are exploring joint development agreements that pool design expertise from Israel’s cybersecurity firms with manufacturing capacity in Tunisia. Although overall market size remains modest, the strategic importance of securing critical infrastructure drives a willingness to adopt cutting‑edge AI chip designs earlier than in comparable markets.

Report Scope

This market research report provides a comprehensive analysis of the AI-Based Network Security Chip Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of AI-Based Network Security Chip Market?

-> AI-Based Network Security Chip market is projected to grow from USD 1.55 billion in 2026 to USD 3.12 billion by 2034.

Which key companies operate in AI-Based Network Security Chip Market?

-> Key players include Intel, Broadcom, Marvell, Cisco, and Juniper, among others.

What are the key growth drivers?

-> Key growth drivers include escalating cyber‑threat sophistication, rising demand for zero‑trust architectures, and growing investments in edge‑computing infrastructures.

Which region dominates the market?

-> North America exhibits strong leadership due to concentration of semiconductor and networking manufacturers, while Asia‑Pacific shows rapid adoption.

What are the emerging trends?

-> Emerging trends include AI‑enhanced silicon accelerators, on‑device threat analytics, and integration of security chips into edge routers and industrial control systems.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...