Aerospace Components Market Insights

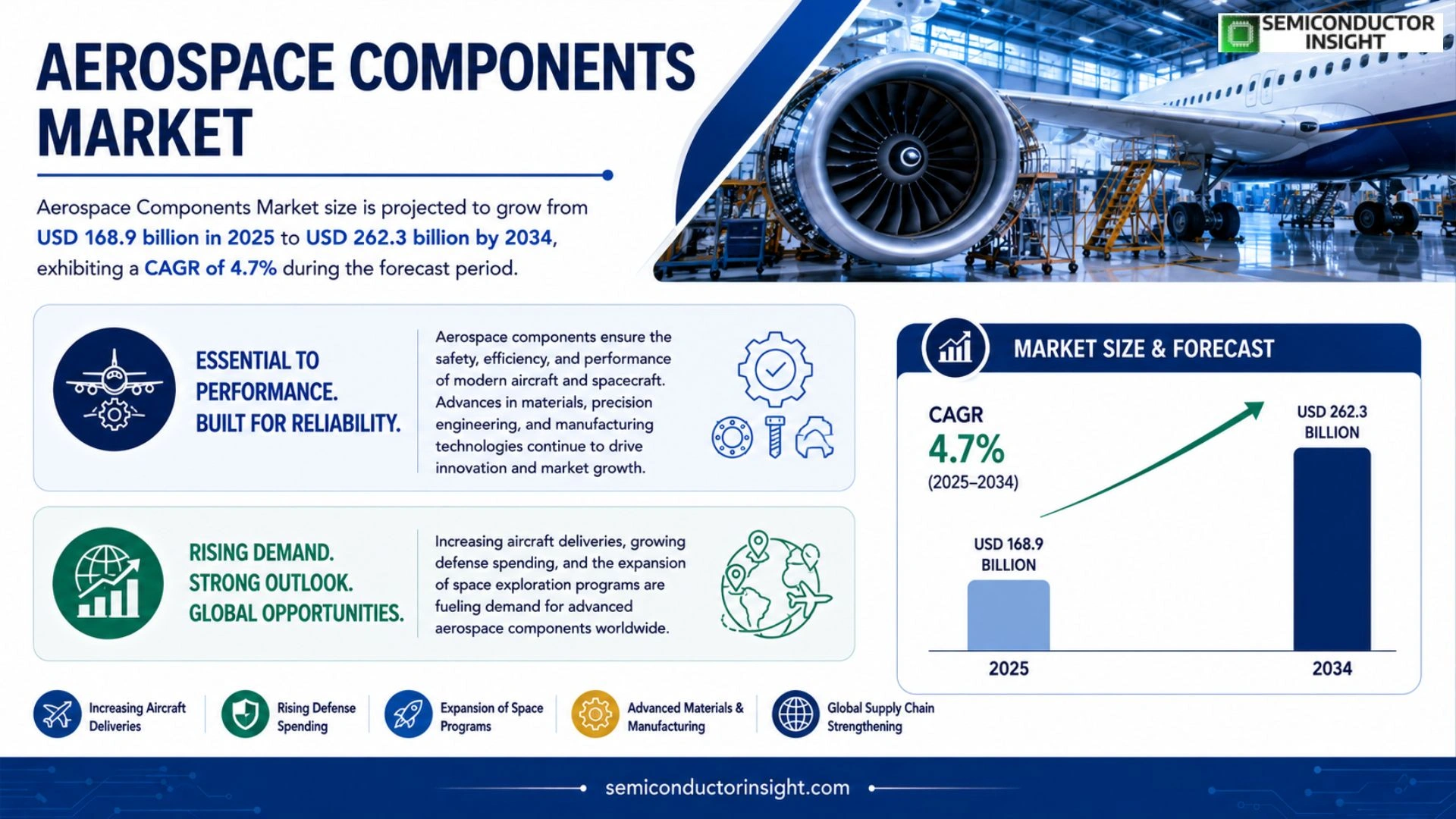

Global Aerospace Components Market size was valued at USD 168.9 billion in 2025. The market is projected to grow from USD 168.9 billion in 2025 to USD 262.3 billion by 2034, exhibiting a CAGR of 4.7% during the forecast period.

Aerospace components encompass a broad range of critical parts used in aircraft, spacecraft and defense platforms, including airframe structures such as wing ribs and fuselage panels, propulsion system elements like turbine blades and combustors, avionics modules, landing‑gear assemblies and fasteners made from advanced alloys or composites. These components are engineered for high strength‑to‑weight ratios, extreme temperature tolerance and stringent safety certifications.

The market is accelerating because airlines are expanding fleets faster than pre‑pandemic levels, while defense spending remains robust amid geopolitical tensions. Furthermore, sustainability mandates are driving adoption of lightweight composites and additive‑manufactured parts that reduce fuel consumption. Key players such as Boeing, Airbus, Safran Group, GE Aviation and Rolls‑Royce are investing heavily in digital twins and supply‑chain digitisation; for example, in March 2024 Airbus announced a strategic partnership with Siemens Digital Industries to scale up additive manufacturing of structural brackets across its production lines.

MARKET DRIVERS

Growing Demand for Lightweight Materials

Aerospace Components Market is being propelled by airlines’ need to reduce fuel consumption. Advances in carbon‑fiber composites and high‑strength alloys enable manufacturers to cut aircraft weight by up to 20%, directly influencing operating costs and environmental targets.

Digitalization and Advanced Manufacturing

Adoption of additive manufacturing, AI‑driven design, and the Internet of Things is shortening product development cycles. Companies that integrate these technologies report up to 30% faster time‑to‑market for critical components.

➤ Industry analysts forecast a 6‑8% CAGR for the sector through 2030, driven by these efficiencies.

Overall, the convergence of weight‑reduction strategies and digital tooling creates a robust growth engine for Aerospace Components Market, reinforcing investment confidence across OEMs and suppliers.

MARKET CHALLENGES

Supply Chain Volatility

Recent geopolitical shifts and pandemic‑related disruptions have exposed the fragility of global supply networks. Shortages of rare‑earth metals and specialty polymers increase lead times and cost volatility for critical components.

Other Challenges

Regulatory Compliance

Stringent certification processes in multiple jurisdictions add layers of testing and documentation, raising engineering overhead and delaying product launches.

Additional pressures arise from fluctuating raw‑material prices, which can erode margins for manufacturers that lack diversified sourcing strategies.

MARKET RESTRAINTS

High Capital Expenditure

Establishing state‑of‑the‑art production lines for aerospace‑grade titanium and composite parts requires multi‑hundred‑million‑dollar investments, limiting entry for smaller players.

Furthermore, the need for specialized tooling and precision equipment intensifies the financial burden, particularly in emerging markets where access to financing remains constrained.

These capital constraints dampen the speed at which new suppliers can scale to meet rising demand, acting as a notable restraint on market expansion.

MARKET OPPORTUNITIES

Expansion into Commercial Spaceflight

The surge in commercial launch services is generating demand for high‑performance propulsion and structural components. Companies that adapt their product portfolios to meet space‑flight specifications stand to capture a fast‑growing niche.

Adoption of additive manufacturing for low‑volume, high‑complexity parts offers a cost‑effective pathway to serve the space sector, reducing material waste and enabling rapid iteration.

Growth in unmanned aerial systems (UAS) also creates a parallel market for lightweight, durable components, expanding the addressable customer base beyond traditional aircraft manufacturers.

Aerospace Components Market Trends

Accelerated Fleet Growth and Defense Investment

Aerospace Components Market is being propelled by a rapid expansion of commercial airline fleets that now surpass pre‑pandemic levels. Airlines are placing large orders for new airframes, which creates immediate demand for structural parts, engine components, and landing‑gear assemblies. At the same time, defense budgets remain strong as governments increase spending on next‑generation aircraft and missile platforms. This dual driver sustains a steady flow of orders for high‑precision components, encouraging manufacturers to scale production while maintaining rigorous safety certifications.

Other Trends

Lightweight Composite Adoption

Manufacturers are shifting toward advanced composite materials for wing ribs, fuselage panels, and turbine blade casings. These composites deliver higher strength‑to‑weight ratios and improved fuel efficiency, aligning with airlines’ sustainability goals. Additive‑manufacturing techniques, such as metal laser sintering, are increasingly used to produce complex brackets and fasteners, reducing material waste and lead times. The combined effect is a measurable drop in aircraft empty weight, which translates into lower operating costs.

Digital Twin and Supply‑Chain Digitisation

Leading players like Airbus and Boeing are investing heavily in digital‑twin technology to simulate component performance throughout the product lifecycle. By integrating real‑time sensor data, manufacturers can predict wear patterns, optimise maintenance schedules, and minimise unexpected downtime. Parallel efforts focus on supply‑chain transparency, with cloud‑based platforms linking tier‑1 suppliers to original equipment manufacturers. This digital ecosystem accelerates design iterations, shortens time‑to‑market, and enhances overall quality assurance across Aerospace Components Market.

COMPETITIVE LANDSCAPE

Key Industry Players

Aerospace Components Market Competitive Overview 2024‑2034

Aerospace Components Market, valued at USD 168.9 billion in 2025, is projected to reach USD 262.3 billion by 2034, driven by a 4.7 % CAGR. Boeing and Airbus dominate the airframe segment, supplying wing ribs, fuselage panels, and structural brackets to a rapidly expanding airline fleet. Their scale enables deep investment in digital‑twin technology and additive‑manufacturing partnerships, exemplified by Airbus’s collaboration with Siemens Digital Industries in March 2024. In the propulsion arena, GE Aviation and Rolls‑Royce command the turbine‑blade and combustor markets, leveraging advanced nickel‑based superalloys and AI‑enabled predictive maintenance to fortify their market share. The concentration of these four giants creates a tiered supply chain where Tier‑1 manufacturers rely heavily on a handful of OEMs, establishing high entry barriers for new entrants while fostering collaborative innovation across the ecosystem.

Beyond the marquee OEMs, a cohort of niche yet strategically vital players enriches the competitive landscape. Safran Group and Honeywell Aerospace supply high‑performance avionics, landing‑gear assemblies, and fasteners, emphasizing lightweight alloys and composite integration. European firms such as Leonardo and MTU Aero Engines focus on propulsion subsystems for both civilian and defense platforms, while Spirit AeroSystems and BAE Systems specialize in structural sub‑assemblies for wide‑body aircraft. Materials specialists like Hexcel Corp and Solvay drive the adoption of carbon‑fiber composites, responding to sustainability mandates that prioritize fuel‑efficiency. Raytheon Technologies, through its RTX subsidiary, delivers integrated propulsion and engine‑control solutions, reinforcing the importance of cross‑functional expertise. Collectively, these companies nurture a diversified ecosystem that balances scale, technological depth, and specialization, ensuring resilience against supply‑chain disruptions and supporting the market’s sustained growth trajectory.

List of Key Aerospace Companies Profiled

- Boeing

- Airbus

- GE Aviation

- Rolls‑Royce

- Safran Group

- Honeywell Aerospace

- Leonardo

- MTU Aero Engines

- Spirit AeroSystems

- BAE Systems

- Hexcel Corp

- Solvay

- Raytheon Technologies

Segment Analysis:

| Segment Category | Sub-Segments | Key Insights |

| By Type |

|

Airframe Structures

|

| By Application |

|

Commercial Aircraft

|

| By End User |

|

Airlines

|

| By Technology |

|

Additive Manufacturing

|

| By Material |

|

Composite Materials

|

Regional Analysis: North America

United States

The demand for lightweight and high-strength structural components continues to rise, with a notable emphasis on composite materials to improve fuel efficiency. Innovation in manufacturing processes, such as additive manufacturing, is gaining traction for producing complex geometries.

Advancements in avionics, including integrated flight management systems and enhanced navigation technologies, are crucial for improving aircraft safety and operational efficiency. The integration of artificial intelligence and machine learning is further transforming avionics capabilities.

The development of more fuel-efficient and environmentally friendly propulsion systems, encompassing both traditional jet engines and alternative technologies like electric and hybrid propulsion, is a key focus area. Research into sustainable aviation fuels is also gaining momentum.

The burgeoning space sector presents significant opportunities for aerospace component manufacturers, particularly in areas like satellite components, launch vehicle systems, and components for space exploration missions.

Europe

Europe represents a significant market for Aerospace Components, characterized by a strong legacy of aerospace manufacturing and a growing emphasis on technological innovation. Government initiatives promoting collaboration and investment in key technologies are driving market expansion. The region’s focus on sustainability and reducing carbon emissions is influencing the development of more eco-friendly aerospace components. Key players are concentrating on advanced materials, digital manufacturing, and automation to enhance competitiveness. The European Union’s regulatory framework plays a substantial role in shaping market dynamics and fostering standardization across the industry.

Asia-Pacific

Asia-Pacific is emerging as the fastest-growing region withAerospace Components Market, propelled by rapid industrialization, increasing air travel demand, and substantial investments in aerospace infrastructure. China, in particular, is becoming a major manufacturing hub and a significant consumer of aerospace components. The region is witnessing a surge in demand for components across various aircraft types, including commercial airliners, military aircraft, and helicopters. The focus on developing domestic aerospace capabilities and reducing reliance on imports is further fueling market growth. The Asia-Pacific market is characterized by diverse regional dynamics and varying levels of technological sophistication.

South America

South America presents a smaller but steadily growing market for Aerospace Components. The expansion of commercial aviation and the increasing focus on regional connectivity are driving demand. Opportunities exist in the maintenance, repair, and overhaul (MRO) sector, as well as in supporting the growing aerospace manufacturing base in countries like Brazil. The market is susceptible to economic fluctuations and regulatory uncertainties.

Middle East & Africa

The Middle East & Africa region exhibits potential for growth Aerospace Components Market, driven by increasing air travel, defense spending, and infrastructure development projects. The region is witnessing investments in airport expansion, modernization of existing air fleets, and the development of indigenous aerospace capabilities. Demand for components related to defense and security applications is particularly strong. However, geopolitical factors and economic instability can pose challenges to market growth.

Report Scope

This market research report provides a comprehensive analysis of the Aerospace Components Market , covering the forecast period 2026–2034. It offers detailed insights into market dynamics, technological advancements, competitive landscape, and key trends shaping the industry.

Key focus areas of the report include:

- Market Overview: The report begins with an overview outlining its current market scenario, key growth indicators, and industry transformation drivers. It discusses macroeconomic factors, demand–supply balance, regulatory landscape, and the strategic role of semiconductors in powering advancements across industries such as automotive, telecommunications, consumer electronics, and industrial automation.

- Market Size & Forecast: Historical data and future projections for revenue, unit shipments, and market value across major regions and segments.

- Segmentation Analysis: Detailed breakdown by product type, technology, application, and end-user industry to identify high-growth segments and investment opportunities.

- Regional Insights: Insights into market performance across North America, Europe, Asia-Pacific, Latin America, and the Middle East & Africa, including country-level analysis where relevant.

- Competitive Landscape: Profiles of leading market participants, including their product offerings, R&D focus, manufacturing capacity, pricing strategies, and recent developments such as mergers, acquisitions, and partnerships.

- Technology Trends & Innovation: Assessment of emerging technologies, integration of AI/IoT, semiconductor design trends, fabrication techniques, and evolving industry standards.

- Market Drivers & Restraints: Evaluation of factors driving market growth along with challenges, supply chain constraints, regulatory issues, and market-entry barriers.

- Stakeholder Insights: Insights for component suppliers, OEMs, system integrators, investors, and policymakers regarding the evolving ecosystem and strategic opportunities.

Primary and secondary research methods are employed, including interviews with industry experts, data from verified sources, and real-time market intelligence to ensure the accuracy and reliability of the insights presented.

FREQUENTLY ASKED QUESTIONS:

What is the current market size of Aerospace Components Market?

-> Aerospace Components Market size was valued at USD 168.9 billion in 2025. The market is projected to grow from USD 168.9 billion in 2025 to USD 262.3 billion by 2034.

Which key companies operate Aerospace Components Market?

-> Key players include Boeing, Airbus, Safran Group, GE Aviation, and Rolls‑Royce, among others.

What are the key growth drivers?

-> Key growth drivers include airline fleet expansion, sustained defense spending, and sustainability mandates driving lightweight composites and additive‑manufactured parts.

Which region dominates the market?

-> North America holds the largest market share, while Asia‑Pacific is emerging as a fast‑growing region.

What are the emerging trends?

-> Emerging trends include additive manufacturing, digital‑twin technology, and increased use of lightweight composite materials.

Get Sample Report PDF for Exclusive Insights

Report Sample Includes

- Table of Contents

- List of Tables & Figures

- Charts, Research Methodology, and more...